CA - Jaguar Mining: A Disappointing Start To The Year

2023-04-15 01:01:28 ET

Summary

- Jaguar Mining was one of the worst performing gold producers yet again in 2022, declining more than 40% vs. a 15% decline in the Gold Juniors Index.

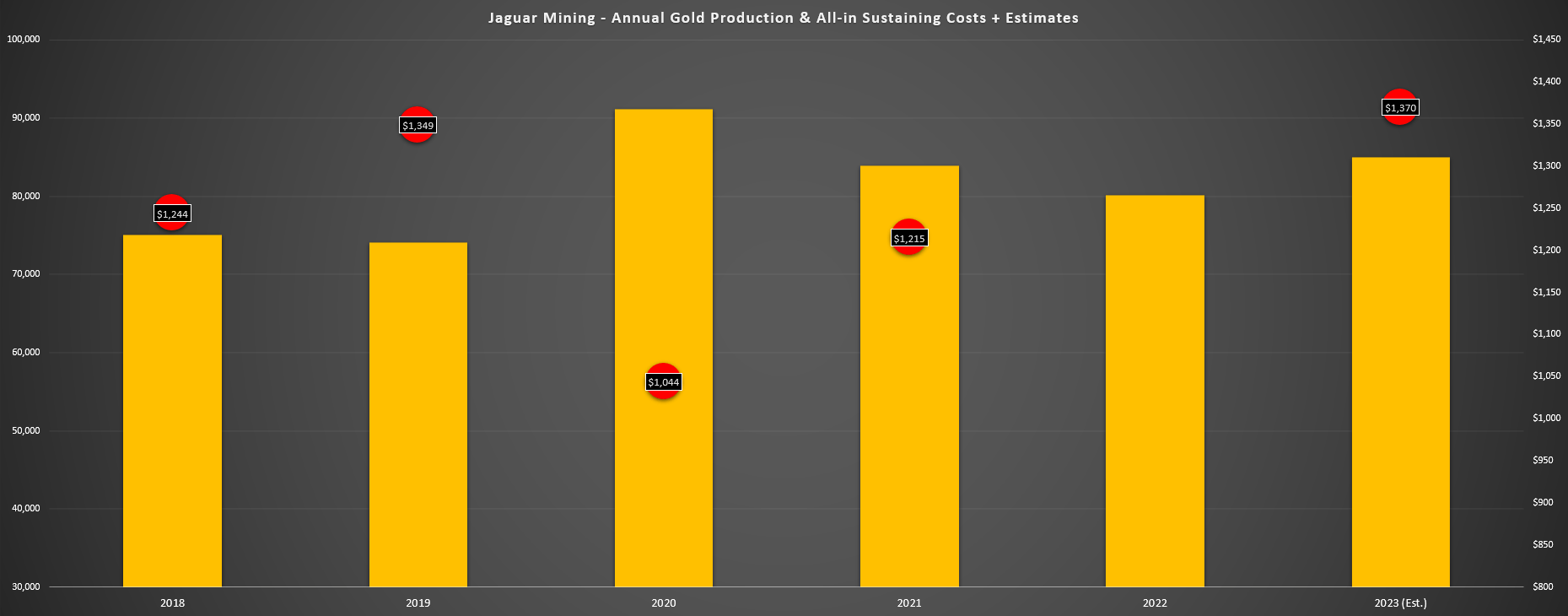

- The poor performance was attributed to another miserable performance relative to annual guidance with FY2022 production of ~81,000 ounces at costs of $1,483/oz, a significant miss.

- Unfortunately, 2023 isn’t expected to be a much better year based on guidance, and costs could miss yet again with the strengthening of the Brazilian Real.

- So, while Jaguar remains reasonably valued and is one miner that hasn’t participated in the sector-wide rally to date, I still see far more attractive opportunities elsewhere.

2022 was a tough year for the Gold Miners Index ( GDX ) with mostly flat production, a significant increase in costs and little help from the gold price. The difficult year resulted in a few companies packing up all together like Pure Gold ( OTC:LRTNF ) and Great Panther Mining ( OTC:GPLDF ) and while there were a couple of exceptions like Orla Mining ( ORLA ) and Lundin Gold ( OTCQX:LUGDF ), most miners didn't even come close to meeting guidance. Unfortunately, for investors in Jaguar Mining ( OTCQX:JAGGF ), the company missed guidance yet again and reported a high double digit increase in operating costs and all-in sustaining costs [AISC]. The result was a significant decline in free cash flow generation, a dividend cut, and negative margins on an all-in cost basis.

