JBLU - JetBlue Earnings Show A Company Without A Flight Plan

2023-08-04 07:00:00 ET

Summary

- JetBlue's 2Q2023 earnings report showed a 6.7% increase in total revenues, but passenger revenues were below double-digit increases seen by competitors.

- The shift in demand from domestic to international destinations is dragging down JetBlue's revenues, as the big 3 global carriers benefit from strong international demand.

- JetBlue's poor on-time performance, lack of product distinction, and increasing labor costs are contributing to its financial struggles.

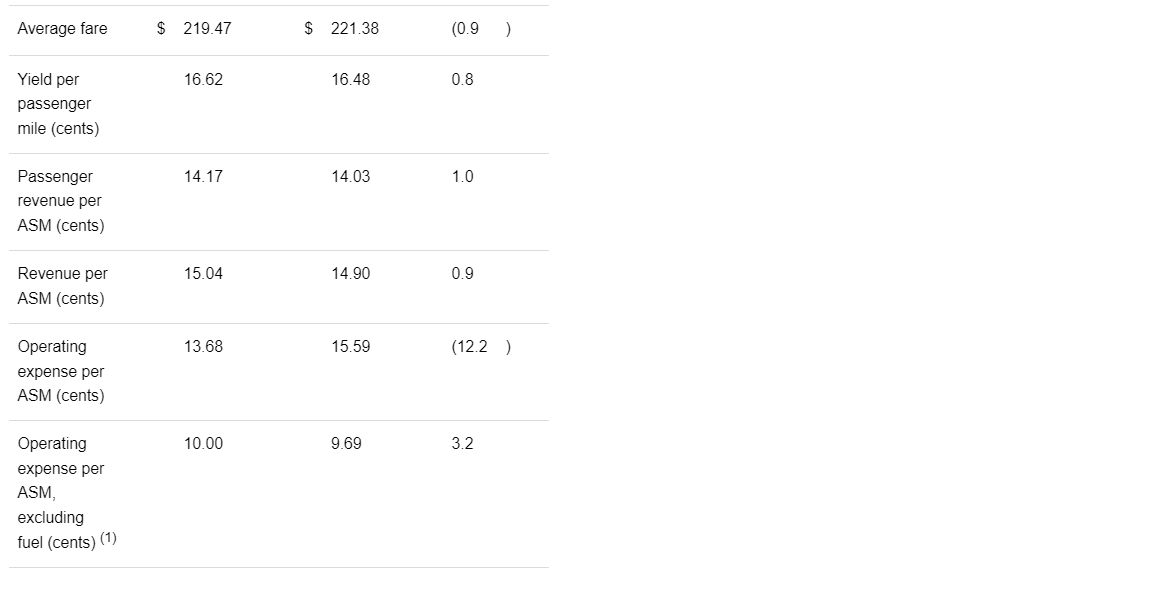

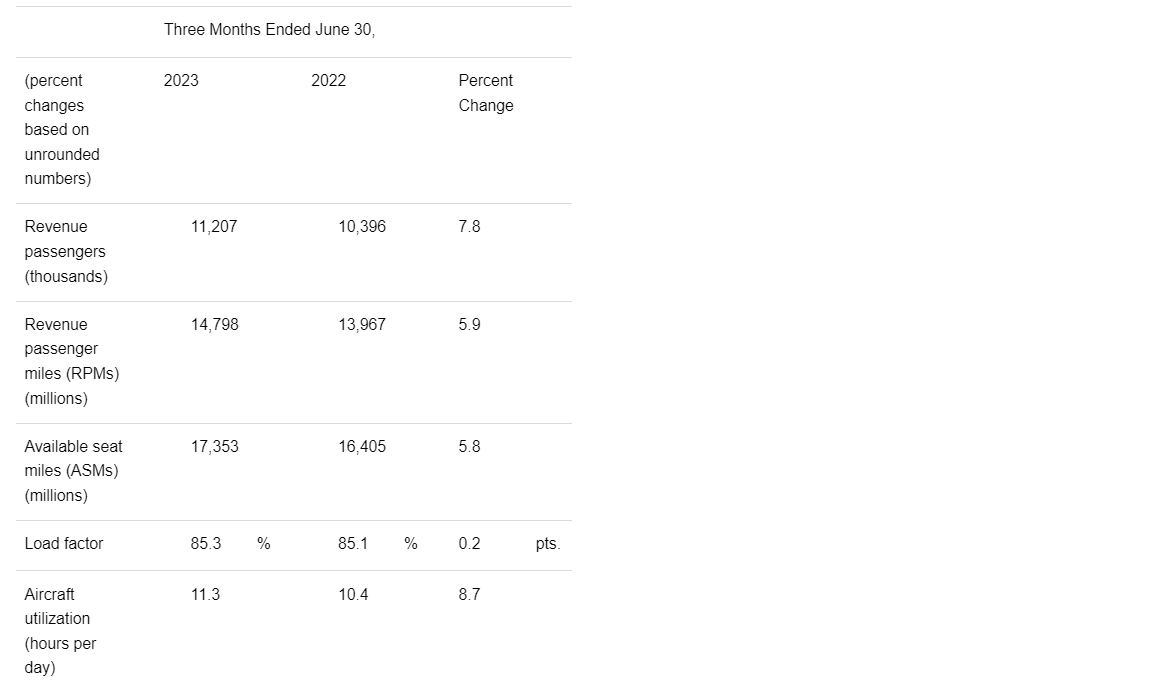

JetBlue Airways ( JBLU ) reported second quarter 2023 earnings on Tuesday August 1 after the big 4 – American ( AAL ), Delta ( DAL ), Southwest ( LUV ), and United ( UAL ) as well as Alaska ( ALK ). By the time LUV reported, industry earnings trends became clear and expectations were not high for JBLU’s earnings – and they solidly underwhelmed even their fiercest supporters. JetBlue’s 2Q2023 earnings report showed a 6.7% increase in total revenues with passenger revenues slightly ahead of that measure, well below double digit revenue increases for competitors. On the expense side, JBLU’s fuel expense fell by 34% due to lower pump prices; the $300 million decrease was partially offset by increases of other expenses including labor. JBLU’s 5.3% net income margin put it at the back of the pack of the largest airlines that reported before it. Spirit (SAVE), JBLU’s intended merger partner, reported on Thursday Aug 3 and continued the trend of very weak financial results with a GAAP net loss due in part to merger-related expenses. SAVE reported much deeper decreases in revenue performance than higher fare and the global carriers but also JBLU.

JBLU revenue stats 2Q2023 (Seeking Alpha) JBLU traffic stats 2Q2023 (Seeking Alpha)

