BACRP - JPC: Best To Dollar Cost Average In Until Rates Peak

Summary

- Americans today are ever more desperate for new sources of income due to the rapidly increasing cost of living.

- JPC invests in a leveraged portfolio of fixed-income securities in an effort to provide us with a high level of current income.

- The fund's share price has been declining all year, which is likely to continue until interest rates peak.

- The fund is covering all of its distributions solely with net investment income, which is a very nice thing to see as it should ensure sustainability.

- The fund is currently trading at a much larger than normal discount to the net asset value.

It is not likely to be a surprise to hear that many Americans have been desperately trying to increase their incomes over the past year or two. This is in direct response to the inflation that has been plaguing the economy, particularly in the necessary categories of food and energy. For many people, their efforts have been focused on taking on second jobs or performing odd tasks for others. Fortunately, as investors, we have other options available to boost our incomes. One of the best of these is investing in the shares of a closed-end fund that specializes in the generation of income. These funds are somewhat underfollowed by many but they provide a great way to easily acquire a portfolio of assets that is managed by professionals that can in many cases deliver a higher yield than just about anything else in the market. In this article, we will discuss the Nuveen Preferred & Income Opportunity Fund ( JPC ), which currently yields a respectable 8.64%. I have discussed this income-focused fund before but more than a year has passed since that time so obviously, a great many things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund’s finances. Thus, let us proceed onward and see if this fund could be a good addition to a portfolio today.

About The Fund

According to the fund’s webpage , the Nuveen Preferred & Income Opportunities Fund has the stated objective of providing its investors with a high level of current income. This is not surprising considering that the name of the fund implies that it invests in preferred stock and other fixed-income securities. These securities are generally purchased by those investors that are seeking income because they deliver the overwhelming proportion of their investment return in the form of direct payments made to the investors. This is because these securities do not have any direct link with the growth and prosperity of the underlying company. Thus, there is no reason for them to increase in value as the company’s profits grow since these securities have no claim to these profits. Rather, these securities tend to rise and fall in conjunction with interest rates. The reason for this is fairly easy to understand. A newly issued bond, for example, will have an interest rate that corresponds to the prevailing market rate at the time that it was issued. As such, already existing bonds will adjust in price so that they deliver the same yield-to-maturity as an existing bond with similar characteristics. This means that bond prices decline as interest rates rise and vice versa. The same applies to preferred stocks since they are basically bonds with no maturity date.

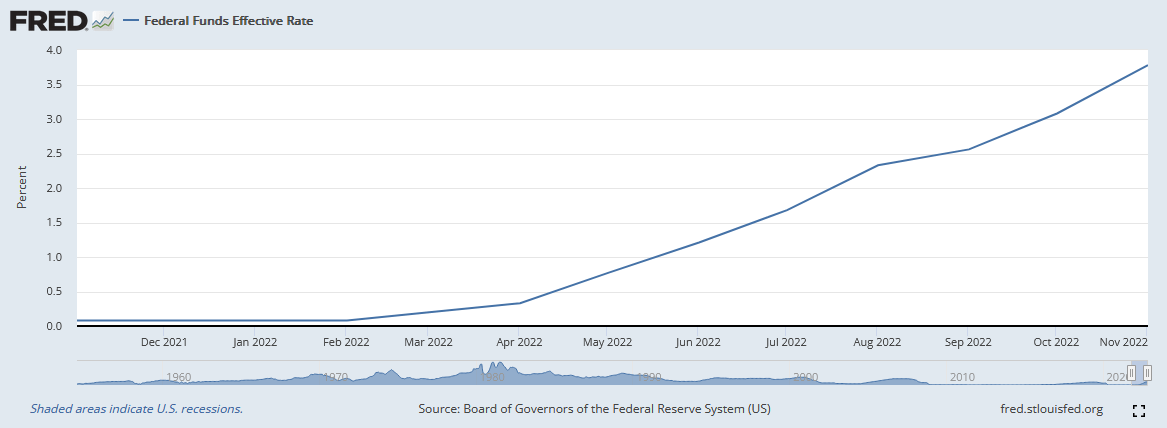

As everyone reading this is no doubt well aware, the Federal Reserve began tightening monetary policy earlier this year. The federal funds rate, which is the benchmark interest rate for the American economy, was 0.08% back in February 2022 but it is 3.78% today:

Federal Reserve Bank of St. Louis

{kind=link}

This has been great for those that are saving money in the bank as the interest rate paid on deposit accounts has increased significantly over a very short-term period. However, it has had the effect of driving down bond and preferred stock prices. As of the time of writing, the iShares Preferred and Income Securities ETF ( PFF ) is down 18.46% year-to-date. The Nuveen Preferred & Income Opportunities Fund has certainly not been unaffected by this as the value of its assets has also fallen over the time period. This fund is down 24.37% year-to-date. Although this is quite a bit more than the index fund has fallen, the fact that the Nuveen fund has a significantly higher yield helps to offset the difference, although it has still underperformed the index fund overall.

