JMIA - Jumia: Questions Around Turnaround Linger Runway May Only Last Several More Quarters

Summary

- Jumia is Africa's largest e-commerce company generating $1 billion in GMV (gross merchandise value).

- The company generated an operating loss of $227 million in 2022 and is now left with $228 million in cash & term deposits.

- Given the low market capitalization of around $350 million, another equity offering to fund its journey looks currently unlikely.

- The company is therefore planning drastic cost cuts, but we have doubts about the feasibility of the plan. Macro headwinds complicate the situation further.

- We rate the company a Strong Sell as long as macro conditions do not improve and the company does not show further tangible cost reduction results.

The Thesis

Jumia Technologies AG (JMIA) has made an operating loss of $227 million last year and is now left with only $228 million in cash & cash equivalents. In light of Africa's economic headwinds, we have questions around the feasibility of the new management's cost cutting program and deem the risk-reward ratio as unfavorable because of a real threat of running out of cash by 2024.

About Jumia

Jumia Technologies AG is an African e-commerce company operating in 11 markets across the whole continent. The company offers e-commerce services through a marketplace and first party sales, food delivery, logistics services as well as payment services through its fintech JumiaPay. The company is a generalist selling everything from small value categories such as groceries to big ticket items including appliances. The company generated around $1 billion in Gross Merchandise Value in 2022 and has around 8 million customers annually.

Jumia is a former offspring of Rocket Internet, a serial start-up building company, and was co-founded by the two ex-McKinsey consultants who until recently led the company. Jumia got listed on the NYSE in 2019 and counted big names such as Mastercard ( MA ) among its investors (we couldn't find evidence during our research that Mastercard still holds stock in Jumia). It was long hailed as Africa's Amazon and Citron even labeled it as a generational investment opportunity.

