CA - Jaguar Mining: Another Year Of Massive Underperformance Relative To Guidance

2023-12-27 16:37:08 ET

Summary

- Jaguar Mining's Q3 production declined by 18%, leaving year-to-date production at just ~61% of its previous (since withdrawn) annual guidance.

- Meanwhile, it was one of the few producers to report a significant decline in AISC margins year-over-year despite benefiting from easy comps and a much higher gold price.

- In this update, we'll dig into the Q3 results, recent developments, and where the stock's updated buy zone lies.

Just over five months ago, I wrote on Jaguar Mining ( JAGGF ), noting that while the stock was on track for another year of missed guidance, the stock would become a Speculative Buy at US$1.23 or lower. This turned out to be a poor call in hindsight as the stock plunged another 20% before finding its eventual bottom, but it's since recovered these losses and was one of the best-performing producers in Q4 with a ~50% return. Unfortunately, the Q3 results were below my expectations, costs continue to track miles above the industry average, and it's difficult to trust future projections after three years of significant guidance misses. In this update we'll dig into the Q3 results, recent developments, and where the stock's updated buy zone lies.

{kind=link}

Jaguar Mining Operations - Company Website

Q3 Production & Sales

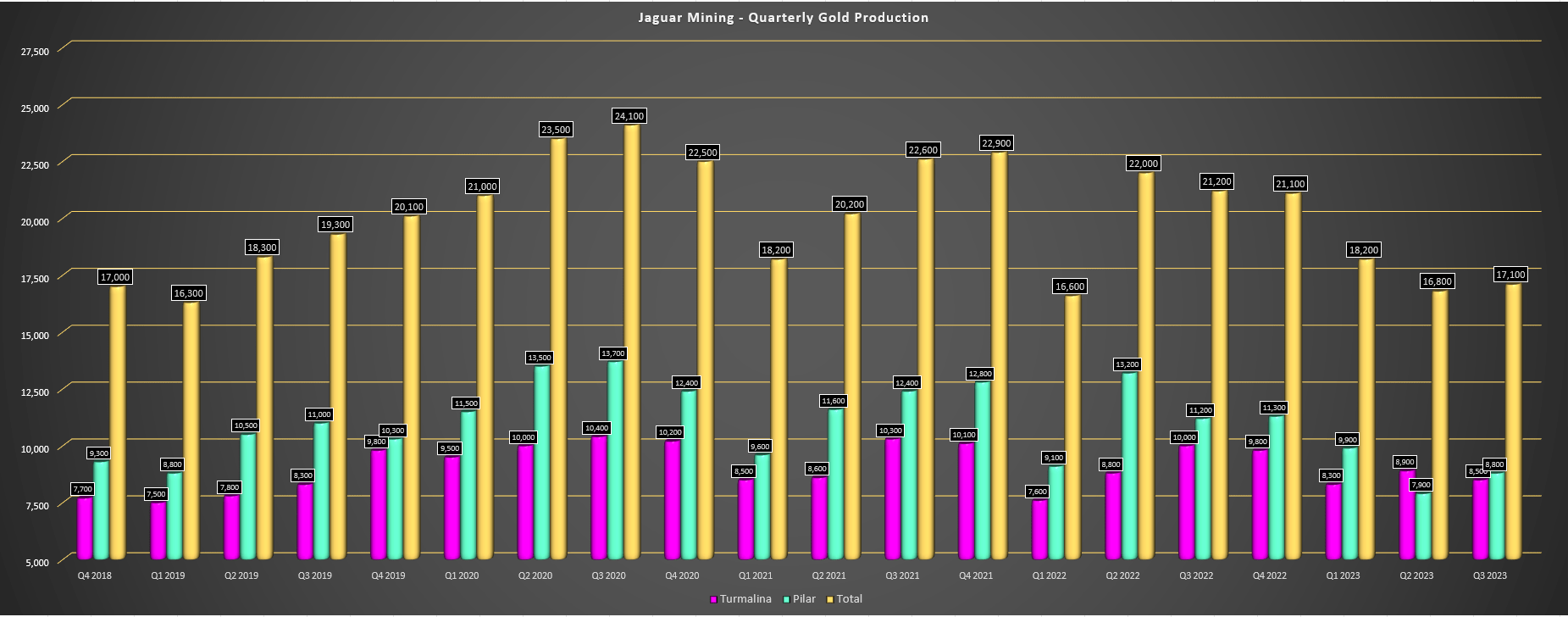

Jaguar Mining released its Q3 results in November, reporting quarterly production of ~17,300 ounces of gold, an 18% decline from the year-ago period. This significant decline in output was related to lower production at both of its operating mines in Brazil, with Pilar's production down 22% to just ~8,800 ounces while Turmalina's production slipped 14% to ~8,500 ounces. Unfortunately, this has left year-to-date production sitting at just ~52,200 ounces or ~60.7% of its initial guidance mid-point , which is remarkably an even worse position than the company was in at the same time last year with production of ~59,900 ounces vs. a guidance midpoint of 90,000 ounces (~66.6%).

{kind=link}

Jaguar Mining - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

Jaguar Mining 2023 Guidance - Company Filings

Although a single guidance miss on the back of worse than expected weather is not the end of the world (Q1 2023 affected by the rainy season in Minas Gerais), this is the third consecutive year of guidance misses for Jaguar, with the company set to produce barely 70,000 ounces this year. In fact, if we look at its past three years of production, the company will have produced ~235,000 ounces in the period vs. a combined guidance midpoint of ~276,000 ounces, leaving it in rare air vs. peers as a producer with three consecutive misses, and sizeable misses at that. Plus, as we'll detail below, the performance relative to cost guidance has been no better, and Jaguar has now found itself as one of the highest-cost producers sector-wide.

Digging into the production results a little closer, its Pilar Mine processed ~107,000 tonnes at 2.88 grams per tonne of gold vs. ~111,000 tonnes at 3.51 grams per tonne of gold in the year-ago period, translating to a significant decline in total output. The company noted that changes in dip and ore thicknesses within Panel 15 limited the amount of mineable blocks and grades. The company has since shifted to cut and fill mining (from long-hole open stoping) and expects to see better production with ounces coming from Panel 16 during Q4, with the company also working to improve grade control. Unfortunately, the lower production/sales led to a significant spike in all-in sustaining costs [AISC] despite a less reliance on more expensive contract mining, with costs up ~38% year-over-year to $1,701/oz.

As for the company's Turmalina Mine, year-over-year production fell due to lower grades, with overall production down 14% year-over-year. On a positive note, Jaguar shared it benefited from lower fuel consumption, from more efficient hauling and shorter cycles that resulted in more respectable AISC figures ($1,399/oz vs. $1,265/oz), but costs were still up over 10% year-over-year despite the benefit of lower sustaining capital spend. Still, all-in sustaining costs are sitting nearly 15% above the industry average at $1,580/oz year-to-date, leaving little room for free cash flow generation despite relatively modest sustaining capital expenditures (~$11.8 million year-to-date), with higher sustaining capital expected in 2024 (~$19.0 million).

