JMIA - Jumia Technologies: Shift In Strategy Creates A Viable Path To Profitability

Summary

- Jumia's recent shift in strategy has created a viable path to profitability.

- Jumia still has significant work to do to lower costs, improve efficiency and scale the business before breakeven is achieved.

- Structural limitations on the growth of ecommerce in Africa will likely limit Jumia's returns, even if the company does reach profitability.

Jumia (JMIA) is a leading ecommerce and digital payment platform in Africa. Since listing in 2019, the company has struggled with moderate growth and large losses that have shown little sign of improvement. Despite this, the stock has seen several boom and busts, as investors have at times been enthralled by the Africa ecommerce narrative. A recent change in management has been behind a shift in strategy that is prioritizing profits over growth and eliminating some of the waste that has plagued the company. While Jumia still has a long road ahead to prove that it has a viable business, the new strategy at least makes this a possibility, and the company still has a relatively large amount of cash and financial assets on hand to support ongoing losses.

Management

Jeremy Hodara and Sacha Poignonnec stepped down from their Co-CEO roles in November 2022. While the specific reason hasn't been stated, it appears that the supervisory board did not believe in the strategic direction of Jumia or its ability to achieve profitability.

Francis Dufay and Antoine Maillet-Mezeray have been appointed as members of the company's Management Board and Francis has been made acting CEO. Francis has been with the company since 2014 and has held multiple senior leadership roles, including CEO of Ivory Coast. He was most recently responsible for the group's e-commerce business across Africa. The new management team is focused on building a profitable and growing business , while the search for a permanent CEO is ongoing.

Shift in Strategy

To achieve profitability Jumia believes they need to scale the business and implement a far more efficient cost structure. The company's strategic priorities now include:

- Enhance business focus by terminating a number of non-core activities in support of unit economics

- Significantly reduce costs

- Accelerate monetization

Jumia Prime has been discontinued as adoption of the product and user retention fell short of targets . The monthly subscription program with free delivery was trialed over the past few years and management has blamed its failure on market immaturity.

Jumia is also scaling back first party grocery activity in Algeria, Ghana, Senegal and Tunisia. This is expected to improve profitability and reduce business complexity. The grocery vertical has a number of procurement and logistics challenges and Jumia has decided not to continue investing in countries where the grocery business is operating below the minimum viable scale. Jumia believes that the grocery vertical is able to improve marketing efficiency in more advanced markets. In smaller markets it adds operational complexity without providing sufficient upside in terms of product adoption and user retention.

Jumia has also suspended their logistics-as-a-service offering in a number of countries as they are shifting focus to improving logistics for their own e-commerce business. They will continue developing logistics-as-a-service in Nigeria, Morocco and Ivory Coast as the concept has already been proven in these countries.

Food delivery has been discontinued in Egypt, Ghana and Senegal due to poor economics. For example, in Egypt the market is competitive and there are a number of established vendors, making it difficult for Jumia to succeed. Despite this, food delivery remains a core part of Jumia's value proposition, and they plan on continuing to support its development across their largest markets, Nigeria in particular .

JumiaPay continues to be a strategic priority , but Jumia is not going to subsidize payment penetration on the platform. Jumia is working on product and UI/UX to make JumiaPay a more effective enabler for their e-commerce business. Jumia plans on expanding their payment processing activities in Nigeria and Egypt where they have already obtained the relevant licenses.

Financial Analysis

While Jumia's business continues to expand, growth has been fairly modest due to a combination of macro factors and Jumia rationalizing their product portfolio, like grocery, food delivery and the number of digital services on the JumiaPay app.

Some countries have seen supply challenges due to a shortage of US dollars , like Egypt. Supply has also been impacted in Tunisia and Nigeria. Depreciating currency values have also weighed on Jumia's revenues, which are reported in USD. In particular, during the nine-month period ending September 30, 2022 compared to same period of 2021, the Nigerian Naira, Egyptian Pound and West African CFA depreciated by 5%, 14% and 13%, respectively against the dollar.

