JBLU - JetBlue Q1 Earnings: Riding A Pleasant Tailwind

2023-04-26 08:26:47 ET

Summary

- JetBlue Airways exceeded analyst expectations in its first quarter 2023 earnings report.

- JetBlue is seeing success in its current operational and strategic initiatives.

- JetBlue continues to push for two major strategic initiatives which are being challenged by the Dept. of Justice.

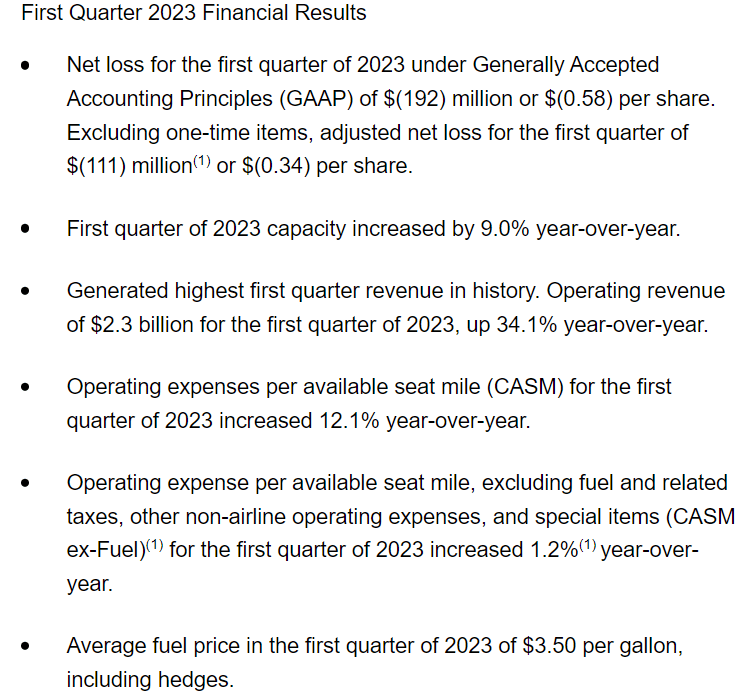

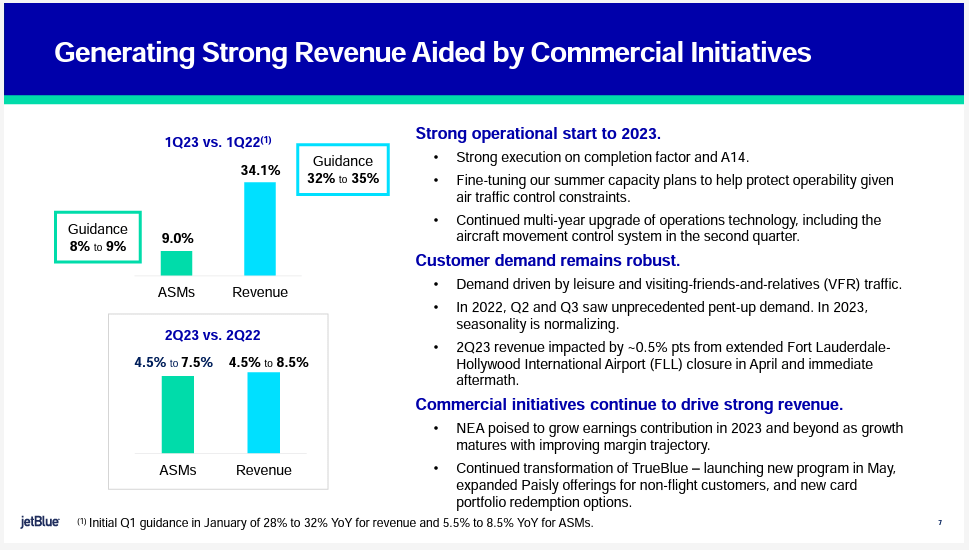

JetBlue Airways ( JBLU ) released its financial results for the first quarter of 2023 before the markets opened on 25 April 2023, beating analysts estimates by 4 cents/share but posting a non-GAAP loss of 34 cents/share while beating revenue estimates by $10 million. On a GAAP basis, JBLU's losses totaled $192 million or $0.58 per share. JBLU revealed that its first quarter 2023 revenue was the highest in company history, echoing similar statements from other airlines, esp. those with a strong presence to/from Florida. JBLU noted several factors for its stronger than expected performance including somewhat better weather than expected as well as a more stable operation. With their operation heavily concentrated in the delay-prone Northeast corridor of the United States, JBLU's operational performance and earnings are some of the most sensitive to bad weather of any U.S. airline. JBLU says that its loyalty program and credit card partnership are providing strong revenue while the New York City market continues to see increased demand, reversing the trend from last year. Capacity increased 9%.

