UAL - JetBlue Is Ready To Regain Its Destiny (Rating Upgrade)

2023-12-11 09:00:00 ET

Summary

- JetBlue Airways stock has seen a recent increase, but there are several challenges and uncertainties facing the company.

- The airline's updated investor guidance shows strong revenue and moderating cost pressures.

- JetBlue's improved operational reliability and expansion into Europe are positive factors, but challenges remain with the termination of the Northeast Alliance and the proposed merger with Spirit Airlines.

JetBlue Airways Corporation ( JBLU ) stock saw a healthy increase last week followed by mild profit-taking. There were several significant pieces of news affecting JBLU and the airline industry last week. In this article, we will look at each of those pieces of news and determine if there is further room for expansion of JBLU’s stock price which will help investors decide if they should get in, hold, or sell.

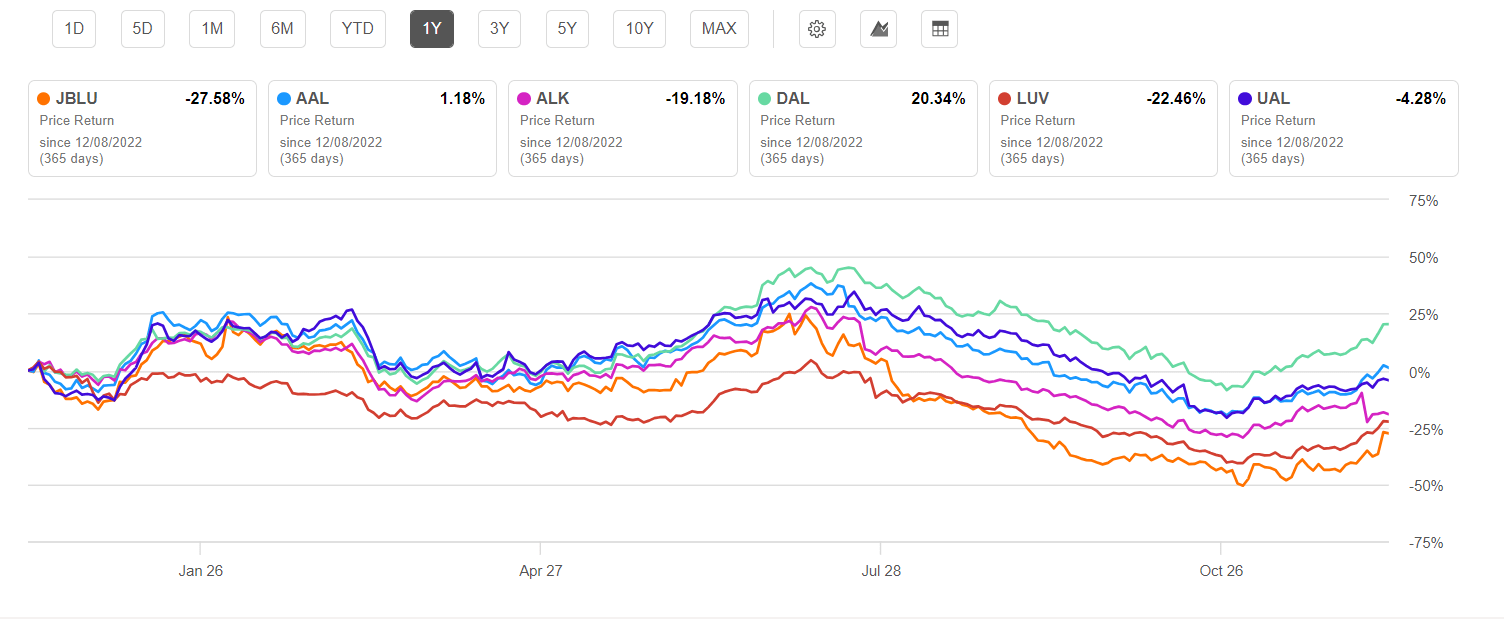

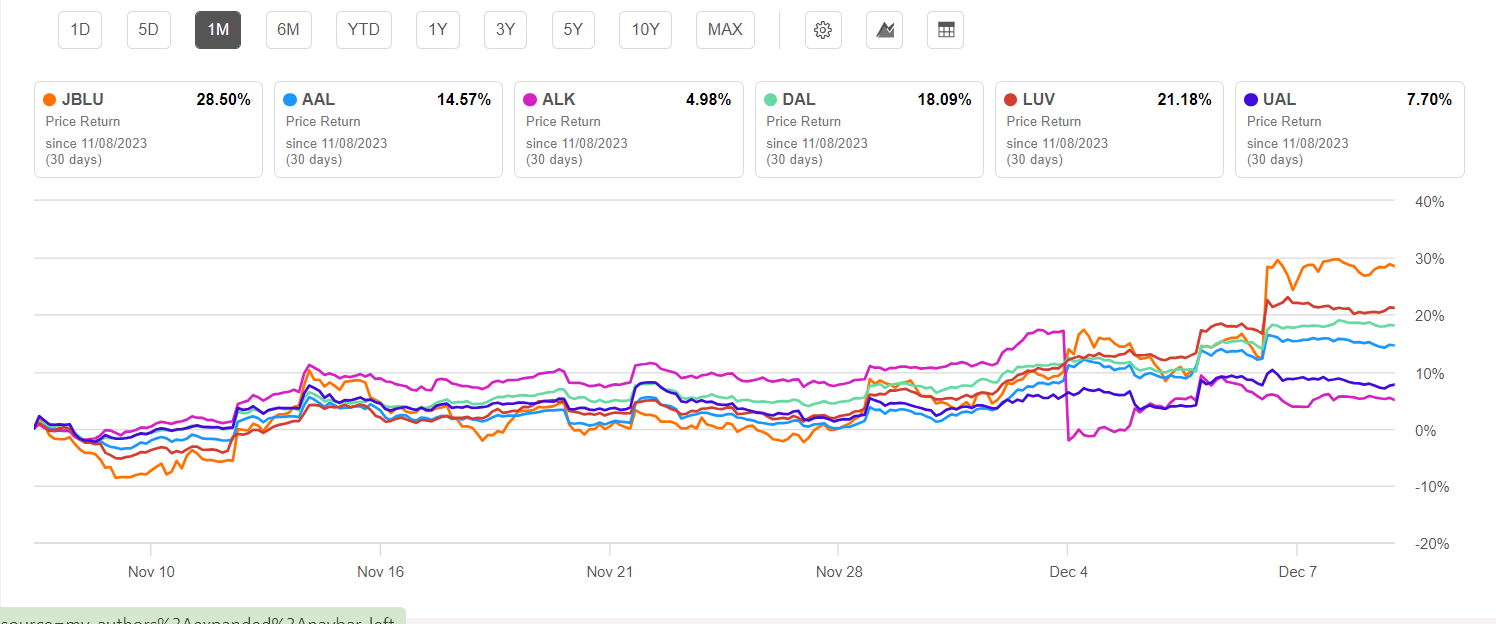

First, let’s look at a few charts highlighting JBLU stock performance over the past year and month, showing that JBLU has been one of the most beaten-down stocks in the airline industry but which has seen a month of good returns after a slow slide during the summer and early fall.

JBLU v industry 1 yr 10Dec2023 (Seeking Alpha) JBLU v industry 1 mo 10Dec2023 (Seeking Alpha)