{kind=link}

{kind=link}

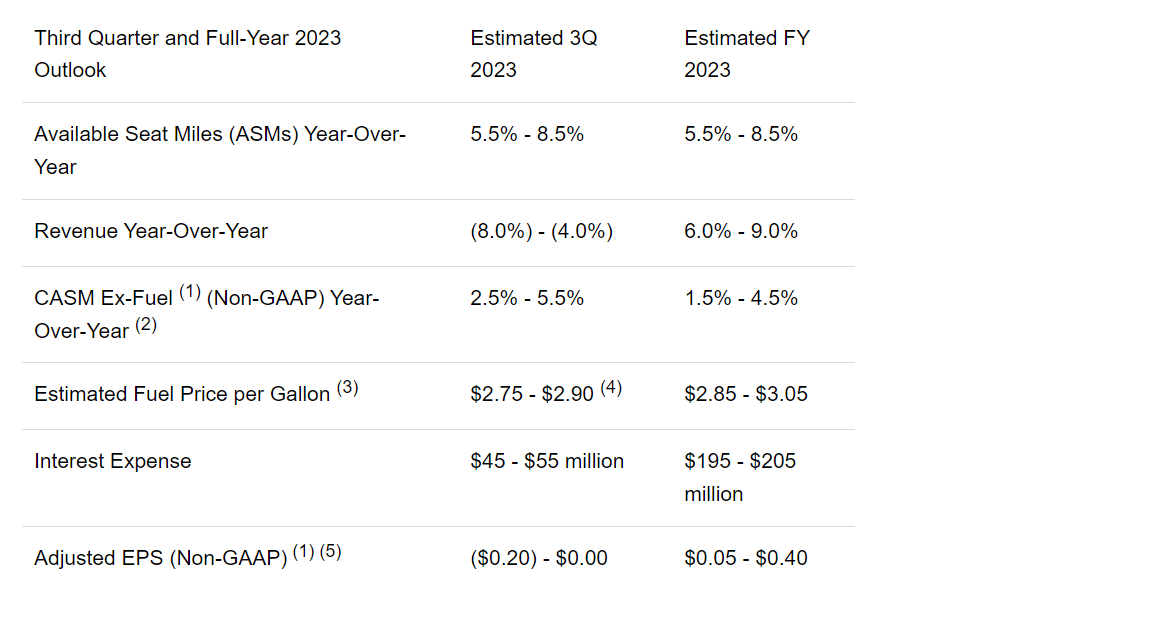

The biggest blow in JBLU’s earnings release was its guidance for the 3 rd quarter and full year 2023 that indicates that the NYC based airline will likely not be profitable in the 3 rd quarter as revenue is expected to fall 4-8%.

JBLU guidance as of Aug 2023 (Seeking Alpha)

{kind=link}

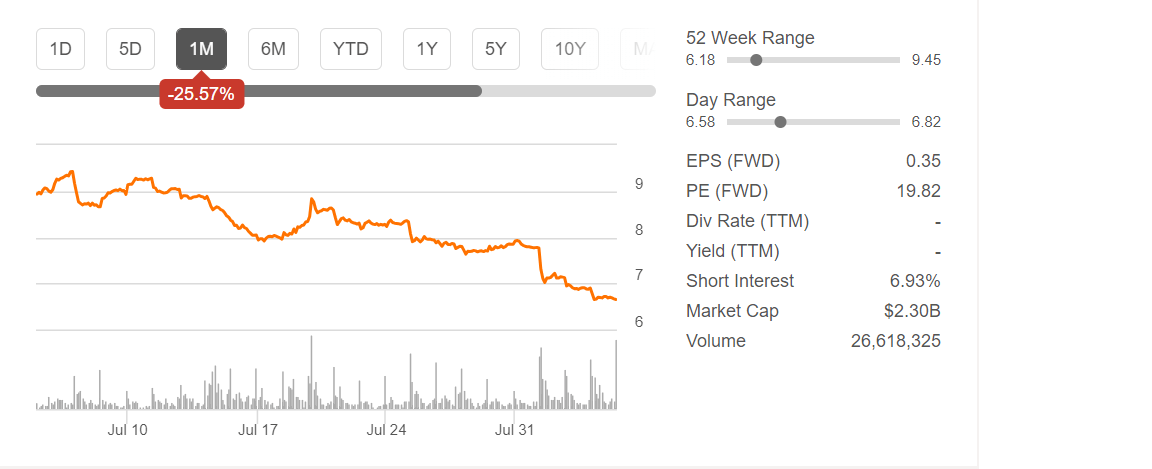

JBLU stock has been one of the weakest airline stocks over the past year in a sector that has outperformed many indices. JBLU stock has declined about the same amount over one month, six months, and one year.

JBLU one month chart 3Aug2023 (Seeking Apha)

{kind=link}

Investors legitimately have to ask if JetBlue can overcome the drivers that have dragged down its performance and if the strategies the company is proposing are sufficient to turn the company around.

Changing Industry Dynamics

JetBlue execs highlighted that one of the biggest factors dragging down revenues is a shift in demand from domestic to international destinations. Since JBLU serves London and Paris even though it is predominantly a domestic airline, it has the ability to see shifting signs of demand. However, LUV and ALK both expressed a similar weakening of domestic demand, something that the U.S. DOT saw in June .

