CA - Jaguar Mining: A Rough Q2 Operationally

2023-07-11 10:10:02 ET

Summary

- Jaguar Mining Inc. Q2 results showed a 24% decline in gold production year-over-year, with the company tracking at just 40.7% of its full-year guidance midpoint.

- The company has withdrawn its guidance due to operational challenges, marking the third consecutive year of significant misses vs. its annual guidance midpoints.

- Given Jaguar's inability to meet production targets and position as a high-cost and small-scale producer which reduces its attractiveness to potential suitors, I continue to see the stock as an Avoid.

The Q2 Earnings Season for the VanEck Gold Miners ETF ( GDX ) is just around the corner, and preliminary results from several miners have begun to trickle out, with solid reports from Calibre Mining ( CXBMF ) and Victoria Gold ( VITFF ). Unfortunately, Jaguar Mining Inc. ( JAGGF ) was not one of the companies with a solid Q2 report, and its brutal Q2 performance (output down 24% year-over-year) followed a disappointing Q1, leaving the company tracking at just ~40.7% of its full-year guidance midpoint. The company has pulled its guidance, which isn't a surprise, and this has set the company up for a third consecutive massive guidance miss, with double-digit percentage misses in 2021 and 2022 relative to its guidance midpoint. In this update, we'll look at what went wrong and whether Jaguar stock is worthy of consideration:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q2 Production Results & Sales

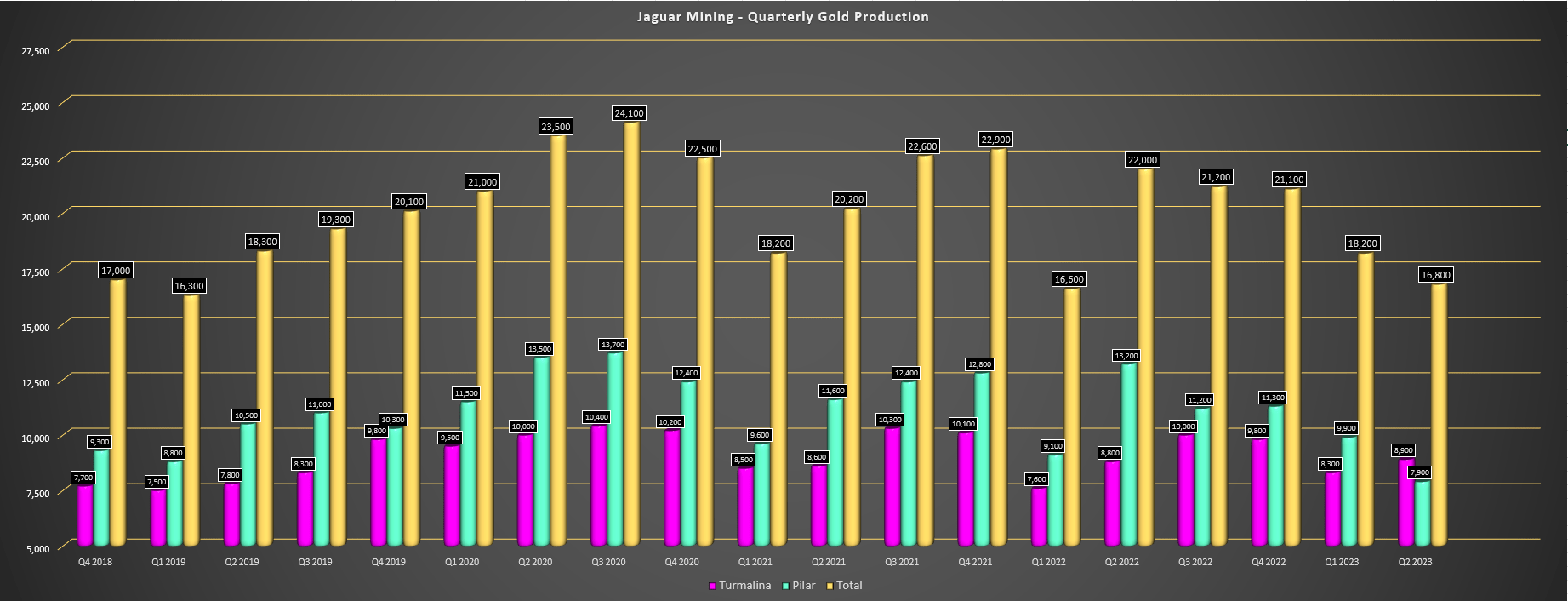

Jaguar Mining released its preliminary Q2 results this week, reporting total gold production of ~16,800 ounces, a 24% decline from the year-ago period. The sharp decline was related to much lower tonnes processed (203,000 tonnes vs. 228,000 tonnes in Q2 2022) and much lower grades, with head grades slipping to 2.80 and 3.04 grams per tonne of gold at its Turmalina and Pilar mines, respectively. These grade declines represented an average decline of 15%, and this was the third-weakest quarter for the company operationally in the past four years. As noted, this has left the company tracking at barely 40% of its planned production of 86,000 ounces (FY2023 guidance midpoint). With Jaguar being a ~21,000 producer even in a good quarter, there's no way to make up this significant shortfall by year-end.

