JBLU - JetBlue Airways Can't Get Airborne

Summary

- JetBlue Airways generated financial results that were at the low end of the U.S. airline industry during the pandemic.

- JetBlue is pursuing two major strategic initiatives that are under federal review.

- JetBlue and other low cost carriers are facing a more challenging cost environment.

JetBlue Airways ( JBLU ) burst on the airline scene over 20 years ago with the promise of offering a more upscale leisure product in the New York City market which had not participated in low cost carrier expansion that had taken place in many other parts of the country. The weakness of the legacy carriers in the post 9/11 environment provided fertile ground for JBLU’s early growth which was facilitated by the gifting of dozens of slot pairs at New York's JFK airport which also served to ensure that other carriers could not duplicate JBLU’s strategies. JetBlue expanded to Boston and quickly became the dominant carrier there even without slot controls; Delta ( DAL ) and US Airways both had large operations at Boston pre-C ovid but cut them in the post 9/11 environment creating an opening for JetBlue. While JBLU’s network from the Northeast to Florida and the Caribbean and to the west coast grew, JBLU’s profits hit plenty of rough spots amid a series of executive changes. For brief periods during the last 10 years, JBLU’s profit margins were industry-leading and the company was considered a darling of the airline industry. The company has fared below average financially among U.S. airlines during the pandemic and has still not obtained or even guided to generate the margins that other airlines are generating in the post-C ovid environment.