Jumia has not given guidance on revenue or GMV for 2023, which indicates management uncertainty regarding topline growth prospects. They have given guidance on operating losses though, indicating that Jumia is willing to do what it takes from a cost perspective to achieve profit targets, independent of revenue growth. Jumia expects to halve their adjusted EBITDA loss for 2023 versus 2022, with adjusted EBITDA loss in the 100-120 million USD range.

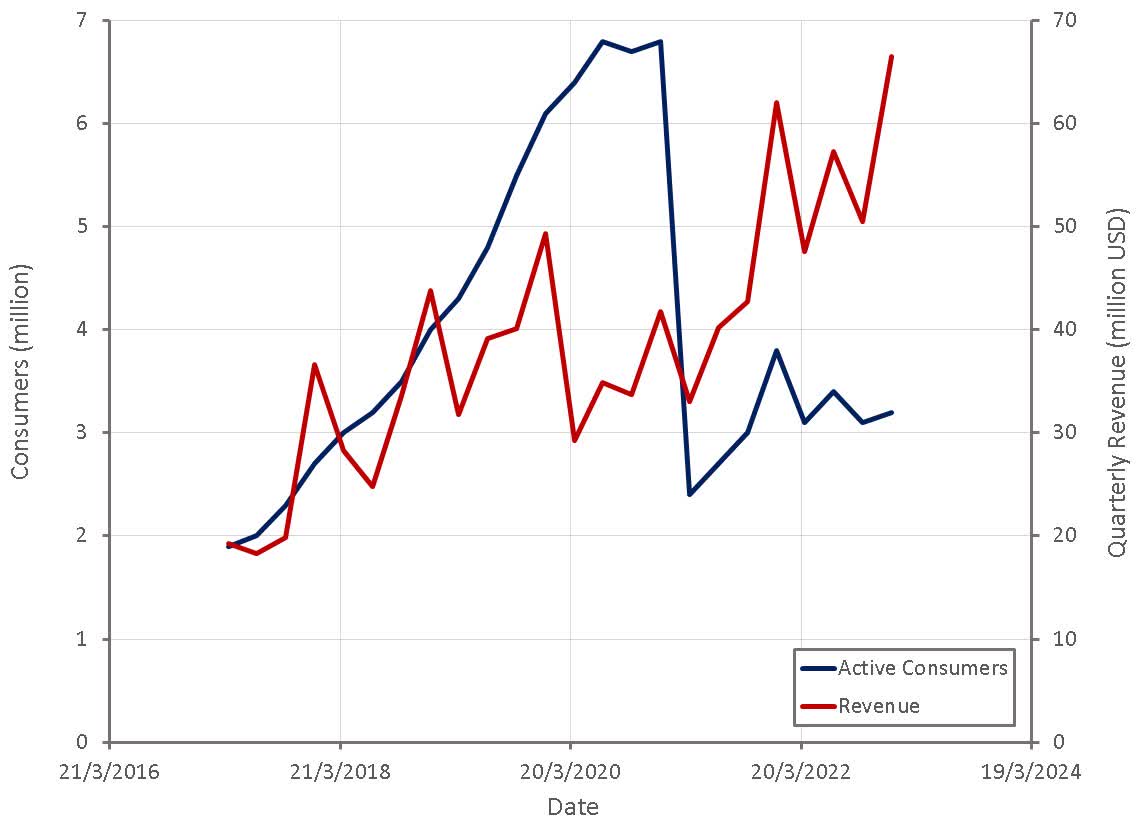

Figure 1: Jumia Revenue and Active Consumers (source: Created by author using data from Jumia)

{kind=link}

GMV growth has been weak in recent years as Jumia has reduced geographic exposure and more recently their product portfolio in support of margins. As a result of these factors, it is difficult to say what Jumia's underlying growth rate is, but given the lack of growth in active consumers, it appears that growth is fairly modest.

Jumia can continue to grow revenue by offering more services and increasing adoption of existing services, but ultimately the user base needs to increase to support the long term success of the company.