Jaguar Mining - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Unfortunately, while the weak Q1 2022 was disappointing (2nd-weakest quarter of the past four years), Q2 2023 was weak for the wrong reasons. This is because mining challenges are much worse than a heavy rainy season or COVID-19 staffing issues (Q1 2022) that can be overcome and have nothing to do with planned production. And as Jaguar noted in its prepared remarks, it saw a change in geometry of primary orebodies at Pilar that didn't fit its current mining method, with the result being increased dilution and losing some planning mining blocks, in addition to lower grades than planned. Jaguar has since changed its mining to account for the ore being narrowed and flatter, and fortunately, there is no material change to resources and reserves.

As for its slightly smaller Turmalina Mine, the company saw greater variability than usual, resulting in lower than planned grades, which was certainly clear in the results as grades fell 10% year-over-year to 2.80 grams per tonne of gold (Q2 2022: 3.10 grams per tonne of gold). Jaguar noted it has changed its grade control program to improve stope design and grade control, but grade issues of this magnitude and excess dilution is never a positive sign at any mine, let alone at both mines in the same quarter. And while the issues could be localized and not something that Jaguar will face in future quarters, this has added uncertainty to what's already a relatively weak story, with Jaguar continuing to be a high-cost miner that's seen its costs soar over 40% from FY2020 levels ($1,044/oz --> $1,483/oz in FY2022) and it looks like they'll remain well above the $1,400/oz level this year.

Tracking For Another Significant Guidance Miss

2021 was a year to forget for Jaguar Mining given continued COVID-19 related staffing headwinds, and the massive miss on guidance was excusable, with production coming in at ~83,900 ounces, miles short of the 100,000 ounce guidance midpoint. Worse, costs blew up well above guidance levels, with all-in sustaining costs [AISC] of $1,215/oz vs. expectations of $1,050/oz. However, while it wasn't unreasonable to give the company a pass for 2021, 2022 was no better. In fact, production and costs came in at ~80,100 ounces and $1,483/oz, respectively, another significant miss vs. FY2022 guidance of 90,000 ounces at $1,200/oz at the midpoint. This was two strikes against the company, given that these were not small misses by any means, and it's no surprise that the market has lost confidence and the stock has continued to bleed lower.

{kind=link}

Given this poor track record, I warned earlier this year that while the bar was being set low at 86,000 ounces at $1,325/oz for its FY2023 guidance midpoint; I was not confident in the company meeting cost guidance. This was because of the inability to come remotely close to guidance over the past two years and the fact that Brazilian Real was strengthening, providing a headwind from an operating cost standpoint. That said, I was optimistic that the company might at least deliver 85,000 ounces (low end of guidance) at $1,370/oz (high end of guidance), which would have been an improvement from the rough 2022. However, discussed by the company and what we can infer from its disappointing H1 results, production and costs will come in nowhere near these levels this year.

"Given the challenging quarter and the changes we plan to implement to our mining systems during the second half of the year, we feel it is prudent to temporarily suspend our forward-looking guidance for fiscal 2023 in regard to the Company’s expected ounces of production and costs so that we can, in the future, provide updated guidance that should reflect the implementation of the aforesaid changes"

- Jaguar Mining - July 11, 2023.

Looking at the below chart, I think more reasonable estimates for FY2023 given the continued strength in the Brazilian Real and production shortfall in H1 is for ~77,000 ounces at $1,470/oz AISC, which would mark the weakest production year since 2019 and another year of $1,450/oz plus AISC, over 10% above the industry average. Obviously, the company could beat these figures if it can surprise to the upside in H2, but even if they beat these figures, this will still represent a year of limited margin expansion after AISC margins have already crumbled from $701/oz in FY2020 to what looks to be a best case of $500/oz in FY2023.

So, when we're seeing several other miners like Barrick Gold ( GOLD ) return capital to shareholders through dividends and buybacks and enjoy much better margins this year, it's tough to make a case for owning a producer with limited margin improvement and no shareholder returns even with the gold price spending a record 17 weeks above $1,900/oz - an environment when a producer should thrive, not simply be treading water.