{kind=link}

{kind=link}

A Nice Investor Update

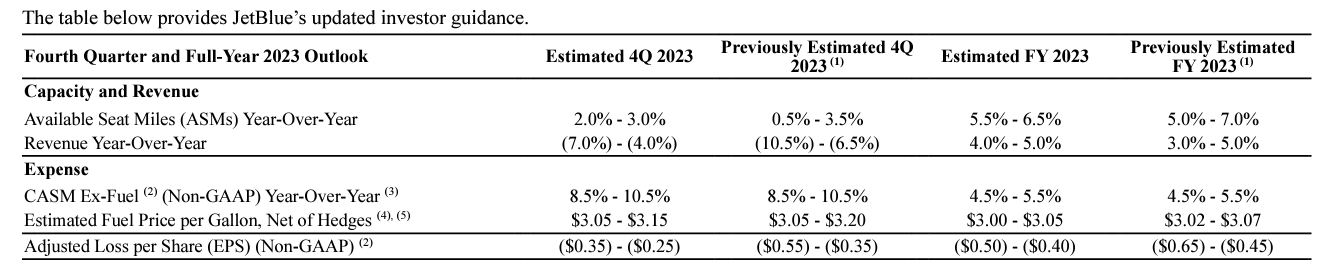

The most significant piece of news came with JetBlue’s updated investor guidance which came Thursday, December 7. In its update, JBLU indicated that revenue remains strong and cost pressures are moderating. As I noted in my recent Seeking Alpha article on U.S. Global Jets ETF (JETS), the U.S. airline-heavy ETF, revenue metrics for the industry have been strong due to several factors. The soft landing that economists have hoped for might be occurring for the U.S. economy. Work from home and remote work habits have extended the holiday travel periods; the U.S. Thanksgiving holiday saw record levels of demand on tighter capacity. Delta ( DAL ) provided its updated guidance last week indicating strong domestic and international demand; while JBLU does not have an international network the size of DAL or United ( UAL ), both of which have been buoyed by strong international demand and longer peak travel seasons, or even as large as American (AAL), JBLU has done more to expand its international footprint over the past 2 years and continues to grow in Europe where it continues to add new service from its New York and Boston hubs. DAL noted in a JP Morgan Consumer conference that the Christmas travel season looks to mirror the Thanksgiving travel period, good news for all U.S. airlines since those two holidays are heavily domestic-based and also sees boosts in travel volumes to the Caribbean and Latin America, regions which JBLU serves.

JBLU guidance update 7Dec2023 (JetBlue.com)

{kind=link}

On a cost basis, JBLU’s costs have been pressured due to reduced capacity, the result of air traffic control volume caps esp. at the New York City airports due to FAA staffing. As a NYC-based airline and with its largest operation at JFK airport and its second largest hub at Boston, JBLU is more susceptible to operational challenges in the Northeast U.S. than other airlines. JBLU’s unit costs have been pressured due not just to the reduced not just because of ATC system reductions but also because of the aircraft engine recalls for inspection and repairs of the Pratt and Whitney ( RTX ) Geared Turbofan – GTF – engine. JBLU’s A321NEO ( EADSY ) aircraft are powered by the GTF engine and some of the airline’s engines are subject to the engine recalls which could take over 2 years to complete with some aircraft potentially out of service for months at a time due to limited shop capacity and parts shortages. Both factors have led to reduced capacity for JBLU and other low cost and ultra-low cost carriers which has also led to a strong pricing environment for the airline industry. Lower crude oil prices are reducing fuel pressure and providing slight benefits compared to earlier guidance.

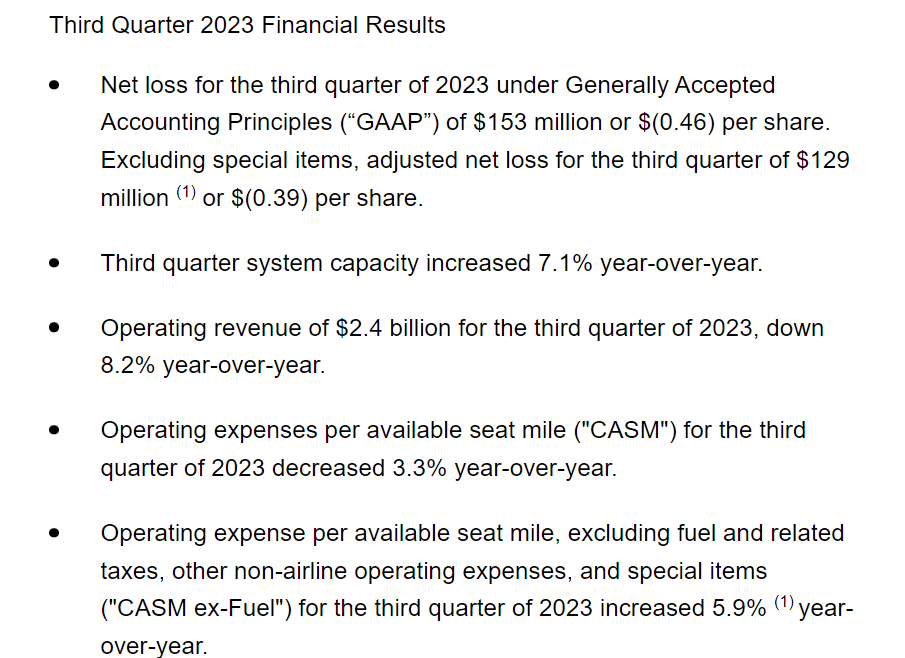

JBLU's 3rd quarter was not a bright spot for the company as a result of a number of factors, and the company reported a loss even as other carriers reported handsome profits.