{kind=link}

Jaguar Mining Quarterly Revenue - Company Filings, Author's Chart

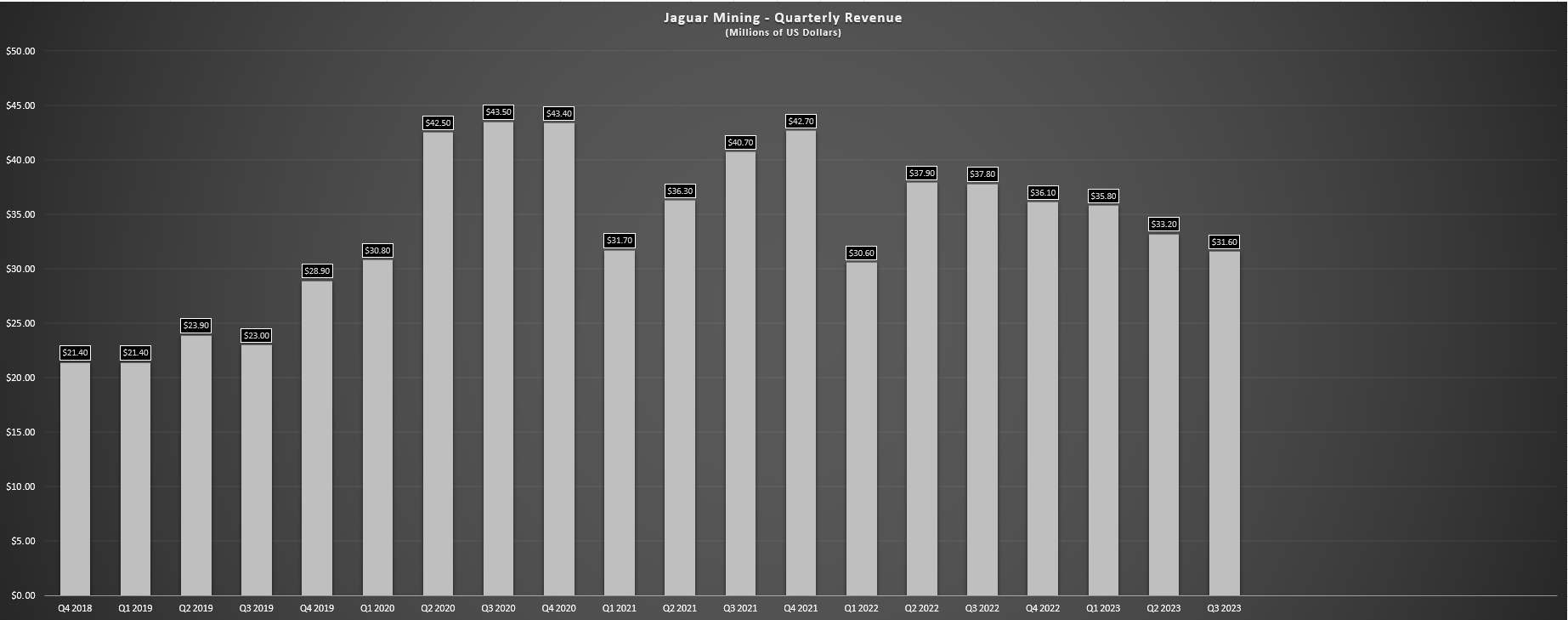

Not surprisingly, Jaguar's financial results were underwhelming, with revenue down 16% year-over-year to $31.6 million, while operating cash flow sunk to just $6.3 million (Q3 2022: $13.3 million) and net income fell to ~$3.8 million. This translated to negative free cash flow with ~$9.0 million in investments and the company's cash balance fell from ~$29.9 million to ~$20.0 million compared to the year-ago period. And while this translates to a net cash position of ~$14.0 million, it's difficult to see how the company will be able to fund its ambitious growth plans (growing production by over 50%) without additional share dilution, given that it's unable to generate consistent free cash flow even with quarters where the gold price is sitting close to all-time highs. In fact, free cash flow is negative year-to-date as well, with ~$28.4 million spent on investments vs. ~$26.7 million in operating cash flow.

