JMIA - Jumia Technologies: I See Several Red Flags

2023-08-16 08:56:09 ET

Summary

- Jumia is a pan-African e-commerce platform operating in 11 African countries.

- Last quarter's earnings were very weak, with crucial revenue-driving metrics falling by more than a quarter each.

- The stock is overvalued based on my valuation analysis.

Investment thesis

Yesterday, Jumia Technologies (JMIA) released its Q2 earnings , which were disappointing. This resulted in a massive intraday sell-off with a 16% stock price decline. As a growth e-commerce company operating in a promising African continent, many investors might be tempted to buy the dip here. But my fundamental analysis suggests several red flags, and I have many doubts that this business is sustainable. Cutting marketing expenses to almost zero looks very strange to me as well. To sum up, I assign JMIA a "Strong Sell" rating.

Company information

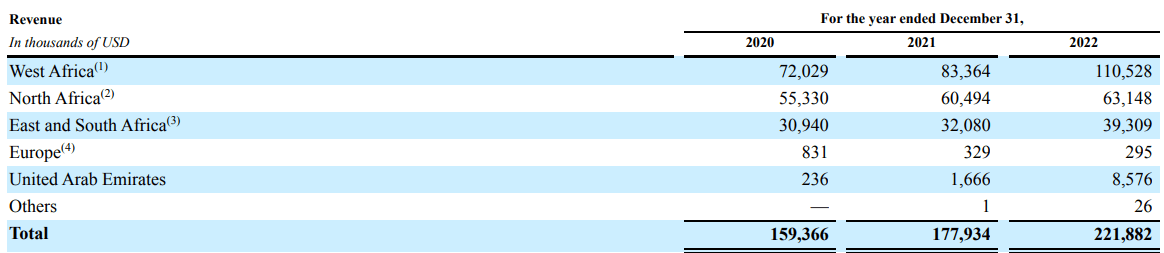

Jumia is a leading pan-African e-commerce platform. The platform consists of the marketplace, which connects sellers with consumers, Jumia Logistics, and JumiaPay. The marketplace covers 11 African countries, which account for approximately 70% of Africa's GDP.

The company's fiscal year ends on December 31 with a sole operating and reportable segment. According to the latest annual SEC filing, the company generates half of its revenue in West Africa.

JMIA's latest annual SEC filing

{kind=link}

Financials

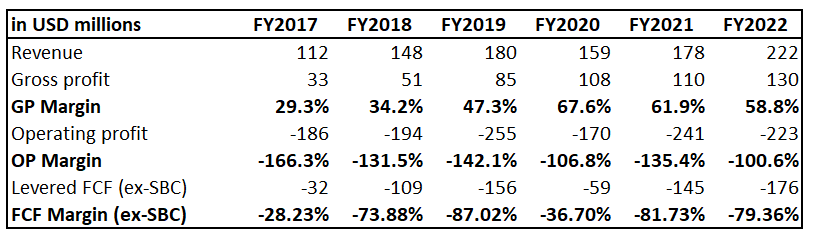

Since 2017, Jumia's revenue compounded at an impressive 14.7% CAGR. The gross and operating margins improved notably while revenue compounded at double digits. But the operating loss equaled total revenue in FY 2022, meaning that the operating margin equaled about -100%. The free cash flow [FCF] margin ex-stock-based compensation is also far from positive.

{kind=link}

The company's rapid cash burn rate looks like a notable red flag. As of June 30, 2023, the company had a $166 million liquidity position, and cash utilization for Q2 was $38 million. If the same cash burn rate remains, the company has sufficient liquidity to operate over the next four quarters. After it, they will need to raise additional finance, whether by issuing new debt or new shares, but both options are unfavorable for equity investors. During the latest earnings call , the management upgraded its EBITDA loss guidance for the full FY 2023. The EBITDA loss guidance was improved from -$110 to -$95 at the midpoint of the given ranges. While this is generally a positive sign, the improved guidance means, on average, about a $4 million improvement for the quarterly cash burn, which does not cancel the high probability of running out of cash in summer 2024.