{kind=link}

JBLU also noted strength from the Northeast Alliance, the U.S. DOT blessed arrangement which JBLU has with American Airlines ( AAL ) that, at its root is intended to improve usage of New York City airport slots which AAL was not fully using prior to covid. Under the arrangement, AAL and JBLU can coordinate schedules and share revenues on certain domestic markets to/from NYC and Boston. JBLU has very likely disproportionately benefitted with additional new flights by using slots that were previously assigned to American.

On the cost side, JBLU kept its operating unit costs ex-fuel or cost per available seat mile - CASM - at just 1.2% growth, a respectable showing indicative of the value of reinstating growth, an essential ingredient to low cost carrier strategies in order to limit cost growth. On an all-in basis, JBLU's CASM grew 12%, reflecting a $3.50/gallon price for jet fuel. JBLU reinstated hedges after not doing so for a number of years and believe that the tool will be most helpful in fuel cost budgeting during increasing fuel price periods although the company was slightly underwater on its hedges in the first quarter.

Guidance for a Strong Remainder of the Year

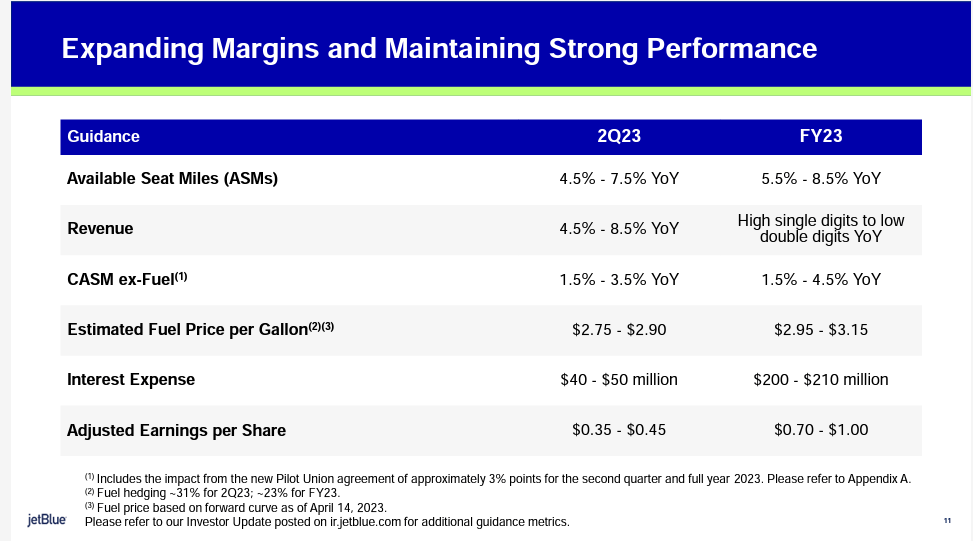

The best news coming from JBLU was that it expects the second quarter to remain strong with capacity growing by 4.5 to 7.5%, revenue growing by a similar to slightly higher level, and for its non-fuel cost basis to accelerate only slightly from the most recent quarter, leading to an expectation for in the second quarter of $0.35 to $0.45/share. On a quarter over quarter basis, JBLU's fuel cost estimation is expected to fall by 7-10% excluding the apparent negative impact from hedges in the first quarter.

On an annualized basis, JBLU expects its financial rebuilding to continue with capacity and revenue growth accelerating into the summer and potentially beyond. JetBlue execs noted that the first quarter is typically the carrier's most challenging and they expect to share in the continued strong demand patterns that are expected in their core northeast and eastern U.S. markets.