The good news is that while the gold price provided little reprieve to balance inflationary pressures experienced last year, it is cooperating in 2023 and is one of the best-performing asset classes year-to-date. However, Jaguar has started out the year with a limp once again, reporting a sub 20,000-ounce quarter because of a difficult rainy season in Minas Gerais. This means that it will be selling fewer ounces into a $1,900/oz plus gold price than hoped in the quarter and its costs could be pressured a little with a full year of inflationary pressures plus a stronger than expected Brazilian Real. Let’s take a look below:

All figures are in United States Dollars unless otherwise noted.

FY2022 Results

Jaguar Mining was one of the last companies to release its FY2022 results in the mining sector, and similar to last year, they didnt save the best for last. Not only did FY2022 production come in miles below its initial guidance midpoint of 90,000 ounces at just ~81,000 ounces, but cash costs soared 26% year-over-year to $1,052/oz while AISC spiked to $1,483/oz. The latter figure was up 22% year-over-year and nearly 24% above the guidance midpoint, eroding any confidence investors might have had regarding counting on management to deliver against guidance. In fairness, Jaguar was hardly the only company to miss cost guidance, but its miss was among the largest in 2022 and it was the second consecutive significant annual miss that made last year’s performance less forgivable.

Jaguar Mining - Annual Gold Production, AISC & Forward Estimates (Company Filings, Author's Chart & Estimates)

{kind=link}

Given the decline in ounces sold combined with a slightly weaker average realized gold price ($1,780/oz vs. $1,790/oz), annual revenue slid to $142.5 million and operating cash flow dipped to $40.8 million, representing significant declines on a one and two-year basis. Meanwhile, Jaguar elected to suspend its dividend, with the previously industry-leading yield being one of the few consolations to owning a stock that has dropped like a stone since its peak two years ago. In fact, while the Gold Juniors Index ( GDXJ ) is down 20% since its 2016 highs, Jaguar Mining has declined over 65% and it continues to be one of the worst performers sector-wide across nearly every time-frame.

