JBLU - JetBlue - Spirit Airlines Merger Hits Roadblock Spirit Stock Has Upside

2023-03-08 11:01:32 ET

Summary

- The DoJ is attempting to block the JetBlue-Spirit combination.

- Opposition was expected, but JetBlue reached one prime target, and that's preventing the combination of a bigger ultra low-cost carrier.

- Spirit Airlines stock is the better investment with significant upside.

A year ago, Frontier Airlines (ULCC) attempted to combine its operations with Spirit Airlines (SAVE) to create a big ultra-low cost carrier. JetBlue (JBLU) threw itself into the bidding for Spirit Airlines and ended up on top, but with both potential combinations significant regulatory opposition exists, which I outlined in a report as part of my extensive coverage following the acquisition of Spirit Airlines. Indeed, we're now seeing that the DoJ is attempting to block the combination of JetBlue and Spirit Airlines supported by the Department of Transportation.

That there would be an attempt to block the deal does not come as a surprise, what is however surprising is that the opposition primarily focuses on the cost-conscious traveler, but that's not odd as we assess in this report.

Why Did JetBlue Want To Buy Spirit Airlines?

{kind=link}

Let's first discuss why JetBlue wanted to buy Spirit Airlines in the first place. That was actually not so much driven by JetBlue looking for a partner to merge with. What happened is that as Frontier Airlines did bid for Spirit Airlines, JetBlue would see itself ending up as the weaker player in a further consolidated market with significantly ultra-low-cost pressure in their key markets such as Florida, the New York-Boston area and Las Vegas. By blocking the combination with Frontier Airlines, JetBlue would already have what it wanted.

Beyond that there were other reasons to actually be interested in Spirit Airlines. Spirit Airlines aims at an aggressive market penetration and to be frank that would hurt JetBlue most. JetBlue prides itself as bringing the JetBlue effect to legacy carriers, forcing prices down. Their argument for approving the combination with Spirit Airlines is that as a bigger airline they could compete more effectively with the legacy carriers and bring down prices even more. However, none of that fits with the reality that Spirit Airlines post acquisition would see its business model disappear as the aircraft would be reconfigured closer to JetBlue configuration. That's where the focus of the Department of Justice on cost-conscious travelers is interesting. The DoJ argues that aircraft would be configured less densely and the ancillary revenues business set up where customers pay for the services and products require would be eliminated. For years, we have been seeing how there's some opposition against letting travelers pay for every bit of service they require but the DoJ is now highlighting densely-configured aircraft and having to pay for everything as a nice business model. With that, the DoJ aligns itself in a trend where service and comfort is eroding. So, while good for the cost conscious traveler the DoJ also sends a questionable signal to the industry.

Another reason why JetBlue would be interested in Spirit Airlines is the simple fact that JetBlue is some steps behind in its fleet renewal and Spirit Airlines has aircraft on order that could support the JetBlue fleet renewal. So, what Spirit Airlines has in the order books with aircraft manufacturers to grow and compete more fiercely is what JetBlue wants to use to update its fleet.

The Spirit Effect Is Stronger Than The JetBlue Effect

The big issue for JetBlue has been ultra-low-cost pressure, the company claims it's more effective than Spirit Airlines in forcing fares down. Reality is that in response to ULCC market penetration, legacy carriers have altered their main cabin segmentation and in fact in response to that and more particularly in response to Spirit Airlines even JetBlue was forced to lower its prices which was sparked mostly by Spirit Airlines which forced legacy carriers to drop prices and JetBlue got caught by that as well. So, the idea of a bigger carrier exerting more pricing pressure on legacy carriers is not particularly true and there will be no compounded Spirit-JetBlue effect as JetBlue aims to eliminate the Spirit ultra-low-cost business. That's also why the DoJ has not provided extensive comment on pricing pressures from the JetBlue-Spirit combination on legacy carrier pricing.

