VFC - Jerash Holdings: A High-Yielder Waiting To Bounce Back

2023-08-09 13:29:19 ET

Summary

- Jerash Holdings is a contract apparel manufacturer that has historically delivered low-teens sales growth and maintained a solid balance sheet.

- The company has the potential to onboard new customers and increase production capacity as apparel sales normalize in the next 1-2 years.

- Jerash's strong balance sheet and low enterprise value in relation to sales, assets, and earnings potential provide limited downside and significant upside for the stock.

Jerash Holdings ( JRSH ) is a contract apparel manufacturer and a likely beneficiary of deglobalization. Despite the unappealing industry and alarming customer concentration, Jerash has historically delivered a low-teens sales growth, maintained a solid balance sheet and rewarded shareholders with a constant dividend.

The sales of apparel has been turbulent in the past couple of years due to the pandemic slump followed by quick recovery which led to overstocking by the retailers. The normalization of apparel sales in the 1-2 year timeframe would leverage the promising both onboarding of new customers and increased production capacity. Despite the weakness in the apparel industry, Jerash has run its capacity fully utilized.

After a brief run up in the spring, the stock price is again at its historical low from January this year. The downside is limited by the strong balance sheet and low enterprise value in relation to sales, assets and earnings potential. The tangible book value per share is significantly above the share price and the company is under-earning due to the weak operating environment. When demand normalizes there should be a significant upside for the stock to appreciate.

A manufacturer supported by free trade agreement

Jerash is a manufacturer of apparel for 19 different clothing brands. Its customer portfolio includes New Balance, Delta Apparel, American Eagle and VF Corporation. Jerash is specialized in the manufacturing of sportswear and outerwear, especially jackets. It has six factories in Jordan and four distribution centers in different locations. The company employs 5700 people and most of them are guest workers from South East Asia.

Jerash was founded in 2001, but as a listed company Jerash is relatively new, it IPOed in 2018. The fiscal year of the company ends on the 31st of March. The company’s sales growth has been rapid. The compounded annual revenue growth has been 12.1% since 2017. However, the net income margin has stagnated to 4-7% range.

Revenue and net income margin of Jerash. (Tikr)

There are naturally risks related to Jordan. Its location between Israel, Iraq and Iran is one example and listing the numerous others on a headline level doesn’t provide much value. The main pillar of Jerash’s competitive advantage is Jordan’s free trade agreements with the United States and European Union. The status provides Jerash a cost advantage compared to many other producers, but also makes the company fragile if the trade agreements cease to exist.

Market conditions are tough

On a quarter to quarter basis the business is fluctuating heavily. The company primarily fills up the capacity with the orders from its U.S. based customers with whom the margins are higher. If there’s spare capacity available, Jerash can take so-called local orders. Also, the customers can postpone planned deliveries to a further date in order to manage their working capital, which increases quarterly fluctuation.

Revenue and gross margin for the 2023 fourth quarter continued to be impacted by fewer orders from our two major U.S. customers, as well as a shift in product mix to lower margin items. We also are comparing against a particularly strong revenue quarter a year ago. - Sam Choi

The fourth quarter revenue and earnings were a bit of a disappointment. The realized revenue was approximately $2 million lower than what the company guided at the low end ($26-28 million). For the full fiscal year of 2023, the realized gross margin at 15.8% was slightly below the guidance of 16% to 18%.

The current market condition remains tough. The apparel brands and retailers still have high inventory levels and they are placing smaller orders to the manufacturers. According to the company this has pushed many of its local competitors to lay off workers or even out of the business. This could represent an opportunity for Jerash to onboard more customers or acquire capacity opportunistically. Jerash has been the only producer in Jordan to operate at a full capacity.

Growth and earnings potential is increasing under the hood

Customer portfolio is getting less vulnerable

The greatest business related risk for Jerash and its shareholders is the customer concentration. In the last fiscal year 60% of the company's revenue came from V.F. Corporation ( VFC ) and particularly its The North Face brand.

Based on Google Trends search the interest for The North Face brand has not diminished, but is following a regular pattern of spikes around Christmas sales. In the latest fiscal year results (reported on May 23rd) The North Face brand grew 17% in constant currency and 16% in the last quarter. This is encouraging for Jerash.