The domestic U.S. market never closed to the extent that international markets did during covid. The big 3 noted very strong international demand last summer, something that United, which did not retire aircraft during the pandemic, was well-prepared to capture. Delta added more than a dozen widebody aircraft to its fleet for this summer’s peak travel season and all of the big 3 provided data that shows all three global regions are delivering stronger financial than the domestic marketplace. While it is not certain yet if the substantial increase in domestic airfares post-covid as well as higher interest rates is squeezing consumer pocketbooks, there is enough data to know that the big 3 are benefitting from strong international demand which is stronger than the domestic marketplace in a paradigm shift for U.S. airlines.

In addition, the big 3 are all seeing strong demand for premium services including the willingness of some consumers to buy up to first class and use premium ground services, including airport lounges. While JBLU has some aircraft configured with its Mint premium cabin which are predominantly used on transcontinental routes, the majority of JBLU’s aircraft do not have premium cabins which means that JBLU is probably missing out of some of the revenue increase that the legacy carriers are seeing. Southwest is in an even more disadvantaged position and its revenue metrics were worse than JBLU’s; LUV noted that part of the problem with its revenue production was due to the use of transportation vouchers which it issued as a result of its December 2022 operational meltdown. Finally, the big 3 are producing more revenue than ever from their loyalty programs and credit card affiliations. JBLU has those types of programs but they don’t come close to delivering the amount of revenue that the big 3, and esp. Delta, receives.

In addition, U.S. airlines received abundant government aid so none of them failed, one of the first times a major global crisis has not led to the failure of an airline. Consequently, airlines are still positioning themselves post-covid even as domestic business travel is about 80% recovered according to the best estimates, meaning there is more competition for leisure and “bleisure” (blended business/leisure) travelers. So many of the basics of the airline industry and consumer behavior were shaken up during the pandemic and the big 3 global carriers have come back stronger relative to low-cost carriers than has ever been the case which has allowed the big 3 to add capacity at a faster rate. Delta and United both registered capacity increases in the high teens percentages while JBLU didn’t break 6% ASM (available seat miles, the airline industry measure of capacity) growth.

JetBlue is Losing its Cost Advantage

One of the post-covid paradigm shifts that has taken place is the soaring cost for airline labor. The pandemic interrupted the training and career paths of many types of employees including airline pilots, even as tens of thousands of airline employees retired during the pandemic. Early in the pandemic, it became apparent that regional airlines could not supply the number of pilots necessary to staff their operations. Since the general historic pathway for airline pilots was to start their civilian careers at regional airlines, then often move to low-cost carriers and then some ended up at the big 3, the pilot shortage put the low-cost carriers in the bullseye of being a target for larger airlines which moved to raid low-cost carrier pilot ranks. JBLU and many low-cost carriers moved quickly to raise salaries for their pilots to prevent being the target for other airline pilot recruiting; notably Southwest is one of the few holdouts in reaching a new contract with its pilots and the level of dissatisfaction and attrition at that airline is rising. However, the big 3 are still often the first career choice for airline pilots because of their use of widebody aircraft which can result in millions of dollars more in career earnings. While JBLU currently appears capable of obtaining enough pilots for its operations, one of the justifications it gave for its merger with Spirit was to obtain a supply of labor, including pilots. While much less discussed, the number of new aircraft mechanics is not growing fast enough to provide the supplies necessary so airline mechanic salaries are also rising, although many low-cost carriers outsource large percentages of their maintenance to foreign companies which are not experiencing the same labor dynamics as is the case in the U.S. In a major plot twist from most of the deregulated airline era in the U.S., the global/legacy carriers are using their revenue advantage to increase labor costs which puts pressure on low-cost carriers; as JetBlue’s most direct legacy competitor and also the most profitable U.S. airline, Delta had to know the implications of being the first of the big 4 airlines to agree to a rich pilot contract and then followed it up with raises for its remaining employees, most of which are non-union. Other carriers continue to work through labor expectations for increases comparable to what Delta gave its employees.