JBLU 3Q2023 earnings summary (JetBlue.com)

{kind=link}

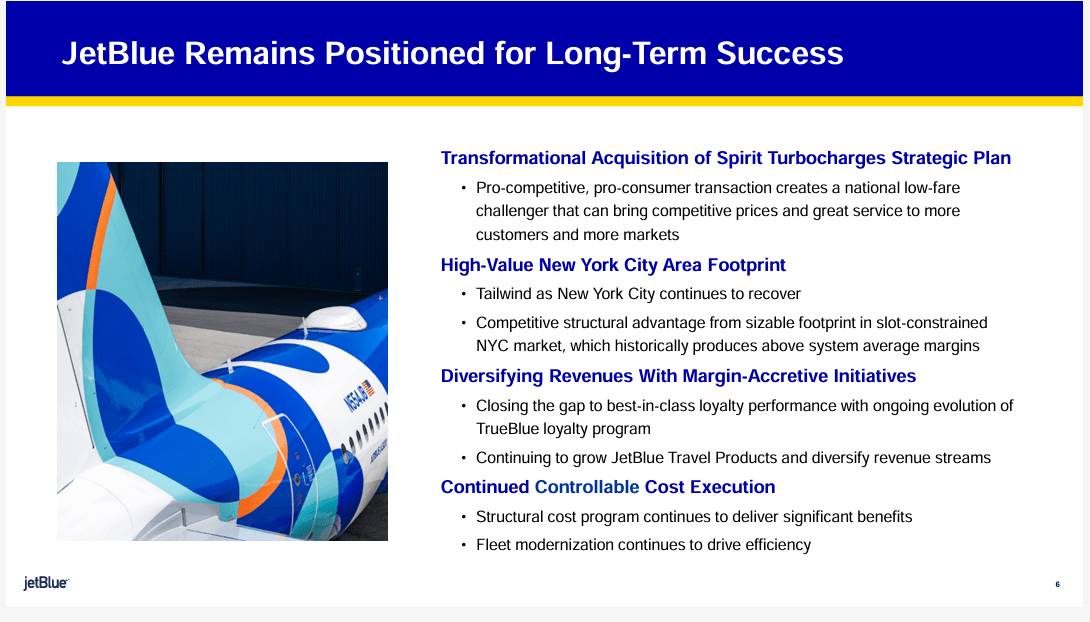

JetBlue highlighted in its 3rd quarter earnings presentation that it believes it has the right strategies for the long term and a balance sheet that will support those strategies.

JBLU long-term success 3Q2023 (JetBlue.com)