North Face search trend in Google Trends. (Google Trends)

Jerash has the potential and action plans in place to reduce its reliance on VF Corporation. Its production for VFC is seasonal concentrated in the months preceding the winter season. Therefore it can onboard customers whose clothing lines are for the summer season. The main question here is why it has not happened yet and how would Jerash succeed to acquire such customers now?

Jerash recently announced a joint venture with an Indonesian manufacturer Busana Apparel Company. The company painted a picture of the joint venture bringing in new customers that it has not served before. According to the press release Jerash will own 51% of the JV and will manufacture products for Busana’s international customers in Jordan taking advantage of the duty-free agreements with the EU and the U.S. The initial manufacturing of the JV is expected to commence in the second half of 2023.

These are not just empty words. In the Q3 earnings call Jerash said that Busana was a key facilitator to bring Hugo Boss to its customer portfolio, which is the first European-based customer for the company. Jerash seems to be optimistic that other brands will follow, but reminds that lead time from the start to actual delivery takes six months to a year. To accommodate new demand Jerash has added 15% of capacity by expanding its existing factory with an investment of $1.1-$1.3 million.

On the positive front, our joint venture with Busana Apparel Group is progressing well. Initial feedback from Busana's global branded customers indicate their keen interest in geographically diversifying production to Jordan from Asia, in part, to take advantage of duty-free agreements with the U.S. and other countries. We anticipate production as part of the joint venture to start in the second half of the current fiscal year. -Sam Choi

Furthermore, Jerash is ramping up production for Skechers (500 000 pieces annually and initially ) and for Timberland. In the current fiscal year 2024, the company expects the volumes of Timberland apparel to double.

Deglobalisation is boosting the business

In the long term Jerash might benefit from deglobalisation. The management has multiple times mentioned that many brand customers have expressed their interest in shifting their production from Southeast Asia to Jordan. Furthermore, Jerash is beneficially located near the garment producing countries in the Middle East and North Africa. Traditionally China and other Asian countries have been the main suppliers of garments. This is likely an advantage when brands make decisions between different contract manufacturers.

Fortunately, we continue to receive inquiries from other premium brands as global brand trends remain to diversify supply chains away from Asia, especially China. - Eric Tang

Unfortunately deglobalisation presents a risk as well. The most obvious one is that VFC could come to a conclusion that its sourcing has too much geographical weight in Jordan. There’s no contract between Jerash and VFC. However, the relationship with VFC has lasted since 2012, so it would probably be risky for VFC to shift the volumes to another supplier. Furthermore, according to the fiscal Q2/2023 earnings call one of the manufacturing partners of VFC is facing financial trouble, which is positive from Jerash’s perspective.

Consumer spending on discretionary items is a near term risk for Jerash. As most of the apparel manufactured by Jerash ends up in the U.S. market, consumer spending is a key trend to watch. Although excess savings has been mostly consumed, the wage growth is picking up to match inflation, but spending power could be subdued in the near term. Retail sales are expected to weaken for the rest of the year after a brief peak. This is why the time horizon of the investment case is most likely in the span of one to two years.

One of the factors pressing down Jerash’s net income has been the increase of the tax rate. Prior to the year 2020, the tax rate was 11% in total. Since the beginning of 2020 the tax rate has increased to 15%, in 2021 to 17% and in 2022 to 19% or 21%. Furthermore, Jerash was exempted from a local sales tax of 16% in Jordan. According to the 10-K for fiscal 2023 the exemption expired in February 2023, but according to the latest 10-K the exemption was again extended to February 2024.

Investing for the future growth

Throughout the latest five quarterly calls the management has been highlighting that their production is running at full capacity. The product and customer mix is fluctuating which results in varying financial performance. Once the volumes from more profitable customers return, the combination of better margins, new customers and higher capacity should trickle down to the bottom line.

In the end of 2021 Jerash completed the acquisition of MK Garments and the factory and land underneath the operations (Kawkab Venus) for a total of $4.9 million. The acquisition brought in 500 additional workers and Jerash said it increased production capacity by 20%. Considering the company’s track record of revenue growth, an investor could be rather content with the investments in the capacity expansion, which has constantly grown as presented in table 1 in the beginning of the article.

