JMIA - Jumia: Cutting Costs Won't Be Enough

2023-08-29 11:42:51 ET

Summary

- Jumia faces challenges due to high inflation and a restricted supply of goods, impacting consumer spending on its platform.

- Jumia is also pulling away from activities with questionable economics, negatively impacting growth.

- While Jumia's profitability has improved on the back of cost-cutting measures, a return to steady consumer growth is necessary for long-term success.

Jumia (JMIA) continues to face a difficult operating environment due to high inflation and a restricted supply of goods. This macro environment is reportedly impacting usage performance , although Jumia's inability to drive adoption does raise questions.

Jumia believes it has now right-sized its cost-base and as a result is turning its focus towards capitalizing on the large opportunity ahead of it. This will be critical for Jumia's future as the company cannot just cost cut its way to profitability. More efficient operations are required, and this will likely require significant supply chain investments.

Market

The average inflation rate across the countries Jumia operates in was 14.1% in June 2023 , with particularly high rates of inflation in Egypt, Ghana and Nigeria. The ability of sellers to source goods has also been impacted by restrictions on imports in many countries. These factors are undermining consumer spending on Jumia's platform, a problem that is being exacerbated by the company's category rationalization.

JumiaPay

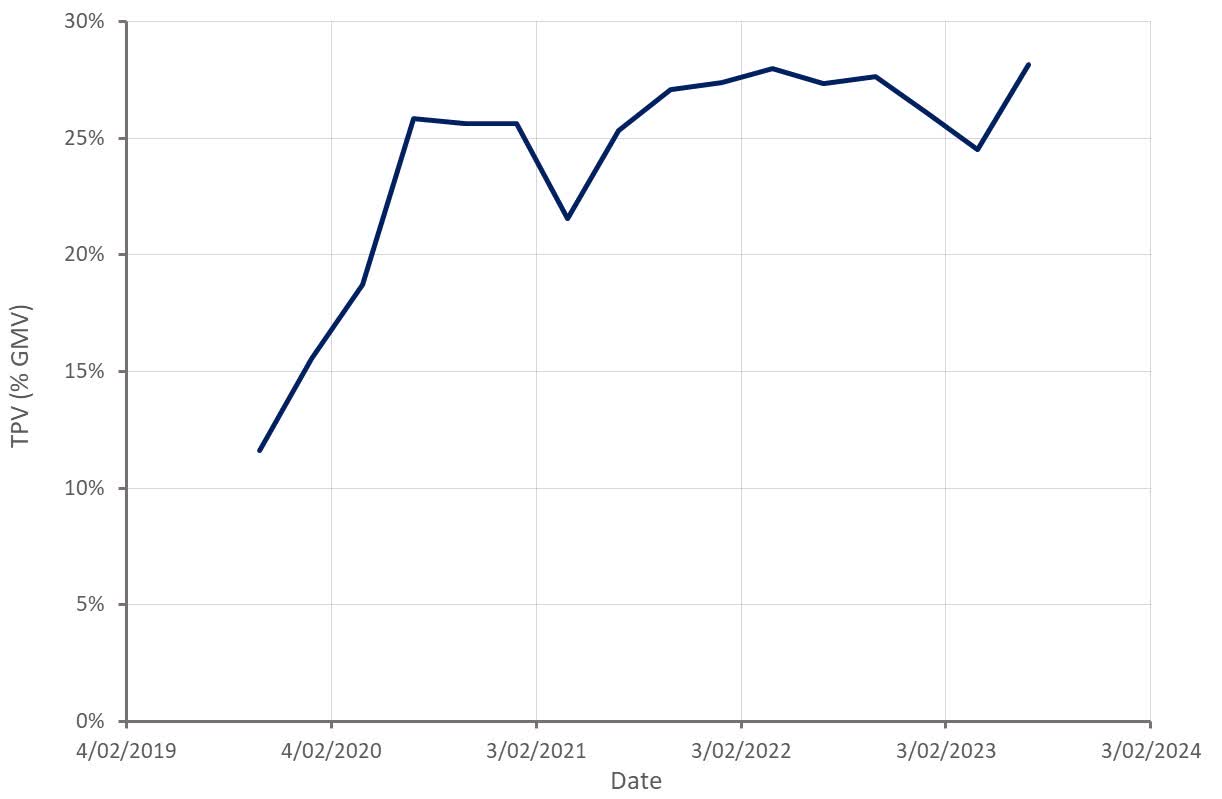

Similar to Jumia's ecommerce business, JumiaPay's growth has been poor as the company has been pulling back on uneconomic activities. For example, Jumia has suspended a number of services that were historically promotionally intensive. While TPV (Total Payment Value) was down around 23% YoY in the second quarter, TPV as a percentage of GMV (Gross Merchandise Value) has been fairly stable.