{kind=link}

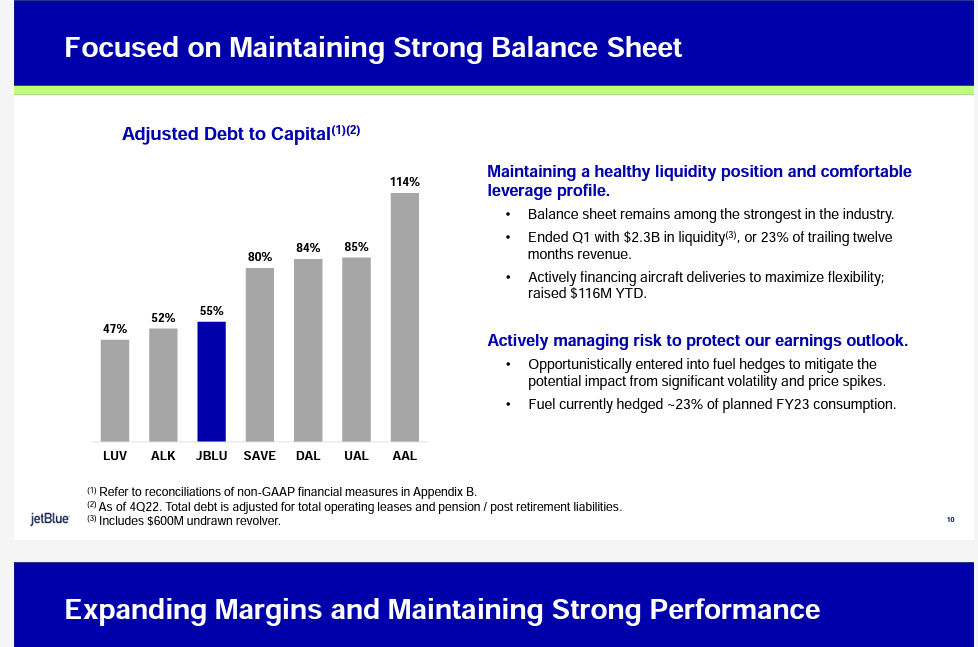

As is true for much of the low cost carrier sector, JBLU's balance sheet is in better relative shape than the larger legacy carriers with JBLU's debt metrics landing pretty close to right in the middle of the industry.

{kind=link}

{kind=link}

Amsterdam, JetBlue is Coming!

JetBlue execs were delighted to share the news that the company has published schedules to begin service to Amsterdam starting in the fall from both Boston and New York/JFK, building on its current service to both London Heathrow and Gatwick airports which will total 5 flights/day this summer and new service to Paris that will start in the spring. JetBlue set out to expand its wings across the Atlantic, becoming an early advocate for the Airbus A321XLR, the longest range narrowbody (single aisle) aircraft I production. While the -XLR will not be entering service until next year, as expected, due to continued government certification, JBLU can operate service to the United Kingdom and "near continental Europe" using other A321NEOs, now having experience crossing the Atlantic in the winter. Because JBLU is using narrowbody aircraft with a high percentage of premium cabin seats, their total number of seats is relatively small compared to the big 3 (American, Delta and United) as well as their British and European joint venture partners. In all of the markets that JBLU serves across the Atlantic, JBLU capacity is a small fraction of total capacity - but also leads to elimination of the charge that JBLU frequently leveled that it was being locked out of key markets in order to support the dominance of the established large carriers. While JetBlue has fought hard to gain access esp. to London and Amsterdam, it will be much harder for them to continue to expect to gain slots on a limited cost basis; in addition, narrowbody transatlantic flights will only operationally work from a limited number of cities outside of the northeast. Nonetheless, each of the big 3 are noting strong demand on their flights across the Atlantic, a longer season, and a shift in pricing strength from their highest priced cabins in favor of stronger leisure and premium economy-type tickets, all of which make for a very favorable environment for JBLU as it expands its transatlantic service. While the company expects to continue to grow to more cities in Europe, the economic success of its narrowbody model will take time to assess, esp. as other airlines including American and United ( UAL ) begin to receive their own A321XLRs; notably, Delta ( DAL ) aligns with the European legacy carriers in not expressing interest in narrowbody transatlantic operations, with the Atlanta-based carrier saying that labor costs are not favorable for transatlantic flights on narrowbody aircraft given the relatively small number of seats compared to widebodies and the need to include a third pilot on many transatlantic flights.