The Spirit Airlines JetBlue Merger Details

{kind=link}

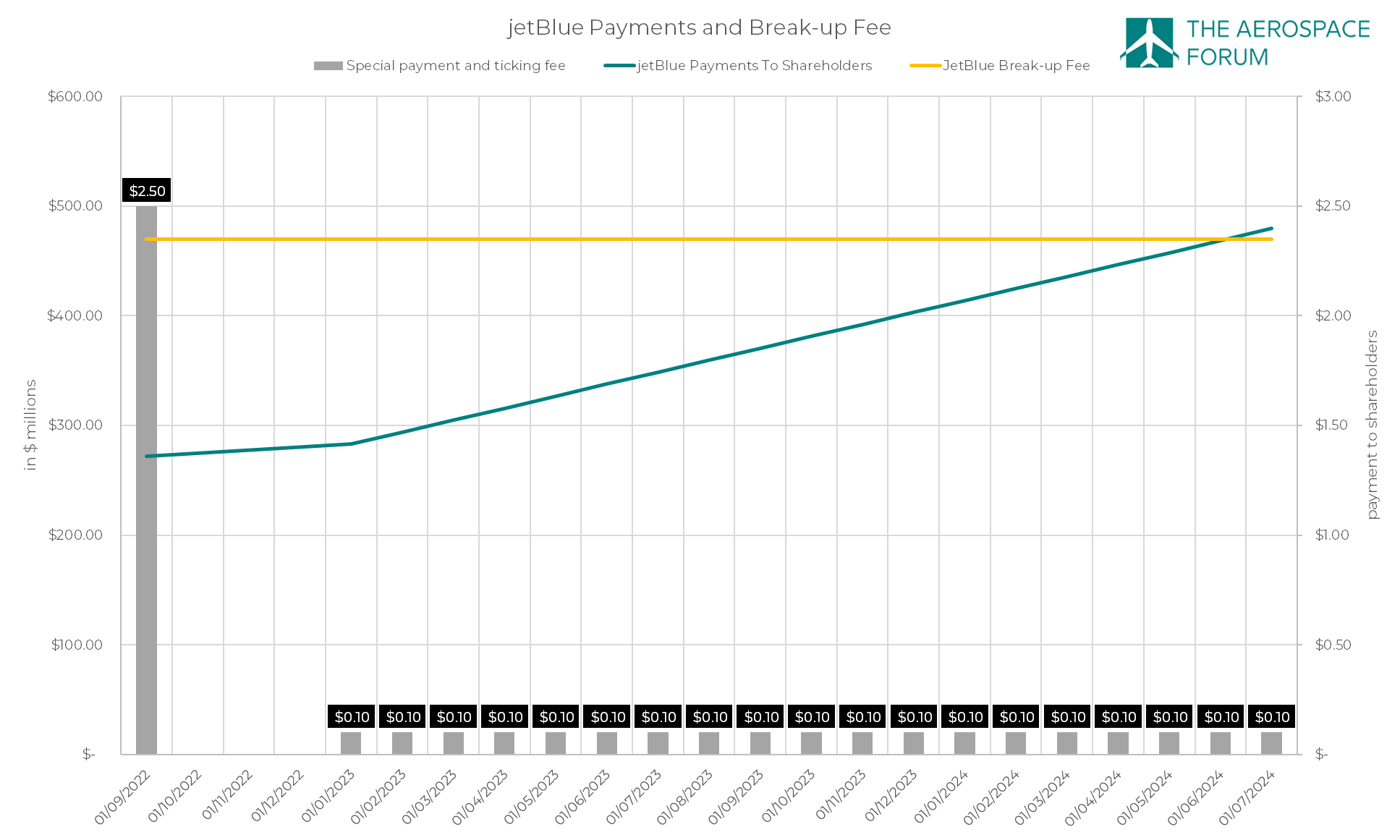

JetBlue offered $3.8 billion or $33.50 per share. This includes a $2.50 per share payment which happened on approval of the JetBlue takeover by Spirit Airlines shareholders and a $0.10 ticking fee starting January 2023. With the combination in jeopardy, it's also interesting to look at the break-up fee conditions which was one reason for JetBlue to end up on top of Frontier Airlines to acquire Spirit Airlines. If Spirit Airlines walks away from the proposed combination, it will have to pay $94.2 million to JetBlue. If JetBlue walks away from the merger agreement, it will pay $70 million to Spirit Airlines and $400 million to Spirit Airlines shareholders. That's where it becomes interesting. Investors are now looking at the break-up fee as being a positive to the deal falling apart. The reality is that shareholders have little to gain here. The deal is structured such that the payment to shareholders upon termination is $400 million less all payments that were already made which includes a ticking fee of $0.10 per month and the $2.50 special payment. By the end of the year, JetBlue would already reach that $400 payment to shareholders. So, only a merger termination before that point will actually be beneficial to shareholders as it accelerates the payment. However, we also see that the complete payment of $470 million upon break-up is structured such that by the time JetBlue hopes to have the deal fully approved, it will have returned approximately $470 million to shareholders. That means that with the break-up fee in mind there is little reason for JetBlue to walk away from the merger at a point earlier than July 2024.