Table 1: TPV as a Percentage of GMV (source: Created by author using data from Jumia) Figure 1: JumiaPay TPV (source: Created by author using data from Jumia)

{kind=link}

Jumia remains a believer in this business though, and is introducing a number of new products which should support growth. Jumia is in the process of expanding the range of payment methods that can be linked to a JumiaPay account, which the company hopes will support adoption. Jumia is also developing a Buy-Now-Pay-Later solution to support purchases on its platform. In addition, Jumia wants to extend JumiaPay off-platform, processing payments on behalf of third-party merchants starting in countries where it has the relevant licenses (Nigeria and Egypt). Jumia is also introducing JumiaPay on-delivery, which will allow customers to pay digitally upon delivery of their order, through either a payment link or QR code.

Financial Analysis

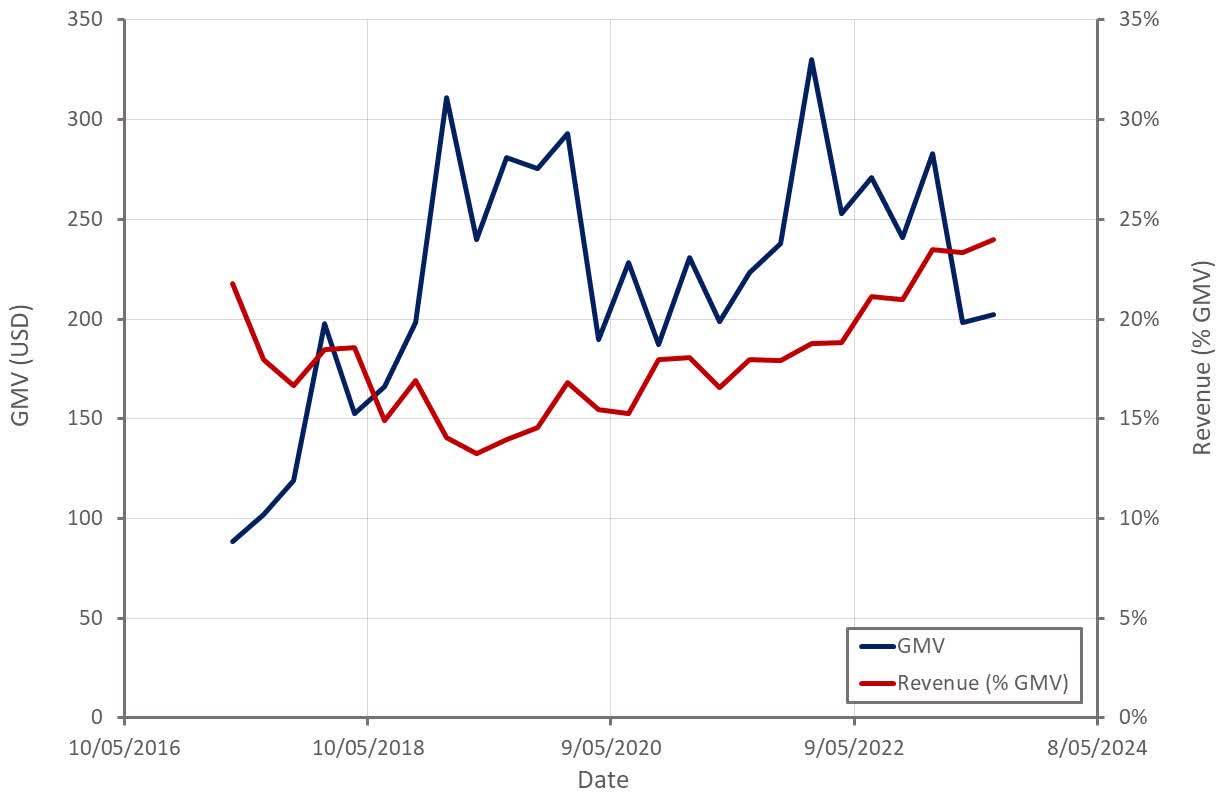

Jumia continues to move away from unprofitable categories like its first party grocery offering, which along with a rationalization of JumiaPay app services is pressuring GMV and revenue. JumiaPay app services, combined with the FMCG category, accounted for 45% of the decline of items sold and 32% of GMV decrease during the second quarter. Foreign exchange effects contributed 14 percentage points to the 25% YoY GMV decline.

Figure 2: Jumia GMV (source: Created by author using data from Jumia)