Costs & Margins

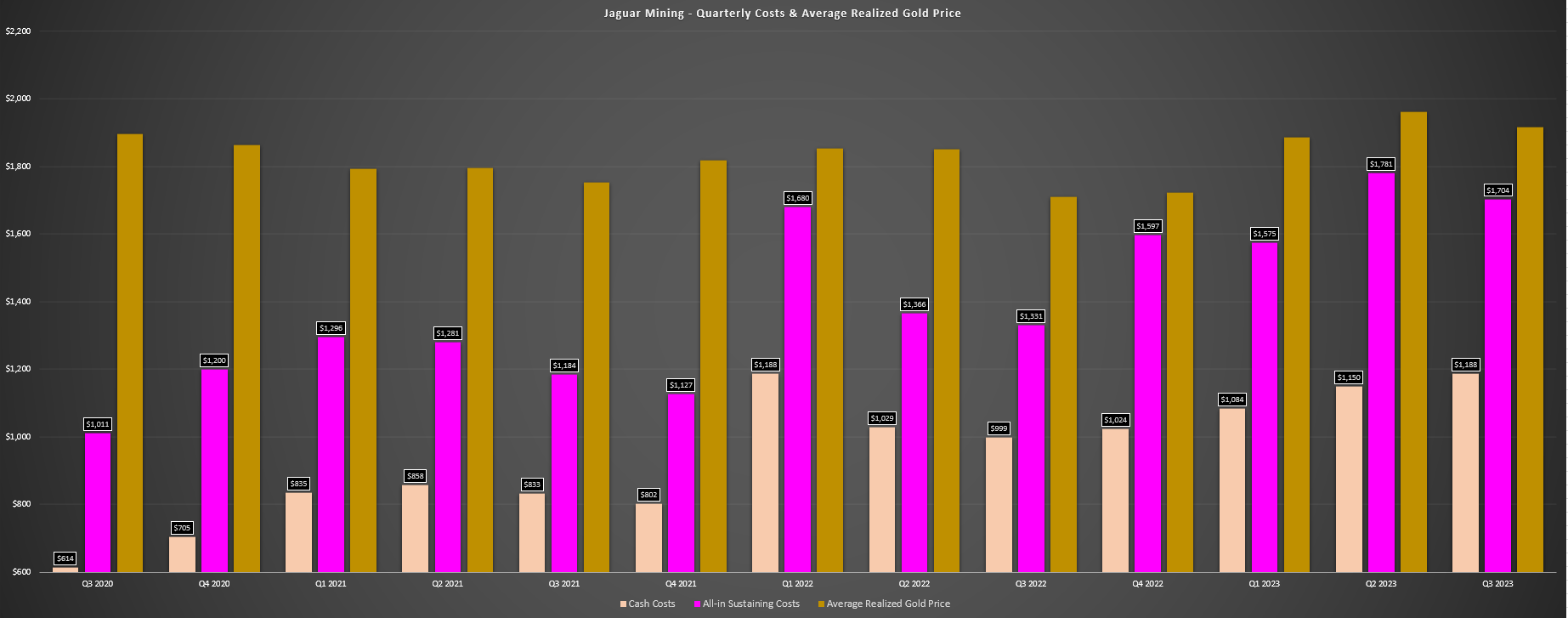

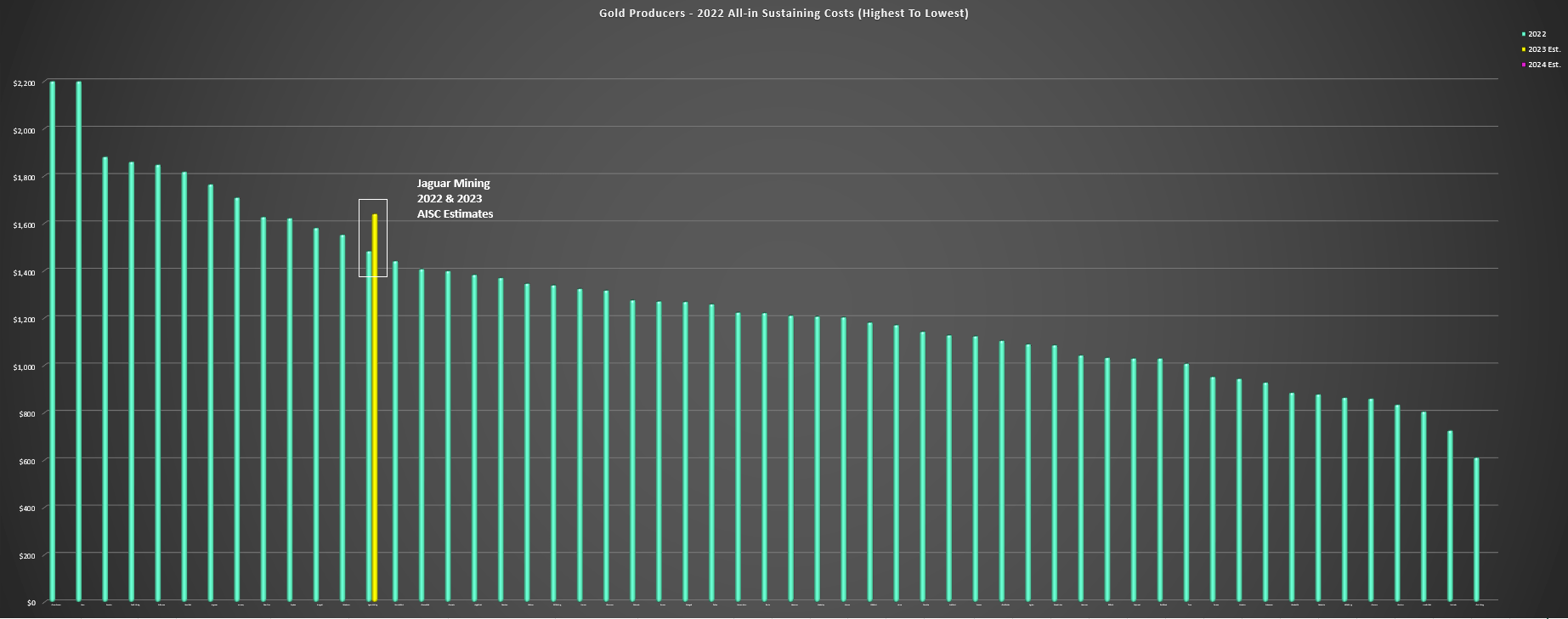

Moving over to costs and margins, Jaguar's performance was just as disappointing, with all-in sustaining costs of $1,704/oz, a 28% increase from the year-ago period. This was because of fewer ounces sold and slightly higher sustaining capital in the period, and year-to-date AISC is sitting at $1,682/oz, nearly 30% above its guidance midpoint of $1,325/oz provided earlier this year. And while the company appears confident it can improve costs with its cost-savings program (reduced usage of contractors, more efficient truck fleet with higher haul speeds and lower fuel consumption), these will still be relatively high-cost and low-scale operations even with the benefits of cost-savings, and Jaguar's trend higher in costs has been among the worst sector-wide as shown below, and with it set to be one of the top-10 highest-cost producers in 2023.

{kind=link}

Jaguar Mining Quarterly Cash Costs, AISC & Average Realized Gold Price - Company Filings, Author's Chart

{kind=link}

Jaguar Mining AISC (2022 & 2023 Est.) vs. Peers - Company Filings, Author's Chart