JetBlue's transatlantic growth supported by a fleet plan shows that the New York-based airline will continue to take modest deliveries of new A321NEOs (of which the -XLR is one subtype) as well as the A220-300, the 140 seat all-new small narrowbody that has best-in-class unit costs and cross-country range. JBLU expects to begin accelerating retirement of older A320s and its E190 aircraft and notes that removal of the latter is leading to significant reductions in costs. JBLU has taken charges for retiring its E190s so is in a position to benefit as those aircraft are retired.

JBLU order book 1Q2023 (JetBlue.com)

Northeast Capacity Crunch

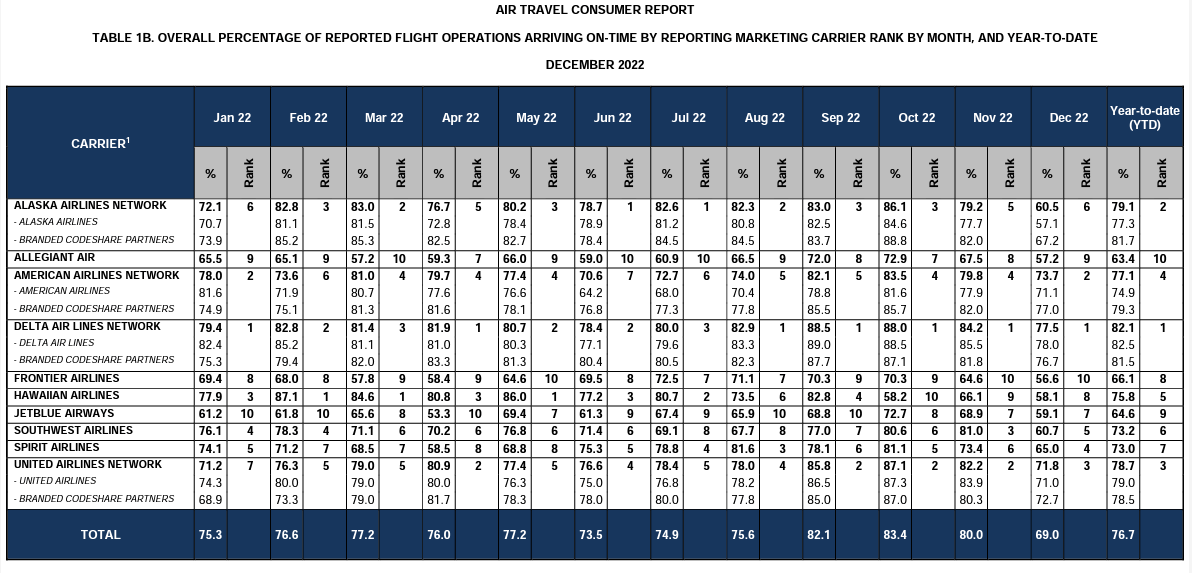

While JBLU execs are pleased with the performance of their new transatlantic routes, they voiced clear frustration with air traffic control shortages that led the Federal Aviation Administration to ask U.S. airlines to reduce capacity to/from a number of northeast U.S. airports, predominantly concentrated on New York City and LaGuardia and JFK airports which are slot-controlled. JBLU, like all of the big players in the northeast, has worked with the FAA to reduce schedules, with a general reduction in short-haul flights within the northeast while retaining as many long and medium haul flights that maximize revenue generation from the precious airport departure and arrival slots. While JBLU execs noted that they are pleased that the FAA is recognizing and preemptively addressing potential operational challenges, they note that FAA staffing is more on par with ten years ago than even before covid. The airline expects the summer of 2023 to be particularly challenging and believe they are adequately prepared. In 2022 and for many years before, JBLU's on-time was one of the lowest in the U.S. airline industry, leading to reduced customer satisfaction scores as well as other DOT-reportable metrics.