{kind=link}

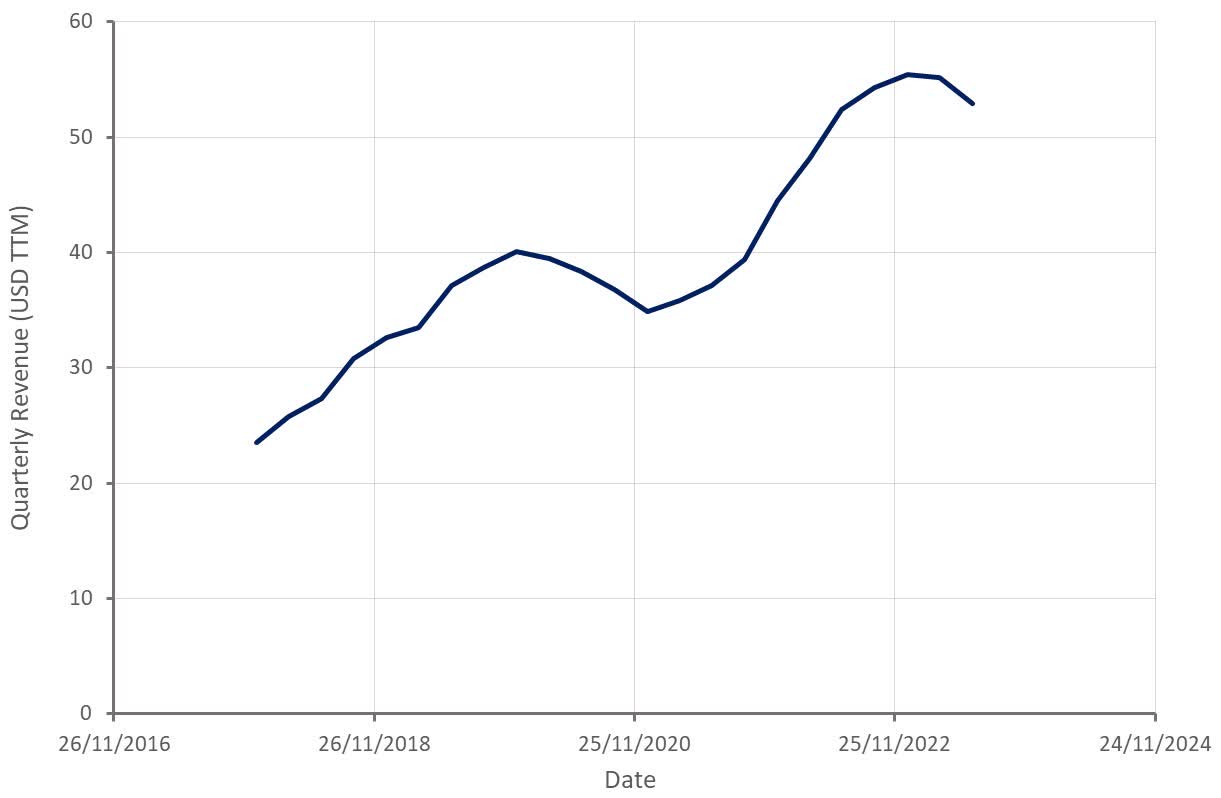

While the decline in revenue may look concerning, it is improving Jumia's profitability and was probably a necessary move. At some point, Jumia will need to return to growth in order to maintain the stock's narrative and drive economies of scale.

Figure 3: Jumia Revenue (source: Created by author using data from Jumia)