{kind=link}

Improved Operations

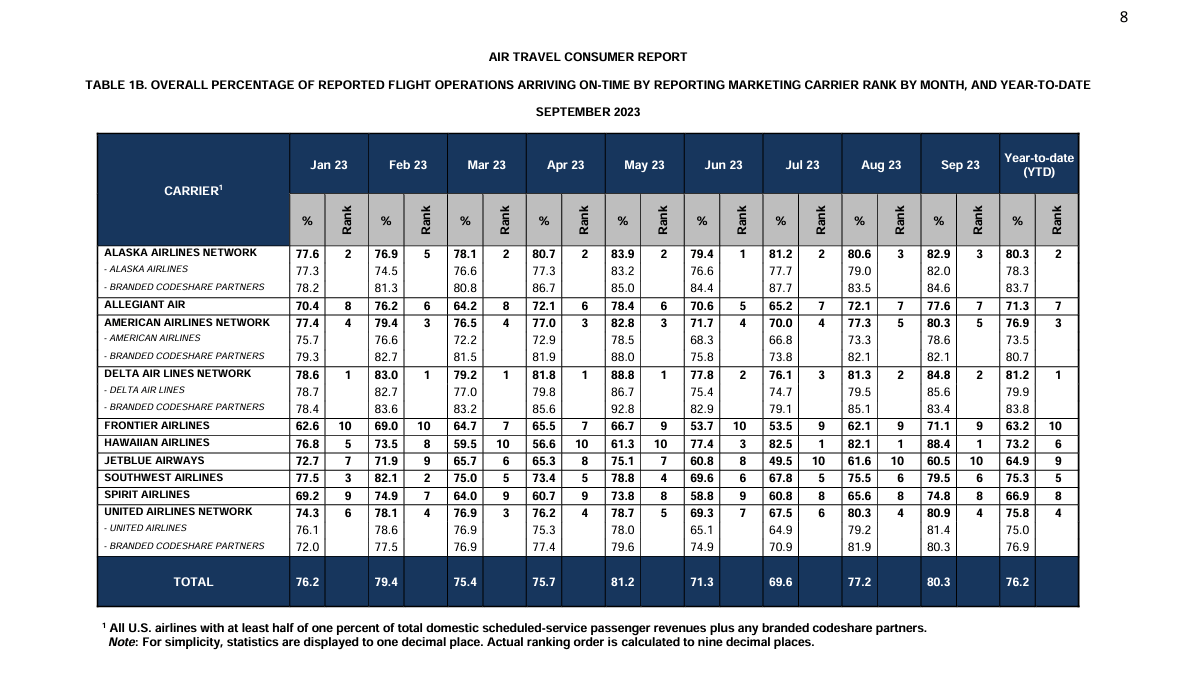

JetBlue’s improved finances are due in part to much stronger operational reliability not just for JBLU but also for the U.S. airline industry, which was significantly negatively impacted by the pandemic. JetBlue has long delivered one of the weakest operational performances of the U.S. airlines, both because of the high concentration of its network in congested NYC airspace but also because, as a low-cost carrier, JBLU needs to aggressively use its assets, not able to dedicate the spare assets – aircraft and crews – necessary to help recover from operational challenges when the operation struggles due to external factors. The U.S. Dept. of Transportation has been very critical of the operational challenges that U.S. airlines have faced including the staffing challenges that have strained reliability even as domestic and then later international demand returned with a vengeance.

Most of the U.S. airlines have been able to address their staffing challenges in the late summer and into the fall while the FAA’s strongly suggested restrictions on NYC airspace have alleviated operational challenges. While DOT on-time data lags actual performance by several months, the Air Travel Consumer Report shows that JBLU remained in the worst position among U.S. airlines as of September but more recent data from private sources shows improvement in JBLU’s performance during the traditionally less disruptive fall.

US airline on-time YTD Sept 2023 (US DOT)

{kind=link}

Unwinding Failed Strategies

JetBlue continues to adapt its network and strategies to comply with the ruling from a U.S. district court that led to the termination of the Northeast Alliance – NEA – with American Airlines. The NEA was an attempt by AAL to improve its use of slots at New York’s LaGuardia - LGA and JFK airports which had fallen below FAA usage requirements even before covid. For JBLU, the NEA provided the opportunity for growth at LGA as AAL transferred slots to JBLU while the reverse happened at JFK, all under an antitrust immunized joint venture. Although the DOT approved the slot transfer parts of the NEA, the Dept. of Justice moved quickly to sue to block the deal on the basis that no two U.S. airlines are not permitted to have antitrust immunity in the domestic marketplace. Although the DOJ lost a number of key merger cases, they re-established their track record of being against business combinations with the win from the federal court which required that the NEA be dismantled. AAL and JBLU both took steps to begin shutting down the agreement although American continues to appeal the ruling, primarily on the basis of challenging the DOJ’s ability to permanently shut down future antitrust immunized partnerships between U.S. airlines. AAL, like DAL and UAL, operates several antitrust immunized joint ventures with foreign airlines.

