BACRP - JetBlue Airways: Cost Improvements Should Push Cash Flows Higher

2023-06-28 11:18:28 ET

Summary

- JetBlue Airways is currently undergoing a potentially beneficial acquisition of Spirit Airlines. Despite regulatory concerns, I believe the deal will likely go through.

- The airline industry, including JetBlue, suffered significantly during the COVID-19 pandemic, with drastic drops in revenue and passenger numbers. JetBlue's revenue has since recovered to pre-pandemic levels, but the bottom line is still struggling.

- I remain cautiously optimistic about JetBlue's future, with potential fuel cost reductions and the potential benefits of the Spirit Airlines acquisition. Despite short-term pain, I believe the stock is currently cheap and give it a soft 'buy' rating.

One of the more interesting players in the airline space these days is JetBlue Airways Corporation ( JBLU ). In addition to the fact that the company is attempting to complete its acquisition of Spirit Airlines ( SAVE ), financial performance has been rather depressed even as revenue has more than recovered from the COVID-19 pandemic. In the event that the company can see its cost structure recover back to what it was a few years ago, upside for shareholders could very well be significant. But of course, the extreme volatility of its bottom line results does present certain issues that investors must feel comfortable with if they are to make the best investment decision possible. For those willing to tough out these uncertain times, upside for shareholders could be quite appealing. But this is definitely not the kind of investment opportunity for those who can't handle wild gyrations in stock price.

A disclosure regarding Spirit Airlines

Last year, JetBlue Airways announced that it had agreed to acquire Spirit Airlines in an all-cash deal valuing the company at $33.50 per share, plus a $0.10 per share ticking fee for each month starting this year until the transaction is completed. This has been a hot topic regarding JetBlue Airways ever since, and there are already a number of analysts who have opined on the transaction and whether or not it will actually be completed because of regulatory concerns. The purpose of this article is not really to dig into this pending transaction. Rather, my goal in writing this article is to focus on JetBlue Airways in a vacuum.

My professional opinion, based on a review of the situation, is that JetBlue Airways likely will succeed in acquiring Spirit Airlines. Certainly, the management team at JetBlue Airways is pulling out all the stops in the hopes of making the deal go through. The most recent update came on June 1 when management announced that it had agreed to divest all of the holdings of Spirit Airlines New York's LaGuardia Airport, selling those assets to Frontier Group Holdings ( ULCC ) should the transaction between JetBlue Airways and Spirit Airlines be completed. This is a rather significant maneuver aimed at appeasing regulators who have been very vocal about antitrust concerns.

At the end of the day, I would love to see the transaction be completed. According to JetBlue Airways, completing the deal would result in annual net synergies for the combined company of between $600 million and $700 million. As you will see shortly, JetBlue Airways could most certainly use those cost reductions. My overall assessment of the airline operator is cautiously bullish. But if this transaction does get completed, then my opinion on the enterprise would be even more favorable. And as for Spirit Airlines, I find myself incredibly bullish because of the implied upside that shareholders should enjoy if the deal is completed.

