JMIA - Jumia Technologies: More Cost Reductions Improved Monetization But Poor User Metrics

Summary

- Jumia Technologies continues to restructure its business for cost efficiency and lowering (adjusted) EBITDA losses.

- Macro headwinds, like inflation, currency weakness, and supply chain issues, are creating poor user metrics and pressuring the top-line.

- While the company promised significant reductions in adjusted EBITDA loss for 2023, gross margins have likely peaked for now.

- All together, 2023 will be yet another transition year on the way to profitability and a growth inflection. Fortunately, the stock looks almost completely de-risked at current levels.

Jumia Technologies ( JMIA ) is a leading e-commerce company in Africa. Last week, the company reported Q4 2022 earnings that focused on its latest achievements in reducing losses and costs as well as improving monetization. Former acting, and now permanent CEO, Francis Dufay, provided additional details on strategic initiatives that focus the company on a smaller set of core competencies and opportunities. Unfortunately, Q4 was also another quarter of disappointing user and demand metrics. Inflation, domestic currency weakness, and supply issues combined to reduce the count of active customers and orders on a year-over-year basis. Quarterly GMV (gross merchandise value) also fell but on a constant currency basis managed to stay flat. The smaller customer base was higher quality as represented by small declines in order cancellation rates. The company identified drivers from “an enhanced user interface and experience as well as improving consumer education.” Still, long-term investors in JMIA must continue to wait for signs of a growth inflection point in the business.

Restructuring

Dufay struck a different tone for Jumia with a restructuring and rationalization of the business. The company retrenched from initiatives originally designed to explore and experiment for growth potential. The company is more focused on core competencies with proven track records or imminent payoff. This restructuring so far trims the hedges but does not replant the fields. Presumably, the changes will still provide both a higher quality platform for future growth and a leaner business for navigating today’s macro headwinds. Dufay introduced the ideas in the Q3 2022 earnings report . The Q4 report provided more specifics. The truncated and discontinued businesses reportedly represent less than 4% of total GMV, 9% of revenue, and 2% of EBITDA loss in the first 9 months of 2022. The earnings presentation summarized the restructuring:

- Ended Jumia Prime because of lack of user adoption and retention.

- Eliminated first party grocery from Algeria, Ghana, Senegal and Tunisia because of excessive complexity and poor unit economics.

- Limited logistics-as-a-service to Nigeria, Morocco, and Ivory Coast where “logistics is ready to support third-party volume and where proof of concept has been established.”

- Eliminated food delivery from Egypt, Ghana and Senegal because of inability to scale economically.

While this restructuring introduces more focus to the company, it was not a major source of cost reduction. The cost reductions came from operational efficiencies and other strategic choices.

Cost Reductions

For Q4, Jumia reported an EBITDA loss of $49M, which was at the lower end of the guidance range of $42M to $62M. For the full year, Jumia reported an EBITDA loss of $207M. This loss was below the midrange of its $200M to $220M guidance for 2022. For 2023, Jumia promised to cut the EBITDA loss further by up to 50% with a range between $100M and $120M. The company bases its confidence on its existing initiatives. In response to an analyst’s question, Dufay implied that any further deterioration in revenues would be met with additional cost cutting in order to hit guidance for 2023. This commitment is important given the $227.8M in cash and deposits on the balance sheet. Cost reduction is the bridge to get the company to the other side of growth.

On a constant currency basis, operating loss decreased 34% year-over-year and adjusted EBITDA loss decreased 22%. Adjusted EBITDA is EBITDA further modified by stock-based compensation. This line-item was positive $12M a year ago and negative $2.3M this year (the significant change was not explained in the earnings report, but I assume company layoffs had an impact). Jumia slashed costs across fulfillment, sales and advertising, and general administrative (layoffs). Fulfillment costs declined partially from a 12% decline in orders. More importantly, Jumia achieved unit cost reductions. “The ratio of fulfillment expense per order excluding JumiaPay App orders, which do not incur logistic costs” fell from 3.24% a year ago to 2.17% in Q4 2022. Fulfillment expense also dropped from 9.2% to 8.5%. Jumia explained that the company is finding savings by optimizing “footprint and logistics routes, improving warehousing staff productivity and reducing packaging costs.”

Jumia improved marketing efficiency ratios. Sales and advertising expense per order declined year-over-year from $2.80 $1.90. Sales and advertising expense improved three percentage points year-over-year to 6.5%. Interestingly, Jumia reported “little correlation between marketing spend and growth of the countries when looking country by country.” Thus, a reduction of such spending makes sense until the company figures out what works best.

Jumia also reduced spend on “some of the heavily promotional categories on the JumiaPay App, such as airtime sales and virtual sales.” Sales of these items also took a hit from the lower marketing investment.

Monetization

Cost reductions drove the gross profit and the gross profit margin to all-time highs, $41.0M and 14.5% of GMV, respectively. Jumia explained this achievement as “mostly the consequence of commissions increase, that was undertaken mid-’22. We’re also hitting a record level of advertising revenues.” The company cautioned that it does not expect additional commission increases. As a result, gross profit margin will change little from Q4 levels in coming quarters. Future monetization gains may come from scaling the business. However, scaling is running up against macro headwinds.

Declines In Usage and Demand

Usage and demand declines delivered the most disappointing news in the earnings report. In Q3, Jumia showed off the ability to grow despite a challenging economic environment. Q4 was a different story even with the period including the holiday season. The weight of the macro environment was a reminder of the sizable gap Jumia has to close to become a growth company.

