JEF - Jefferies Financial Group: Streamlined Core Activity Focus Enables Superior Capital Returns

2023-05-12 16:45:29 ET

Summary

- Over the past year, Jefferies has seen returns superior to the capital markets industry (KSX: +0.21%) but trailing the general market (SPY: +4.78%).

- This reflects a general apprehension against financial stocks in lieu of higher interest rates and recent banking crises, as well as declines in indices which hold Jefferies.

- In spite of this attitude, Jefferies has rebounded from negative FCF in 2022, to positive levels of TTM cash flow, borne of mean reversion the stock has yet to follow.

- To ensure a more nimble organization able to navigate macro headwinds, Jefferies has focused on streamlining the company to focus on investment banking, capital markets, and asset management.

- The combination of said corporate strategy alongside a discounted price leads me to rate the company a 'buy'.

Jefferies Financial Group ( JEF ) is a New York-based integrated investment banking and securities firm, with activities across asset management and capital markets as well.

Its activities have enabled TTM revenues of $8.01bn alongside an EBITDA of $2.42bn in the same time period. Although these represent YoY declines, the firm has experienced QoQ performance reversions, a promising sign for future demand levels.

Introduction

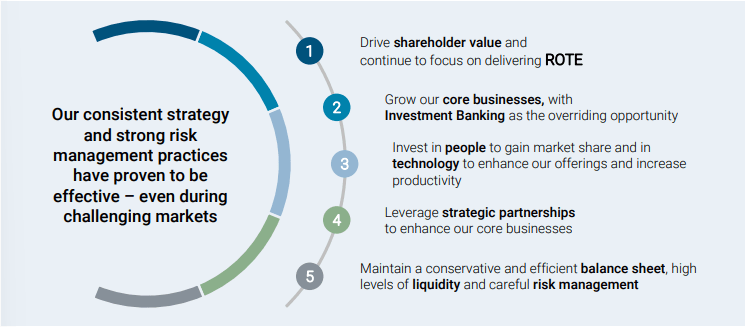

To overcome the headwinds of the present and position itself to capture greater future growth, Jefferies has identified a fivefold execution strategy including shareholder centricity, the development of core financial businesses - investment banking in particular, and the formation of strategic partnerships, enhancing core vertical offerings.

{kind=link}

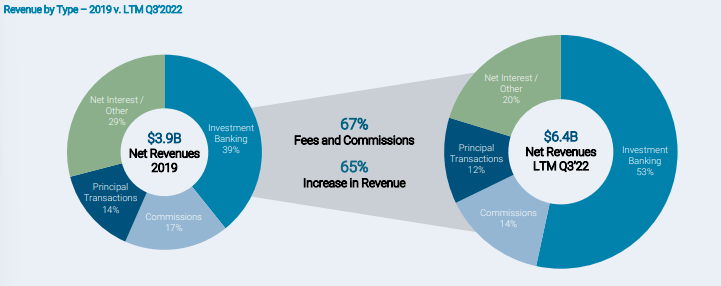

Jefferies' execution of this strategy has enabled significant revenue and investment banking growth over the past 3 years; LTM Q3 2022 revenues were 65% greater than 2019 revenue, with investment banking's share of revenues growing from 39% to 53%.