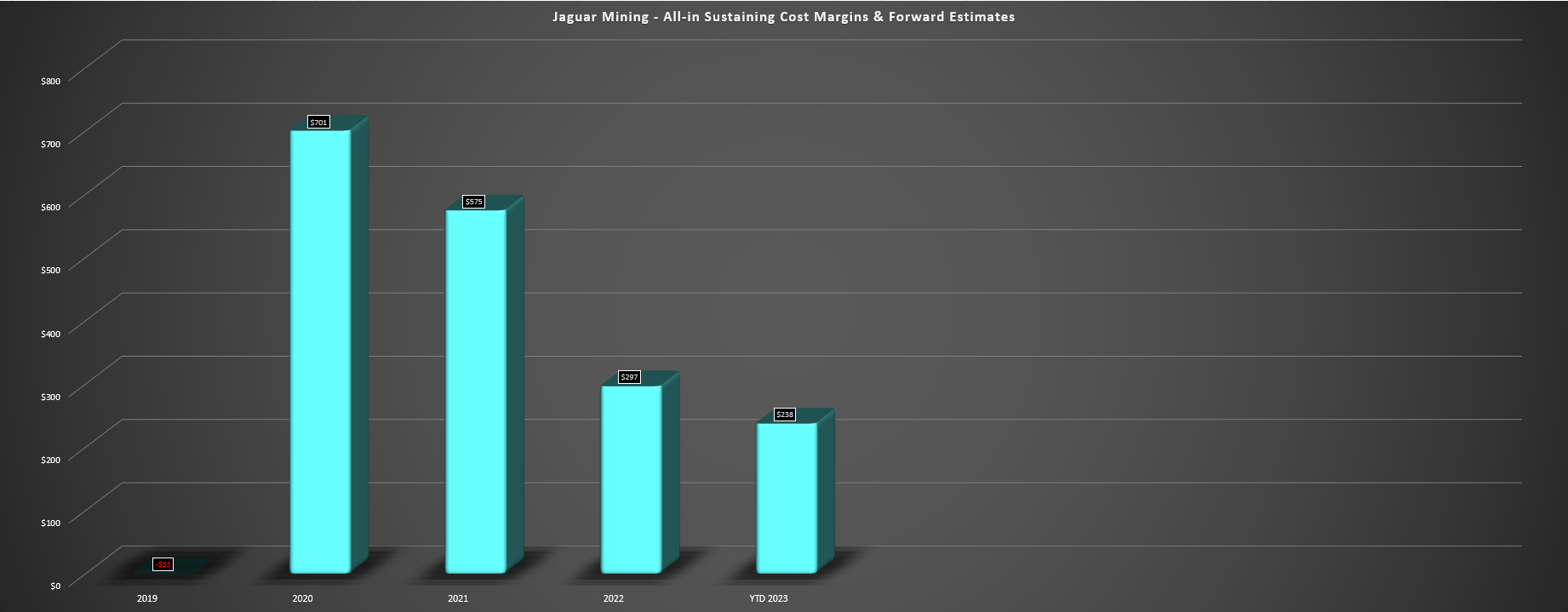

As for the company's margins, most producers were busy reporting significant margin expansion, and even though up against difficult comparisons given the tailwind from the gold price. However, Jaguar's AISC margins plunged from $380/oz in Q3 2022 to $212/oz in Q3 2023, and year-to-date AISC margins are sitting at a mere $238/oz. This is certainly not ideal and while many investors might argue that the stock has been unfairly punished with an 80% share price decline, it's important to note that the share price has largely followed margins, which have slid from ~$700/oz to ~$240/oz year-to-date in 2023, with an additional impact from a higher share count. Obviously, with barely 10% AISC margins even with gold near record highs, it's tough to be optimistic about the company's ability to self-fund growth, especially if the Brazilian Real strengths further against the US Dollar ( UUP ).

{kind=link}

Jaguar Mining - Annual AISC Margins & YTD 2023 Margins - Company Filings, Author's Chart