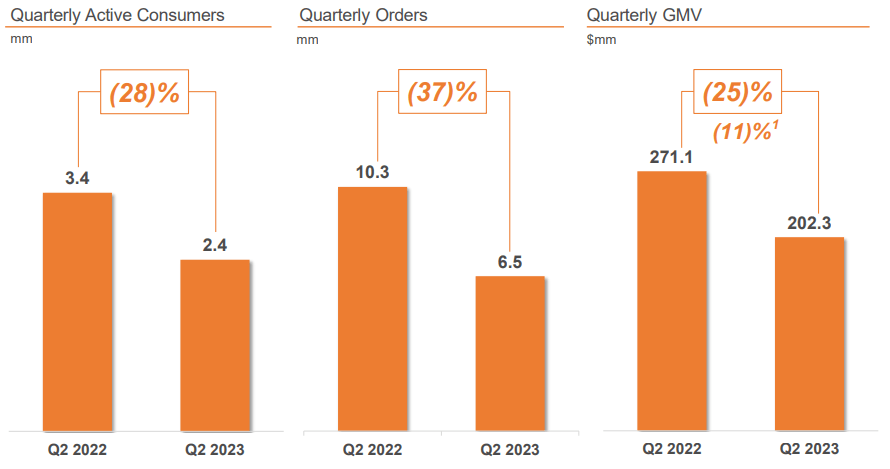

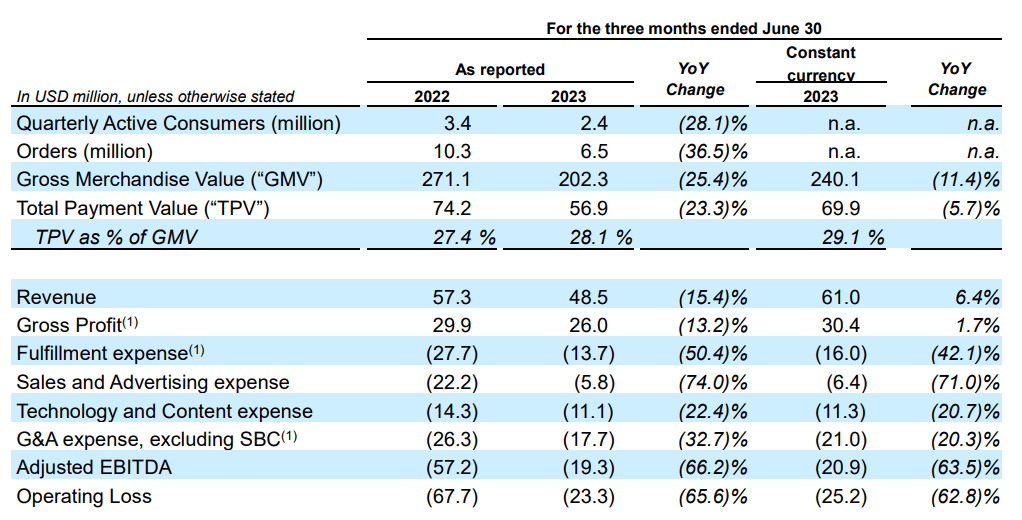

The reason I do not share the management's confidence in the EBITDA loss improvement is a massively deteriorating revenue side. In Q2, all key metrics driving sales deteriorated massively on a YoY basis. The key three usage performance metrics deteriorated by more than 25% YoY. The management explains it by a challenging environment, but I can hardly imagine that retail sales in geographies where the company operates shrank by 25%. That said, the effect of macro headwinds is only partial, and the rest relates to the weak company's performance overall.

JMIA's latest earnings presentation

{kind=link}

As a result, revenue declined by 15.4%. The good point is that the management managed to cut expenses at a higher rate than revenue dropped, leading to a solid YoY EBITDA loss and operating loss improvement. The thing I don't like about this improvement is that the major source was a four-fold cut in sales and advertising expenses. Jumia's business is still growing with no solid brand and word-of-mouth. That said, the revenue needs fuel to grow, and marketing is the only fuel for a young, emerging business like Jumia. When the company cuts its marketing expenses to almost zero, I highly doubt the ability to drive revenue growth and conquer market share.