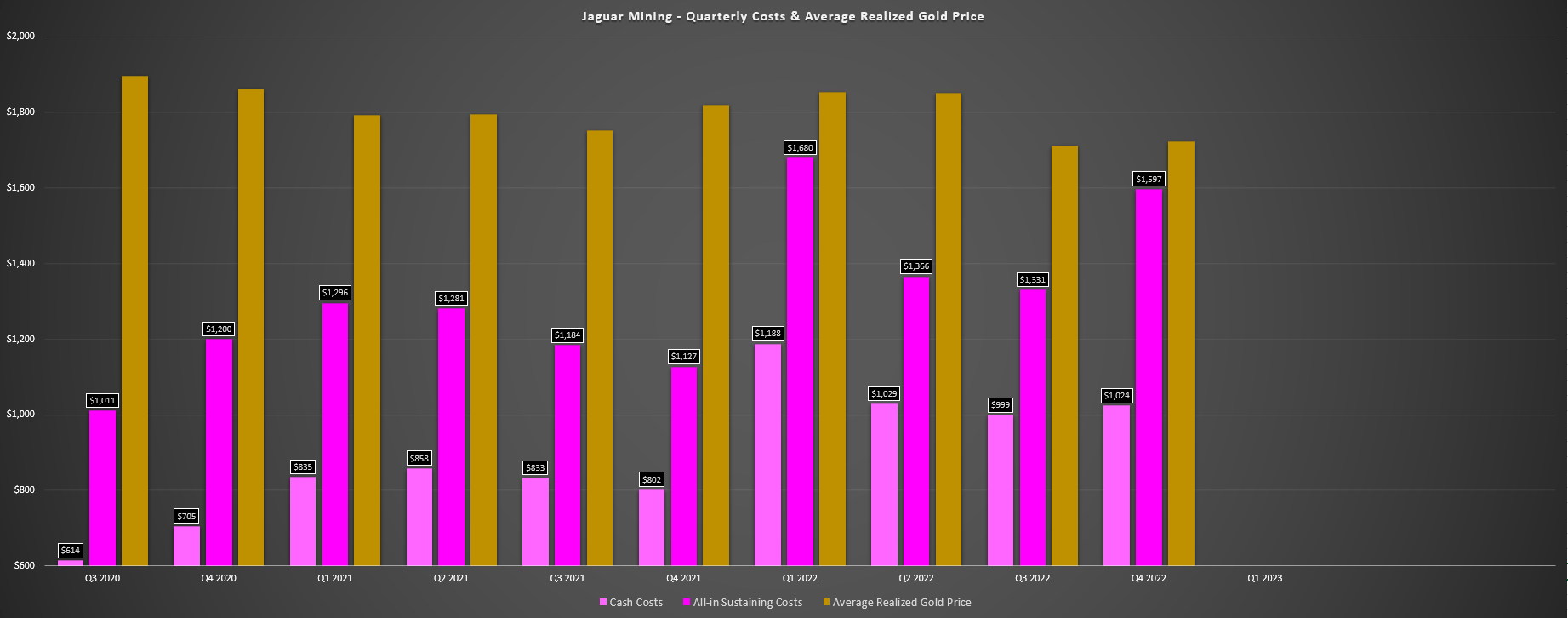

Jaguar Mining - Quarterly Costs & Average Realized Gold Price (Company Filings, Author's Chart)

{kind=link}

Fortunately, Jaguar reported positive free cash flow for the year, and ended the year with a decent cash position of $25.8 million because of the wise decision to suspend its dividend last year. However, free cash flow positive or not, this was hardly a year to write home about with AISC margins sliding by 48% to $297/oz and Q4 2022 AISC increasing to some of the highest levels industry wide at $1,597/oz, resulting in more or less non-existent margins at a $1,800/oz gold price. Worse, all-in cost margins were actually negative for the year, with all-in costs increasing to $1,864/oz (includes growth capital and exploration /evaluation costs). This certainly pales compared to producers like Orla Mining with similar production profiles (~100,000 ounces vs. ~80,000 ounces) like Orla Mining at Camino Rojo, which generated $82.0 million of free cash flow last year, or five times as much free cash flow as Jaguar.