JBLU’s bigger challenge is that it is reaching maturity as a company and now has growing percentages of employees that are at the top of their pay scales. Southwest had to address the same issue but maintained to further increase its efficiency and revenue generation, something JetBlue has been unable to do. Low-cost carriers have typically helped overcome cost creep by growing at high rates compared to other carriers but the competition for labor and supply chain shortages have slowed the ability of low-cost carriers to grow while forcing them to compete at higher costs. From both a revenue and a cost side, JBLU’s business model is not capable of keeping the company from becoming less and less financially viable.

An Indistinguishable Product

JetBlue burst on the scene just over 20 years ago promising to delivery low-cost air service to New York City where then the three major airports were all slot-controlled and the ability for low-cost carriers to grow was highly limited. JBLU convinced government leaders to gift it with enough slots at JFK airport to make it roughly the size of American and Delta at JFK at the time. JFK airport in the late 1990s was not operated as a true hub but rather was served by a number of U.S. and even more foreign airlines as a “spoke” or end of the line station. Continental Airlines transformed the former low fare People Express’ operation at Newark into a global, full-service carrier hub but New Yorkers had experienced a taste of low fare service and JBLU not only promised to provide low fare service at JFK airport but to make low-cost carrier service more upscale than had ever been done in the U.S. Determined not to venture into widebody international operations, JBLU quickly expanded its network to the Caribbean as well as the traditionally strong domestic markets in Florida and to the west coast, posing a major challenge to American. Delta’s post 9/11 restructuring and the relaxation of slot controls at JFK allowed the Atlanta-based airline to build its presence at JFK, eventually overtaking JBLU as the largest airline at JFK and duplicating at JFK the global hub that Continental, later acquired by United, had built at Newark.

Delta also began to copy a number of JBLU initiatives including two versions of low-cost carrier within a carrier that focused on the leisure market, the latter of which incorporated the seatback personal audio-visual systems that helped distinguish JBLU in the marketplace. While Delta merged its internal low-cost carriers back into its mainline system, it succeeded in slowing JBLU’s growth and winning over customers with a route system that largely duplicated what JBLU operated but also including a large transatlantic network – where JFK airport has excelled among U.S. airports. As the Great Recession ended, JBLU had lost much of its network and product distinction and became increasingly focused on competing on price – a strategy that has been less and less successful for it.

