BACRP - JPMorgan Chase Stock: What Can We Expect From Q2 Earnings?

2023-07-10 11:20:47 ET

Summary

- JPMorgan Chase is expected to report significant revenue and profit growth for Q2, primarily driven by higher net interest income due to rising interest rates.

- The bank's stress capital buffer has declined from 4.0% to 2.9%, indicating less risk and allowing for increased capital returns, including a planned 5% dividend increase.

- Despite a premium valuation compared to peers, JPMorgan's solid dividend yield and positive operational outlook make it a solid hold, with potential upside if the industry performs well in Q2.

Article Thesis

JPMorgan Chase & Co. ( JPM ) will report second quarter earnings results on Friday, July 14. We will take a look at what can be expected from the report, and we also will look into JPM's outlook for the foreseeable future.

JPMorgan's Upcoming Earnings

JPMorgan Chase & Co. is always among the first companies in the S&P 500 to report its quarterly results, together with other major banks. On Friday, we will know how the company fared during the second quarter.

Right now, analysts are predicting that the company will report significant revenue and profit growth for the quarter, on a year-over-year basis, as we can see in the following two tables:

{kind=link}

Revenues are forecast to grow by 27% at the midpoint of the guidance range, although the range between the lowest and the highest estimate is pretty wide. Revenue growth will primarily be driven by higher net interest income, which is the most important contributor to JPM's top line. Net interest income growth, in turn, is driven by higher net interest margins - when the Fed increases interest rates, which it has been doing over the last year, banks generally pass on these rate increases faster when they lend money, relative to the money they borrow. During times of rising interest rates, many banks will thus be able to boost their net interest margins, which translates into higher net interest income, all else equal.

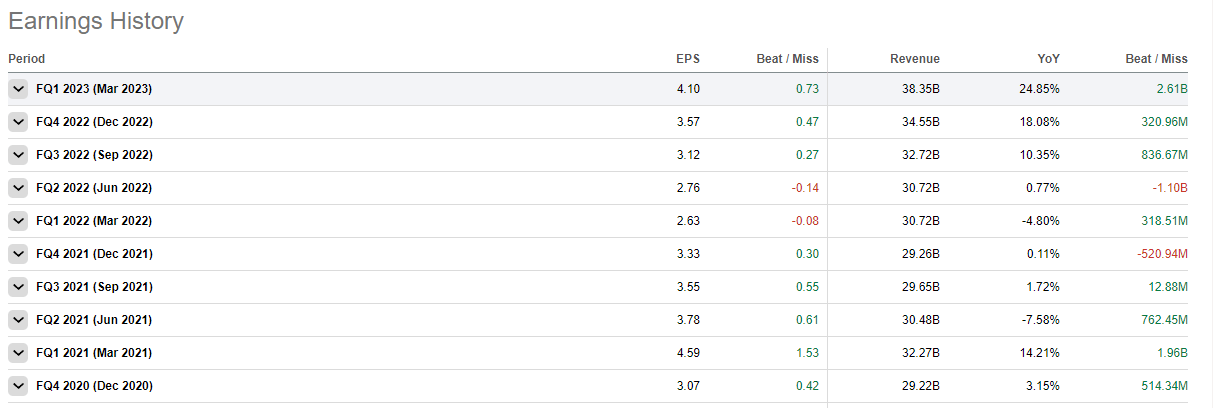

During the previous quarter, JPMorgan Chase has been able to grow its revenues by 25% primarily due to an expanding net interest margin. It would not be surprising to see the same hold true during the second quarter. Looking back at the history of JPMorgan's reported results vs. what analysts had been predicting at the time, there's a pretty clear trend of Wall Street analysts underestimating JPMorgan:

{kind=link}

Over the last ten quarters, JPMorgan has beaten the consensus revenue estimate eight times (it also beat the consensus earnings per share estimate eight times over that time frame). On average, JPMorgan has thus meaningfully outperformed expectations. This does not guarantee that the same will hold true for the second quarter earnings report, of course, but history suggests that there's a solid chance that JPMorgan will surprise to the upside.

Looking at profit estimates, a lot of growth is expected, too:

{kind=link}

Analysts are currently predicting that JPMorgan will showcase earnings per share growth of more than 35%, which would be a very strong result. That being said, it's important to note that the second quarter of 2022 wasn't especially strong - investment banking results were rather weak, for example, due to macro uncertainties caused by COVID policies in China, rising rates, and the war in Ukraine. Showing strong growth from this somewhat weaker base is easier than growing at a similar pace from a very strong level in the previous year. Investment banking results will likely still not be overly strong, but the boost that JPMorgan will see revenue wise from higher net interest income should have a profound positive impact on the company's profits. The fact that earnings per share are forecasted to grow faster than revenues can be attributed to the positive margin impact from operating leverage and fixed cost digression that JPMorgan should experience thanks to its compelling top-line growth.