In the fiscal year 2024, which is now ongoing, the company expects to do $2.6 million worth of capital expenditures, which is approximately $11 million less than in the previous year. This will help Jerash to bridge over the tougher times. In the following year the company expects to invest $8.5 million. Capital expenditures have averaged $3.6 million per year.

Solid balance sheet without net debt

Jerash has a strong balance sheet and its book value and tangible book value are $5.55 and $5.5 per share. The majority of the balance sheet consists of inventory (39%), cash (21.2%) and PP&E (26.7%, accumulated depreciation of 13.7% of total assets). Solid balance sheet should provide a floor to the share price as long as the demand doesn't dry up completely. However, as so much capital is tied up to the balance sheet and Jerash owns many of its assets, returns on capital have been low.

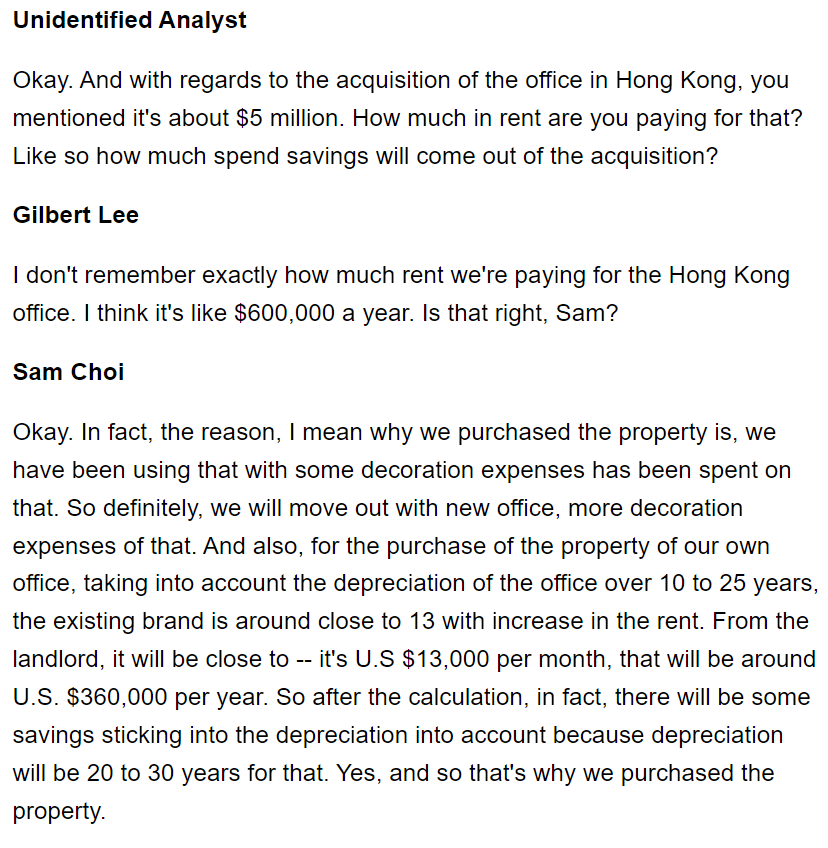

In August 2022 Jerash made an odd acquisition of office space in Hong Kong for $5.1 million. Jerash has been using the space for many years and paid a $360 000 annual rent. According to the fiscal Q1 2023 earnings call , “the board made the decision to take advantage of the fallen real estate prices and save on rent”.

Unfortunately, in the earnings call there was discrepancy between what the CFO and the CEO communicated regarding the actual benefits. From my point of view this is a potential red flag and investing in office space in Hong Kong limits the company's ability to invest in its core business and capacity in Jordan.

Figures behind the investment into office space in Hong Kong. (Q1 2023 earnings call transcript.)

{kind=link}

Concentrated ownership

The largest owner of Jerash is Merlotte Enterprise, which owns 30% of the company. Merlotte Enterprise is controlled by Choi Lin Hung, the CEO and Chairman of Jerash. He also owns 4.2% of the stock directly. Among the largest owners there are two other management team members holding 9% of the stock combined. Furthermore there are two individuals, Ka Lun Chiu and Lee Kian Tijauw, who own approximately 15.5% combined. Concentrated ownership is a great driver to boost the share price when demand environment normalizes.

