ITRN - Ituran: Strong Fundamentals And Growth Momentum Make The Company A Buy

2023-12-11 11:12:29 ET

Summary

- Ituran has solid financial metrics and growing subscriber growth, making it a good long-term investment with an enticing risk/reward ratio.

- The company has a strong financial position with low debt and a stable current ratio, indicating no liquidity issues.

- Ituran has improved its efficiency and profitability in recent years, with a high return on invested capital and a competitive advantage over its competitors.

Investment Thesis

I wanted to take a look at Ituran's ( ITRN ) financial health to see if the company is a good investment in the long run. The company possesses really solid financial metrics that I deem to be necessary for a good investment in the long run, coupled with growing subscriber growth, ITRN seems to be positioned well for the future, however, not without risks. Nevertheless, I rate the company a buy since I believe the risk/reward is very enticing here.

Briefly on the Company

Ituran is a company that helps its subscribers locate their vehicles at any given time. If your car was stolen, it can track it and help you get it back safely using GPS to track its location. It can also help keep your car safe and will alert you if your car was moved or tampered with. Furthermore, the company can optimize the routes of your fleet and save fuel.

Financials

As of Q3 '23 , the company had around $40m in liquidity, against barely noticeable long-term debt of $263k. This should attract many investors to the company, as many of them try to avoid companies with excess leverage, which I think is fair, but debt is not an issue if the company can manage it correctly. In any case, ITRN is at no risk of insolvency because the debt is very small, which means it is not paying much in annual interest expense. This allows for a lot of flexibility in how the company wants to spend its available capital to increase its value, whether that is through dividends (my least favorite way of rewarding shareholders), share buybacks (if the shares are considered cheap), or reinvesting the available capital into the company, which I think in the end will be the best way of rewarding shareholders in the long run.