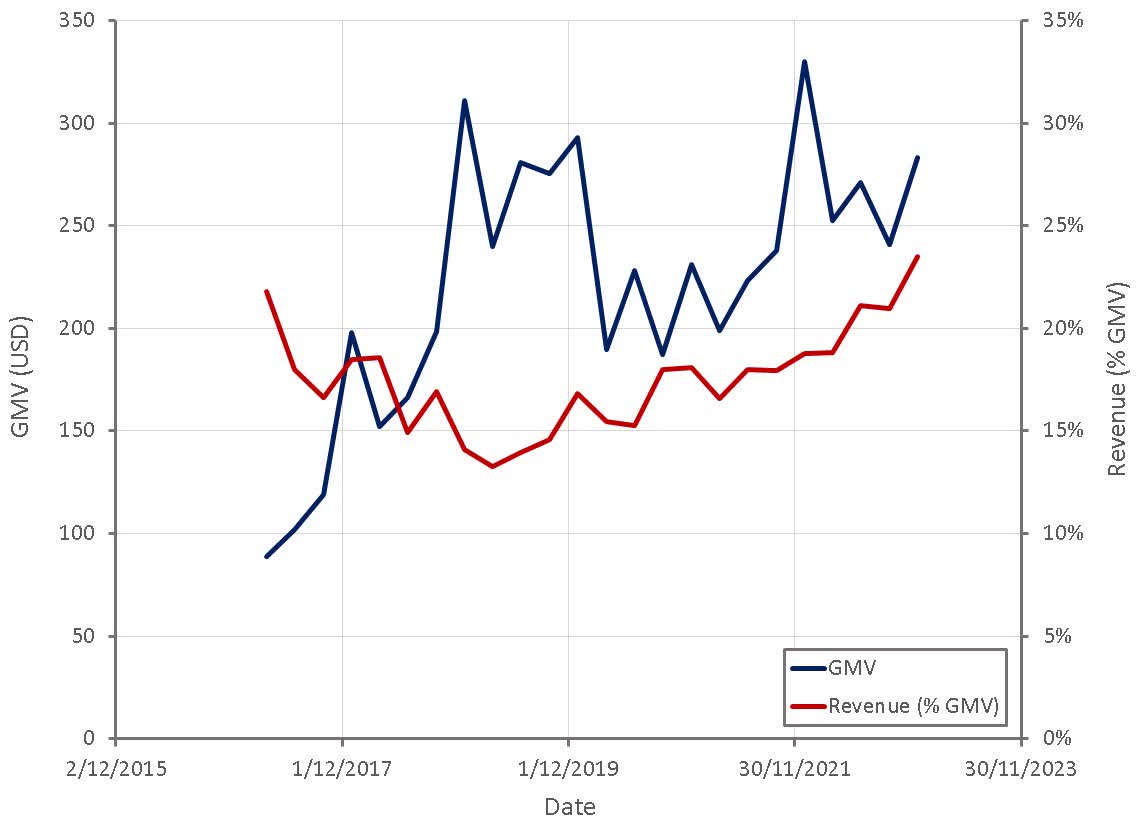

Figure 2: Jumia Gross Merchandise Value (source: Created by author using data from Jumia)