Recent Developments

So, is there any good news?

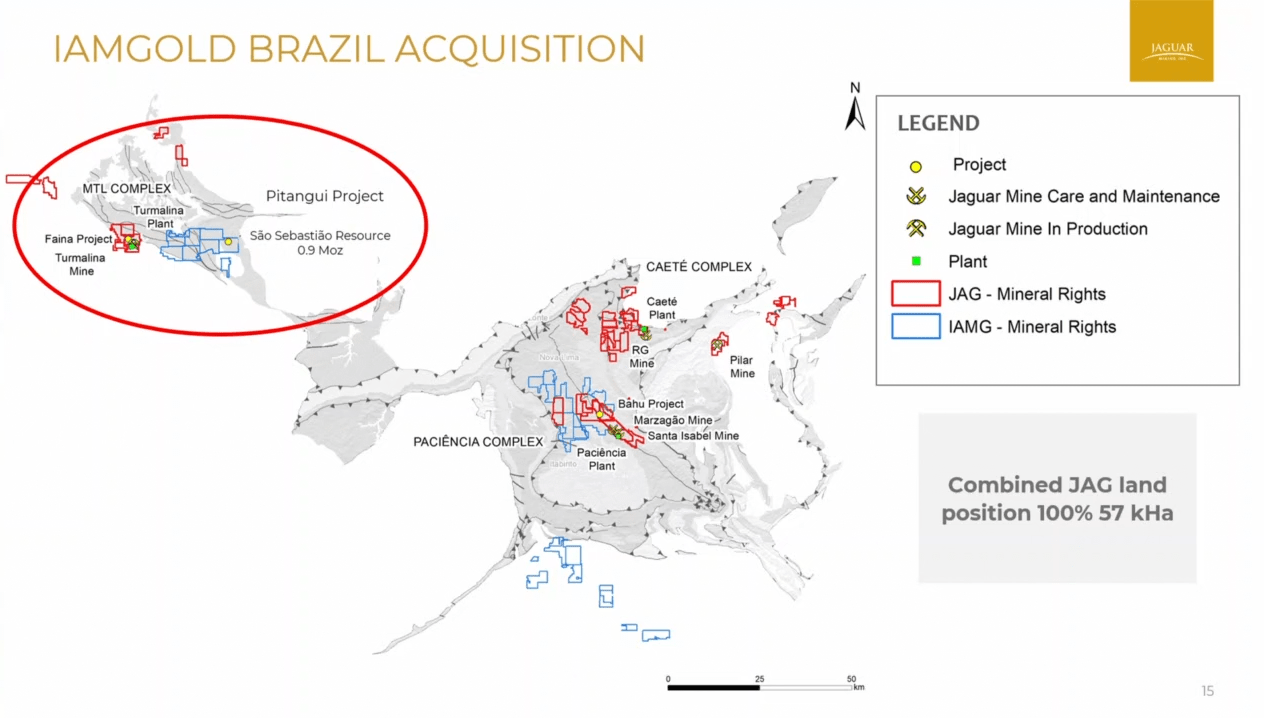

The most significant development in the quarter was the acquisition of Iamgold's ( IAG ) Pitangui Project and the remaining interest in the Acurui Project in exchange for ~6.3 million shares of Jaguar (not to be traded or transferred for at least 12 months), translating to just shy of 9% share dilution on a fully-diluted basis. Jaguar also granted Iamgold contingent consideration, including a $80/oz payment for the initial 250,000 ounces of gold sold from Pitangui (1.5% multiplied by the net smelter returns realized for gold sales in excess of 250,000 ounces), and a net smelter return on all gold sales from the Acurui Project equivalent to 1.5% multiplied by net smelter returns realized. As the image below shows, this was a very strategic acquisition from a synergy standpoint, adding ~450,000 M&I ounces at above-average grades (4.07 grams per tonne of gold) in close proximity to its Turmalina Plant.