This price weakness is likely to continue for a while yet. The Federal Reserve is generally predicted to continue hiking rates over the next few months, although it is in debate at what level interest rates will peak. Following today’s CPI miss to the downside, many banks have begun predicting that the Federal Reserve’s hawkish policy will not be as long as was projected over the weekend. Morgan Stanley, for example, now projects that the federal funds rate will peak at 4.625% by March 2023. There are very few predictions that the central bank will not raise rates over the next two committee sessions though, so we are likely to still experience a few more months of declining prices for the fund. However, it is still difficult to predict when the share price will bottom out so it might be best to slowly accumulate a position as opposed to trying to catch the bottom.

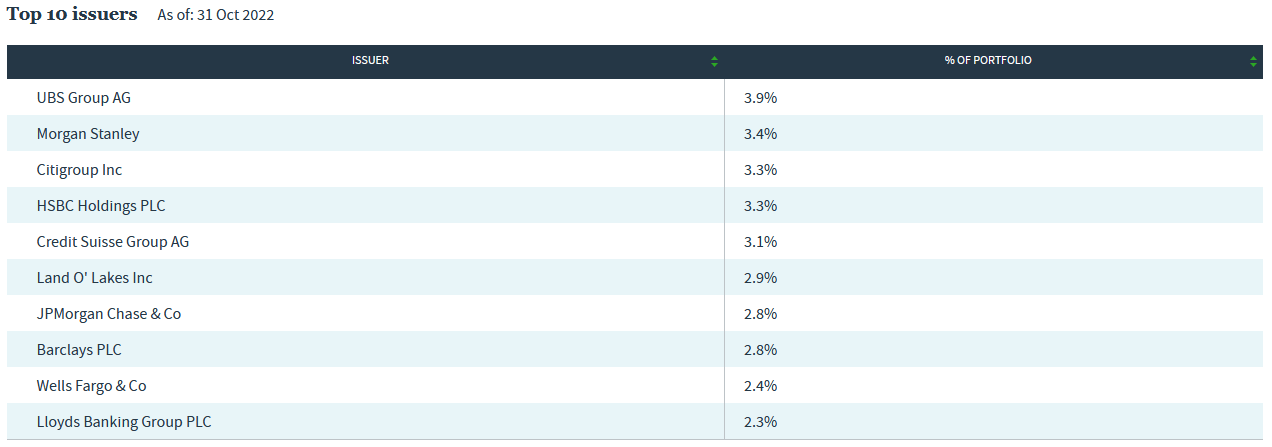

As is frequently the case with preferred stock funds, the majority of the fund’s largest positions are banks or other financial institutions:

{kind=link}

This is typical because the banking sector is by far the largest issuer of preferred stock in the market. The reason for this is international banking regulations. In short, banks are required to maintain a certain proportion of their assets in the form of Tier one capital. Tier one capital is the degree of assets that a bank has that are not also liabilities to someone else (such as a depositor). The only two ways that a bank can increase its Tier one capital are by issuing common stock or issuing preferred stock. Thus, when a bank needs to increase its Tier one capital, it will usually issue preferred stock in order to avoid diluting the common equity holders. There is little need for companies in other sectors to issue preferred stock because they do not need to comply with these regulations and preferred stock is more expensive than debt. Thus, the banking sector is left as the major player in the preferred stock marketplace by default.

The largest positions in this fund are largely the same as the last time that we looked at the fund, although the weightings of many of the individual issuers have changed quite a bit. That can easily be explained by one company’s securities outperforming another in the market, though. The only significant changes that we see here are that Bank of America ( BAC ) and CHS Inc. were replaced by Morgan Stanley ( MS ) and Barclays ( BCS ). For the most part, though, the largest positions in the fund have consistently been preferred securities issued by some of the largest banks in the United States and Europe. This overall consistency may lead some readers to believe that the fund has a very low turnover rate. This is actually not the case as the fund’s 71.00% annual turnover is on the high side for a fixed-income fund. The biggest reason why we are concerned about the fund’s turnover is that trading fixed-income assets costs money, which is billed to the shareholders. This creates a drag on the fund’s performance and makes management’s job somewhat more difficult. This is because it requires management to deliver sufficient returns to both cover these extra costs (when compared to an index fund) and still satisfy the fund’s shareholders. There are very few management teams that manage to accomplish this consistently, which is one reason why passive index funds frequently outperform actively-managed funds.