{kind=link}

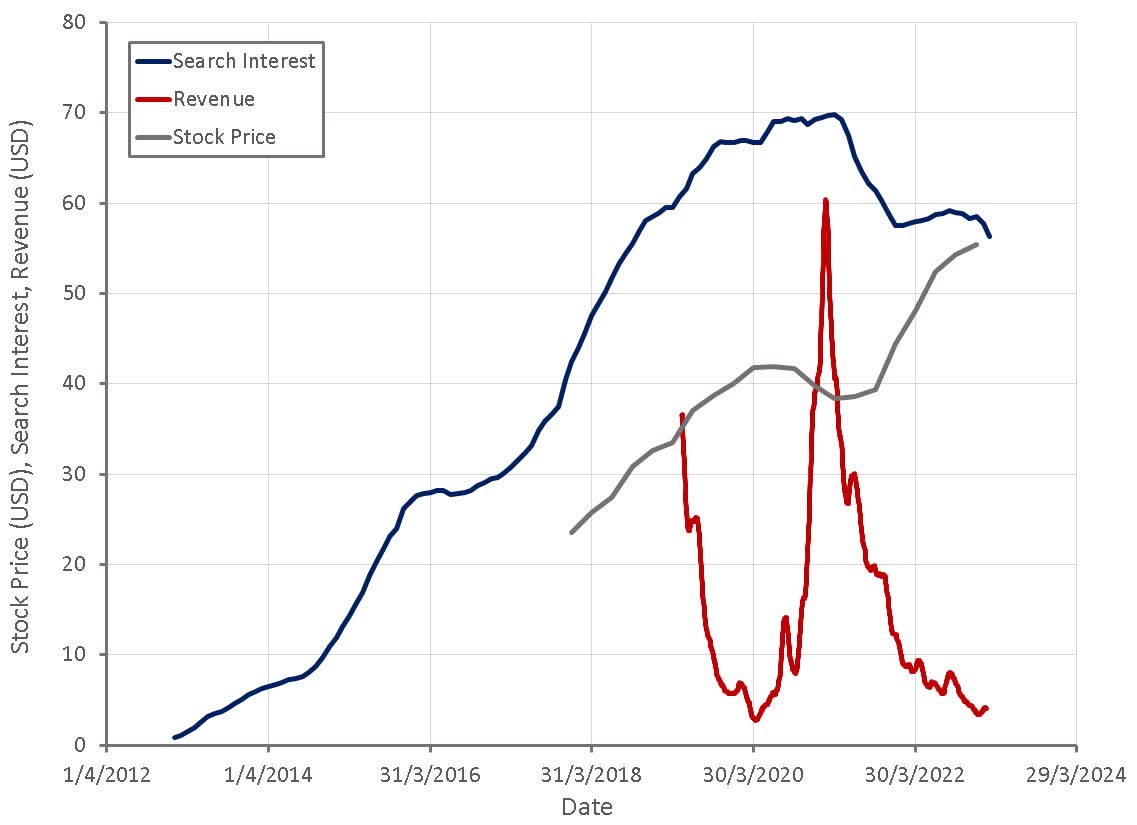

Search data indicates that interest in Jumia's platform has been declining, which could be the result of product rationalization or Jumia reducing their geographic footprint.

Figure 3: Jumia Search Interest (source: Created by author using data from Jumia, Yahoo Finance and Google Trends)