Choi Lin Hung has an earlier background from the banking industry. Therefore it's rather easy to speculate that Jerash could be a potential acquisition target for large Asian manufacturers such as the JV partner Busana, which is several times larger than Jerash on different measures. Busana could be an interested buyer to reduce its own geographical risk and serve its customers better. Now, it has to share the profits through the joint venture.

In September 2021 the company made a secondary stock offering of one million shares (currently there are 12.4 million shares outstanding) at a price of $7. The offering was conducted at the time when Jerash was about to complete its acquisition of MK Garments. Merlotte Enterprise, the largest shareholder, sold 400 000 shares in conjunction with the offering. The offering diluted the shareholders at the time, but as for now, the company expects to fund its investments from the operational cash flow.

When apparel market normalizes so should the shares

Due to the bumpy earnings and cash flows, high and in my opinion partly questionable investments of late and the key risks, Jerash is relatively difficult to value. The main risks and the qualities of the business don’t warrant high multiples for the stock. Nevertheless, the main question here is what could the earnings look like in more normal conditions after one to two years, when people start buying clothing again and supply chain situation normalizes?

-

Typically Jerash has generated approximately 25 000 dollars of revenue per employee. Since its capacity and revenues are tightly correlated to the number of employees, this number is a convenient way to model revenue development.

-

Between 2019-2022 its net income margin averaged 5.8%. If we include the weak 2023 the average is 5%.

-

In 2023 the company had 5500 employees. From 2019 onwards the company has hired on average 560 employees per year.

-

According to Tikr the average forward looking P/E-multiple has been 10x since its listing. Due to the change in the interest rate environment, it’s safer to look at what the price of the shares would be at a significantly lower multiple.

-

Based on these historical figures, we can model what the future could look like in terms of growth and profitability. In a bear case the company doesn’t succeed in its growth initiatives and the revenues stay stagnant. This is what the company is currently guiding for fiscal 2024.

-

In terms of profitability, in a base case we would assume that the profitability returns to a slightly lower level assuming that the new business is not as profitable as the business with VFC. In a bull case one could argue that the higher volumes lead to better profitability and the growth investments gradually slow down. In a bear case higher taxes and lower gross margins could pressure the net income margin to a lower level.

-

Assuming a net income margin of 5.5%, growth scenario of 5800 employees and a P/E of 9x, we would arrive at a target price of $5.4 per share.

Stock price in different scenarios based on net income margin. (Author.)

Due to the weak fiscal 2023 the P/E-ratio of Jerash is back on a high level. Deducting the cash, which is partly restricted, the P/E is greatly reduced. On operational cash flow basis the stock still looks attractive.

When looking at the multiples where the denominator is more stable such as sales and book value the stock appears historically very inexpensive. On an EV/EBIT basis the stock doesn't command a high multiple.

There are two analysts following the company with an average target price of $6 implying an upside of 67%. As usual the target price has inched lower along with the stock price.

Steady but high dividend yield

Jerash has been paying a quarterly dividend of 5 cents per share since its listing. 20 cents annual dividend translates to a dividend yield of 5.4%. Against the weak earnings the payout ratio is currently 105%. Due to the decline of the share price, the current yield is significantly higher than the five year average of 3.4%.

In addition to the dividend the company has been buying back shares under a program that expired at the end of March. In the third fiscal quarter the company repurchased 1.3% of the shares outstanding at an average price of $4.8. Despite the buybacks the number of shares outstanding has grown. The buybacks are limited due to the low free float and trading volumes.

Conclusion

The nature of Jerash business, industry characteristics and the company specific risks don’t warrant much of a multiple expansion from its typical trading range.

However, there’s no reason to expect that the company couldn’t return to normal profitability levels when the operational and demand environment normalizes in a medium time frame. Jerash has very promising opportunities for growth, many of its weaker competitors are going out of business and the company is derisking its business profile. For these reasons Jerash appears an attractive investment for a risk tolerant investor.

Jerash is about to report its Q1 2024 on August 9 before the market opens.

For further details see:

Jerash Holdings: A High-Yielder Waiting To Bounce Back