{kind=link}

Jaguar Mining Acquisition (Pitangui) - Company Website

Overall, I think Jaguar made out well on this acquisition with a price paid of just ~$13/oz (excluding contingent consideration) and it could help the company to leverage its meaningful processing infrastructure in Brazil, including Turmalina which has excess capacity. Although this deal is positive, Jaguar noted that even a fast-tracked development scenario could mean up to four years to put the asset into production, hence we will not see this growth overnight. So, while Jaguar could potentially increase its total gold production by 2028 (~70,000 to ~130,000 ounces) with multiple development assets and three mills, there are higher-growth stories at better margins that are self-funded elsewhere in the sector, such as K92 Mining ( KNTNF ) that will enjoy ~300% production growth (~120,000 to 480,000 GEOs) at industry-leading margins (sub $700/oz AISC or 65% AISC margins) in the same period (2023-2027).

{kind=link}

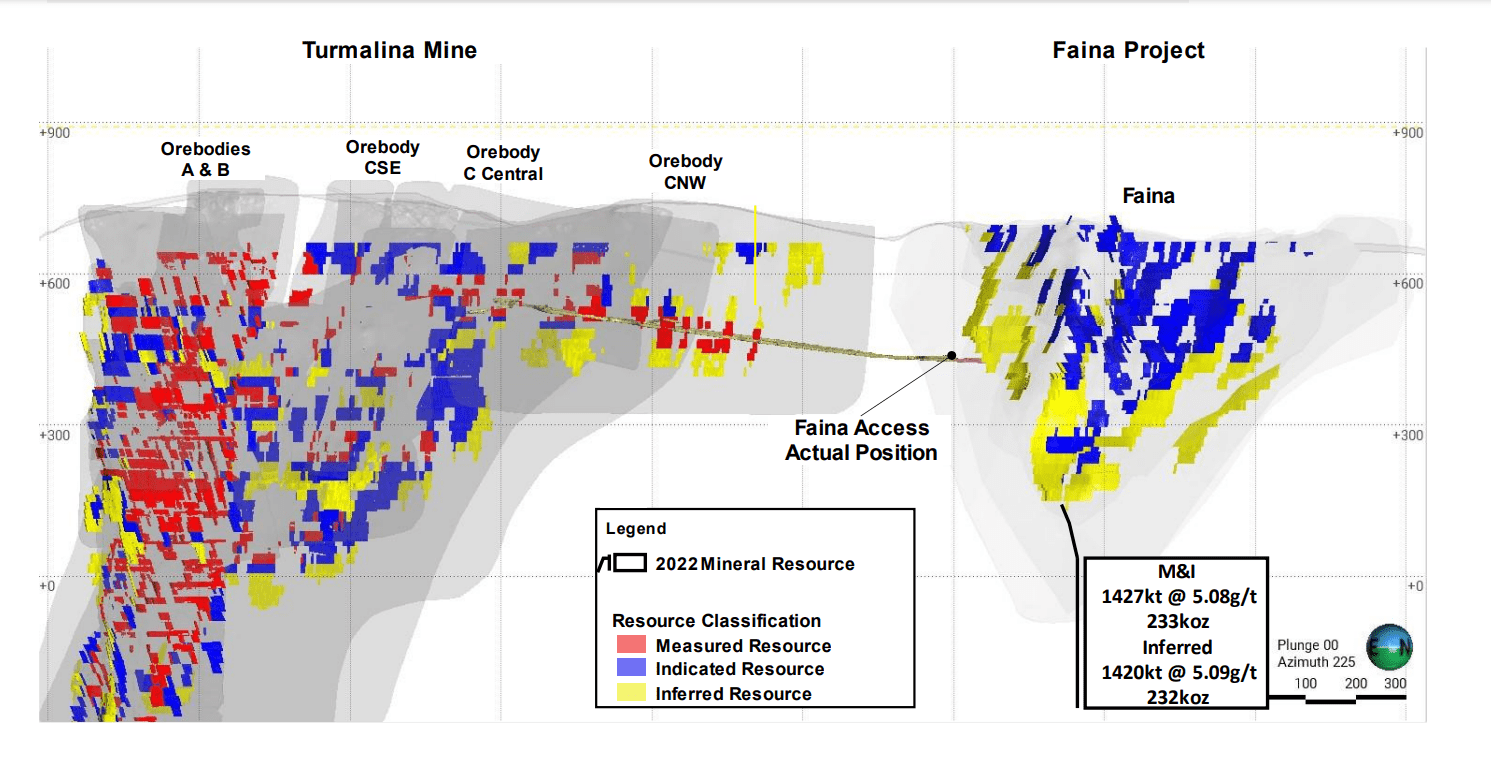

Turmalina Mine & Faina Development - Company Website

The other positive development worth noting is that Jaguar is seeing solid progress in regards to developing towards its higher-grade Faina Project, and the company is expected to reach the deposit by year-end. Obviously, access to higher-grade ore will benefit its Turmalina Complex if the resources can reconcile well with expectations and this should to drive unit costs down at this asset. That said, 2024 will be a transition year as the company works through development ore, so I would not expect to see a meaningful improvement until 2025 when Faina is in full production. In summary, while this is a near-term positive, I still expect Jaguar to be a high-cost producer at both its assets in 2024 and this certainly makes it a riskier bet if the gold price turns lower as its margins are already razor-thin.

Valuation

Based on ~81 million fully diluted shares and a share price of US$1.43, Jaguar trades at a market cap of ~$115 million, making it one of the lower capitalization companies in the junior producer space behind names like Galiano Gold ( GAU ), Fortitude Gold ( FTCO ), and ahead of small producer Soma Gold ( SOMA:CA ). And while this market cap figure might seem extremely low given that Jaguar trades at a fraction of the valuation of some developers, the stock remains cheap for a reason given that it's a high-cost producer in a Tier-2 ranked jurisdiction with a terrible track record of delivering on guidance. In fact, the company is on track for its third consecutive guidance miss, with all of these being sizeable misses relative to the initial outlook.