DOT on-time for CY2022 (DOT Air Transportation Consumer Report)

{kind=link}

JetBlue's Strategic Dependence on the DOJ

JetBlue is in a unique position among U.S. airlines in having two major initiatives that is engaged in or pursuing being sued by the Dept. of Justice. Its Northeast Alliance with American, was challenged by the DOJ, leading to a trial in a Boston court which has already been heard; expectations are that an announcement of the judge's decision could come at any time but JetBlue's merger proposal with Spirit Airlines ( SAVE ) - which was announced before the NEA trial was concluded - make it hard not to separate the two cases.

The Northeast Alliance has several unique features which make it in many ways more problematic than the merger proposal. AAL and JBLU have the ability to coordinate schedules and revenue share, even on a limited basis, something the DOJ does not allow two domestic airlines to do. In addition, the DOJ argues that the alliance reduces the likelihood that JBLU will serve as a check against higher prices by the larger legacy airlines, an attribute that JBLU uses to support its own merger proposal with SAVE. Several states have joined the DOJ in its challenge of the NEA, noting the concentration between American and JetBlue on a number of routes to/from New York City and Boston. As noted above, the NEA has allowed JBLU to add a number of new flights, esp. in markets where AAL has not been able to profitably operate but where JBLU's lower costs likely make those flights viable once again.

JetBlue's merger proposal with Spirit Airlines serves in contrast to the NEA in that it combines two smaller airlines; JBLU forcefully and accurately notes that it will still be much smaller than the big 4 (including Southwest) and has lower costs than each of those airlines, allowing the price reduction mechanisms that both are known for to continue. However, the largest problem that JBLU faces is that SAVE is an ultra-low cost carrier and the merger will result both in a reduction in capacity as seats are removed from each SAVE aircraft in the process of converting them to JBLU configurations and in an increase in fares; SAVE's ultra-low cost carrier model uses cafeteria-style pricing to allow customers to buy a very low basic air transportation ticket and then add on services that each passenger deems as valuable. JBLU's pricing model is much more like the legacy carriers', making it likely that the majority of customers will pay more than they would have under the SAVE model but not as much as the legacy carriers.

Managing a Tight Labor Supply

JetBlue faces a couple of unique challenges from a labor cost perspective: first, it heavily operates from northeast airports where labor costs are higher, on average, than in other parts of the country and also because escalating airline labor rates erode many of the benefits of the low cost carrier model, esp. for pilots. JBLU acted fairly early to extend its union contract with its pilots to ensure that it is able to compete for pilots; many low cost carriers, including at JBLU, start their careers from flight schools and in-house pilot development programs or from regional airlines, where the pilot shortage is most pronounced. All of the big 3 airlines have noted that they are not flying all of the regional jets they own or contract for because of the pilot shortage; while salaries for regional jet pilots have increased dramatically over the past two years, the movement of pilots in the industry has made training new pilots challenging.

JBLU noted on its earnings call that its in-house pilot training program is working and they expect to have 1000 pilots in their program or having completed it very shortly. They also are allowing current non-pilot JBLU employees to apply to the program and be trained by the company after a minimum of two years in their current job. Other low cost and ultra low cost carriers report challenges filling their pilot training classes; part of the original justification for the merger with SAVE was to obtain pilots that are already flying and to have access to SAVE's current fleet and order book.

JBLU Stock Outlook

Even the theme across the U.S. airline industry during the current earnings season has been positive (half of U.S. airlines have yet to report), stock movement has been sluggish at best. Airlines have historically been tied to two major factors: general macroeconomic conditions and fuel costs. I have long argued that the general sentiment toward the stock market as a whole should not apply to the airline industry because airline stocks were heavily depressed during covid and have still not recovered. Some airlines, predominantly the big 3, are reporting or guiding to margins close to or exceeding pre-covid levels based on strong demand - and yet airline stock movement has not reflected the positive outlook. Fuel remains a concern for airlines, although airlines are more fuel-efficient than ever and JBLU joins a few airlines including Southwest ( LUV ) and Alaska ( ALK ) which have hedging strategies, and DAL, which is benefitting from its unique refinery strategy. Despite what certainly appears to be some of the best management the U.S. airline industry has seen in more than 40 years of deregulation, airline stocks are still viewed in poor favor.