Part of AAL and JBLU’s revenue weakness in the 3 rd quarter – which is likely to continue into the 4 th quarter – is because of the rapid changes that both airlines have had to make to their networks. JBLU began the process of returning slots to AAL in October and the process will continue over the next several months with the same process being repeated at JFK in reverse. Consequently, both airlines are adding significant amounts of essentially new capacity to routes which they had hoped the other would operate as part of the NEA. In addition, AAL is no longer able to place its code on JBLU flights which helped to feed AAL’s long haul international flights, reducing revenue and undoing the loyalty program benefits that passengers of the two airlines enjoyed, even if on a temporary basis. While AAL and JBLU have both probably not fully disclosed the impact to their bottom lines from dismantling the alliance, it is likely that there will be benefit as the two readjust their networks, restart and optimize their presence on routes that they did not operate during the NEA, and strengthen their own internal marketing rather than relying on each other.

Pursuing A Historically Unique Merger

As if ending the NEA was not a big enough headache for JBLU, the airline finds itself in the uncomfortable position of also having its proposed merger with Spirit Airlines ( SAVE ) taken to court. While SAVE originally intended to merge with Frontier ( ULCC ) to join the nation’s two largest ultra low-cost carriers, JBLU stepped in to top ULCC’s offer and SAVE’s board and shareholders ultimately backed the JBLU deal which was sweetened by upfront and monthly payments to SAVE stockholders while the inevitable legal process plays out. JetBlue’s rationale for the merger is to create size and scope to compete with the big 4 U.S. airlines as well as to obtain the delivery positions for new aircraft that SAVE has on order – both JBLU and SAVE operate Airbus’ A320 family of jets – and the crews that support them. As with other low-cost carriers, JBLU has been handicapped by not having widebody long haul international routes which helps to boost pilot career earnings, making the U.S. global 3 carriers the most attractive destination amidst the current pilot shortage. While both JBLU and SAVE have boosted pilot salaries, attrition to the larger carriers still remains problematic.

The DOJ’s case against the JBLU/SAVE merger is based on JBLU’s intent, stated from the very beginning, to repurpose SAVE’s assets from the ultra low-cost to the low-cost carrier model, removing seats from every SAVE aircraft as they are reconfigured to a less dense configuration. In addition, moving from the ultra low-cost carrier model pricing is certain to increase fares for some passengers; even though the ultra low-cost carrier model features an unbundled product and few passengers buy solely basic air transportation without the “add-ons” which include baggage and other travel components, some degree of passengers will see the cost they spend on air travel to increase. The trial – also held in Boston but under a different judge – just ended last week. While JBLU already agreed to divest some assets including SAVE’s NYC and Boston assets to other ultra low-cost carriers, the DOJ’s stance during the trial was that there is no amount of divestitures that can address the anticompetitive nature of the merger proposal.

JBLU has argued throughout the defense of its deal that each of the big 4 have been allowed to merge with other carriers which has resulted in reduced competition and higher fares, even though all of the big 4 carriers are the product of mergers of “like” airlines – legacy/global carriers with other legacy/global carriers and low-cost carriers with low-cost carriers. JBLU argues that its merger should not be blocked given the DOJ’s previous policy of airline mergers esp. since the U.S. airline industry is heavily concentrated in the hands of the big 4 airlines. While a number of legal scholars have weighed in on arguments from both sides, many believe the DOJ did not make its case because U.S. antitrust law does not focus on the void left after a merger takes place – in this case the loss of lower-priced competitors in the industry – but rather on what will take place as a result of the merger of the companies that are proposing to merge.

Because JFK and LGA airports are slot-controlled, JBLU made the decision to essentially propose a no-growth scenario for itself in NYC. Termination of the NEA – which JBLU originally sought to defend – would have allowed JBLU’s position to be bolstered by AAL – but that option is not on the table. The federal judge in the NEA case did note that JBLU was free to apply to the DOT for a simple codeshare and marketing agreement which does not include antitrust immunity or revenue sharing in response to DOJ demands during that trial that AAL and JBLU dismantle all parts of the relationship and reapply for whatever it might choose to do in the future. AAL operates a non-immunized partnership with Alaska Airlines ( ALK ) on the west coast which both sides say has been beneficial; the AAL/ALK relationship also allowed ALK to join the oneworld airline alliance, of which American serves as one of the founders and primary carriers.