Overall, we can thus summarize that JPMorgan will most likely show a strong recovery from the somewhat weaker results seen a year ago. Rising interest rates are a major tailwind for JPM and its peers, and profits are about to benefit from that. That being said, due to not very strong investment banking results, profits will likely remain below the peak levels seen in the first quarter of 2021, when JPM earned slightly more than $4 per share.

Fed's CCAR Results And Capital Returns

June always is an important month for major banks as the Fed releases its Comprehensive Capital Analysis and Review ('CCAR') results. These impact what capital levels are required at specific banks, and thus have an impact on banks' capital return policies over the coming quarters.

Toward the end of June, JPMorgan showed how it fared in this year's CCAR review. The bank has seen its stress capital buffer decline from 4.0% to 2.9%, which made its Common Equity Tier 1 ratio drop by a similar 110 base points - from 12.5% to 11.4%. This is good news - in the eyes of the Fed, the bank has become less risky and does not need to hold as much equity capital to balance out these risks, all else equal. At the end of the first quarter, JPMorgan's CET1 ratio stood at 13.8%. That's well above the 12.5% needed at the time, and way above the 11.4% needed now. JPMorgan thus could reduce its equity capital meaningfully going forward, e.g. by paying out more capital to its owners.

And, indeed, JPMorgan announced plans to ramp up its capital returns following the release of its CCAR results. The bank plans a dividend increase of 5%, which will bring its dividend to $1.05 per share per quarter, or $4.20 per share per year. Relative to a current share price of $144, that makes for a dividend yield of 2.9%. That is pretty attractive relative to the meager ~1.5% dividend yield that is available from the broad market (S&P 500), but on the other hand, JPMorgan has been trading with a substantially higher dividend yield not too long ago - in spring, when markets were worried about banks, JPM traded in the mid-$120s for some time, where its dividend yield was north of 3%, even before accounting for the expected dividend increase. While the dividend increase is good for shareholders, it does not mean that JPM is now a great income buy solely due to the dividend being increased by 5% -- JPM was a better income investment earlier this year when its shares were cheaper and when it was trading with a higher implied dividend yield.

JPMorgan does not only plan to increase its dividend, it also plans to buy back shares going forward. That has been the case in the past as well, although buybacks were temporarily paused during the midst of the pandemic. The buyback pace will likely not be dramatic, but over time, these buybacks will add meaningfully to JPM's earnings per share growth, which, in turn, influences the value of each share. Buybacks also make the dividend safer, all else equal, as paying a specific amount of dollars per share is less costly on a company-wide basis when the share count keeps declining.

JPM: What's The Outlook?

JPMorgan is about to report compelling quarterly results, and I believe that there's a good chance that the remainder of the year will be positive for the company as well, at least on an operational basis. The tailwinds for its revenues and profits from rising interest rates and expanding net interest margins should persist, and buybacks will positively impact its earnings per share growth on top of that.

A potential recession is a risk factor, as it likely would go hand in hand with higher provisions for credit losses, which would put a temporary dent in JPM's profitability. That being said, it does not look like there will be a severe recession - employment is strong, and experts seem split between "no recession" and "minor recession." A Great Recession 2 seems unlikely, I believe, thus risks aren't dramatically high for JPMorgan.

Shares are currently trading for almost exactly 10x this year's expected net profit. That's far from expensive in absolute terms, but it's worth noting that many other major banks are less expensive, including Bank of America ( BAC ), Citigroup ( C ), and Wells Fargo ( WFC ), which trade at 8x, 8x, and 9x this year's profits, respectively. One can argue that JPM deserves a premium valuation due to its impressive size and strong history, but it does not seem very likely to me that this valuation premium will expand a lot, thus relative upside potential seems limited. It is, of course, possible that the whole industry gets bid up when the major banks report strong results for their respective second quarters - in that case, JPM has upside potential, of course. With its solid dividend yield and a good operational outlook, but also a premium valuation vs. peers, JPM looks like a solid hold to me right here.

For further details see:

JPMorgan Chase Stock: What Can We Expect From Q2 Earnings?