{kind=link}

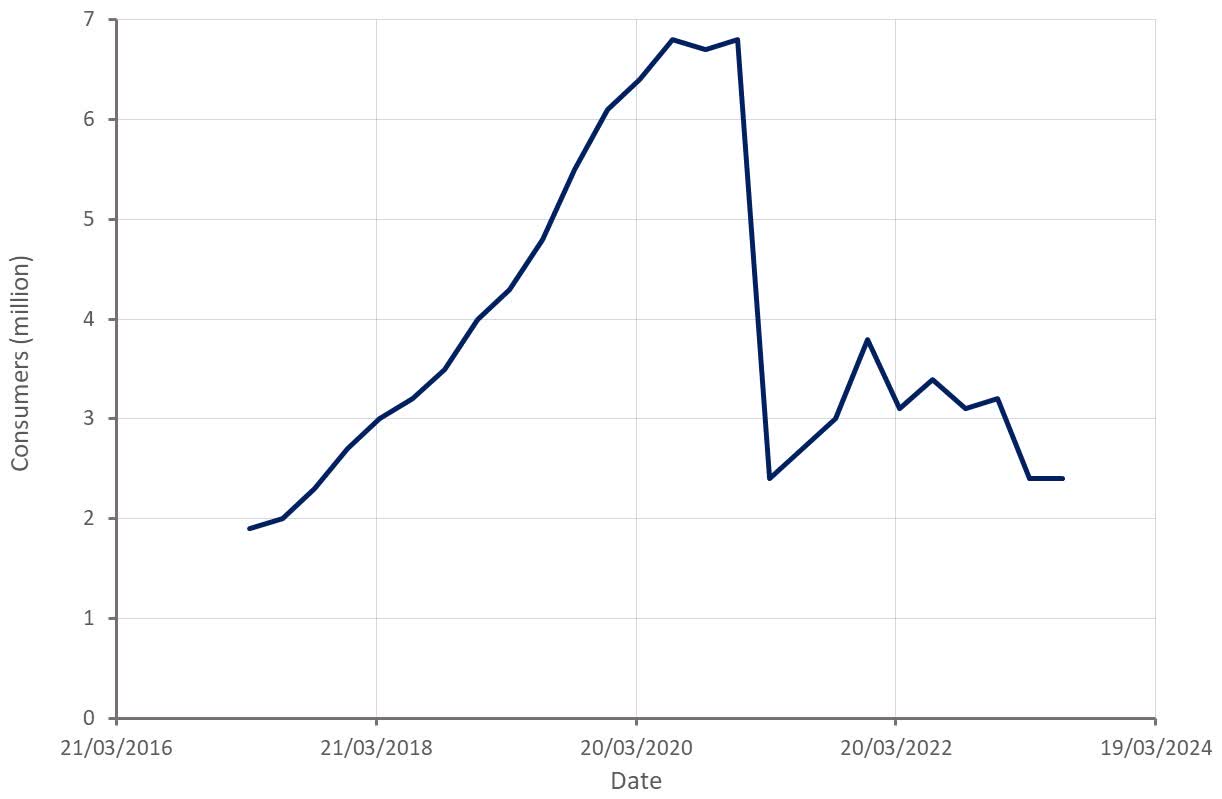

More concerning for Jumia is the relatively poor adoption of its platform. Jumia has been operating for over a decade and yet it still only has around 2.4 million active consumers. The countries in which Jumia operates have a total population of around 600 million, indicating very low penetration. While some of this can be explained by the fact that Jumia has been pulling back from unprofitable geographies and categories, Jumia will soon need to return to steady consumer growth.

Ecommerce in Africa is a difficult business though, as the markets are highly fragmented and have underdeveloped logistics and digital payments capabilities. Many regions do not have an organized address system, making deliveries inefficient and reliant on local expertise. The growth and profitability of ecommerce in Africa will likely be largely limited by development of infrastructure, logistics and digital payments capabilities. In addition, many countries have high import tariffs and there is limited ability to source products locally, increasing the cost of ecommerce.

Figure 4: Jumia Active Consumers (source: Created by author using data from Jumia)

{kind=link}

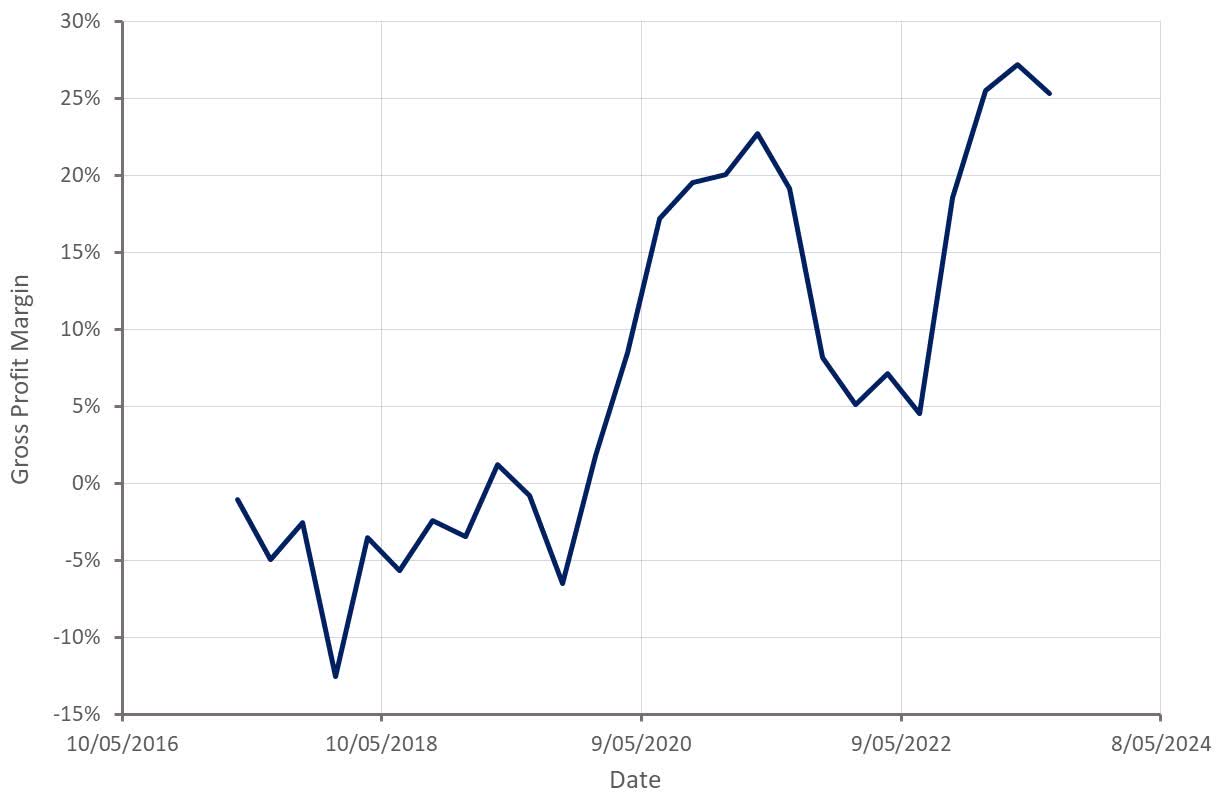

Jumia's gross profit margins have increased significantly over the past 12 months, with a large portion of this improvement likely coming from the shift away from uneconomic categories. While margin improvements have stalled in recent quarters, revenue mix shift, pricing and improved efficiency could still drive gross profit margins higher.