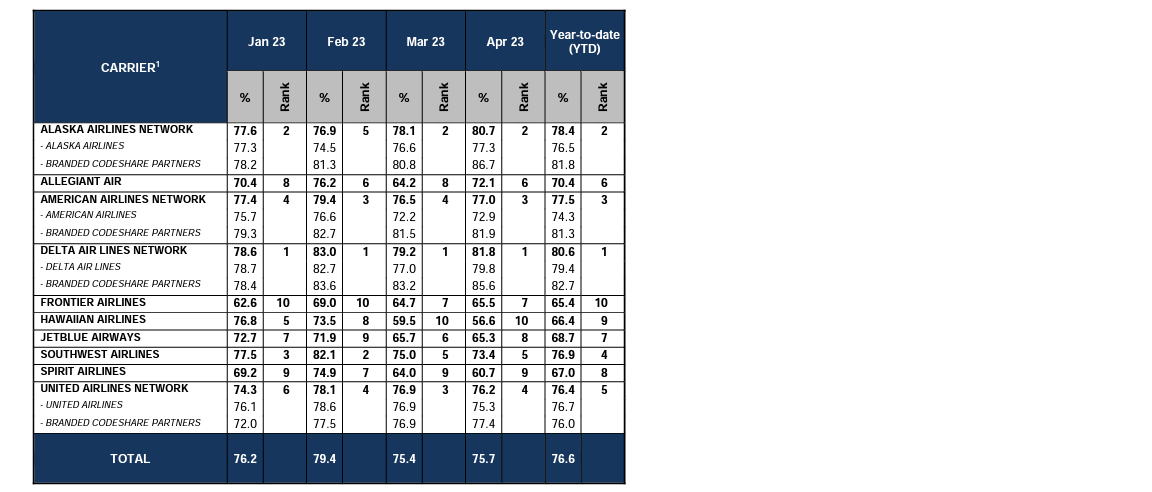

JetBlue’s biggest negative distinction is its poor on-time performance. While JBLU frequently blames its high percentage of operations in the Northeast U.S. and esp. NYC for its poor on-time performance, they seem powerless to address the problem and content to let more and more high-value passengers defect to other airlines which operate more reliably even from the same airports. In fact, although DOT data for the summer is not yet available, the latest data continues to show JBLU near the bottom of the U.S. airline industry and underperforms larger peers including Delta – which shares hubs with JetBlue at JFK and Boston – by 10% or more. The Northeast has absolutely been very challenging operationally this summer and United’s decision to extend schedule reductions into the fall indicates things won’t get better anytime soon. However, the gap between JBLU on-time performance and other carriers has been going on for years. While the legacy carriers often cancel regional carrier flights when bad weather limits the number of flights an airport can operate, JBLU has no regional carrier flights although its E190 aircraft is a larger version of the same E175 regional jets that global airlines have in their regional carrier fleets. Instead, JBLU runs flights that become even more delayed. Because their business model includes large percentages of overnight flights, there is little room for the operation to recover. It would seem that one obvious solution for JBLU would be to dedicate some standby aircraft to help with recovery but JBLU is resistant to invest in aircraft that might sit idle for days – although airlines and airline passengers are now seeing frequent major disruptions in the NE at least on a weekly basis this summer and often more frequently than that.

DOT Air Travel Consumer Report YTD Apr 2023 (U.S. DOT)

{kind=link}

JBLU’s onboard product is no longer distinctive either. Delta has rolled out seatback entertainment on most of its fleet and United is now committing to do the same thing esp. as part of its massive domestic fleet expansion and replacement plans. Other airlines are expanding and upgrading their inflight WiFi systems and Delta recently became the first large airline to match the free WiFi that JetBlue offered its customers for years. In short, other airlines are matching or have matched the product attributes that made JetBlue distinctive but also run much more reliably and attract higher quality revenue in part because of their larger route systems.

JetBlue’s attempts to move upscale are confounded by the ultra low-cost carriers including Spirit, Frontier ( ULCC ) and Allegiant ( ALGT ) and the latter two are performing financially better than JBLU. Unlike Southwest, which has substantial market moats in a number of its “hubs” or major bases such as at Chicago Midway, Dallas Love Field, and Houston Hobby airports, JBLU has no markets which it dominates meaning there is minimal opportunity to offset its service woes by the lack of airline choice that comes from dominance in air travel markets. Factor in that JBLU has limited consumer preference or market share outside of its primary markets of Boston, NYC, and Ft. Lauderdale and its relatively weak loyalty program doesn’t help its ability to compete. JetBlue is an airline that is squeezed between larger carriers that generate revenue more efficiently with a broader range of services and ultra low-cost carriers that offer consumers lower prices.

The Costly Unwind of The Northeast Alliance

The greatest concern from JBLU’s earnings release was its guidance for the third quarter which indicates that the company will not only see a 4-8% decrease in revenue but also a likely loss. The unwinding of the Northeast Alliance, the joint venture that American and JetBlue formed in 2021, promptly challenged by the DOJ, and ruled illegal under U.S. antitrust law by a U.S. District Judge in Boston earlier this year. As the NEA is unwound, the greatest drop off in capacity will come as JBLU has to return slots at LaGuardia (LGA) to AAL and exit routes at Boston that it flew for American which are no longer profitable without revenue sharing. JBLU tripled the number of flights it operated at LGA because of the Northeast Alliance. JBLU says it has already begun to adjust schedules in Boston since slots are not involved but will step down its schedules at LGA over the next nine months with one wave of reductions occurring in October and the second major wave in the spring of 2024. AAL also guided to a much weaker 3 rd quarter than direct peers Delta and United so the revenue chaos in unwinding the NEA will be substantial to both AAL and JBLU. Although JBLU says it will find new markets to enter as replacements for the cancelled routes which will also diversify its presence in the northeast, which it still expects to suffer from air traffic control delays into 2024, JBLU has tried multiple times to add new routes outside of the northeast without success.