{kind=link}

Valuation & Financials

General Overview

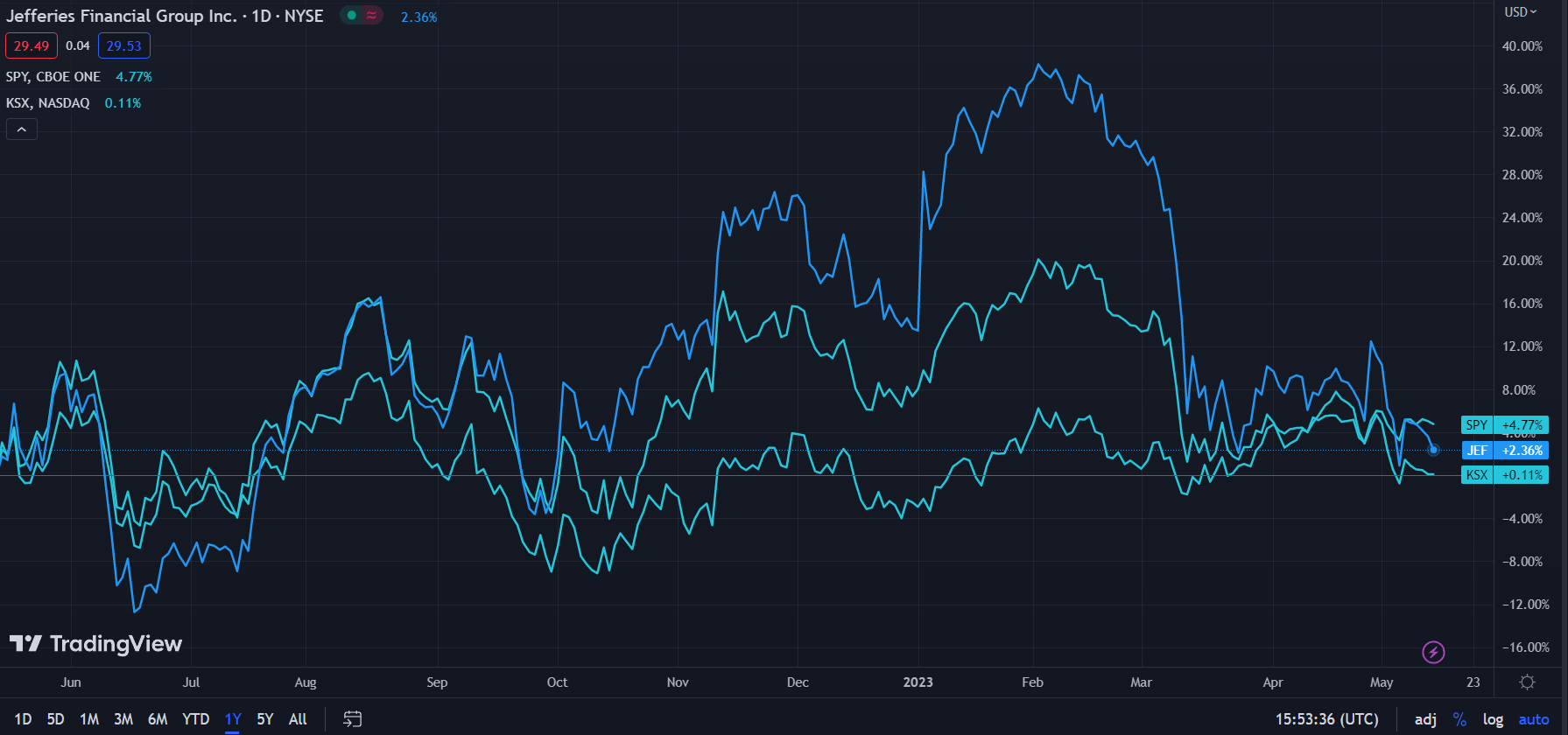

Over the previous year, Jefferies, up 2.40%, has experienced middling price action, superior to the capital markets industry ( KSX ), up 0.21%, but poorer than the general market ( SPY ), up 4.78%.

{kind=link}

To me, this seems to be a product of both rising interest rates, which have reduced M&A and IPO activity, thus harming both Jefferies and the industry, alongside banking crises. However, although Jefferies saw real declines in net income and revenue figures YoY, the growth the firm has experienced over the past few years means that despite recent challenges, Jefferies still experienced strong 2Y growth.