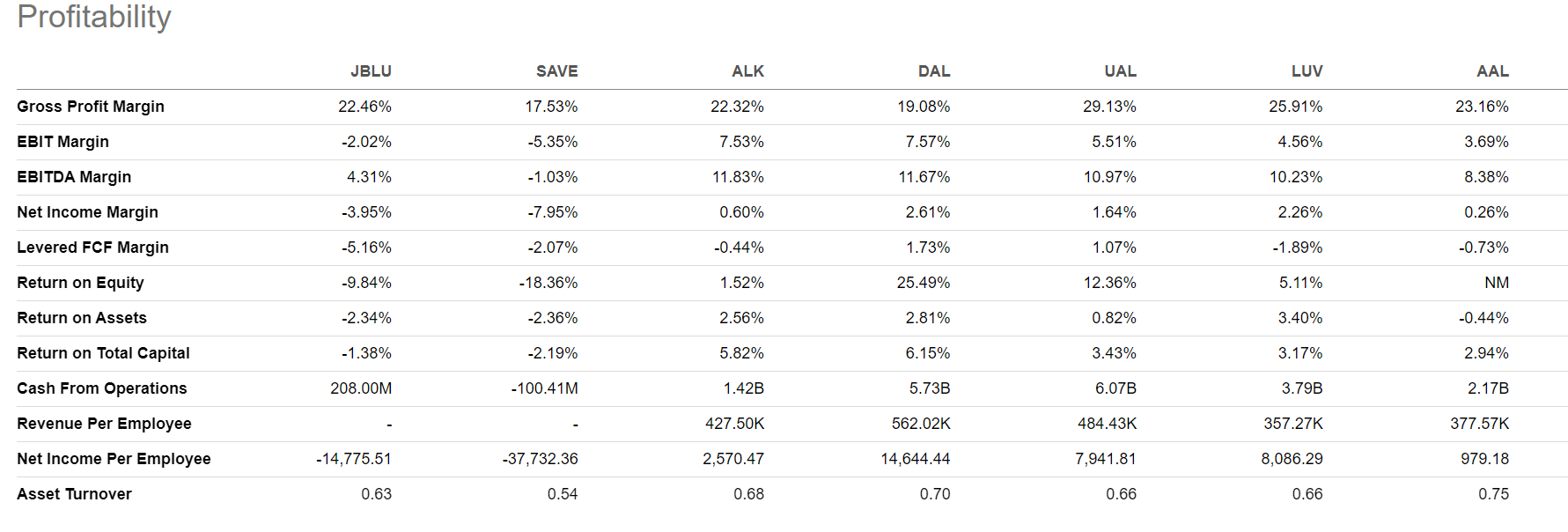

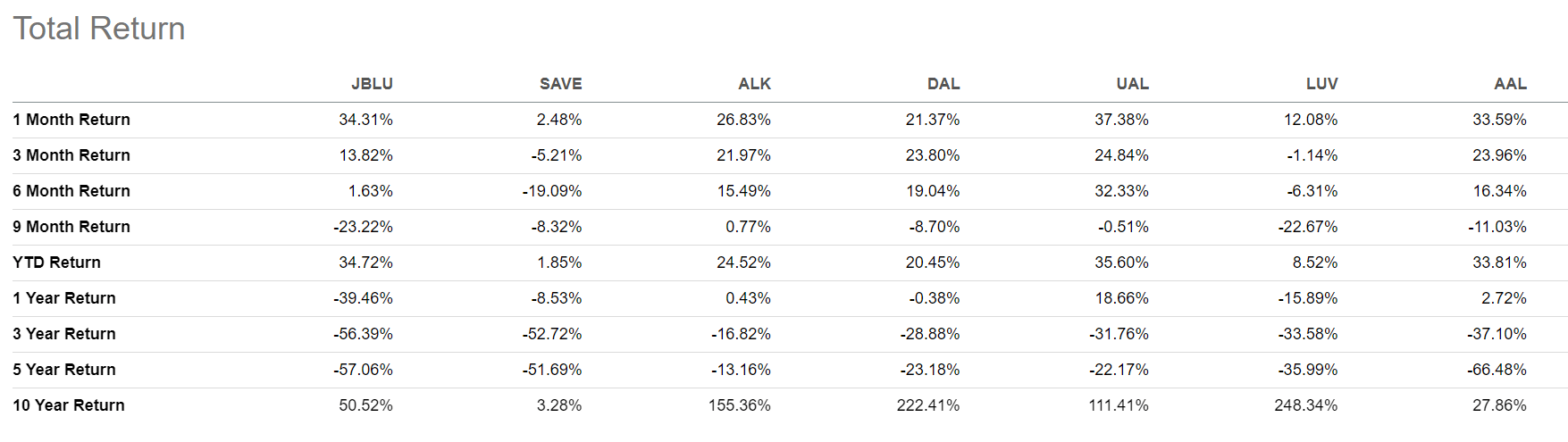

JBLU stock has fared worse than DAL, LUV (Southwest), and UAL (United) over the past year even with LUV’s fourth quarter losses and expected losses for the first quarter of 2023, while Delta and United posted profits in the fourth quarter which are expected to continue even at reduced levels in the first quarter. JetBlue posted a small profit in the fourth quarter and is guiding to a loss in the first quarter of 2023 and a low level of profits compared to its competitors for 2023 as a whole.

JetBlue 4Q2022 earnings (JetBlue.com)

JBLU is still worth just under $3 billion in market cap and is still considered a major airline by U.S. Dept. of Transportation standards but is becoming increasing irrelevant as even a trading stock in an airline industry which struggles to convince investors that it is worthy of being viewed as a long-term investment. This article serves as a review of JetBlue’s strategies and performance, its competitive positioning both as a stock and in the marketplace, and its longer term strategies – all to help determine if JBLU is worthy of investor consideration.

{kind=link}

JetBlue’s Business Model and Foundational Challenges

JetBlue determined from its founding to elevate the airline experience and largely succeeded in doing so. While seatback individual entertainment systems were largely confined just to long-haul international aircraft at the time of JBLU’s founding, JBLU added them to every seat, later adding free high speed Wifi before other airlines. It offered more legroom and no-added-charge services and added quirky features like its unique blue potato chips. However, most airline products can be duplicated and Delta added in-seat audio video systems to the aircraft it used to compete with JBLU as Delta designated JFK airport as a hub and began aggressively growing where it is now the largest carrier. Delta has since expanded in-seat entertainment systems to nearly all of its fleet and just rolled out free high speed internet across its domestic fleet. Other airlines including United are now adding similar systems to their fleets.