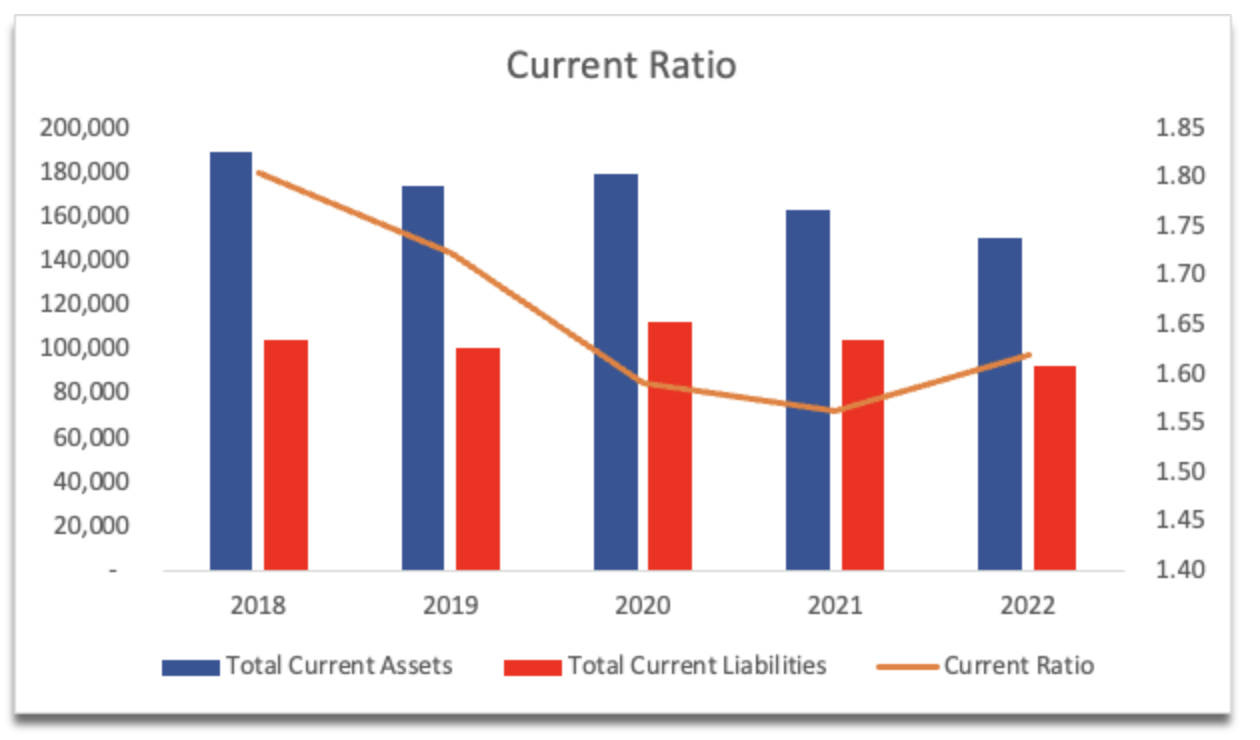

The company's current ratio in the past has been very stable and healthy. This has not changed in the latest quarter, which stood at around 1.9. Over the last few years, the company's current ratio has hovered in that range I consider to be efficient. Which is the range of 1.5 to 2.0. Anything over 2.0, I consider to inefficient use of assets like cash, which could have been used to further the growth of the company. Nevertheless, it is still better to have a strong current ratio than under one. It's safe to say, ITRN has no liquidity issues.

{kind=link}

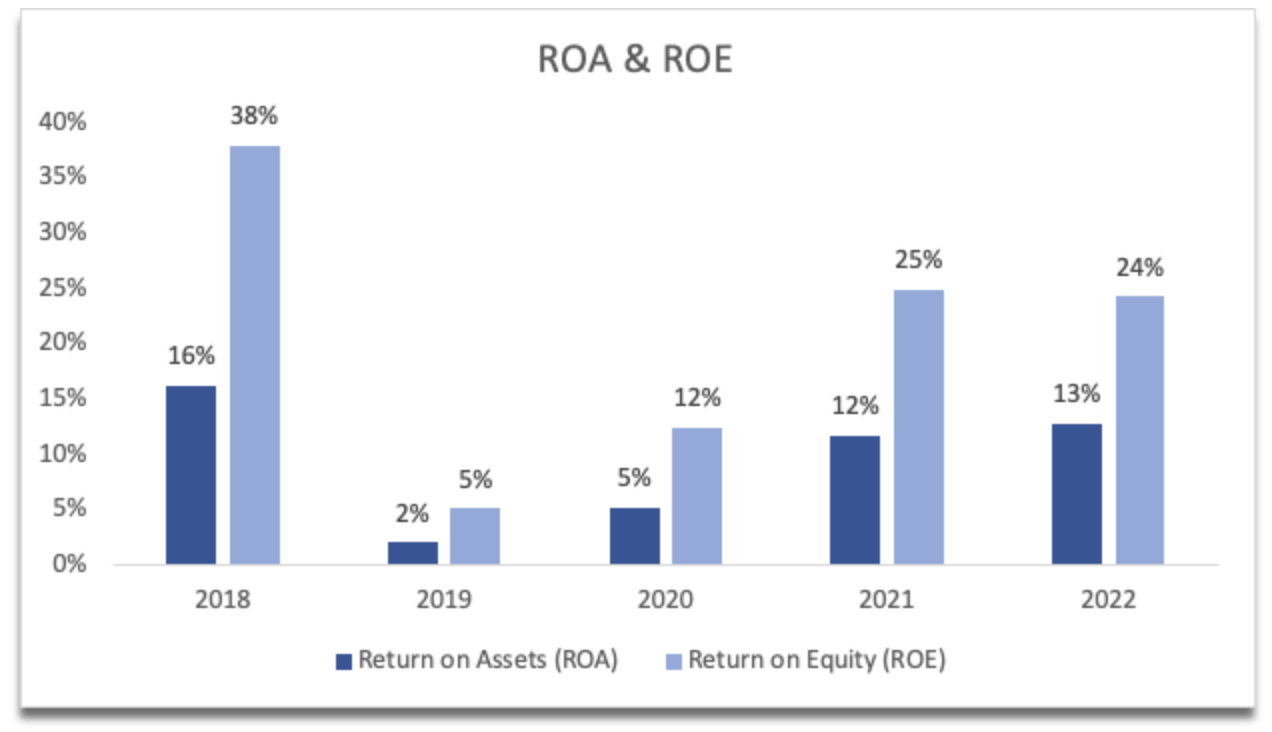

Speaking of efficiency, in the last couple of years, the company's ROA and ROE have improved significantly, which can be attributed to the management's ability to reduce operating expenses while having sales growth, especially in the last two years, when the company saw 10% and 8.2% increase in sales while operating expenses reduced by around 300bps over the same period. The company has become much more efficient in the last couple of years, and that is a good trend to have. I'd like to see the efficiency come back to FY18 levels, and I'm sure it will with time.