Comparable Companies

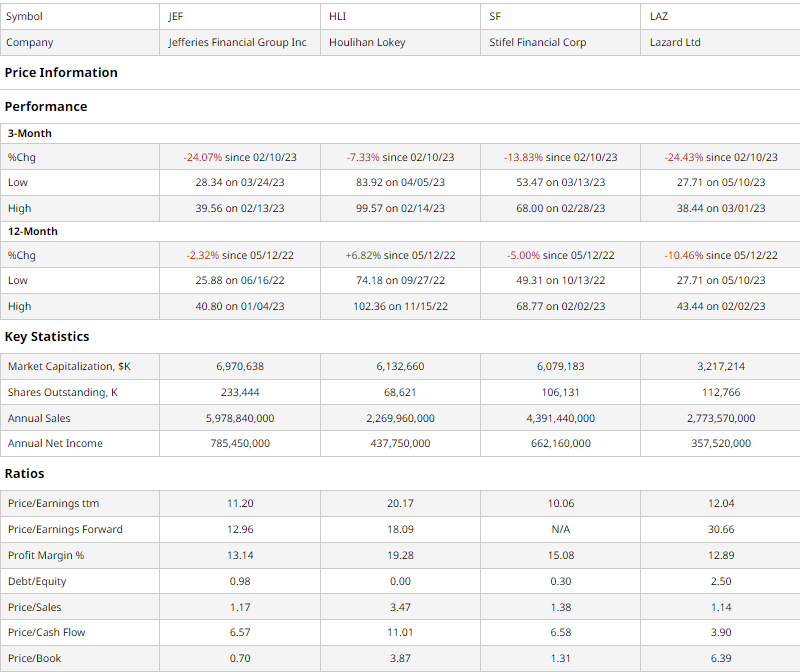

The financial services and investment banking industries can be divided into larger, universal banks, such as JPMorgan (JPM) and Goldman Sachs (GS), smaller boutiques, and mid-sized firms that often operate across only banking and maybe private equity and asset management. Among these mid-sized firms, which can be considered peers to Jefferies, are Houlihan Lokey ( HLI ), Stifel Financial ( SF ), and Lazard ( LAZ ).

{kind=link}

As demonstrated above, Jefferies has seen the poorest price performance of the past quarter bar Lazard, though the difference between the two's quarterly performance is negligible. However, while Jefferies has demonstrated multiples-based value, Lazard seems to be overvalued, with higher debt levels.

Illustrating this multiples-based value has been Jefferies' second-best P/E, P/S, and P/CF ratios.

Alongside this, the firm holds superior forward P/E and P/B, ultimately demonstrating balance sheet and future cash flow-centric growth, value, and security.

Valuation

According to my discounted cash flow analysis, the fair value of Jefferies, at its base case, is $51.46, meaning the stock is currently undervalued by 43%.

My model assumes a discount rate of ~10%, in light of a debt-heavy cap structure and the stressors of higher interest rates. Additionally, I expect a continuation of pre-2022 net margins - such that margins are not compressed by the delta of interest rates - and revenue growth to grow at ~2% a year, much lower than historic revenue growth and the expected 5Y investment banking industry CAGR of 7.1%.

{kind=link}

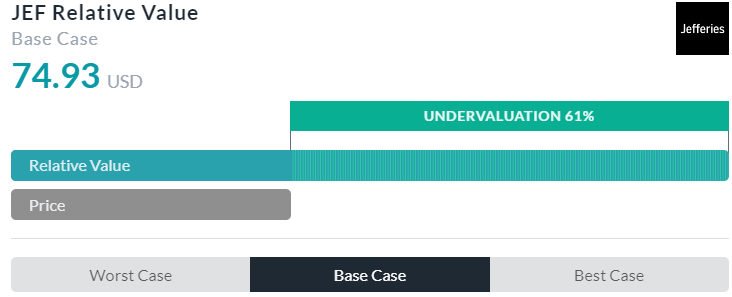

AlphaSpread's multiples-based relative valuation tool more than supports my thesis on undervaluation, calculating that Jefferies is undervalued by 61% and sustains a fair value of $74.93.