JetBlue or Spirit Airlines: Which Stock Is The Better Buy?

As it became clear that chances of a regulatory approval were slimming, Spirit Airlines stock lost over 10% while JetBlue shares went higher. The fact that JetBlue stock gained is not odd given that it would likely be financing the Spirit Airlines acquisition with debt. Spirit Airlines stock went lower as it seems that the $29.80 offer per share excluding the special payment of $2.50 per share and the ticking fee of $0.10 per month will not materialize. However, there's one big advantage that I think Spirit Airlines has over JetBlue and that's really the Spirit effect, which is way stronger than the JetBlue effect meaning that Spirit Airlines can continue pressuring legacy carriers as well as other low-cost carriers while JetBlue is stuck trying to pressure legacy carriers but feels the pressure from ultra-low cost competition. One thing that I reiterated several times when covering the Spirit Airlines acquisition is that Frontier Airlines did not value the business as it would acquire using pandemic share prices while acquiring a business with a lot of potential. By the end of 2018, Spirit Airlines was trading at roughly $40 per share or a $2.75 billion market cap. Currently the stock trades at roughly $17, which is way lower than pre-pandemic prices. However, since then shares outstanding increased 60%. On a comparable basis that would still give Spirit Airlines a normalized share price of $27 and a $1.9 billion market cap. For an airline that's able to pressure the legacy carriers and aspires a high growth rate, the current share prices do not reflect in the slightest Spirit's future strength and growth as a standalone business.

Fellow Seeking Alpha contributor Bram de Haas sees 87.65% upside for Spirit Airlines stock, but that's under the assumption that after the valid points made by the DoJ approval for the transaction is gained after all which I don't think is the base case at this time. It's very hard to value airline stocks as we had several years of hardship for airlines which messes up the data points a bit, but pre-pandemic from 2013 to 2019 the average EV-to-EBITDA for Spirit Airlines was 8.6x. Currently Spirit Airlines is trading at 7.1x EV-to-EBITDA (forward) suggesting that in order to be in line with the historic multiple there is 21% upside though it should be noted that from 2013 to 2019 Spirit Airlines traded 3 out of 7 times at a 7.1x multiple. Bringing the company to sector perform would indicate 54% upside and I actually don't see why that could not be the potential of Spirit Airlines given their strength as an ultra-low cost carrier that can force fares down on the US domestic market and the Caribbean.

By 2024, the EBITDA margin is expected to rise to 15% and 16.6% in the year after. Using an enterprise value of $4 billion to $4.8 billion that would imply 83% upside by 2024 based on an enterprise value of $4 billion and based on an enterprise value of $4.8 billion the upside would be roughly the same but it would be achieved by 2025. If we align the EV-to-EBITDA multiple to the average for Spirit Airlines, we would get to 10 to 35 percent upside for this year and 125 to 170 percent upside by 2025. So, it seems that whether Spirit Airlines is acquired or not the company should be able to do well as a stand-alone company.

Conclusion: Deal or No Deal, SAVE Stock Is A Buy

I can perfectly understand why a combination with JetBlue would ultimately be blocked. I don't see high chances at this moment for the deal to gain regulatory approval. However, the break-up fee is not necessarily going to be a relief to investors as the fee is set up in such a way that at the time the ticking fee will no longer be paid out JetBlue the compounded costs of paying a special dividend and a ticking fee will more or less equal the break-up fee meaning there is no big financial incentive for JetBlue to walk away from the deal earlier than that.

In the end, whether the deal happens or not, JetBlue is either going to pay $3.8 billion and harvest the yield preservation over the long term or pay $470 million to prevent a bigger ULCC combination from rising. The company itself has to figure out how it is going to position itself in the future as a stand-alone business because it is attempting to pressure legacy carriers while it started suffering more ultra-low-cost pressures as well and as a result is trapped in the middle.

When it comes to the strength of both airlines as standalone businesses, I do believe that Spirit Airlines has the upper hand and I could see its business approach resulting in significant double-digit returns in the years to come, perhaps even triple digits. As a result, I do believe that if you believe in the low-cost strength of Spirit Airlines and their growth prospects this could be a compelling point to buy Spirit Airlines stock.

For further details see:

JetBlue - Spirit Airlines Merger Hits Roadblock, Spirit Stock Has Upside