Figure 5: Jumia Adjusted Gross Profit Margin (source: Created by author using data from Jumia)

{kind=link}

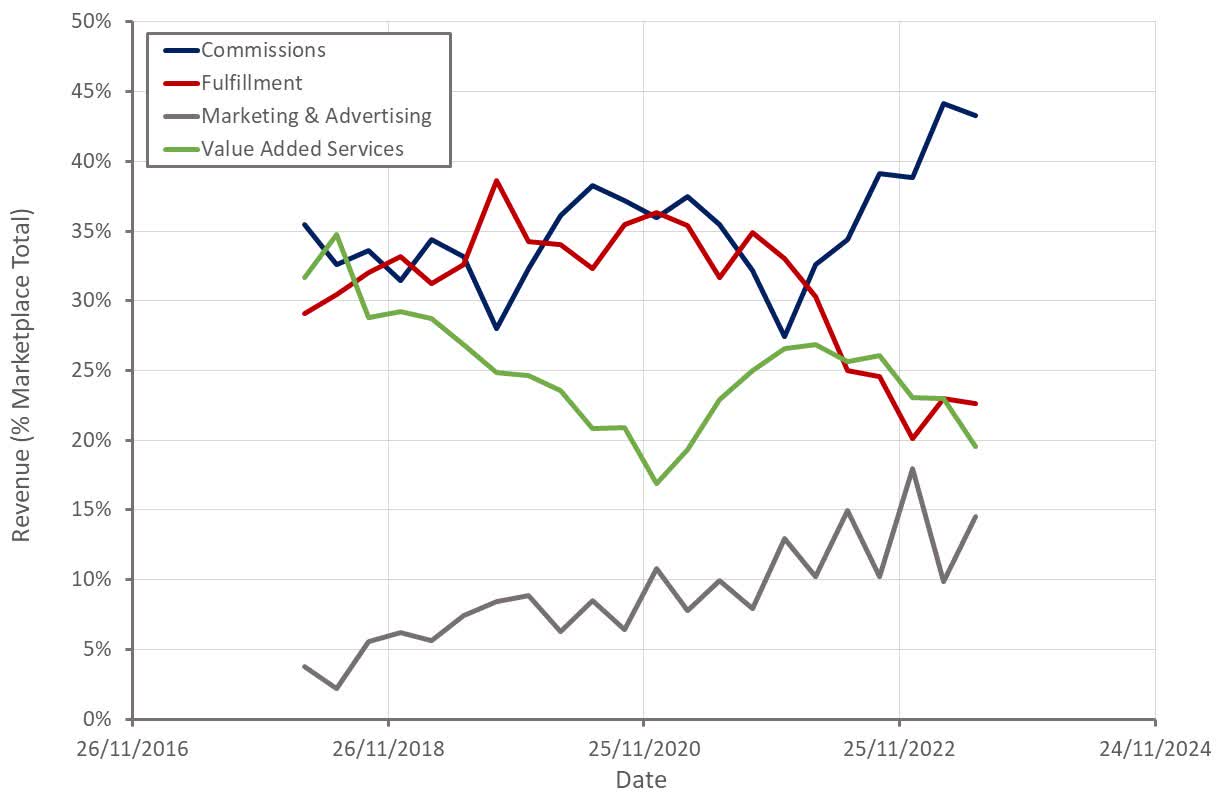

Jumia's margins have likely been greatly aided by the move away from value-added services revenue (mainly logistics revenue from sellers) and fulfillment revenue. Jumia is also improving the monetization of its logistics services and the pass-through of fulfillment costs. The ratio of the sum of fulfillment and value-added services revenue over fulfillment expense increased from 56% to 80% over the past year.

Figure 6: Jumia Revenue Breakdown (source: Created by author using data from Jumia)