{kind=link}

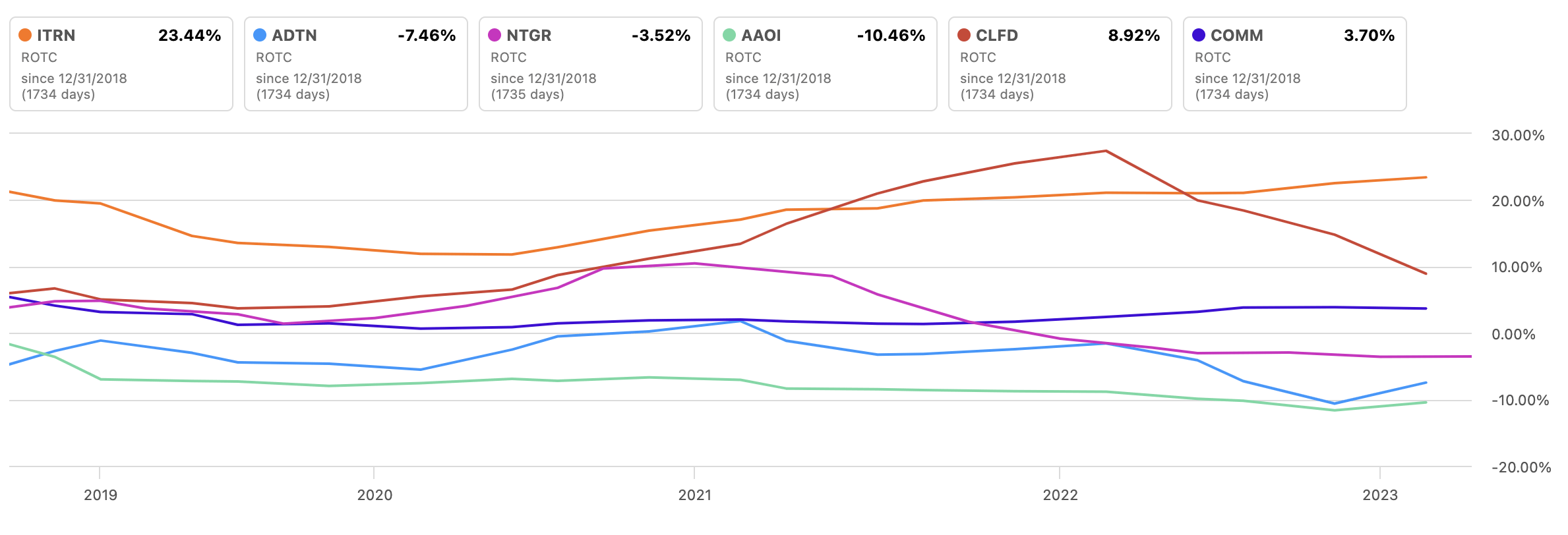

The next metric is what attracted me to this company in the first place. On my stock screener, ITRN displayed a high and growing return on invested capital, which is one of the main metrics that show me how well the management allocates capital to highly profitable projects, and in the last couple of years, the management has done a commendable job. What ROIC also tells me is that the company may have a competitive advantage and a strong moat, which is always a requirement for me. Furthermore, we can look at the company's competition to see how well they're doing relative to ITRN, and we can see the company has a competitive advantage over them. To note one thing, ROTC is slightly different from ROIC, however, seeing that the company has no debt, it should be a close match.

{kind=link}

The reason I like this metric is that research shows that companies with high ROIC tend to perform better overall. History is not an indicator of the future, but I like the odds here if I focus on companies with higher-than-average ROIC.

High ROIC stocks tend to perform better than peers (FactSet)

{kind=link}

Moving on to revenues. ITRN managed around 6% CAGR over the last decade, which isn't very exciting for many investors who look for growth, however, top-line growth is not the only metric to judge a company's worth. Efficiency and profitability are much more important in my opinion, and if a company can grow sales at a reasonable pace AND become more efficient, that's just the icing on the cake. Over the last 3 quarters, the company managed to grow the top line at 10%, 11%, and 12% in Q1, Q2, and Q3, respectively, which double what the company managed in the past. That is encouraging. It seems that the company's products and services are more in demand now.

Revenue Growth (Author)

The company's historic margins have seen worse, and better days. The good thing about them right now is that in the last 9 months of the year, these have improved slightly from FY22. The company continues to improve on efficiency and profitability, and that is the way to drive value and reward patient shareholders in the future.

{kind=link}

Overall, I can see a company that has improved quite drastically since the bottoms in FY19 and FY20. The company also has a very strong competitive advantage with a strong moat, and very capable management, which led to the company's stellar performance in the first place. I wouldn't be surprised to see the company returning to even better profitability in the future, just like the last 9 months suggested. High ROIC demands less of a margin of safety in my opinion, or in other words, I would be willing to pay more for such companies to own in the long run.