Orders declined by 12% year-on-year as a result of both “macro changes and a rate category rationalization.” Orders increased sequentially 5.3%. Active customers declined 15% year-over-year and increased sequentially 3.2%. In addition to macro headwinds, customer count declined from an elimination of sale items with “more challenging unit economics, including grocery as well as the number of digital services on the JumiaPay app.” As I mentioned earlier, GMV declined 14% year-over-year but was flat on a constant currency basis. GMV increased 17.6% quarter-over-quarter.

Jumia reported that inflation impacted supply chains and demand in Egypt, Ghana, Tunisia, and Nigeria. Currency depreciation relative to the U.S. dollar hurt GMV across Jumia’s markets.

Perhaps on the positive side, Jumia’s restructuring “removed layers of central management and business complexity.” Hopefully, this brings leadership and decision-making closer to local markets which in turn will enable a “clear focus on profitability and long-term sustainable growth.”

The Trade

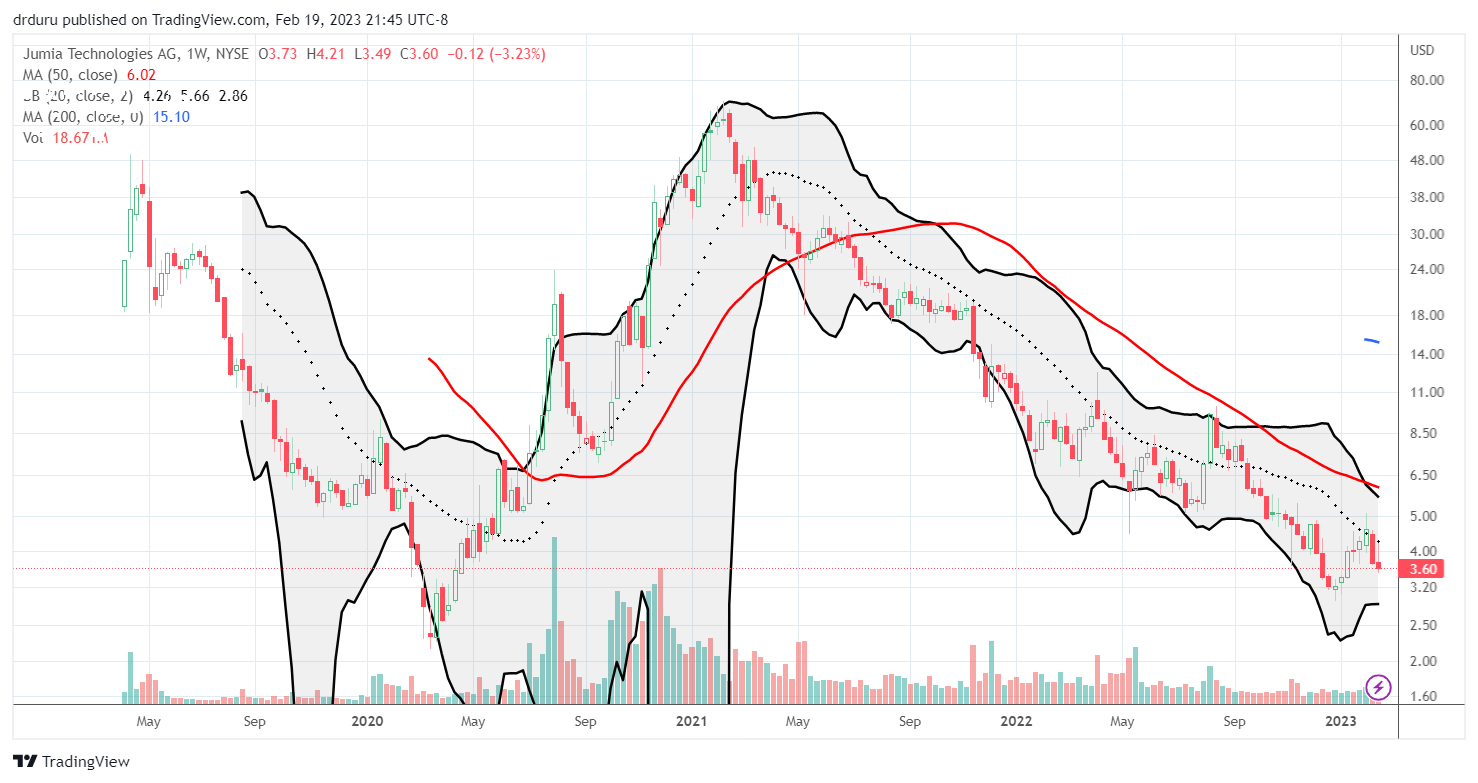

JMIA understandably lost 11.7% after disappointing on growth. The stock now trades close to its December low which in turn was a 2 1/2 year low. Investing in Jumia continues to be a bet on the long-term future of e-commerce in numerous African countries but that future has yet to clearly materialize. Yet, trading at 2x sales , JMIA looks nearly completely de-risked if the company can stabilize sales. I am still looking to add shares, but I am staying patient. I want to see at least the outlines of fresh growth catalysts.

{kind=link}

JMIA's weekly chart shows a 2-year slide that may not be quite over yet. (TradingView.com)

Be careful out there!

For further details see:

Jumia Technologies: More Cost Reductions, Improved Monetization, But Poor User Metrics