A look at recent troubles

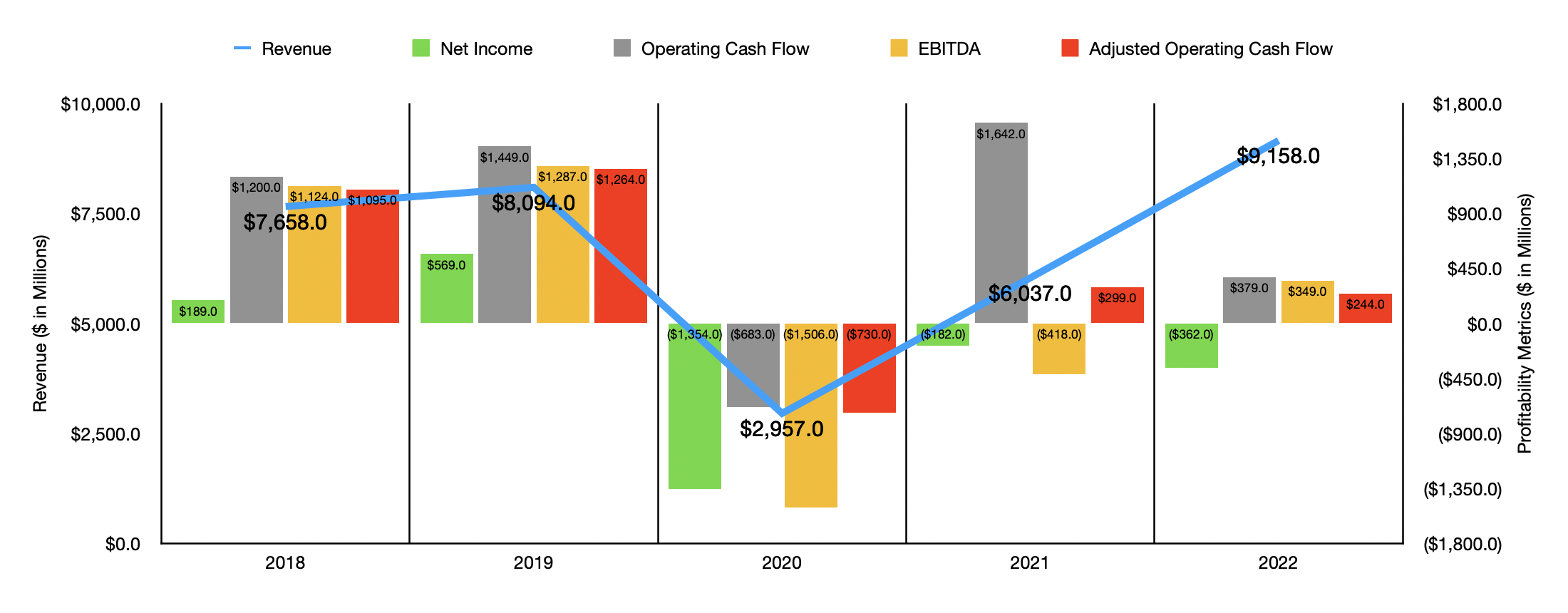

With these initial thoughts out of the way, I believe the best way to proceed is to focus on the recent financial history of JetBlue Airways. Like every company in the aviation space, JetBlue Airways was decimated by the COVID-19 pandemic. After seeing revenue climb from $7.66 billion in 2018 to $8.09 billion in 2019, sales then plummeted to only $2.96 billion in 2020. Naturally, bottom line results for the enterprise suffered as well. The firm went from generating a net profit of $569 million in 2019 to losing $1.35 billion. Operating cash flow declined from $1.45 billion to negative $683 million. Even if we adjust for changes in working capital, we would have seen the metric fall from $1.26 billion to negative $730 million. And finally, EBITDA for the company went from $1.29 billion to negative $1.51 billion.