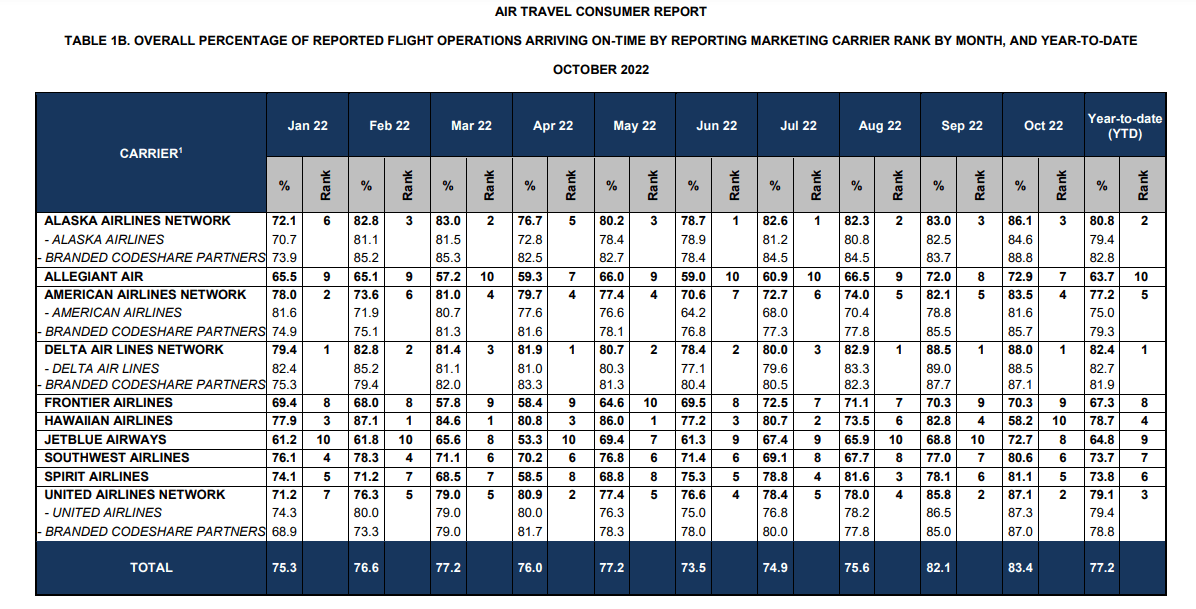

In the face of cost pressures, JBLU has added fees and added seats to its aircraft, reducing passenger space. Most significantly, JetBlue has been dogged for years as being an unreliable operator, recording one of the most persistently low on-time ratings according to DOT data. Because business travelers are heavily focused on getting where they need to be reliably and quickly, JBLU has failed to attract business passengers in amounts necessary to support its escalating costs which are growing as a result of its maturity as a business.

US Airline On-Time Performance (U.S. DOT Air Travel Consumer Report)

{kind=link}

JBLU’s network was originally focused on leisure routes up and down the east coast to sun destinations and later to the west coast. Other airlines were able to match or undercut JetBlue’s fares and also to add enough capacity to make it difficult for JBLU to gain a revenue premium – which DOT data says it generally does not get. JetBlue has expanded into the Caribbean and the northern tier of Latin America where fares have been higher but other airlines including ultra-low cost carriers such as Spirit have done the same. Spirit ( SAVE ) duplicated much of what JBLU built at Ft. Lauderdale and offers lower fares. Delta renewed its focus at Boston and has overlaid many of the routes that JBLU flies.

JetBlue recently added service to London, helping to compete more effectively with the legacy carriers that have hubs in the same metro areas as JetBlue. JBLU intends to expand to Paris in 2023 and additional European cities using the longest range Airbus ( EADSY ) A321NEOs. JBLU’s European service revolves around its Mint lie-flat business class product which has successfully raised its average fares on its JFK and Boston transcontinental routes to levels much closer to what the legacy carriers receive. JBLU believes it can offer discounted business fares featuring Mint although the economic success of long-haul narrowbody aircraft remains to be seen since widebody low cost carrier service by other carriers has not been financially successful.

Competitive Considerations

From a competitive standpoint, JBLU has few advantages since its network, fares, and product can be and have been duplicated by other carriers, most of which are larger than JBLU. The legacy carriers offer more extensive networks and premium cabins across their fleets, richer loyalty programs and amenities such as airport lounges that are sought by business passengers.

From a financial and competitive standpoint, one of the best comparisons between JetBlue is with Alaska Airlines ( ALK ). While JBLU operates in the northeast corner of the U.S., ALK operates mostly in the northwest with its headquarters and primary hub in Seattle. Neither location is great geographically to serve as hubs but Seattle is essentially a single airport metro area while New York City – a much larger metro – has three major airports making it more challenging for JBLU to achieve a leading position in the NYC metro area. ALK is the largest carrier in Seattle and the Pacific Northwest as well as in its namesake state of Alaska. Delta is the largest direct competitor to ALK at Seattle and across its network; Delta is larger than JBLU in New York City but the two are similarly sized in Boston. Delta’s strategy for competing with both carriers is to tout its premium products and global network. ALK does a better job of getting revenue similar to DAL than JBLU does in part because ALK is less focused on high volume leisure routes. ALK is much closer to having a moat than JBLU, supporting Warren Buffet’s belief that companies need to have advantages which competitors cannot duplicate in order to maximize margins. Neither ALK nor JBLU operates widebody aircraft and ALK does not fly long-haul international flights although it has flown to Asia before.