While this reflects both my thesis and what I stated in the 'Comparable Companies' section of this analysis, I believe the AlphaSpread model is somewhat skewed due to its inability to account for Jefferies' relatively high debt/equity.

Therefore, using a weighted average leaning towards my DCF, the fair price for the company is $55.62, or a 47% undervaluation from today.

Streamlined Organization Enables Margin Growth & Capital Return

{kind=link}

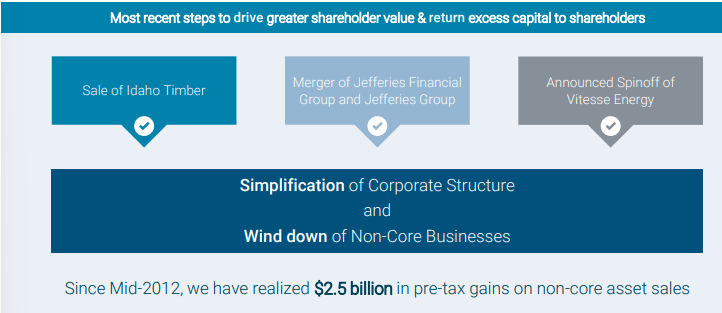

At the forefront of Jefferies' transformational long-term strategy is the organizational simplification of its business, orienting it towards investment banking, capital markets, and asset management. For instance, in the past few years, Jefferies has completed the sale of some of its private equity holdings, such as Idaho Timber while announcing the spinoff of Vitesse Energy. Alongside the streamlined merger of the Jefferies Financial Group and the Jefferies Group, this has led to $2.5bn in pre-tax gains being realized.

{kind=link}

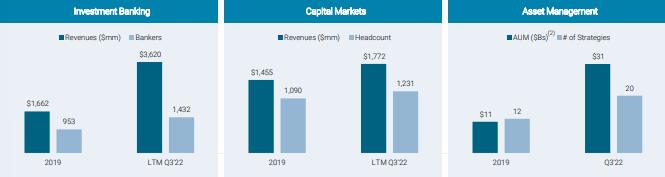

And this strategy has bore positive results, with significant growth across all three desired verticals. The high degree of specialization Jefferies now puts a premium on has additionally enabled industry-leading investment banking revenue growth, at 131.8% versus peer growth of 68.8%.

This success, in conjunction with a plethora of strategic partnerships - which have themselves enabled scale (i.e, SMBC and healthcare sectoral access), AUM growth (i.e, MassMutual), and diversification (real estate and Berkshire Hathaway (BRK.A) (BRK.B)) - have supported positive financial results, leading to a fortress balance sheet. Jefferies operates with >$11bn in liquidity and 3.8% of financial instruments owned are level 3 assets, meaning a vast majority of assets are effectively liquid and simple to value.

Jefferies 2022 Annual Presentation

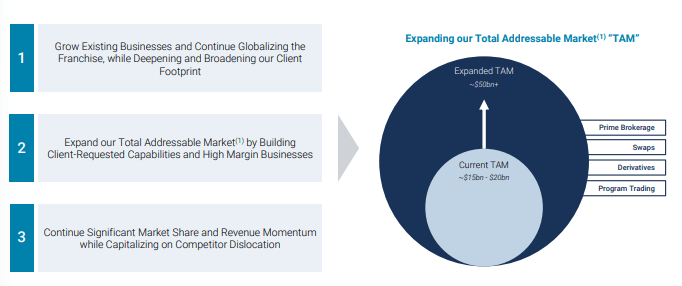

Jefferies operates with a disciplined capital deployment strategy, maintaining a 4.02% forward dividend yield, buyback authorization of $250mn, and a focus on organic growth. Thus, by reinvesting in core businesses and their growth, expanding headcount in different geographies, and capitalizing on current competitor dislocation, the company is scaling up from a TAM between $15bn-$20bn to >$50bn, cementing a level of long-term growth.