JBLU has wisely not chosen to pursue an appeal or engage in anything with American while its merger with SAVE plays out. JBLU has also agreed to divest gates at Ft. Lauderdale – FLL - where both it and Spirit operate hubs, making them the two largest carriers. The greatest overlap and the greatest potential for fare increases is likely in S. Florida where American is the largest carrier at its Miami hub. All three carriers have extensive networks to the Caribbean and the northern tier of Latin America although AAL has the most flights to most destinations. The combination of JBLU and SAVE will allow the combined carrier to compete more effectively if they maintain their combined frequencies. Although it has not stated that it intends to do so, JBLU could use its A321XLR, the longest range variant of Airbus’ largest narrowbody aircraft, to serve deep S. America esp. from S. Florida. The DOJ seems less concerned specifically with the overlap at FLL than the loss of ultra low-cost fares domestically.

It is the DOJ’s focus on the overall competitive situation and the desire to keep a large ultra low-cost carrier presence in the U.S. that some legal scholars believe could sway the judge in a decision that would favor JBLU. Further, the judge indicated that he does not believe that it is reasonable for the DOJ to ask for a permanent injunction of a merger between JBLU and SAVE given that the industry does evolve and JBLU is providing access for other ultra-low fare carriers to grow in some of the largest and most desirable airports. JBLU’s lawyers seemed stumped at a question regarding the potential for more divestitures, indicating that there could be a remedy acceptable to the judge that would go beyond what JBLU has already proposed.

While I personally believe that, if the merger is approved, JBLU will spend significantly more in pursuit of a merger net of divestitures and the costly retrofit of SAVE aircraft than it could have via other methods. However, from a legal standpoint, the trial seemed to end with the potential that the merger could be approved, something that seemed much less likely when it started, due to unreasonable expectations for the industry by the DOJ and an intransigence on finding a resolution. Final written submissions from each side are due this week, providing further insight and also providing the opportunity for each side to propose solutions before a ruling is made.

No Longer the Only U.S. Airline Merger

The end of testimony in JetBlue’s merger case last week coincided with an announcement from Alaska and Hawaiian Airlines of their intended merger with ALK becoming the acquiring carrier. ALK and JBLU competed to win Virgin America almost a decade ago after the latter carrier stumbled in its startup business plan. ALK ultimately won the merger contest but paid far more than it originally intended and then dismantled large portions of Virgin America’s network, retreating to Alaska’s core markets in the Pacific Northwest. All of ALK, HA, JBLU and SAVE face similar size and scale issues relative to the big 4 and recognize that they strategically need to better compete with the big 4.

Unlike the JBLU/SAVE merger, ALK and HA are both technically legacy carriers. Although ALK only operates the Boeing ( BA ) 737 family, HA has a fairly complex fleet composed of Boeing and Airbus aircraft with the Boeing 787 set to join the carrier’s fleet to support its service from Hawaii to Asia and the South Pacific, supplementing Airbus A330s which also serve the U.S. mainland.

The Alaska/Hawaiian merger could help JBLU/SAVE since it highlights that mergers are needed and likely need to happen in the middle tier of the U.S. airline int industry despite the DOJ’s opposition to any airline industry mergers. ALK and HA overlap in a number of west coast to Hawaii markets which is highly competitive just as is true for the eastern U.S for JBLU and SAVE. While it is certain that fares will increase as a result of the ALK/HA merger, the two carriers are not low cost or ultra low-cost carriers, potentially questioning whether the DOJ’s fixation on price increases due to elimination of a lower cost competitor is valid given that consolidation has happened between carriers of the same business model and would also occur in the ALK/HA merger.

Since all 4 airlines are headquartered in different states, there might be more economic pressure on the DOJ to modify its anti-consolidation stance. Although the ALK/HA merger will face its own review, the DOJ is not likely to make any comment on that merger until a decision is made on the JBLU/SAVE merger, which could happen early in 2024.

JetBlue Can Overcome its Challenges

JetBlue began operations just over 20 years ago as an innovative low fare, high amenity disruptive airline in New York City, the largest air travel market in the world. Although it has experienced some years of strong success, it has faced a number of challenges; 2024 has been a particularly challenging year for JetBlue. Its Northeast Alliance with American was ordered to be unwound. Its operation has been negatively impacted by caps on air traffic control capacity as well as aircraft groundings due to engine concerns. Its labor costs have grown due to the need to implement new wage rates in order to keep employees from jumping to larger airlines. Its merger with Spirit Airlines, intended to provide a platform for growth in a consolidated industry, has been challenged by the Dept. of Justice.