{kind=link}

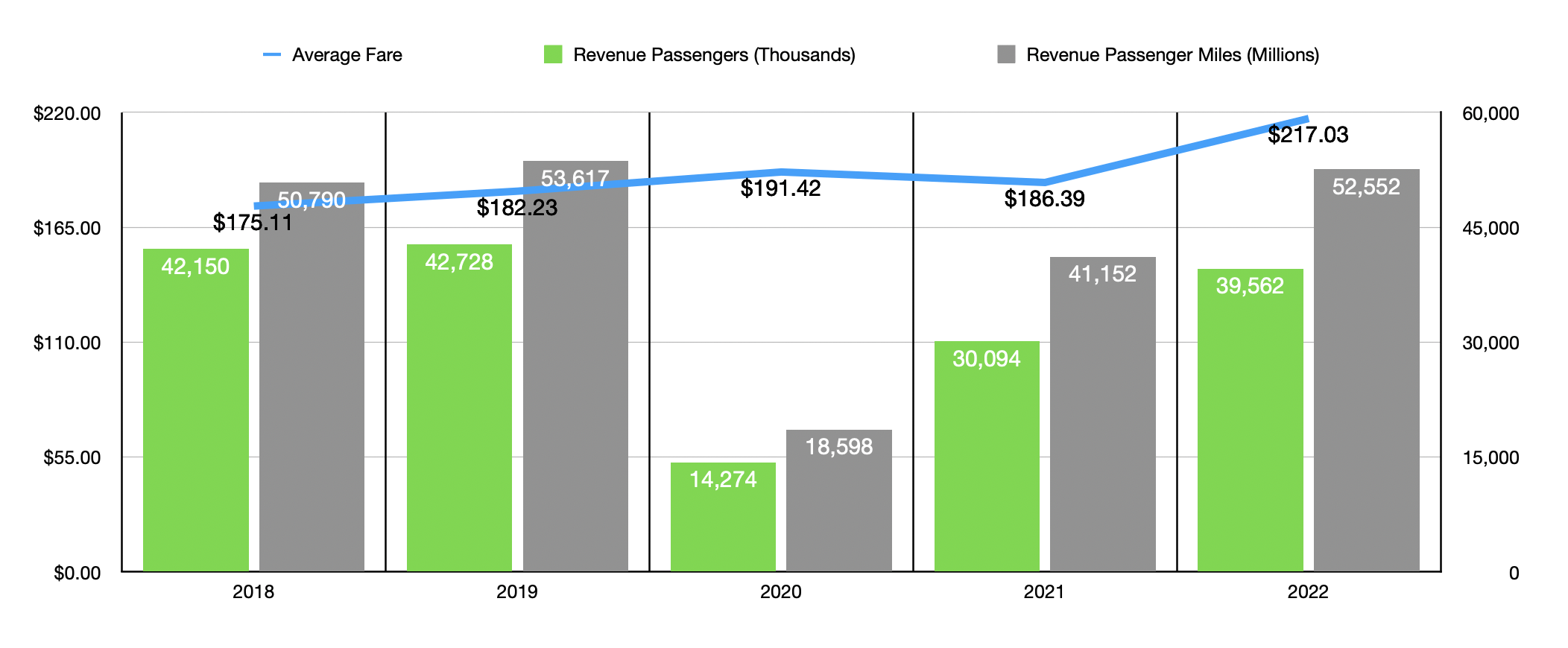

It's no secret what caused these massive declines. Even though the company saw the average fare that it charged grow from $182.23 to $191.42 from 2019 to 2020, the number of revenue passengers plummeted from 42.73 million to 14.27 million. Revenue passenger miles naturally fell as well, plunging from 53.62 million to 18.60 million. That occurred as the number of departures dropped from 368,355 to 168,636. Fortunately, JetBlue Airways was not alone in its plight. According to data from the TSA, the number of enplanements that the industry in the US saw in 2020 came out to only 319.1 million. That's down 62% compared to the 840.3 million reported for 2019. Entire economies shutting down, a shift to remote work, and extreme social distancing, all led to this pain.