{kind=link}

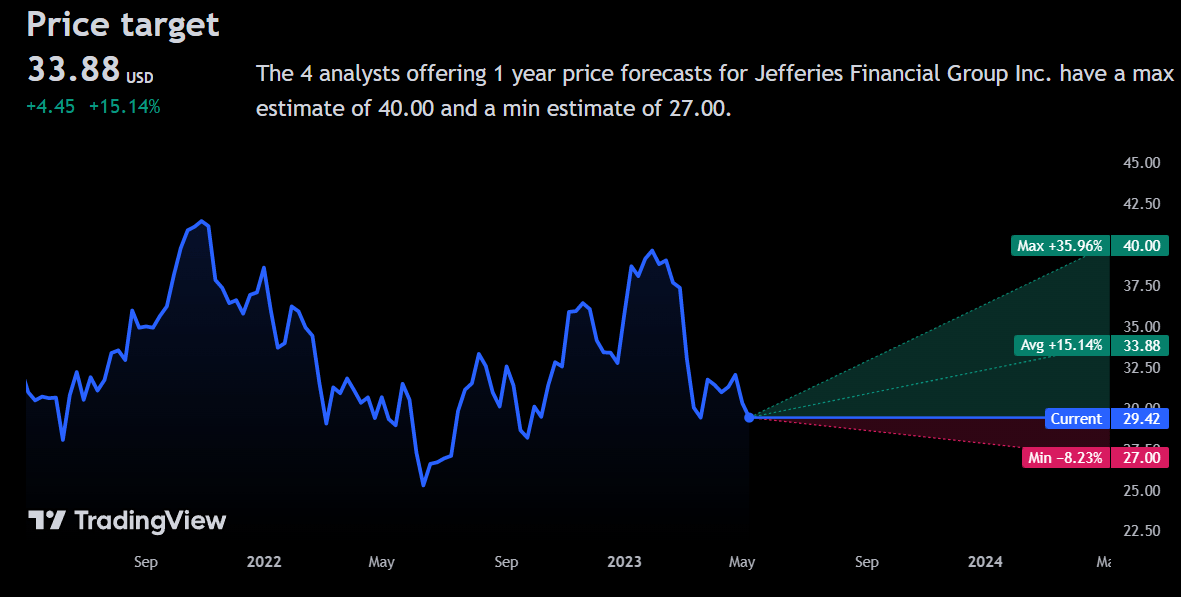

Wall Street Consensus

Analysts largely echo my bullish view of the company, projecting an average 1Y price increase to $33.88, up 15.14%.

{kind=link}

Even the minimum price decline of -8.23% to a price of $27.00 would be partially compensated by dividend income returns and is a relatively smaller decline, considering the ongoing pressures in the financial services industry.

Risks & Challenges

Multi-Party Risk

As a firm in the financial services industry, Jefferies is both exposed to risk from buy-side and sell-side firms. Therefore, with compressed demand or capital supply, or given increased financial failures, Jefferies faces a sustained risk to its cash flow and profitability.

Continued Recessionary Pressures

Although there seems to be a reversal of Jefferies' financial trajectory, resurging inflation and subsequent interest rate increases may revert the firm to negative free cash flow territory. If this is sustained at any level, it may lead to material declines in the firm's ability to operate, as demand for M&A and IPO activities would be depressed.

Risk Management Efficacy

Jefferies maintains strong asset management and balance sheet activities. However, if said activities are not sustained, and the company purchases poorer quality assets, Jefferies will be unable to maintain creditworthiness and face an inability to compete with peers in the short and long term.

Conclusion

In the short term, I expect Jefferies to grow into fair value and continue to post superior cash flow.

In the long term, the firm's transition to streamlined growth and a solid capital deployment strategy will lead the company to steady appreciation in my view.

For further details see:

Jefferies Financial Group: Streamlined Core Activity Focus Enables Superior Capital Returns