On a positive note, the company has bolstered its land and resource position by adding the Pitangui Project, and we should see a lift in feed grades in 2025 when the company is processing higher-grade ore from Faina. Meanwhile, the company appears confident it can grow into a 120,000 ounce producer at lower costs later this decade. That said, I would expect another mediocre year in 2024 and it's tough to be optimistic about the company delivering on this growth without additional share dilution given its inability to consistently generate positive free cash flow. Plus, there's no shortage of high-cost non-Tier-1 jurisdiction junior producers, meaning that there's little allure to owning Jaguar Mining as names like this are a dime a dozen in the sector and often underperform (lack of liquidity, rarely return capital to shareholders, not meaningful enough scale).

So, what's a fair value for the stock?

Using what I believe to be a conservative multiple of 4.0x FY2023 cash flow estimates (~$34 million) and adding ~$14 million in net cash, I see a fair value for Jaguar of ~$150 million [US$1.85]. This points to a 29% upside from current levels, which is a decent upside if the stock trades up to fair value. However, I am looking for a minimum 45% discount to fair value for micro-cap miners to ensure an adequate margin of safety. And when we apply this discount to Jaguar's estimated fair value of US$1.85, the stock's ideal buy zone comes in at US$1.02 or lower. In summary, while Jaguar may have upside from current levels, I don't see the reward/risk ratio as compelling enough here after the stock's sharp rally.

Summary

Jaguar Mining may be reasonably valued and is certainly one producer that could have enormous recovery potential given the distance that it is from its 2020/2021 highs. However, as I've stated in past updates, the stock never belonged above US$5.00 in the first place, let alone US$9.00, we've seen additional share dilution since then, and inflationary pressures have put a severe dent in margins since FY2020 ($238/oz year-to-date vs. $701/oz in 2020). In addition, I prefer to avoid companies that have a poor track record of delivering on promises, and Jaguar has been one of the most inconsistent names for delivering on guidance in the 2021-2023 period. Hence, I consider it a high-risk, high-reward name, and I consider investing in names with these qualities (poor delivery, razor-thin margins, marginal projects/mines) as gambling, not investing.

In summary, I continue to see far more attractive bets elsewhere and I would only become interested in Jaguar Mining on a dip below US$1.05.

For further details see:

Jaguar Mining: Another Year Of Massive Underperformance Relative To Guidance