{kind=link}

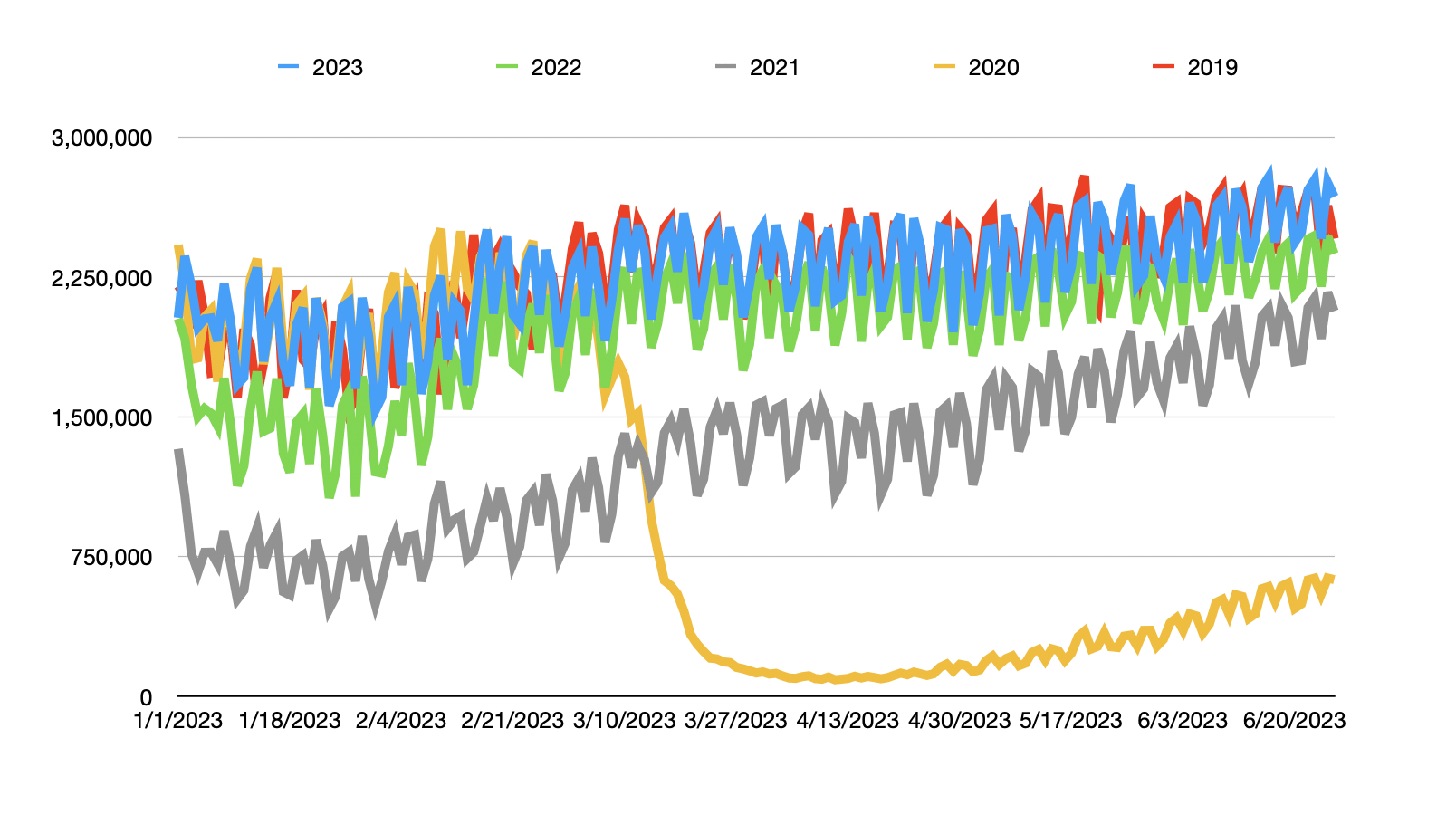

Now that COVID-19 is all but a distant memory, you would think that things would be back to normal. In some ways, they are. Revenue for the company spiked to $6.04 billion in 2021 before climbing further to $9.16 billion in 2022. This came as the number of revenue passengers recovered to levels that were almost as high as what they were in 2019 and as the number of revenue passenger miles also recovered to levels that were very close to pre-pandemic. As you can see in the chart below, the TSA data also looks promising. In fact, from the start of this year through June 26, total enplanements in the US have come out to 400.7 million. This is down only 0.21% compared to what we saw during the same window of time in 2019. The company is also benefiting from continued higher fares. In 2022, for instance, the average fare charged by the business came in at $217.03. That's 19.1% above the $182.23 reported for 2019.