Comments on the Outlook

I believe the company will continue to improve over time. The management's ability to continue to improve margins will bode well for the future performance of the company and its share price.

The company has been growing its subscriber count steadily over the last couple of years and if it can continue to grow at such pace, the future for the company is very bright and profitable no doubt. The ability to raise subscription fees while also continuing to add subscribers tells me that the company's service is very valuable, which means people are not afraid to dish out extra.

It seems that in the last 3 quarters, the company has changed quite significantly for the better, with improving margins and double the historical average of top-line growth making the company very attractive if it can maintain such performance going forward.

Valuation

The company isn't very well covered by the Street and the media, which means I will have to come up with some educated guesses for revenue growth and margins. However, I will approach my valuation with a conservative mindset for an extra margin of safety. I don't want to be too optimistic when it comes to valuations. I know that the company managed low-double-digit growth this year, however, I decided to be much more conservative and beat down estimates to make a stress test. Below are my assumptions for the base, conservative, and optimistic cases, and their respective CAGRs.

{kind=link}

For margins and EPS, I decided to improve gross margins by around 200bps over the next decade, which is very small in my opinion, considering the management has done an amazing job during the last 3 quarters already. Below are those assumptions.

{kind=link}

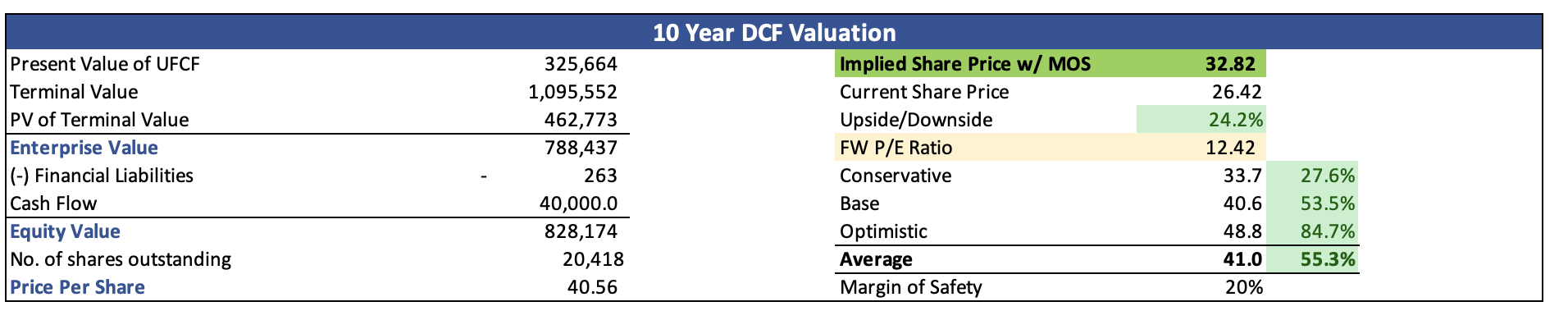

For the DCF analysis, I went with the company's WACC of around 9% as my discount rate and 2.5% as my terminal growth rate. Furthermore, I decided to add another 20% margin of safety to the valuation just to give myself even more room for error. With that said, Ituran's intrinsic value is $32.82 a share, implying the company is trading at a decent discount to its fair value.

{kind=link}

Risks

The company is headquartered in Israel, which means there are a lot of uncertainties regarding the current conflict there. This may bring volatility to the share price, as it has many other companies in the past that had any association with Israel, even if the damage to the operations of the company is minimal. So, far the management has said that the company experienced little to no disruptions, however, they do expect subscriptions in Israel to come in lower next quarter. Almost 50% of revenues come from Israel, so any future changes in conflict may affect the company dramatically.

I would be cautious if the company plateaus and does not continue adding subscribers due to other disruptive technologies that the competitors developed, which started to take market share from ITRN. So far, as we saw in the financials, the company has a lot of competitive advantage, if it continues to come down, I would be very cautious and will dig deeper as to why it is beginning to trend down.

Closing Comments

Even with quite beaten-down estimates, in my opinion, the company is a good deal at these prices. ITRN's fantastic and growing ROIC is one of the main reasons I give the company a buy rating, because that metric is very important to me, and as research shows the companies that have high ROIC tend to perform better overall. The risk/reward is much more enticing when the company has a competitive advantage, therefore I initiate my coverage of the company with a buy rating.

For further details see:

Ituran: Strong Fundamentals And Growth Momentum Make The Company A Buy