Recent Developments

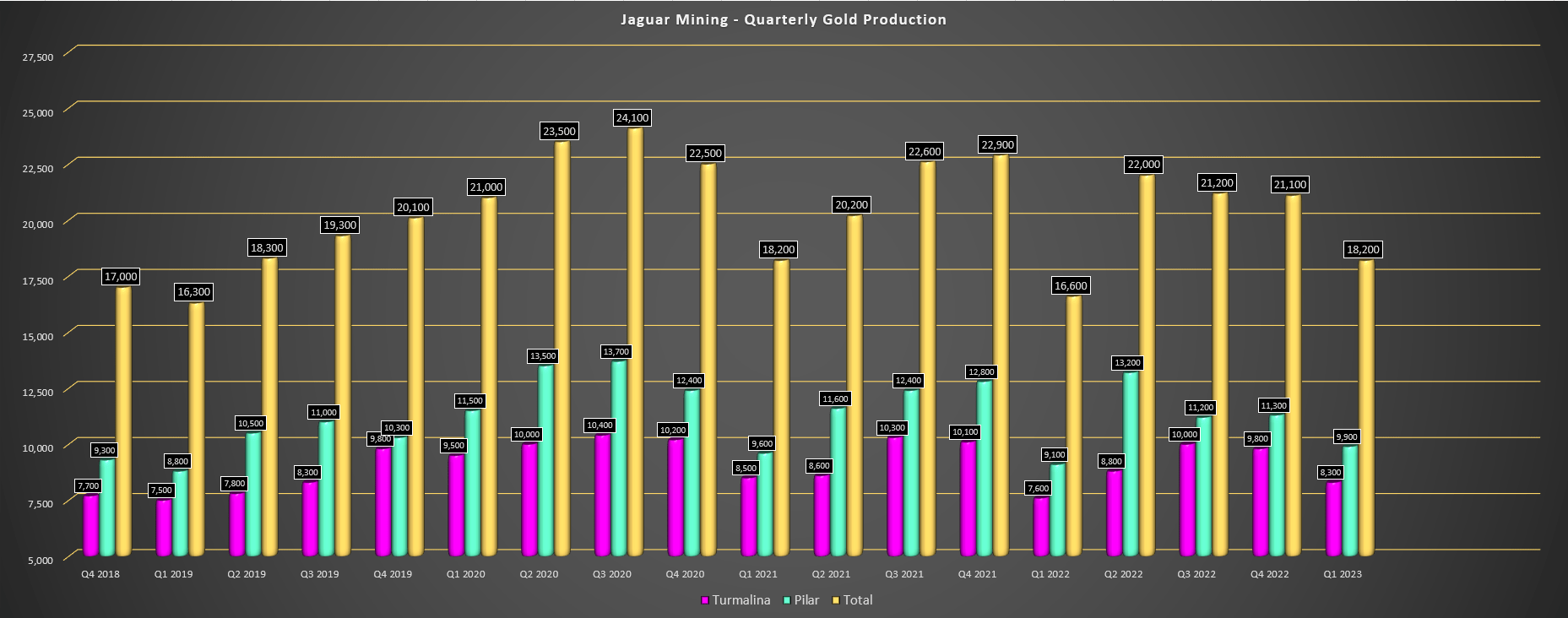

Moving over to recent developments, Jaguar Mining released its preliminary Q1 results last week, and the production figures disappointed. While the headline numbers showed a 9% increase in gold production year-over-year to ~18,200 ounces, the company was up against very easy year-over-year comps, with Q1 2022 being its second-worst quarter from an output standpoint in the past four years. This has resulted in Jaguar tracking at just ~21.1% of its FY2022 guidance midpoint (86,000 ounces) suggesting that we could have another guidance miss on deck if it can't string together three solid quarters. The company noted that the rainy season impacted haulage from its Pilar Mine to its Caete Plant, but with the weather excuse being used last year as well, it might have been prudent to guide a little more conservatively.

Jaguar Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

The good news is that the gold price has surged since the start of the year, suggesting that FY2022 may mark trough AISC margins at ~$300/oz. That said, one would hope that these would be trough margins for the company after a 55% decline in AISC margins on a two-year basis and this isn't anything to write home about. Plus, while it's not clear if Jaguar will meet its FY2022 production guidance this year after the softer Q1, meeting its cost guidance midpoint could also be difficult. This is because its FY2023 guidance midpoint of $1,325/oz assumed a BRL/USD ratio of 5.20 to 1.0 and this ratio is currently sitting closer to 4.80 to 1.0, with the Brazilian Real breaking out against the US Dollar. A combination of slightly fewer ounces sold and a stronger Real could cause costs to come in closer to $1,350/oz.

{kind=link}

So, what's the good news?

While I'm not overly optimistic about Jaguar Mining beating its guidance midpoint after two consecutive misses and a slow start to the year, we should see a material improvement in margins this year even under the assumption that the gold price averages just $1,900/oz. This is because even at the higher end of cost guidance ($1,360/oz), AISC margins would improve from $297/oz to $540/oz, helping the company to have a better year from a free cash flow standpoint. That said, much depends on the gold price, and Jaguar will need to have a much better Q2 through Q4 than its Q1 performance, which was uninspiring for investors that were hoping for a better year operationally and have suffered through a 75% share price decline in barely two years.

Valuation

Based on 75 million fully diluted shares and a share price of US$2.08, Jaguar trades at a market cap of $156 million, which pales compared to most other junior producers with similar production profiles. However, and as noted previously, Jaguar operated at negative all-in margins last year and even if we assume an average realized gold price of $1,900/oz this year, I would still expect razor-thin all-in cost margins, resulting in limited free cash flow generation. So, with Jaguar being a marginal producer with a miserable track record of meeting guidance and assets that lack of economies of scale, I continue to see the stock as an inferior way to play the sector. This is especially true given that Jaguar is not returning capital to shareholders, while investors can expect returns of ~5% from Barrick ( GOLD ) this year.