JBLU’s stock price performance and many of its metrics have been on the lower end of the U.S. airline industry, punctuated by a nice uptick in the last week. JBLU provided investor guidance that indicates revenue is strong. JBLU’s justification for its unique merger might have carried more credence than the DOJ’s case and the judge’s ruling might come in early 2024. JBLU continues to grow to Europe where the big 3 are seeing healthy revenues.

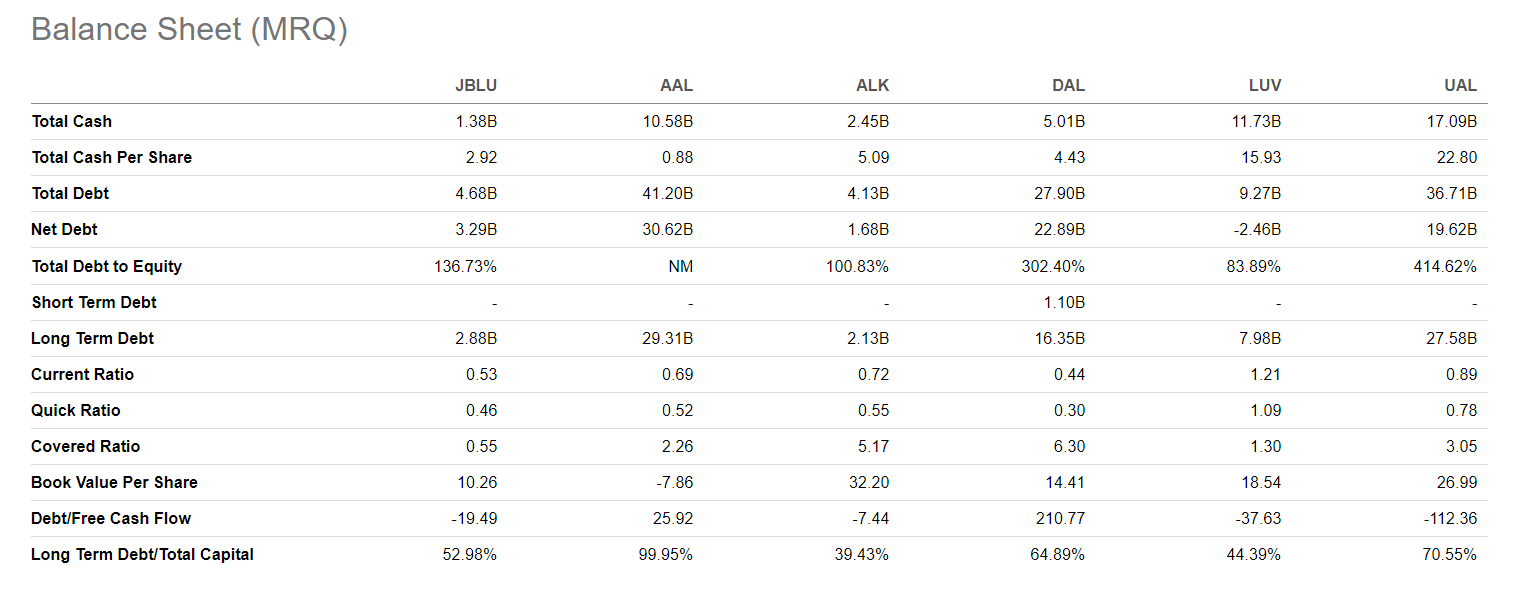

JBLU’s balance sheet is in relatively better shape than many of its larger competitors. It is valued far less than other airlines driven by investor concern about the number of strategic risks the company is taking and its lower levels of profitability.

JBLU v industry balance sheet 10Dec2023 (Seeking Alpha) JBLU v industry risk 10Dec2023 (Seeking Alpha)

{kind=link}

{kind=link}

The trajectory could be changing for JetBlue. It has demonstrated strong commitment to its strategies and is overcoming the macroeconomic factors that have created doubt in the airline industry.

Accordingly, I believe that JBLU stock has seen its lowest point and will continue to appreciate, although it will likely be more volatile than other airline stocks. JBLU justifies a BUY rating.

For further details see:

JetBlue Is Ready To Regain Its Destiny (Rating Upgrade)