{kind=link}

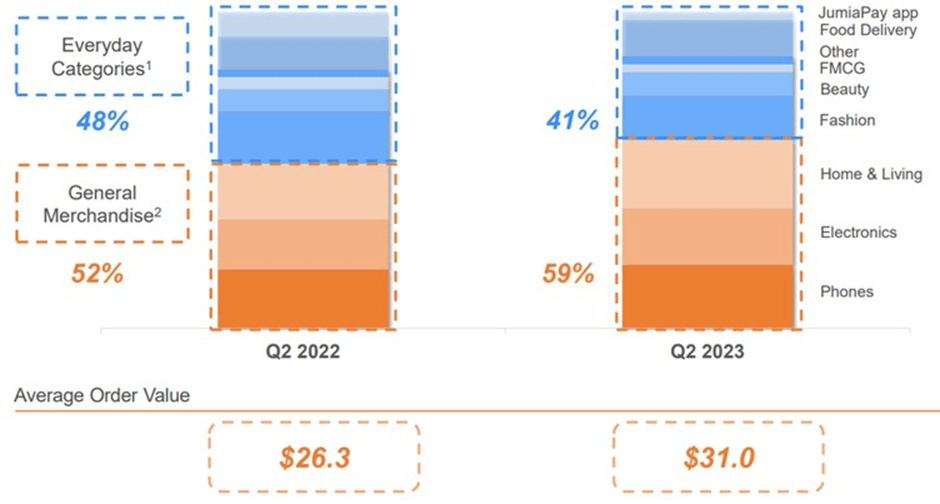

Jumia's Average Order Value increased 18% YoY , reflecting the shift in GMV category mix. In particular, the General Merchandise category, which has an average item value of 42 USD, is increasing in importance. Jumia's focus is now on phones, electronics, home and living, and fashion and beauty. Higher value items should generally lower the burden of fulfillment costs.

Figure 7: Jumia GMV Breakdown (source: Created by author using data from Jumia)

{kind=link}

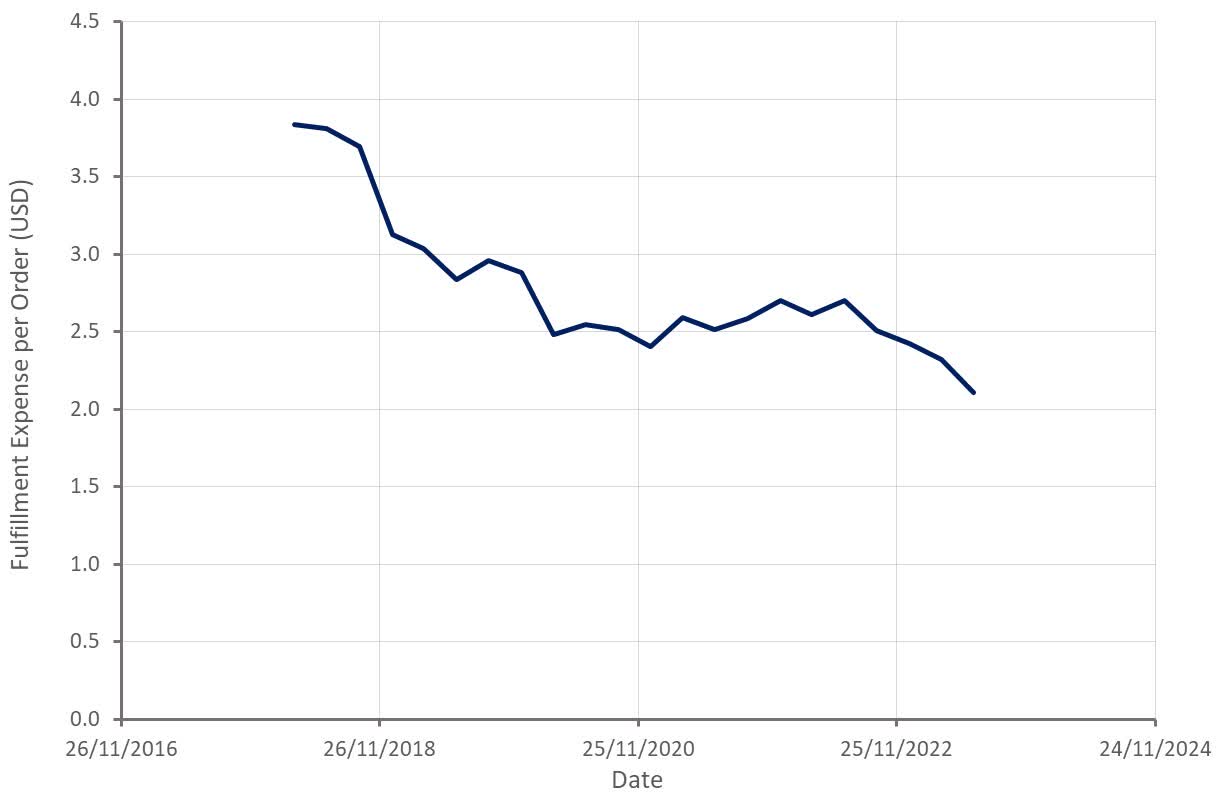

In addition to a favorable shift in revenue mix, Jumia is also trying to drive efficiency improvements across its logistics operations. This includes increasing the use of pick-up stations, which increased from 33% of shipped physical goods orders in Q2 2022 to 42% in the second quarter of 2023.

Jumia is also trying to optimize its footprint and logistics routes, improve warehousing staff productivity and reduce packaging costs. In addition, Jumia wants to tap into the large pool of consumers located outside of major cities, which is generally underserved by retail.