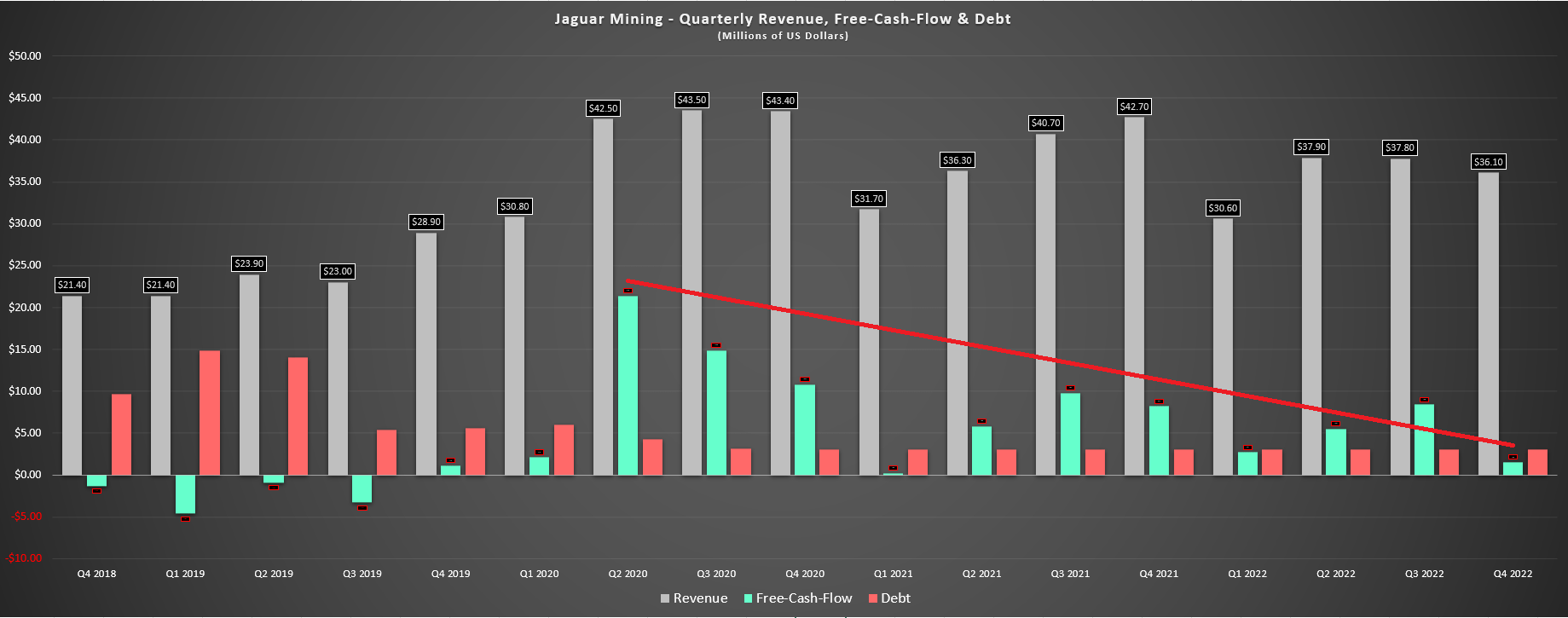

Jaguar - Quarterly Revenue, Debt, & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Some investors will argue that the organic growth profile here makes Jaguar an interesting story and may point out that the stock is undervalued on this basis. Although this growth is certainly positive, this was a five-year plan presented in Q1 2022, and I wouldn't expect the company to see production sustained above the 125,000-ounce level until at least 2026. In the same period, we will see other junior producers like Orla Mining and i-80 Gold ( IAUX ) grow annual production by ~120% and 600%, respectively, and they should have much better margins than Jaguar Mining with AISC margins north of 50%. So, while Jaguar does offer growth, I see names offering more attractive growth in more attractive jurisdictions with better margin profiles like i-80 Gold.

Finally, even if we assume Jaguar generates ~$50 million in cash flow this year, this would translate to a cash flow multiple of ~3.1 which isn't that out of line with larger producers like Aris Mining ( ARIS:CA ) and Calibre Mining ( OTCQX:CXBMF ). And while these producers may be in less attractive jurisdictions (Nicaragua, Colombia), I don't see a valuation of ~3.1x cash flow as that much of a disconnect for a sub 100,000-ounce gold producer that hasn't been able to meet its guidance that boasts negative all-in cost margins. Using what I believe to be a more conservative multiple of 4.5x cash flow and FY2022 estimates of $50 million, I see a fair value for Jaguar Mining of $225 million or US$3.00 per share.

Jaguar Mining Operations (Company Presentation)

{kind=link}

Although this points to meaningful upside, I’m looking for a minimum 45% discount to fair value for micro-cap producers to ensure there’s an adequate margin of safety. In Jaguar’s case, the current setup doesn’t even come close to meeting this criterion, with a 45% discount from US$2.67 placing the ideal buy zone at US$1.65 or lower. So, while Jaguar should see margin improvement this year and does trade well below fair value, I think there are better ways to get exposure to gold on a risk-adjusted basis, and would only become interested in Jaguar closer to US$1.70.

Summary

Jaguar Mining has done a solid job of delineating targets across its vast land package in the Iron Quadrangle and is set up to grow production to 120,000+ ounces later this decade. However, while this represents ~40% growth, some of this is merely a recovery back to FY2020 levels and costs have risen substantially in the period, offsetting the impact of this future growth from a cash flow standpoint. In addition, while this is solid growth, it's difficult to rely on a team that hasn't even come in remotely near guidance the past two years. And while this growth is meaningful, there are several growth stories with more torque elsewhere in the sector.

To summarize, I continue to see Jaguar Mining as an inferior way to play the sector and I would view any rallies above US$2.44 before June as an opportunity to book some profits if I were long the stock.

For further details see:

Jaguar Mining: A Disappointing Start To The Year