{kind=link}

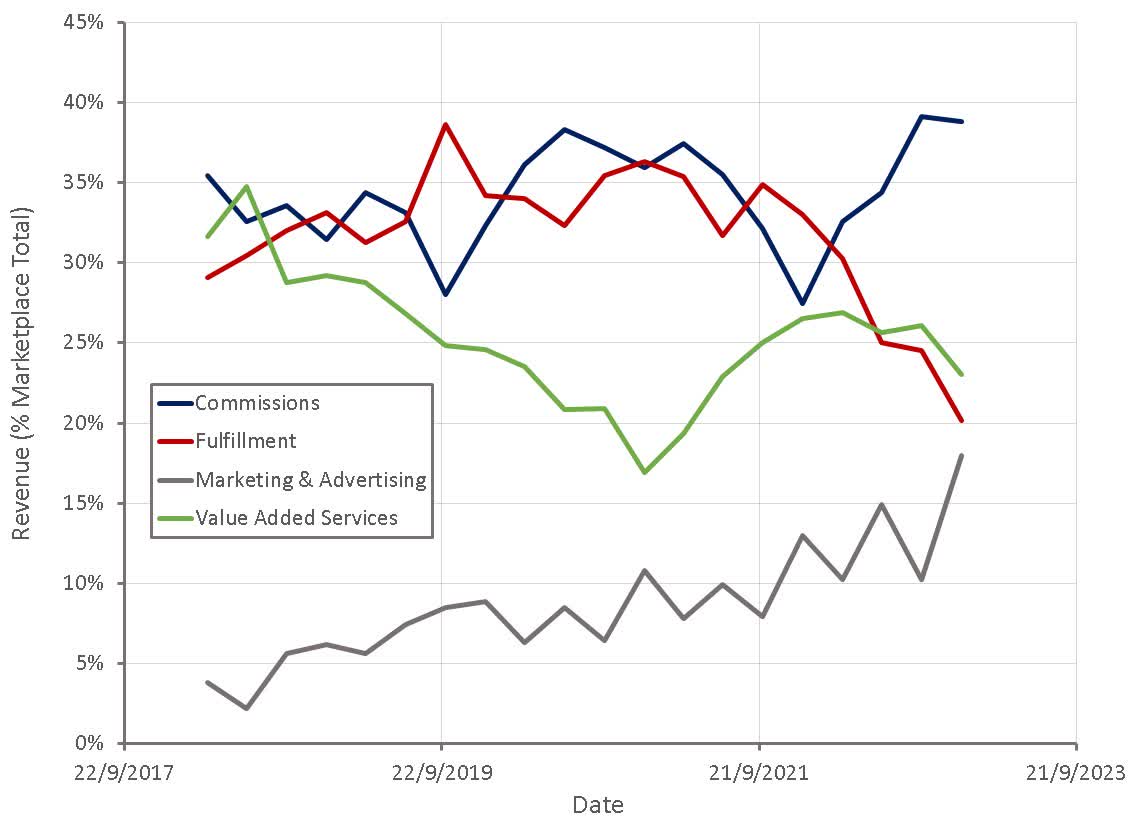

A shift in Jumia's revenue mix has been the major driver behind the company's recent margin improvements. Value-added service revenue has been increasing on the back of growth in warehousing service revenue . Fulfillment revenue has declined, in part due to the selected deployment of next day free delivery early in 2022. Jumia is currently introducing changes to this program, including introducing higher minimum basket sizes and restricting its geographic scope in order to support margins.

Jumia recently increased commissions , which has supported revenue growth and margins, but the company realizes that vendors must be successful to support the long term health of the platform, and hence further increases in commissions are not expected.

Figure 4: Jumia Revenue Breakdown (source: Created by author using data from Jumia)

{kind=link}

With a renewed focus on unit economics, and creating a more efficient business, Jumia's margins are beginning to improve. Despite this, some of the recent improvements are from one-time gains and future incremental progress is likely to prove more difficult.