Jumia is pursuing an asset light business model, and hence its logistics and pick-up station network leverages third-party partners. While this is probably necessary given the size of Jumia's footprint and its limited access to capital, it's not clear that Jumia has any competitive advantage as a result. Particularly in light of Jumia's small user base.

Figure 8: Jumia Fulfillment Expense per Order (source: Created by author using data from Jumia)

{kind=link}

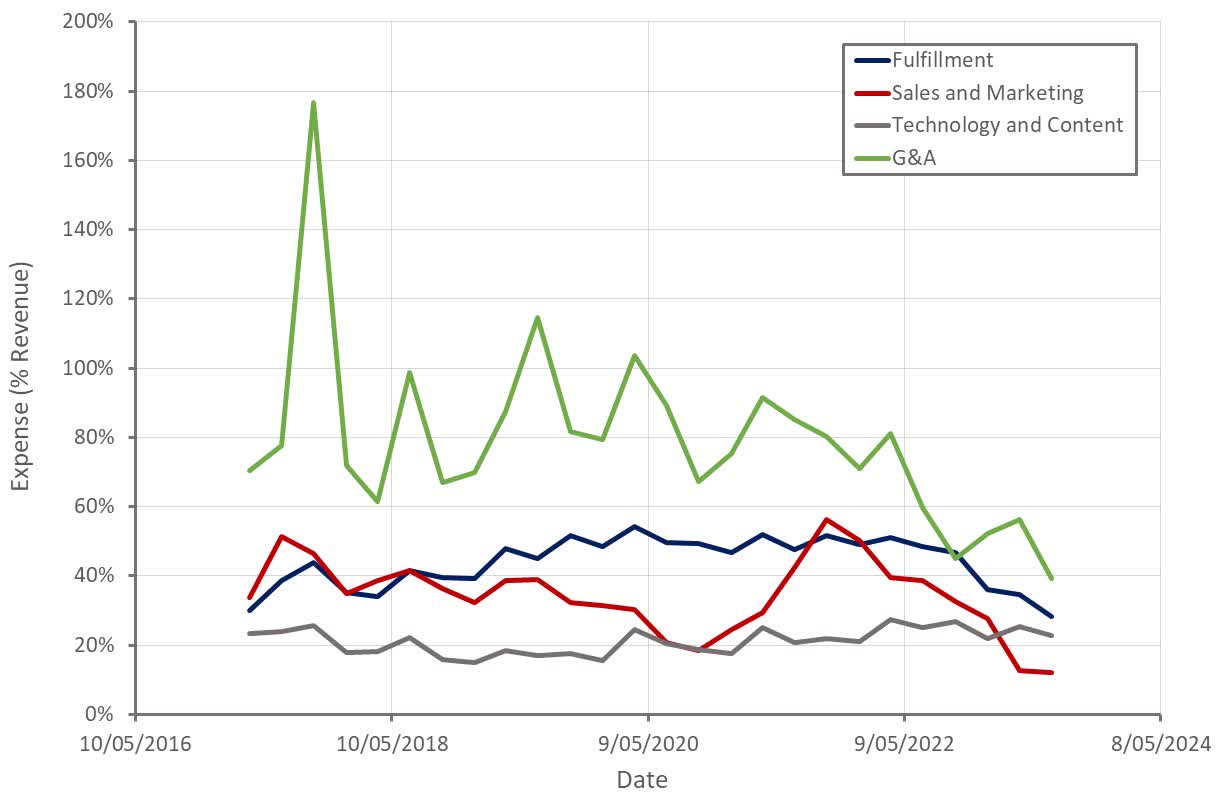

Jumia is also reducing the burden of operating costs, despite a decline in revenue. While Jumia can likely still reduce general and administrative expenses significantly, some of Jumia's other expenses probably don't have much room for further improvement.

Figure 9: Jumia Expenses (source: Created by author using data from Jumia)