{kind=link}

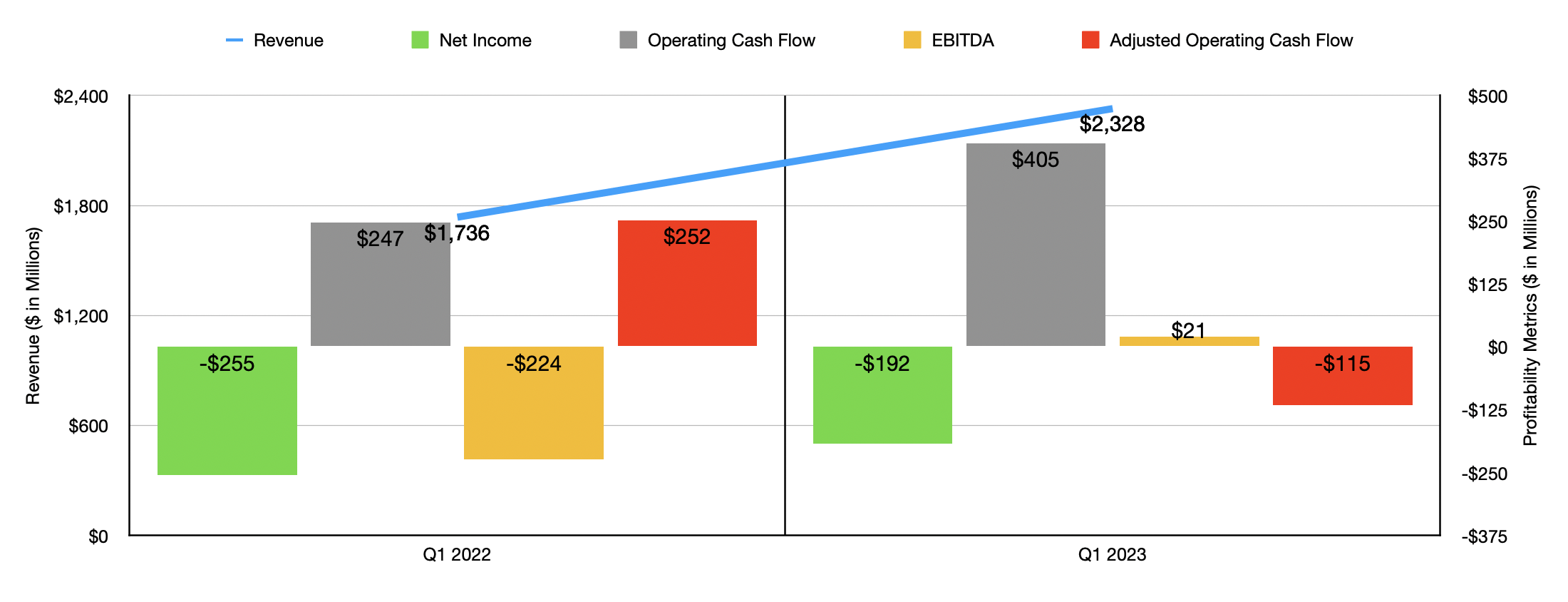

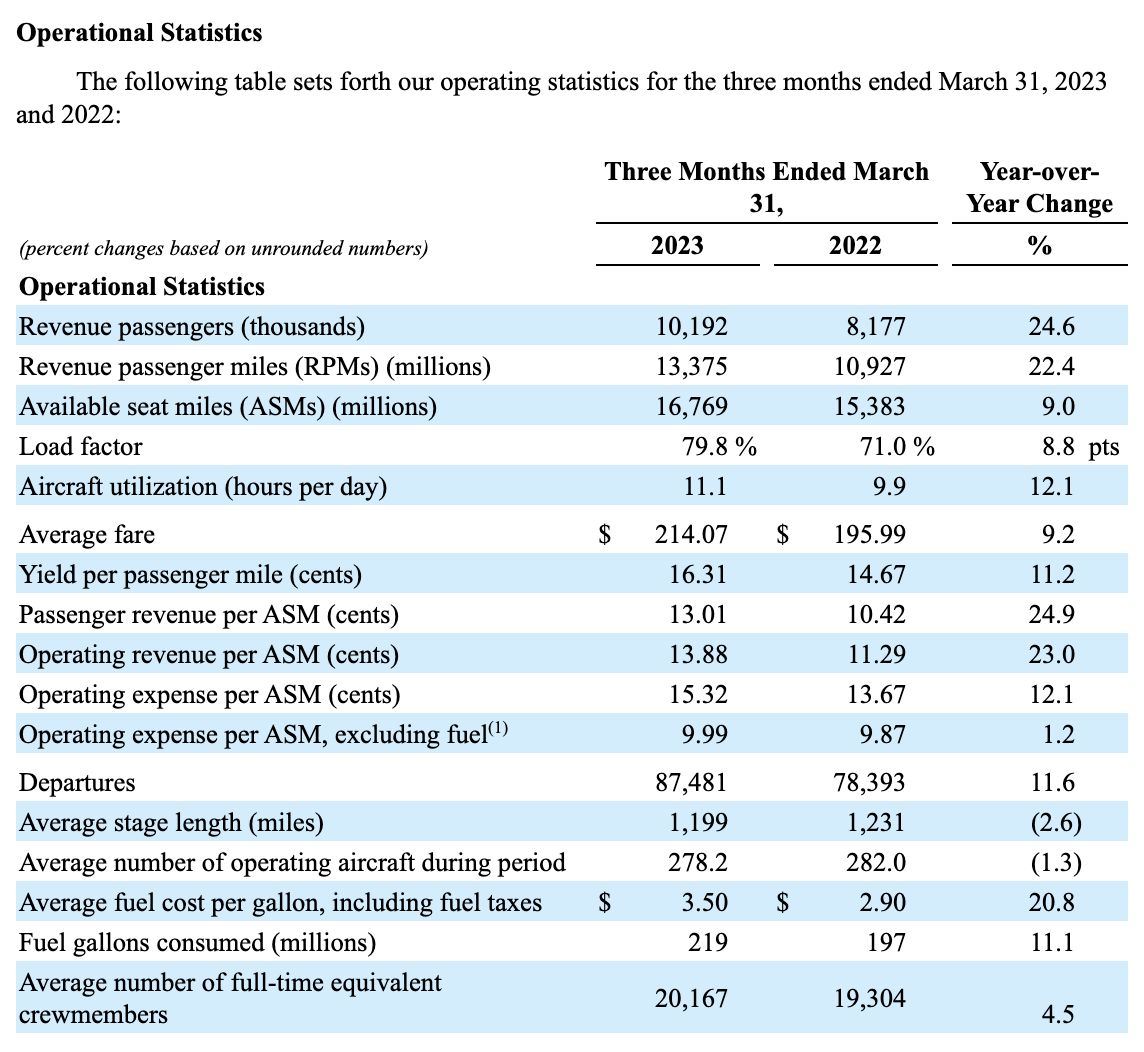

Where the results do not show up, however, is on the company's bottom line. Despite revenue soaring to new levels, the company still generated a net loss of $362 million last year. Operating cash flow was only $379 million, while the adjusted figure for this came in at $244 million. Even EBITDA is struggling to recover, coming in at only $349 million last year. As you can see in the chart below, results so far for 2023 are also mixed. It is true that most of the bottom line figures for the company are improving, driven largely by revenue surging from $1.74 billion to $2.33 billion. But compared to what the company achieved prior to the pandemic, the picture could be a lot better.