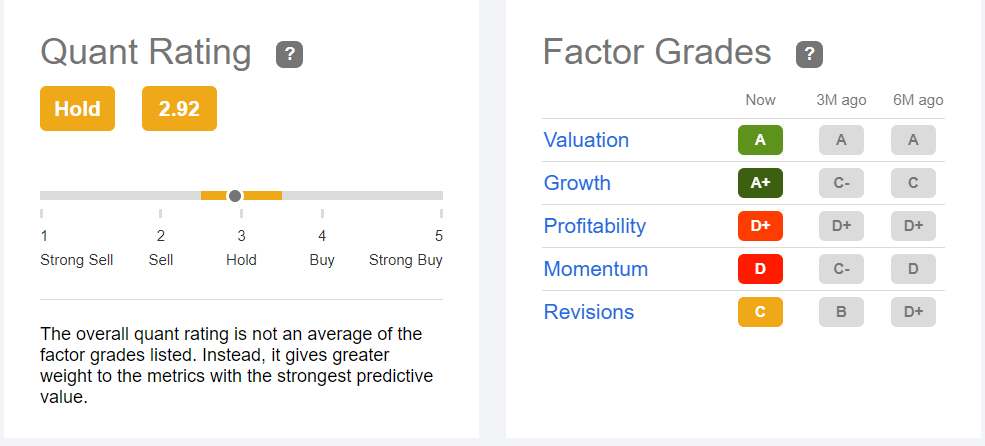

JBLU ratings summary 25Apr2023 (Seeking Alpha)

{kind=link}

{kind=link}

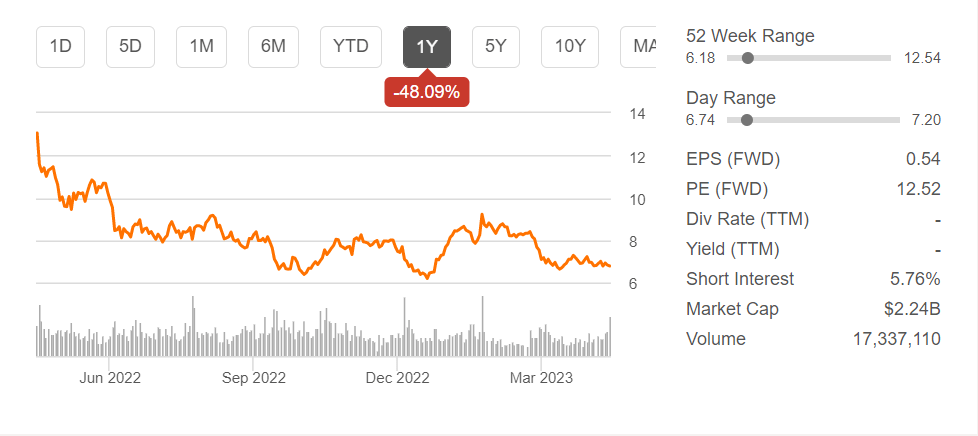

Specifically, JBLU has fallen 48% in the past year, one of the deepest dives in the industry, a result of both weak results for a number of quarters and the uncertainty regarding JBLU's two major strategic initiatives. JBLU sports a hold from the Seeking Alpha Quant system as well as SA and Wall Street analysts. Low profitability and momentum continue to be problematic for JBLU.

A return to profitability for JBLU is great news for investors but will not be able to overcome the overhang from government uncertainty. If the Northeast Alliance receives a favorable green light, some of the stock's uncertainty would be removed but approval of the merger could drag on into 2024. JBLU continues to make payments to SAVE stockholders as part of its commitment to the merger.

While JBLU appears to be addressing its key challenges as a current standalone company better than it has since the pandemic began and perhaps even earlier than that, JBLU will likely to continue to underperform the larger global airlines which not only also serve the strong domestic market but are receiving outsized support from international longhaul market demand.

Considering all of these factors, JBLU rates a HOLD from me -but that is not significantly different than a number of other airlines. Hopefully, 2023 provides more clarity about the future for JetBlue but in the meantime, current JBLU stockholders will see some appreciation in their holdings from covid-era depressed levels. In the meantime, JBLU will enjoy some pleasant tailwinds.

For further details see:

JetBlue Q1 Earnings: Riding A Pleasant Tailwind