{kind=link}

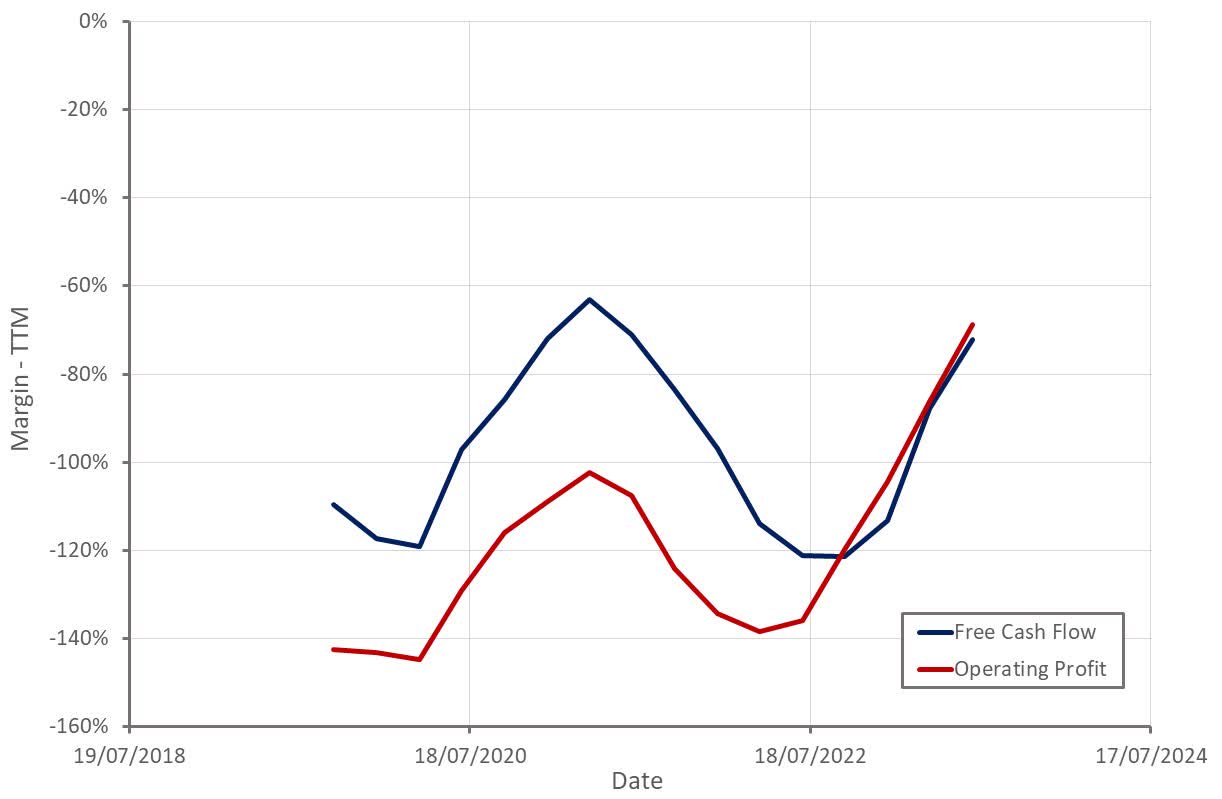

Jumia is still a long way away from breakeven, and it is not clear how much more room they have to cut costs. It appears likely that Jumia will still need to grow the business significantly to improve profitability. The question is whether Jumia has the resources to do this and whether margins can continue to improve when the business returns to expansion.

Jumia has roughly 61 million USD of cash and cash equivalents and 105 million USD of term deposits and other financial assets.

Figure 10: Jumia Operating Profit and Free Cash Flow Margin (source: Created by author using data from Jumia)

{kind=link}

Conclusion

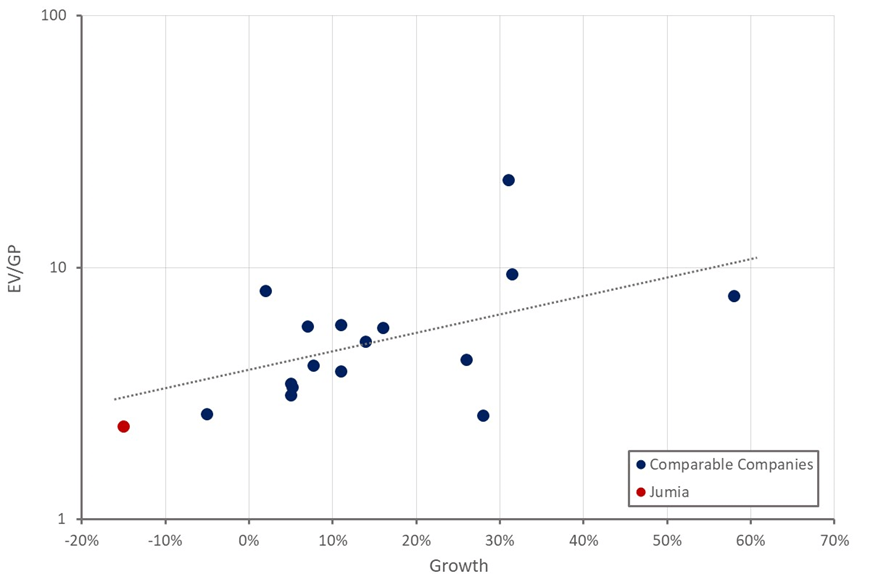

Given the long-term potential of a pan-African ecommerce platform, Jumia could be considered deeply undervalued. This must be weighed against the fact that the company is yet to demonstrate it has a viable business model, despite a relatively long operating history. It is also not really clear what Jumia has gained from its cumulative losses. Its user base is still relatively small and Jumia has elected not to build out its own logistics network.

Jumia has taken a step in the right direction by moving away from uneconomic activities and focusing on efficiency, but the company still needs scale to achieve profitability.

Figure 11: Jumia Relative Valuation (source: Created by author using data from Seeking Alpha)

{kind=link}

For further details see:

Jumia: Cutting Costs Won't Be Enough