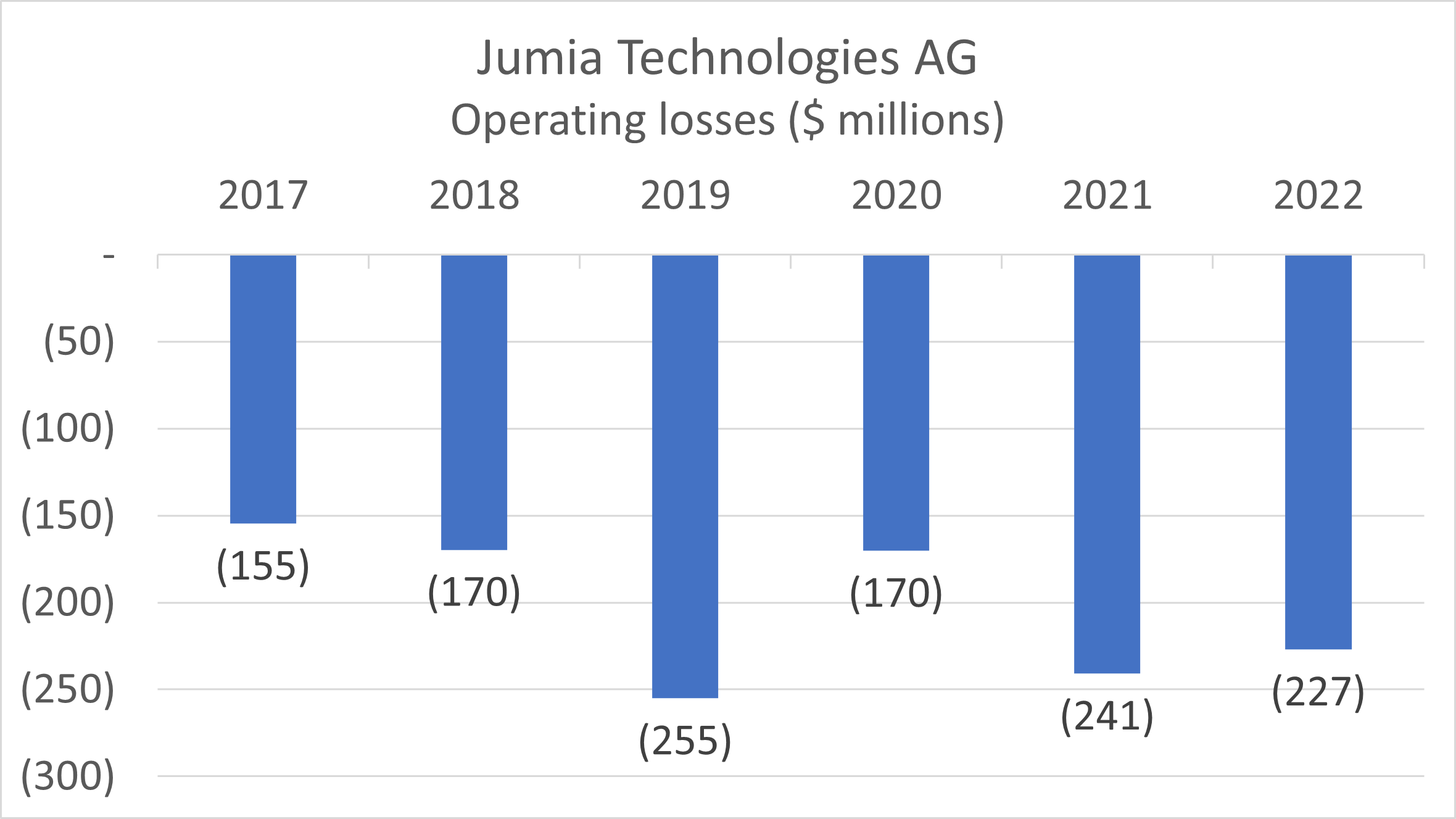

Jumia has been constantly loss-making and generated aggregate operating losses of around $1.2 billion since 2017. Since its founding, it burned through more than $1 billion in investor money.

Jumia Technologies AG annual operating losses (Jumia Technologies AG financial reports)

{kind=link}

The company's share price chart looks like a rollercoaster - the stock lost 75% of its value since the IPO and more than 90% since its Covid-peak.

The never-ending losses have led to a shake-up and the removal of Jumia's founders & co-CEOs in November 2022 . Francis Dufay, an internal nomination, has been appointed as acting-CEO (now confirmed to lead the company as CEO henceforth).

The company recently announced a full year operating loss of $227 million. With its cash reserves dwindling to $228 million and another equity round highly unlikely, Dufay is forced to embark on a severe cost cutting exercise. Investors may therefore justifiably ask how much time the company has left.

What is Jumia's remaining runway?

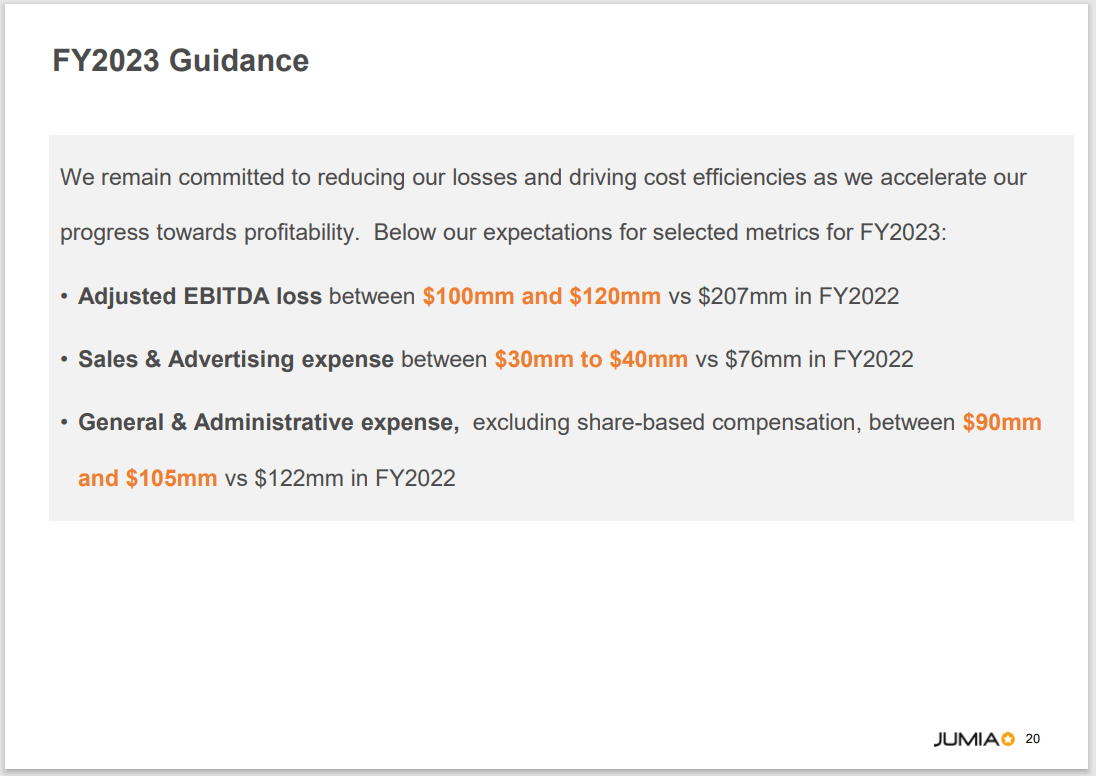

The company targets significant cost savings for 2023 but expects to lose another $100-120 million on adjusted EBITDA basis for the full year. In particular, management plans to save $50 to $80 million in SG&A alone. The company provided the following guidance in its latest earnings release and earnings call :