One thing that we note from looking at the largest positions on the list is that the fund invests in both American and non-American companies. In fact, currently, 37.7% of the fund’s assets are invested in fixed-income securities from foreign companies:

{kind=link}

This is something that is nice to see because of the protection that it provides us against regime risk. Regime risk is the risk that some government or other authority will take some action that has an adverse impact on a company that we are invested in. In this case, the biggest advantage that having exposure to multiple countries provides us is the diversification of interest rate regimes. As mentioned throughout this article, the Federal Reserve has been aggressively raising rates, but not every central bank around the world is being quite as tight with respect to monetary policy. In fact, the Bank of Japan has not raised interest rates yet this year. As a result of these varying interest rate policies, the bonds and other fixed-income securities issued by companies in different nations will perform differently. The fact that the fund has exposure to these different countries thus provides us with the best of all worlds in terms of monetary policy, which is a better position to be in than only having exposure to one single nation’s policy.

Leverage

The Nuveen Preferred and Income Opportunities has the ability to utilize certain strategies that allows it to boost its yield beyond that of any of the underlying assets. This is one of the major advantages that closed-end funds have over other funds. One of these strategies is the use of leverage. Basically, the fund borrows money and uses those borrowed funds to purchase fixed-income securities. As long as the interest rate that the fund pays on the borrowed money is less than the yield on the purchased assets, this strategy works pretty well to boost the yield of the portfolio in aggregate. As the fund can borrow at institutional rates, which are significantly lower than retail rates, this will usually be the case.

However, the use of leverage is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund does not have too much leverage since that would expose us to too much risk. I do not like to see a fund’s leverage above a third of its assets for this reason. The Nuveen Preferred & Income Opportunities Fund is above this threshold and the fund’s levered assets constitute 37.43% of the portfolio. Ideally, the fund would get this ratio down a bit as this is exposing us to more risk than we really like. However, considering that the fund is invested mostly in fixed-income assets as opposed to riskier common stocks, it is probably not too bad.

Distribution Analysis

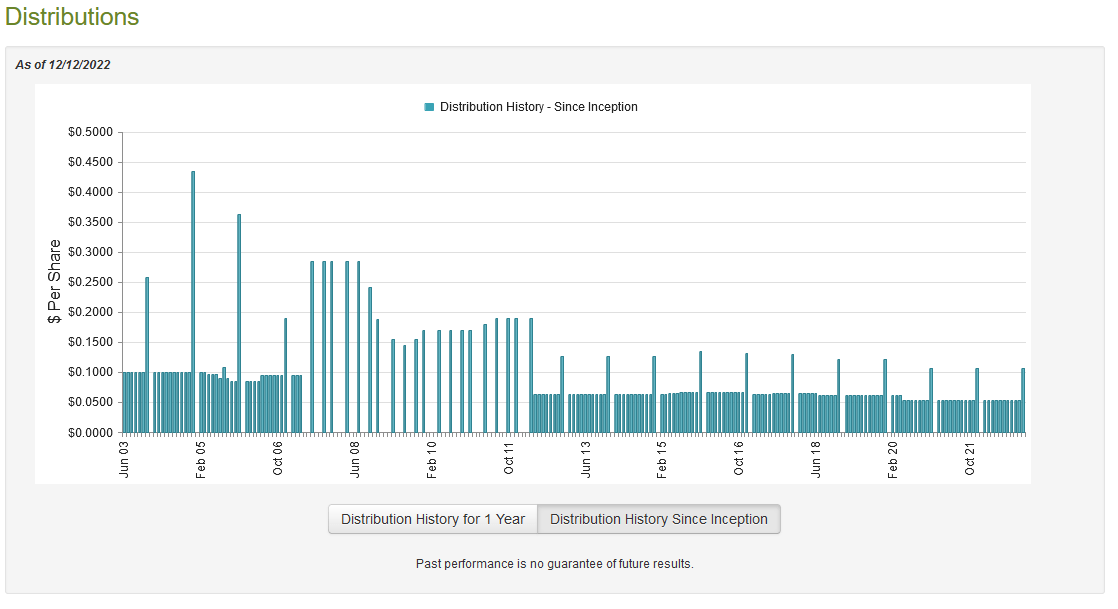

As stated earlier, the primary objective of the Nuveen Preferred & Income Opportunities Fund is to provide its investors with a high level of current income. In order to accomplish this objective, the fund maintains a leveraged portfolio of primarily high-yielding fixed-income securities. We might therefore assume that the fund has a very high distribution yield itself. This is indeed the case as it currently pays out a monthly distribution of $0.0530 per share ($0.636 per share annually), which gives the fund an 8.64% yield at the current price. The fund has unfortunately not been particularly consistent about this distribution over the years. In fact, it has varied the payout quite a bit over its history:

{kind=link}

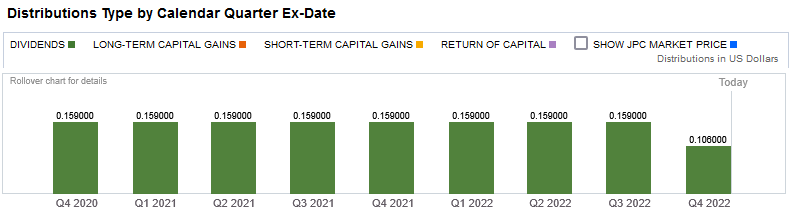

This will likely not prove particularly appealing to those investors that are looking for a stable and safe source of income with which to pay their bills. This is a category that includes most retirees. Despite the varying distribution though, this group may be somewhat comforted by the fact that this distribution consists solely of dividend income and does not include any return of capital or capital gains distributions:

{kind=link}

The reason why this may be appealing is that dividend income is by far the most sustainable way for a closed-end fund to finance the distribution. After all, a return of capital distribution can be a sign that the fund is returning the investors’ own money back to them. This is obviously not sustainable over any sort of extended period. Meanwhile, a capital gains distribution is dependent on the fund actually generating sufficient capital gains during a given period of time. This can be a difficult task to accomplish for a fixed-income fund during a period of monetary tightening. As the dividends and interest payments made by fixed-income securities do not typically vary over time, the fund’s income should be relatively stable, which allows it to sustain its dividends. However, as I have pointed out before, it is possible for these distributions to be misclassified. In addition, new securities added to the portfolio will have different yields than securities that matured or were otherwise removed from the portfolio. We therefore still want to examine the fund’s finances to determine exactly how it is financing these dividends so that we can see just how sustainable they are likely to be.

Fortunately, we do have a somewhat recent document that we can consult for this task. The fund’s most recent financial report corresponds to the full-year period ending July 31, 2022. As such, it will give us a good idea of how well the fund handled the early stages of the Federal Reserve switching from a loose monetary policy to a tight monetary policy. It is also a much newer report than we had available the last time that we looked at the fund. During the full-year period, the Nuveen Preferred & Income Opportunities Fund received a total of $22,544,081 in dividends and $66,182,397 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, the fund brought in a total of $88,801,472 over the year. The fund paid its expenses out of this amount, leaving it with $68,799,874 available to investors. This was more than sufficient to cover the $66,660,132 that the fund actually paid out in distributions over the period. Thus, the fund clearly covered its distributions solely with its net investment income in the full-year period. Overall, we have nothing to worry about here.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the Nuveen Preferred & Income Opportunities Fund, the usual way to value it is by looking at the fund’s net asset value. The net asset value of a fund is the total current value of all of the fund’s assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to buy shares of a fund when we can purchase them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund’s assets for less than they are actually worth. This is, fortunately, the case with this fund today. As of December 12, 2022 (the most recent date for which data is currently available), the fund had a net asset value of $7.98 per share but the shares actually trade for $7.41 per share. This gives the fund’s shares a discount of 7.14% to the net asset value at the current price. This is quite a bit better than the 3.54% discount that the fund’s shares have had on average over the past month. Thus, the price certainly appears to be reasonable today.

Conclusion

In conclusion, the Nuveen Preferred & Income Opportunities Fund could help investors to increase their income today. This is something that becomes ever more important due to the rising cost of living that we are currently experiencing in the nation. Unfortunately, the fund’s share price has been steadily declining over the course of this year, which is likely to continue over the next few months as interest rates continue to rise. The fund does have a lot going for it though including a well-diversified portfolio, sustainable high distribution yield, and a very nice discount to the net asset value. It may be worth considering, although dollar cost averaging is recommended to avoid taking too many unrealized losses until interest rates peak.

For further details see:

JPC: Best To Dollar Cost Average In Until Rates Peak