The real comparison comes in financials. ALK was also a financial darling of the industry when the legacy carriers were financially struggling. Trying to gain size significance, ALK acquired San Francisco based Virgin America but has dismantled large portions of the latter’s former network as Alaska has retrenched to its core strengths. ALK has also returned to its single Boeing ( BA ) 737 mainline fleet strategy after acquiring Airbus aircraft as part of the merger. ALK’s financials have begun to strongly rebound as it puts the merger behind it. Even though the two have similar revenues and numbers of employees, ALK’s market cap is more than twice JBLU’s and ALK has been profitable over the past year, something which has evaded JBLU.

ALK is technically a legacy carrier, having flown interstate service before the U.S. domestic airline industry was deregulated in 1978. ALK has aggressively grown to keep labor costs down and so functions more like a low cost carrier even though it offers premium cabins and lounges like legacy carriers. Both ALK and JBLU have multiple foreign airline partners to whom they sell seats to connect passengers to/from the U.S.

At a higher level, though, the post-C ovid era is proving to be much more difficult for low cost carriers as a group because of increasing costs which legacy carriers are better able to pass along to customers through their higher fare structures and greater business traveler focus. Many analysts said throughout the pandemic that the legacy airlines would be handicapped because of their global route systems which were heavily shuttered, but I countered that notion, including in this article, noting that all carriers compete in the same domestic marketplace and there was significant overcapacity in the domestic market throughout much of the pandemic, preventing anyone from making significant profits, if any at all. Now that global markets are reopening, the legacy carriers are adding significantly more international revenue than low cost carriers are able to add domestic revenue and the legacy carriers aggressively reduced costs and increased their efficiencies during the pandemic. Thus, financial comparisons between JBLU and the global/legacy carriers – AAL, DAL, and UAL – will be harder while ALK’s ability to act like a legacy with a greater focus on business travel, a higher quality product, and better moats in its key markets has allowed it to increase margins and that is expected to continue.

JBLU faces a tighter labor market, especially for pilots and mechanics. The carrier’s pilots agreed to a new contract that boosts pay in line with larger carriers; DAL is the only one of the big-4 that has come to an agreement on a new labor contract with its pilots and Delta’s pilots are voting on that proposed contract at this time. While JBLU’s pilot pay increases put its pay relatively in a similar position as DAL’s proposed rates, there is growing evidence that low cost carriers are losing pilots at an escalating pace to the big-3 global airlines because they offer higher career earnings as a result of operating international widebody aircraft. JBLU did get a bit of good news on the labor front as one group of ground employees rejected a unionization attempt by the International Association of Machinists. Nonetheless, labor cost increases are more difficult for low cost airlines to pass along to consumers because of their simpler, lower fare structures of low cost carriers compared to legacy airlines.

Regulatory Hurdles

More than any other U.S. air carrier, JetBlue faces a grueling review of its most important strategic initiatives. Because JBLU has recognized that its current strategies are not working, they engaged in two initiatives in the past couple of years to change strategies and in the process has triggered significant federal review.

JetBlue’s first major initiative that is under the current review of a federal judge is its Northeast Alliance with American Airlines ( AAL ). American and JetBlue have had a checkered history with JBLU adding service in some of AAL’s key markets, resulting in AAL leaving many of them, only for AAL and JBLU to develop cooperation agreements. The Northeast Alliance originated with the DOT’s review of American’s usage of its slots at New York’s JFK and LaGuardia airports. The DOT noted that AAL had failed to use its slots to acceptable levels for several years pre-C ovid resulting in consumer harm as AAL held onto valuable assets which were not used and were not made available to other carriers. The federal government leveled the same charge against United Airlines at Newark in the mid-2010s; because UAL controlled more than 70% of the slots at Newark, the FAA (which manages the U.S. slot portfolio since slots are intended to be used to control airport capacity) and DOJ decided to end the strictest slot controls at Newark which ultimately resulted in a flood of new low cost carrier competition. Because JFK airport is the largest U.S. gateway for foreign carriers and because American is not the largest slot holder at JFK (Delta is), removing slot controls would do more harm to other carriers than it would to stimulate new demand than would come from better slot compliance by American. American turned to its “friend” JetBlue and created the Northeast Alliance which was to be a joint venture arrangement that would allow American and JetBlue to connect passengers to each other, jointly schedule flights and share revenues from NYC and Boston under antitrust immunity, and swap slots between themselves as necessary in order to jointly create schedules. The DOT, under its antitrust immunity which is usually reserved for evaluating arrangements which U.S. carriers have with foreign partners, signed off on the deal.

