PIPR - Jefferies: All In MD Count

2023-11-15 08:37:44 ET

Summary

- Substantial growth in MD count over the last years has proven effective as a bottom of the cycle investment for the company.

- Resilience is impressive, and performance is better than some more highly valued peers.

- However, our coverage tells us that the M&A activity, particularly from sponsors, will not snap back, and we have outstanding economic worries.

- On an absolute basis, we prefer other picks.

Jefferies ( JEF ) has had impressively resilient performance. We think it all comes down to MD counts which have grown meaningfully over the last several years. Comp costs are up despite pretty weak M&A activity, owed to growing MD counts. At the same time, advisory and ECM and DCM are doing pretty well, in stark contrast to the rest of the industry. While the lack of underlying snap back in M&A is an issue for them considering their personnel investments, they are still performing better than some of their more diversified peers in the sector like Piper Sandler ( PIPR ), and have a lower valuation.

Some Notes and Earnings

Jefferies is a bank with a dramatically improving profile. Some years ago, there was even discussion about it ousting some of the major Bulge Bracket names. Its deals get pretty big, and they're a little more than middle market nowadays due to their recent growth. In particular, their MD growth has been astonishing across all their geographies.

As Rich mentioned, that growth, particularly in these last couple of years, has been across the globe. This was the period where we were able to make inroads in almost every part of the world. Our growth was significant. This is just investment banking MD headcount. It's kind of a 70% overall global increase in the four-year period. Quite interestingly, the way the numbers line up, it's a little over 50% in the U.S., almost 90% in Europe, Middle East, Africa, and 200% in Australia and Asia.

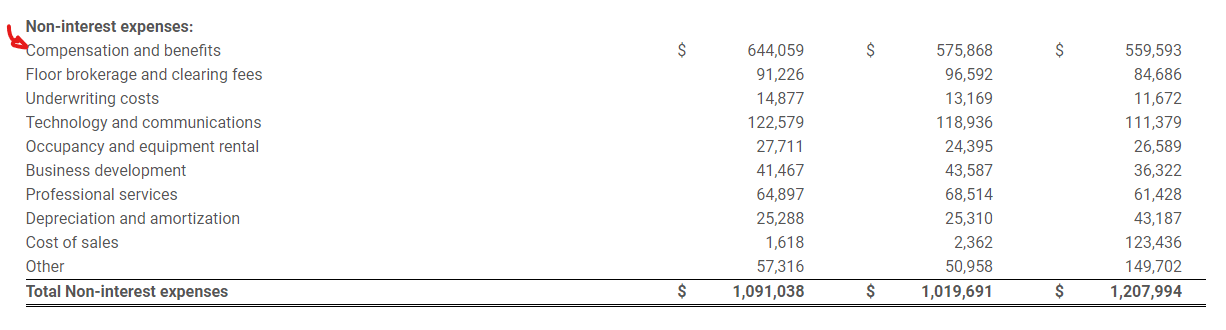

Comp expenses are indeed up quite a lot as well.

{kind=link}

And this is despite the fact that advisory revenues are suffering quite a bit YoY, although overall IB revenues are only down slightly YoY.

{kind=link}

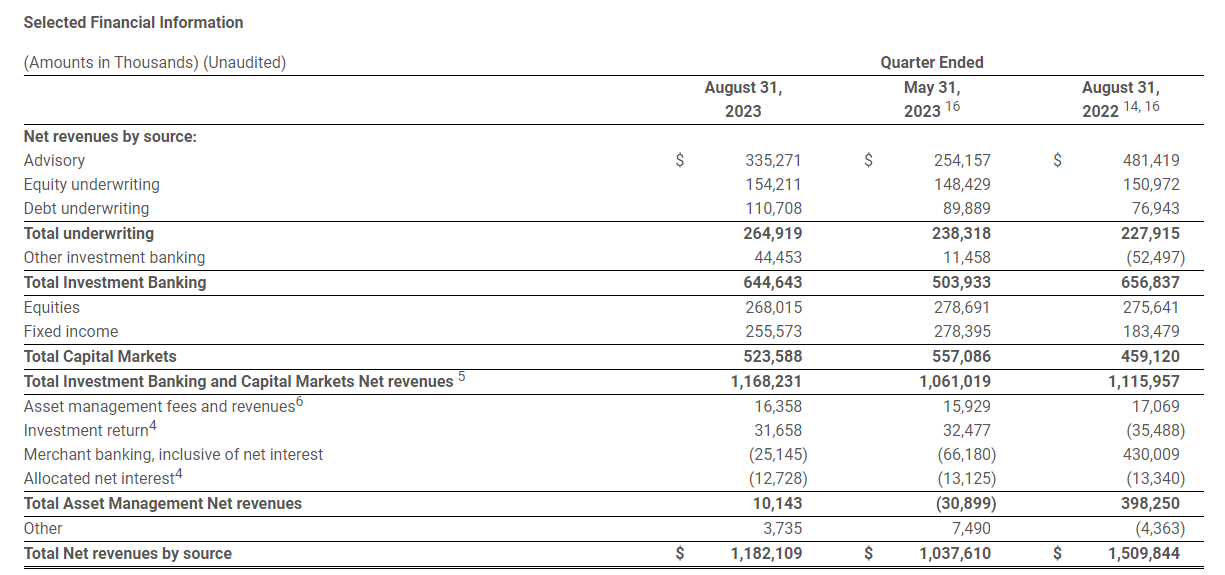

Firstly, the outstanding performance is actually in ECM and DCM, particularly ECM. DCM has had some strength due to the fact that companies are being forced to accept a higher rate environment and refinance. But ECM markets have remained very weak, and YoY revenue growth here, even if slight, is pretty remarkable as most other companies haven't since this occupation bottom out.

On advisory, we note in the coverage of some other companies like PIPR that financial sponsors like PE are really slow in coming back to market. It makes sense as the higher cost of capital environment, write-downs of the bulge of 2021 investments, and massive drypowder is forcing sponsors to be careful with the deals they make and have to fat pitch. JEF has a strong sponsor franchise, so this isn't great. Also, in general we are seeing declines in ticket sizes, and the activity is definitely skewing towards the mid-market companies which are doing pretty resiliently. JEF has mid-market exposure, but the removal of those high ticket deals that they had started to get exposure to affects the advisory revenues a fair bit.

While strategic activity is still happening, and Europe has been more resilient since the comps aren't as tough, cost of capital is still an issue for strategics too.

Bottom Line

It's clear that the many "greenshoots" discussed by analysts aren't proving to be the dramatic inflection point that some market actors may have hoped. The rebound is going to be slow, reflective of the general cost to the economy being paid for as the rate hike regime take effect - perhaps not explicitly recessionary but a sacrifice of growth and economic vigour.

On an absolute basis, multiples, where JEF's is in the mid 20x range for PE, look a little high considering the limited impulse for recovery. While Q4 is seasonally a strong quarter, how things will develop as corporate interest costs rise dramatically starting in 2024 is unclear, and with underlying inflationary factors, namely job openings growth and wage growth, still in full effect, a pivot seems to us to be wishful thinking. Growth won't be massive across the industry and the earnings yields are uncompetitive with the risk-free rates.

However, JEF has invested meaningfully in headcount, and it takes a year or two before MDs become fully productive, so there is latent earnings power in those bottom-of-the-cycle investments. On a relative basis too, the company is cheaper than PIPR, which has similar businesses, including brokerage, and is performing as well if not worse than JEF in terms of resilience. It's a nice company, but we have better options currently in the markets.

For further details see:

Jefferies: All In MD Count