- No significant changes in gross profit margins planned going forward (GP margin was around 13% of GMV in Q4 2022)

- Marketing & advertising costs to reach $30-40 million vs. $76 million in 2022

- G&A to drop to $90-105 million vs. $122 million in 2022

- No specific guidance on Tech & content costs and Fulfillment costs

Jumia guidance for 2023 (Jumia Technologies AG investor relations)

{kind=link}

Jumia's guidance leaves us with some blank spots and question marks in particular with regards to expected GMV growth throughout 2023 and the two key cost buckets 'Fulfillment expenses' and 'Tech & content costs' as well as the phasing of the cost savings and the expected annualized cash burn in Q4.

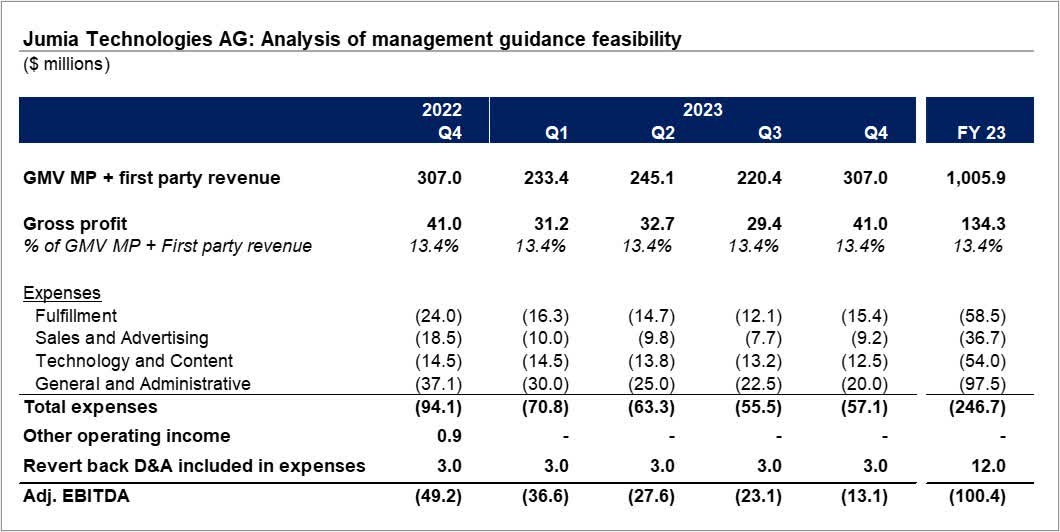

GMV Growth

Our model assumes in 2023 a GMV drop of 10%, driven by a combination of unfavorable macro factors in Africa and Jumia scaling back some of its services and product categories. We further assume stable gross profit margins of 13.4% in 2023, as per management's expectations.

Sales and advertising

Management aims to reduce Sales and advertising costs to $30-40 million (~3-4% of GMV on a full-year basis). We therefore assume a drop from 6% of GMV in Q4 2022 to 3% of GMV by Q4 2023, leading to full-year S&A expenses of $37 million.

G&A

Management further aims to land full year G&A costs at around $100 million, but does not provide further details on phasing. We therefore plan in our model a successive decrease of quarterly costs from $37 million in Q4 2022 to $20 million by Q4 2023. This represents a drop of 46% on a y-o-y basis, which is massive. Such a trajectory would result in full year costs of $98 million, in line with guidance.

Other cost buckets

Adjusted EBITDA would hit the targeted loss of $100 under the following assumptions:

- A decline in quarterly tech & content costs from $14.5 million to $12.5 million

- A decline of fulfilment costs from 7.8% of GMV to 5.0% by Q4 2023

Jumia FY23 quarterly estimates (Author's estimates)

{kind=link}

If everything goes according to plan, according to our estimates Jumia's implicit plan is to end up with a quarterly cash burn in the range of $10-15 million by the end of 2023. With a projected $100 to 120 million left in liquid assets, this would give Jumia a runway of at least another 6 quarters before having to tap into equity markets or others sorts of funding in 2025. Et voilà , problem solved... Or not?