{kind=link}

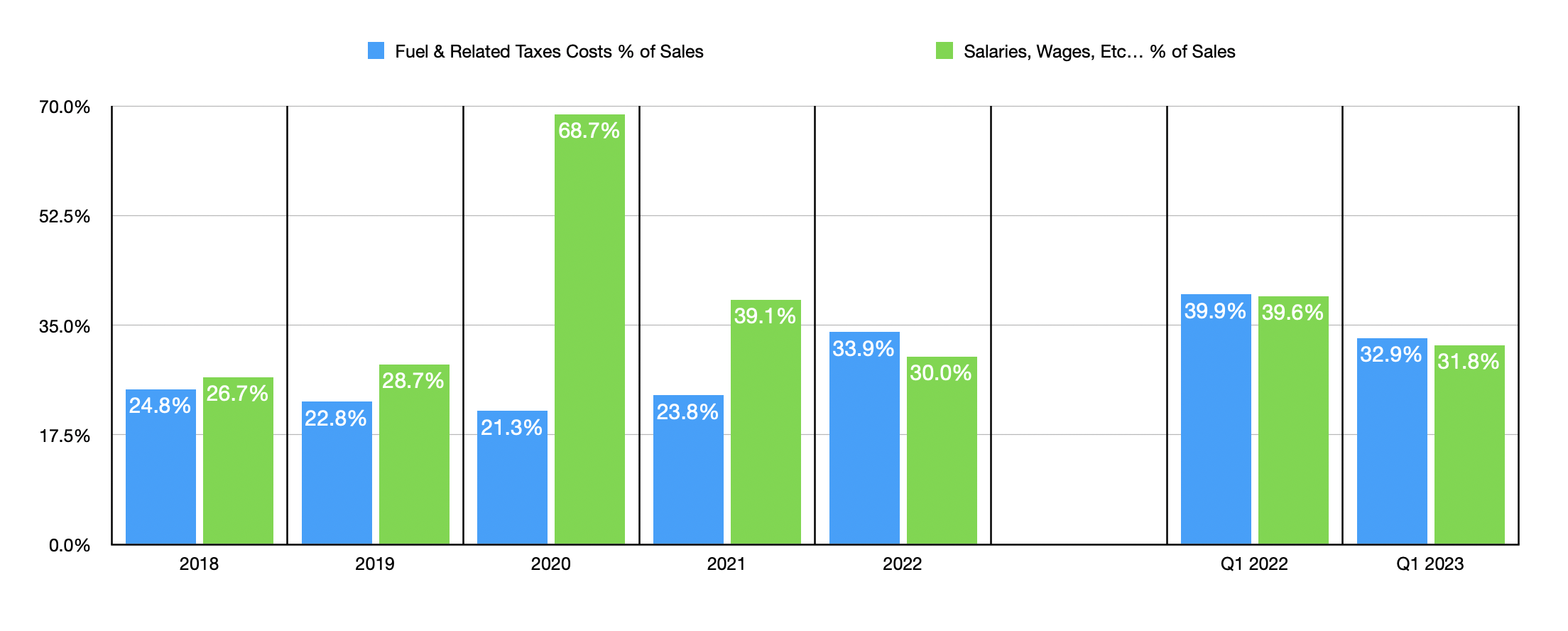

Digging deeper into the numbers, it becomes clear pretty quickly what the problems have been. Even as revenue increased, costs for the business spiraled out of control. Fuel costs, for instance, combined with taxes related to fuel, jumped from 22.8% of revenue in 2019 to 33.9% last year. We also saw an uptick in salaries, wages, and other related expenses from 28.7% of sales to 30%. Frankly, given how close that number is, I can live with the higher salaries and wages. But the fuel cost picture is downright painful. Using the revenue generated in 2022, if the company were to see its fuel costs go back to what they were in 2019 as a percentage of sales, the end result would be another $1.02 billion in pre-tax profits and cash flows to the company's bottom line.

{kind=link}

In the first quarter of this year, we have seen some improvement compared to the same time last year. In addition to seeing salaries and wages drop from 39.6% of revenue down to 31.8%, fuel and related expenses declined from 39.9% of sales to 32.9%. It is worth noting that there is considerable uncertainty over what the salaries and wages picture might be moving forward. This is because, on March 1 of this year, the new pilot union contract for the company became effective. That includes pay rate increases that cover the next two years, such as a 14% pay raise for pilots and with the average number of full-time equivalent crew members experiencing a 4.5% increase in compensation.