It wasn’t too long into the operation of the approved Northeast Alliance ((NEA)) that the Dept. of Justice sued to block the arrangement. The DOJ notes that it never allows two U.S. airlines to obtain antitrust immunity in a challenge to the DOT’s approval of the NEA. The DOJ specifically objects to the ability of AAL and JBLU to coordinate schedules and revenues and swap slots given that the two combined become the largest carrier in NYC and Boston. Arguments before the judge ended in the fall of 2022 and a decision could come from the DOJ’s request to block or amend the NEA at any time. While the DOJ has lost several recent high profile antitrust cases, the airline industry is viewed skeptically because of its high profile and direct consumer nature. It is worth noting that American has a codeshare and cooperation agreement with Alaska Airlines for west coast flights but there is no antitrust immunity and no west coast airport is federally slot controlled. ALK recently joined the oneworld airline alliance of which American is a founding member while JBLU is not a part of any alliance.

The chances of changes to the Northeast Alliance are particularly heightened because of JBLU’s merger proposal with Spirit Airlines. SAVE originally had agreed to a merger proposal with Frontier Airlines ( ULCC ) which is also an ultra-low cost carrier; JBLU is considered a low cost carrier. JBLU ultimately won a bidding process and offered SAVE stockholders significant consideration for SAVE to choose JBLU over ULCC. JBLU’s justification for the merger is that it will allow JBLU to grow to a size large enough to better compete with the big-4 airlines. There are a number of characteristics of the JBLU/SAVE merger that raise even more red flags from a consumer standpoint than the typical airline merger including the fact that JBLU fares are higher, meaning that taking SAVE’s assets to increase JBLU’s size will raise fares for consumers. In addition, JBLU puts fewer seats on comparable aircraft models than SAVE so capacity will be reduced. SAVE has a much larger national footprint that is less concentrated in major cities than JBLU but JBLU and SAVE are the two largest carriers at Ft. Lauderdale airport. A number of legislators have expressed their objection to the JBLU/SAVE merger and a number of state attorneys general have also joined the DOJ in challenging the deal.

The combined impact on the competitive and consumer impact of both the Northeast Alliance and the JBLU/SAVE merger is unprecedented for a single airline in U.S. airline history to defend. While JBLU has provided every indication that it intends to pursue both initiatives, the chances are very, very low that both strategies, as they presently exist, will survive together. JBLU has offered to divest all of SAVE’s assets in NYC and Boston as part of its merger – undoubtedly to quell objections about the NEA – but SAVE doesn’t fly to JFK and only operates about a dozen flights/day at LaGuardia. Further, American is the largest airline at Miami, the closest major airport to Ft. Lauderdale, and JBLU proposes nothing to correct the effective combination of the three carriers to the largest markets in the northeast which the NEA does cover.

The DOJ has only recently started collecting depositions in its case against the JBLU/SAVE merger and the merger proposal expects that a decision on the merger will not be rendered until 2024. JBLU is required by the merger agreement to pay consideration to SAVE stockholders throughout the regulatory review process in addition to potential breakup fees if the merger fails. In the meantime, JBLU must continue to operate its airline that is increasingly being marginalized by more powerful global airlines that are running better operations and are generating higher margins than JBLU.

{kind=link}

{kind=link}

While there are no indications that investors should sell their shares due to impending bad news, the chances are high that JBLU will suffer one or more strategic defeats during the next 12-18 months and will be forced to negatively revise its business plan. Given the uncertainty that JBLU faces as its two major strategic initiatives work its way through the regulatory and judicial systems, it is unlikely that JBLU stock will see appreciation in line with stronger performing carriers including ALK, DAL, LUV, and UAL.

For further details see:

JetBlue Airways Can't Get Airborne