PIPR - Jefferies: ECM Recovery Will See A Bit Of A Stoppage In Q2

2023-06-22 12:48:48 ET

Summary

- Considering the timing of the period close, which was still weak and volatile, we think that the idiosyncratic ECM jump could see some stoppage in Q2.

- Still, Jefferies was able to benefit in equities in its capital markets business on the volatility, and that should continue.

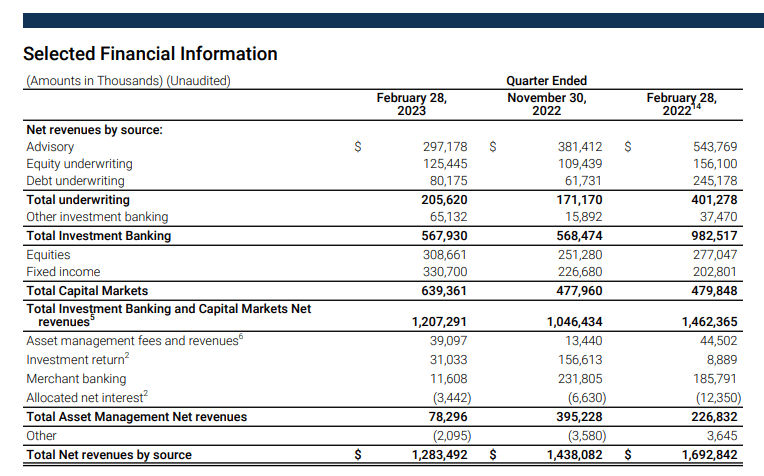

- Investment and merchant banking revenues, the principal capital businesses, are seeing huge declines due to divestments of major holdings Vitesse and Idaho Timber.

- But those were disposed attractively with respect to shareholders so that delta doesn't matter.

- However, with reference to other advisors, the Q2 including March is likely to see continued pressure on advisory as well, and at best a return to January levels in the latter half.

Jefferies Financial Group ( JEF ) has been an interesting stock because of the disposals planned for its merchant banking portfolio. Most of those have been carried out, so what's left is really the commentary on its capital markets business and advisory. Overall, the Q1 ended in February, so we haven't seen the effects of the banking troubles on already quite weak results. While Jefferies stood out in the Q1, the Q2 report next Tuesday should reveal some stoppage there, and also in advisory, which has remained weak. Overall, middle market picks remain better positioned in an iffy M&A environment, and Jefferies isn't that.

Moving Parts and Q2 Preview

The Q1 was the recent earnings, and its books close at the end of February. That means banking troubles are not reflected in the quarter.

Piper Sandler ( PIPR ) references its own ECM business as coming to a screeching halt at the beginning of March when fears of a financial meltdown arose. Jefferies actually had a surprisingly good showing in ECM in Q1, where competitors really had very little going on . But the beginning of March will probably mean some stoppage for JEF, in DCM markets too.

{kind=link}

Advisory also struggled in March for competitors, although they reference that by April activity largely looked encouraging, but in the current context encouraging just means meeting January and February standards, where activity is still somewhat high relative to historical averages but nonetheless a substantial drop-off from peaks. With JEF being more large deal focused than some of the other companies in our coverage, and their Q1 advisory performance already looking pretty poor, we expect more of the same for Q2.

Jefferies had a strong capital markets showing consistent with other companies that offer these services, and this has all largely been because of volatility in markets supporting spreads in these businesses. Jefferies outperformed here. While the fixed income business is likely to suffer in Q2's March as investors stay on the sidelines, and less inventory moves, equities should see similar outperformance as in Q1, especially as things then pick up in the markets.

Bottom Line

Overall, the revenue streams look like they're going to be worse off sequentially due to the March banking issues, where a relatively small capital markets business is unlikely to offset. Using the Q1 0.56 EPS as a ceiling to Q2, we get something like a 13x run-rate PE on the stock assuming a seasonal Q4 pickup, which isn't too bad from a valuation standpoint, but also is not exceptionally compelling considering valuations you can find on other advisors. This multiple could become more compressed if M&A and capital market conditions improve in the latter half of the year, particularly with sponsor activity, which has been some of the most depressed as they digest higher financing costs. However, some analysts have pointed out that a shift away from merchant banking could increase compensation costs longer term, since merchant banking is a cheap business to run on a human capital basis. So there are puts and takes here.

The main shortfall in income has of course been the merchant banking and principal investing business after the sale of Idaho Timber and Vitesse Energy ( VTS ) which were meaningful EBITDA contributors for the merchant banking business. Also, there were no repeat principal investment performances that could keep that revenue up. This is a permanent shortfall, since VTS was paid out as a spin-off to shareholders and the merchant banking portfolio is substantially smaller than it used to be.

JEF isn't a bad pick, but there are other names out there in the sector that go for a lot cheaper on a TTM and a FWD basis. The Seeking Alpha valuation rating gives JEF a D+ grade for PE , and we largely agree with the sentiment. While there are still assets within JEF that could eventually be realized, with private markets being so low in turnover right now, this isn't the moment to be considering the margin of safety they provide for JEF. JEF could be a better play for when those markets are confirmed to have opened again, with JEF being more reflexive to them than some of the other advisors out there who don't have principal investment businesses.

For further details see:

Jefferies: ECM Recovery Will See A Bit Of A Stoppage In Q2