{kind=link}

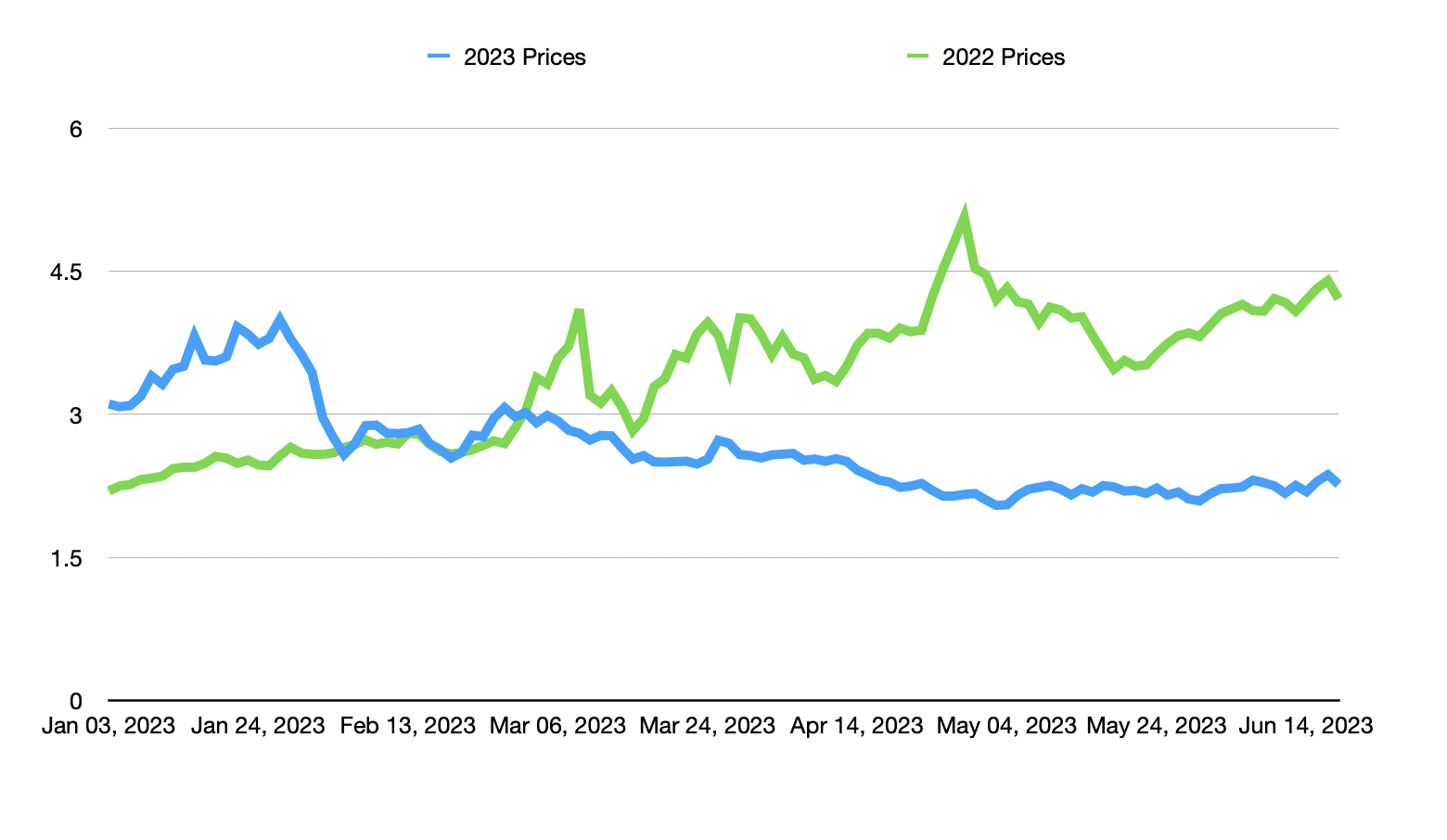

While the company did enjoy a decrease in fuel costs relative to sales, this was really only driven by the company's ability to control the average fare that it charges. This number grew from $195.99 to $214.07. Actual average fuel costs per gallon, inclusive of taxes, spiked from $2.90 to $3.50. This is most certainly painful. But there is some good news. Recently, Bank of America ( BAC ) increased earnings estimates for the aviation sector, citing a recent reduction in fuel costs. From the start of this year through June 20, using daily data, jet fuel costs have fallen from an average price of $3.40 per gallon to $2.65 per gallon. Much of this decline occurred over the past couple of months. In fact, on June 20, jet fuel costs came in at $2.26 per gallon. That's down from the $4.21 per gallon that we saw the same time last year.

{kind=link}

Whether or not prices remain low and possibly even move lower is something only time will tell. Bank of America certainly seems optimistic. I am less so, as I have mentioned regarding the oil space in general earlier this year. But in the event that costs do eventually fall, the upside for shareholders could be significant. Even ignoring the potential acquisition of Spirit Airlines and the positive impact that could have on investors, returning to the levels of profitability seen in 2019 would result in the company trading at a price to adjusted operating cash flow multiple of 2.1 and at an EV to EBITDA multiple of 3.5. By comparison, using the data from 2022, these multiples come in at 10.8 and 13, respectively.

Takeaway

At this point in time, JetBlue Airways has a lot going for it from a revenue perspective. The industry has certainly recovered following the COVID-19 pandemic. As I detailed in another article, there is some other positive guidance for the space as a whole. And there is always the catalyst that is the Spirit Airlines purchase. On the bottom line, we are seeing some pain right now. In the short term, that pain looks set to alleviate. My own personal stance is that the medium term will see some resumption to that pain. But eventually, fuel prices will fall. Given how cheap the stock is right now, and factoring in the other positives that I mentioned already, I believe that taking a cautiously optimistic approach is appropriate at this time. That has led me to rate the business a soft 'buy'.

For further details see:

JetBlue Airways: Cost Improvements Should Push Cash Flows Higher