JetBlue and Spirit Still Want to Merge

The unwinding of the Northeast Alliance comes at the same time that JetBlue will double down on its efforts to merge with Spirit Airlines to which the DOJ is also objecting. JBLU’s stated goals with the SAVE merger were to gain access to aircraft and employees, esp. pilots, and to build a network that could compete with the big 4 – AAL, DAL, LUV and UAL. The DOJ’s objections to the JBLU/SAVE merger center around JBLU’s plan to eliminate a lower cost and lower fare competitor – SAVE is an ultra low-cost airline while JBLU is a low-cost airline – and remove seats from every SAVE aircraft as they are reconfigured to JBLU less dense standards. In addition, JBLU and SAVE are the two largest carriers at Ft. Lauderdale where they both have extensive operations to the eastern U.S., into the Caribbean, and to the northern tier of Latin America.

While it was still trying to hold onto the NEA, JBLU agreed to transfer SAVE’s NYC assets to Frontier ( ULCC ) upon closing of the JBLU/SAVE merger. SAVE does not fly to JFK airport but does serve LGA and those assets are what will be transferred to ULCC. Since JBLU will become much smaller at LGA, not much larger than SAVE, it seems questionable why JBLU was willing to give up SAVE assets in NYC even while litigation of the NEA was still in process. The chances are high that it could have retained all of the combined JBLU and SAVE NYC assets while their combined size in Ft. Lauderdale is far more problematic. While JBLU argues that it will divest gates at Ft. Lauderdale (which is not slot-restricted) in order to allow competitors to grow, the impact of the merger will be to raise fares to one of the largest east coast markets and throughout the Caribbean and Latin America. At the same time, JBLU says it will grow the size of its operation at Ft. Lauderdale by adding service to more cities. JBLU and SAVE’s growth at Ft. Lauderdale provided competition to AAL and its hub at Miami, the largest gateway to Latin America which American dominates. The simultaneous attempts to gain approval for the NEA and the merger are leading to a weakened combined company while not addressing the objections that the DOJ initially raised – elimination of a lower fare and cost competitor and the associated capacity reductions as well as the overlap in Ft. Lauderdale.

Ironically, Frontier Airlines ((ULCC)) was Spirit’s original merger partner and has posted 2Q2023 income margins considerably higher than either JBLU or SAVE, even though ULCC’s margins trail the global carriers and ULCC’s historic levels. A ULCC/SAVE merger would likely not have encountered the objections from the DOJ that JBLU/SAVE is now facing. Finally, it can’t be overlooked that JBLU engaged in a costly bidding contest for Virgin America in the last decade but lost out to Alaska Airlines ((ALK)) which has dismantled large portions of the former Virgin America network. While mergers esp. in the airline industry never have a great track record of success, JBLU seems to be pushing a merger that will have a huge uphill battle for success if it gets past the DOJ.

Bottom Line

On the heels of yet another quarter of low earnings, with the prospect of a loss in the third quarter, and with the prospect of further reduced earnings even as JetBlue tries to pursue one of the more complex mergers the airline industry has seen, investors have to ask if it is worth holding onto JBLU stock. The conclusion seems clearer than ever that JBLU is the highest risk airline stock in a sector that is falling as domestic consumer demand weakens. Investors might be wise to sit on the sidelines while JetBlue decides on strategies that it can make work.

For further details see:

JetBlue Earnings Show A Company Without A Flight Plan