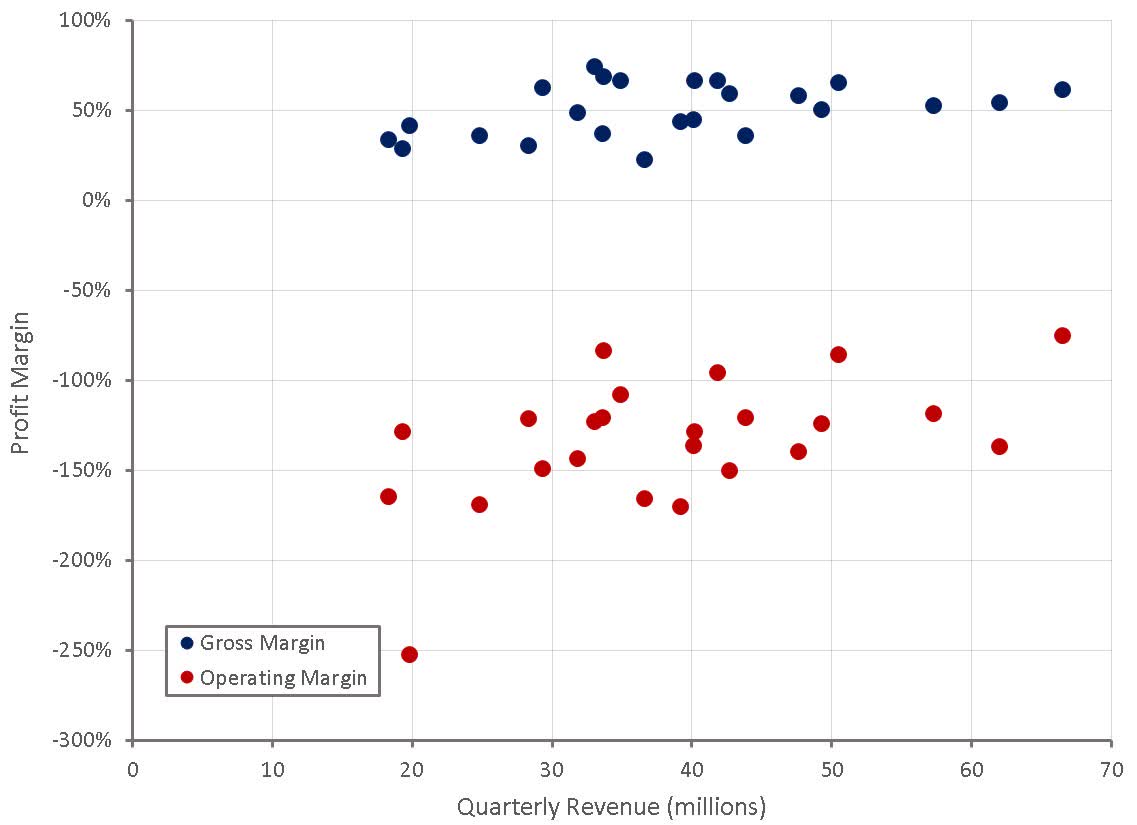

Figure 5: Jumia Profit Margins (source: Created by author using data from Jumia)

{kind=link}

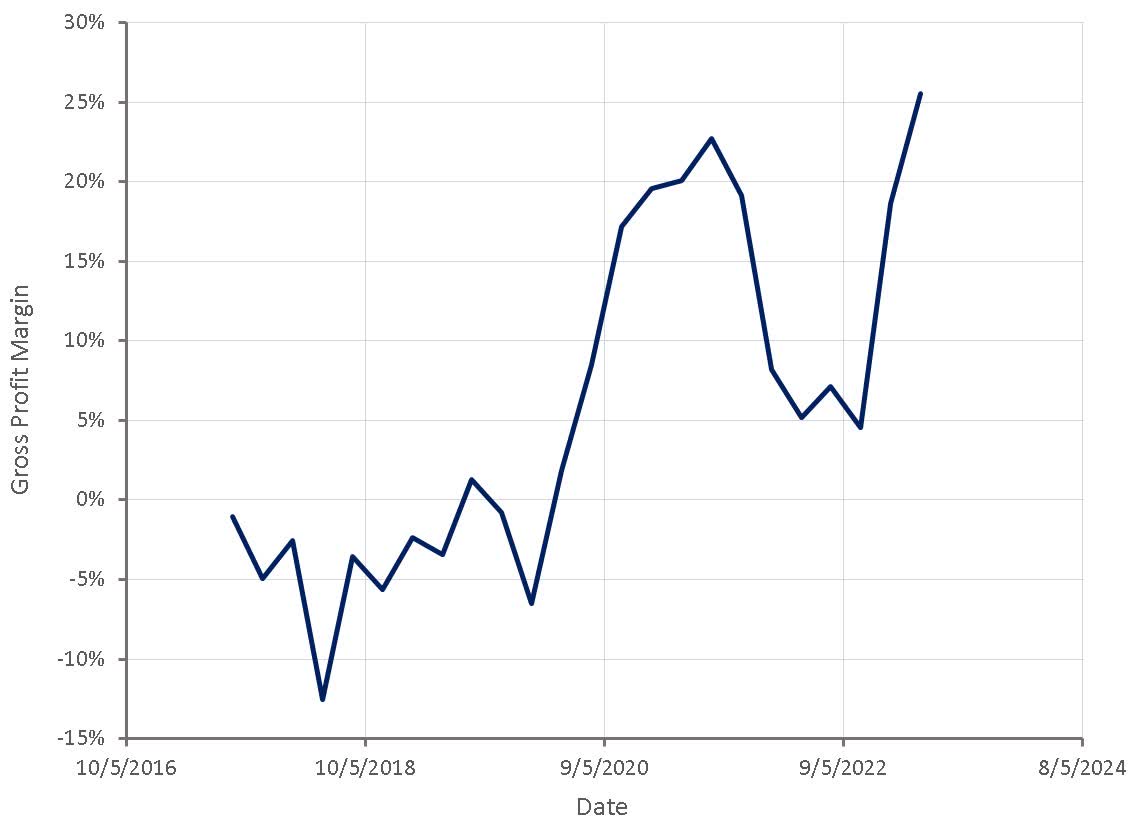

Jumia treats fulfillment as an operating expense, which is acceptable, but it could be argued that it does not reflect the true nature of their business. Including fulfilment in COGS shows how marginal Jumia's business has been in the past. With an increased focus on unit economics and a willingness to abandon initiatives that are not scaling, Jumia's gross profit margins are now improving to the point where the business could eventually be profitable.