JMIA's latest earnings presentation

{kind=link}

I think the better option would be to fuel revenue growth with substantial investments in marketing. But it would be the case if I was confident about the business model's viability. The management's bold decision to cut marketing expenses makes me think they are doubtful about the business model, and the model might need reconsideration.

To conclude, all these adverse recent developments and relatively low remaining liquidity do not make me optimistic about the company's prospects. Several red flags point to the fact that the business model of Jumia might not be economically viable.

Valuation

The stock price was almost flat year-to-date, underperforming the broad U.S. market. Seeking Alpha Quant assigns the stock an average "C" valuation grade, though several multiples are inapplicable due to negative profitability. JMIA's forward price-to-sales ratio is 1.6, almost two times higher than the sector median. This might suggest a substantial overvaluation, but I need more evidence.

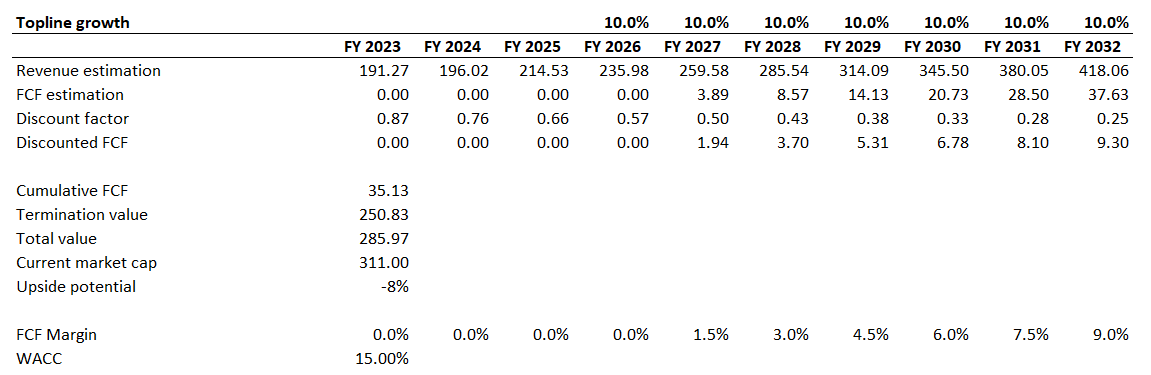

Therefore, let me proceed with the discounted cash flow [DCF] approach. I use an elevated 15% WACC because the company operates outside the U.S., and there is high uncertainty regarding when the company will turn profitable. I have revenue consensus estimates available up to FY 2025. For the years beyond, I have implemented a 10% revenue CAGR. The FCF margin is the hardest to project because the company currently has a massive negative metric. I consider JMIA turning positive from the FCF margin perspective not earlier than FY 2027 with 150 basis points further yearly expansion would be fair.

{kind=link}

Even after yesterday's 16% massive stock price drop after the earnings release, the stock still looks overvalued. Given the current cash burn rate, I do not include the current liquidity position in my DCF calculation because this cash and equivalents will be utilized within the next 3-4 quarters.

Risks to my bearish thesis

I already had a bitter experience with my other bearish articles about fundamentally weak companies. However, large reputable companies suddenly bought stakes or provided financing, which ensured massive short-term rallies for these stocks. That said, there is a possibility that some reputable investors might select Jumia as an investment target which might make the stock price skyrocket. That is the only probable risk that I see for my bearish thesis, given very weak fundamentals.

Bottom line

To conclude, JMIA is a "Strong Sell". The company is fundamentally weak, and I consider current management's cost-cutting steps related to sales and marketing as a "last resort" before they give up on this business model. The current liquidity position is sufficient to finance operations over the next 3-4 decades, and there is little certainty regarding the company's ability to stay in business longer. All key revenue metrics declining at above 20% rate is a huge red flag to me, especially given favorable secular headwinds for the e-commerce industry globally.

For further details see:

Jumia Technologies: I See Several Red Flags