Our concerns

While the EBITDA-level guidance adds up under these assumptions, we have serious doubts about the feasibility and 'doability' of the plan. The guidance does not provide enough details and feels to us more like wishful thinking and reverse-engineering the numbers for the capital markets audience, rather than a bottom-up calculation. These are our particular concerns:

2023 fulfillment costs, Jumia's second biggest cost bucket, has been unaddressed. What worries us in particular is the drop of only 6% in fulfillment costs on a constant-currency-basis in Q4 2022 - considering that orders declined by 12%, it looks like Jumia's fulfillment costs per order actually went up in constant currency terms . However, in order to hit the full year guidance, Jumia heavily relies on a decrease of fulfillment costs by around 1/3, according to our estimates. Given the assumed 10% drop in GMV, costs per order would have to drop by 20% for the equation to balance. Secondly, as per Dufay's earnings call remark, Jumia wants to expand outside of big cities, which is likely going to increase average fulfillment costs per order due to the abysmal African infrastructure and high logistics costs for overground transport. We are scratching our heads as to how Jumia wants to achieve costs savings given all the information.

Sales and marketing costs need to drop to around 3% of GMV by Q4 2023, which implies cutting those costs to 1/2 compared to Q4 2022, after it already declined from 9% of GMV in Q4 2021. The company would be effectively cutting S&A costs by 2/3 over a span of 2 years. While this cost category is fully under management's control, we have worries about the potential negative impact on GMV, given the high reliance of growing e-commerce companies on performance traffic and acquisition of new customers. The company is already facing significant macro headwinds while also shrinking its service offering, so reducing marketing spend may form another drag on customer acquisition and thus GMV growth and gross profits despite's managements assurances that hitherto marketing efforts were to a degree wasteful.

G&A costs is also a big worry for us. Jumia already laid off around 20% of employees in Q4, but wants to cut further. According to our estimates, total layoffs need to be in the range of 1/3 to 1/2 of all employees in order to achieve the 2023 guidance. While certainly doable, we have doubts about the potential business disruptions this may entail. Rocket Internet companies are known for underinvesting in technologies in order to quickly scale businesses up, so our fear is that with significant layoffs, the company may lack the people to keep its business humming & running soundly.

GMV decline and Gross profit volume may turn out worse than anticipated. Africa faces serious macroeconomic headwinds and Jumia may experience a bigger full-year GMV decline than our model assumption of 10%. Q4 results were not encouraging with active consumers down 15%, orders down 12% and Q4 down 14%. Some African markets suffer from high inflation ( 54% in Ghana ), others have introduced import controls (e.g. Egypt ) or are suffering of a currency crisis (e.g. Nigeria ). Pressure on GMV is further compounded by discontinuation of several services and product categories by Jumia.

Conclusion

Jumia is for us a clear Sell. We lack confidence in management because it has not painted a detailed enough picture on its cost cutting plan. We also have questions around the feasibility of its plan. If things do not go fully according to plan and Jumia instead ends up in Q4 2023 with a quarterly cash burn of $30-40 million, it would be left with a runway of around 2-3 quarters, give or take. And even if things do not go awry, the company will still be making substantial losses as it targets a -10% adjusted EBITDA margin (% of GMV) in 2023. The company will thus require another huge step-change effort to move to profitability. To 'add insult to injury', we consider persisting macro headwinds in Africa - a significant risk - impossible to assess going forward.

This is too much risk for us to take. The market doesn't have much confidence either: Jumia's current market capitalization is with $~350 million only $~120 million higher than its cash balance.

Even if skies cleared up a bit by the end of 2023, we think that a loss-making marketplace with a stagnant/declining GMV would get valued at a GMV multiple 0.3-0.5x, translating to a Jumia Enterprise Value of $300-500 million and Market cap of around $400-600 million (between c. 0% to 60% above today's market capitalization). However, the potential downside is total wipeout of investors. We don't like this risk reward ratio, which is still tilted too much towards risk.

One outlandish, speculative scenario we could imagine is a takeover of Jumia by a global player. Once the dust of the recent layoffs settles, some white knight like Alibaba ( BABA ), JD.com ( JD ) or Amazon ( AMZN ) may declare interest in acquiring Jumia. After all, despite its unattractive financial profile, Jumia is the e-commerce leader in Africa and an acquisition would grant the acquirer quick access to swaths of African consumers and operational teams on the ground to build on. Both companies have experience with foreign takeovers: Amazon acquired Souq, a marketplace player in the Middle East, in 2017 and Alibaba acquired Lazada, a marketplace player in Southeast Asia, in 2016. Needless to say, betting on a takeover would be highly speculative.

We therefore rate Jumia a Strong Sell and recommend staying away until there is more evidence of a successful implementation of the turnaround measures and Africa's macro-environment calms down.

For further details see:

Jumia: Questions Around Turnaround Linger, Runway May Only Last Several More Quarters