Valuation

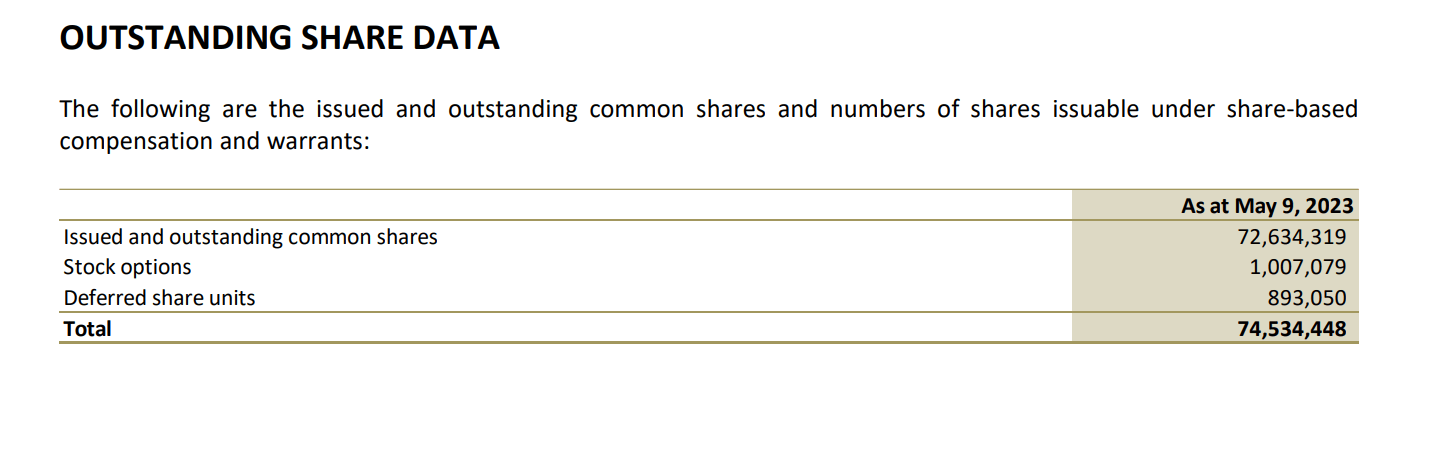

Based on ~74 million fully diluted shares and a share price of US$1.70, Jaguar trades at a market cap of US$126 million, a very reasonable valuation for a Tier-2 producer that was on track to produce ~90,000 ounces of gold this year. However, after another rough H1, this is no longer the case, and the company will be lucky to produce 80,000 ounces this year with another year of costs above the $1,400/oz level. The result will be minimal free cash flow generation, even with the benefit of higher gold prices, and lower cash flow generation, with operating cash flow likely to come in at barely $39 million. And while this leaves Jaguar trading at ~3.2x FY2023 cash flow estimates, I don't see any reason a stock of this caliber (small-scale producer with above average costs in Tier-2 jurisdiction incapable of meeting production targets) would command a cash flow multiple above 4.5x, especially when larger producers now trade at much more attractive valuations.

{kind=link}

So, using what I believe to be a more conservative multiple of 4.25x operating cash flow for Jaguar, the stock's fair value would come in at $166 million or US$2.24 per share. Although this figure points to a material upside from current levels, I am looking for a 45% to 50% discount to fair value for micro-cap producers, and certainly those where management has been unsuccessful in meeting its targets. Even if we apply the lower end of the range (45% discount) to Jaguar Mining, the ideal buy zone comes in at US$1.23 or lower. Hence, even though the stock has suffered a violent correction to date and is off 80% from its highs, I still don't see enough margin of safety here. And given that this is not the case of this being a high-quality producer, I don't see any reason to justify paying up for the stock or being lenient on a required margin of safety level.

Summary

The only good news about Jaguar Mining's rough Q2 report is that the worst quarter of the year should be in the rearview mirror, as I'm not sure it can get much worse than the Q2 results. That said, the company is on track for yet another significant miss on annual guidance (third in a row), and the company continues to be a small-scale and a higher cost producer.

These attributes make it less attractive from an M&A standpoint, which could otherwise be an angle for owning the stock if it were a potential takeover target (which I don't see being the case). Meanwhile, the significant erosion in the share price and reduced liquidity vs. 2020 makes it less attractive from an investment standpoint, with most funds and certainly generalists looking for more liquid producers vs. a stock like Jaguar that trades a mere ~$400,000 a week in average dollar volume.

This doesn't mean that the stock can't go higher, but I believe in buying the best miners with the best ore bodies and management that can deliver on promises when they trade at a deep discount to fair value, and ideally focusing on those names with reasonable trading liquidity. Occasionally, I will settle for only two of these four attributes if a situation is special, but I would argue that Jaguar Mining meets none of these attributes with inferior liquidity, average ore bodies, a lack of scale which makes it a relatively marginal producer, and management that will now miss guidance for the third year in a row by a wide margin.

To summarize, I see far better ways to play the sector elsewhere. That said, if I wanted to gamble with a small portion of my portfolio, I see Jaguar Mining Inc. shares as a Speculative Buy at US$1.23 or lower, where it would trade closer to multi-year support.

For further details see:

Jaguar Mining: A Rough Q2 Operationally