Figure 6: Jumia Gross Profit Margin (source: Created by author using data from Jumia)

{kind=link}

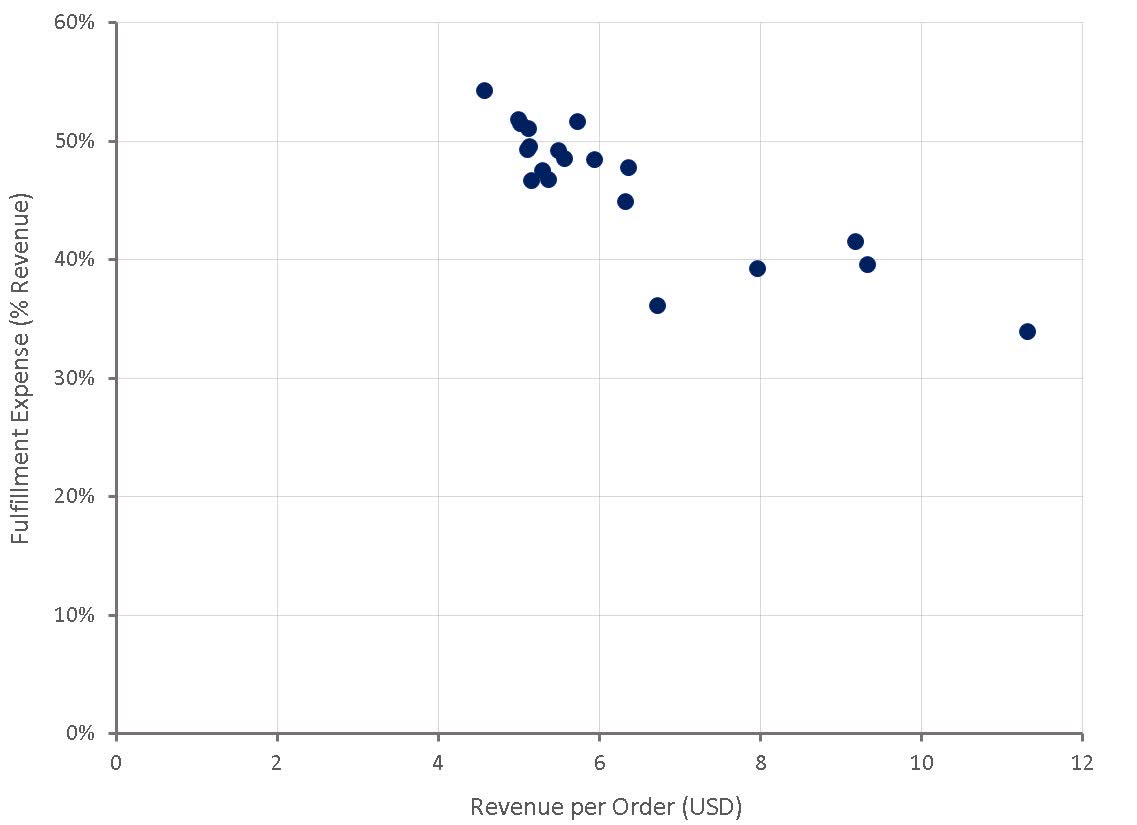

Reducing the burden of fulfillment expenses will be integral to Jumia achieving profitability. Management is currently trying to reduce cancellation rates, failed deliveries and returns in support of this. The CFDR rate as a percentage of orders improved from 16% in 2021 to 15% in 2022. Particularly good progress was made on cancellation rates as a result of consumer education and an enhanced user interface. Jumia is also optimizing their footprint and logistics routes, improving warehousing staff productivity and trying to reduce packaging costs.

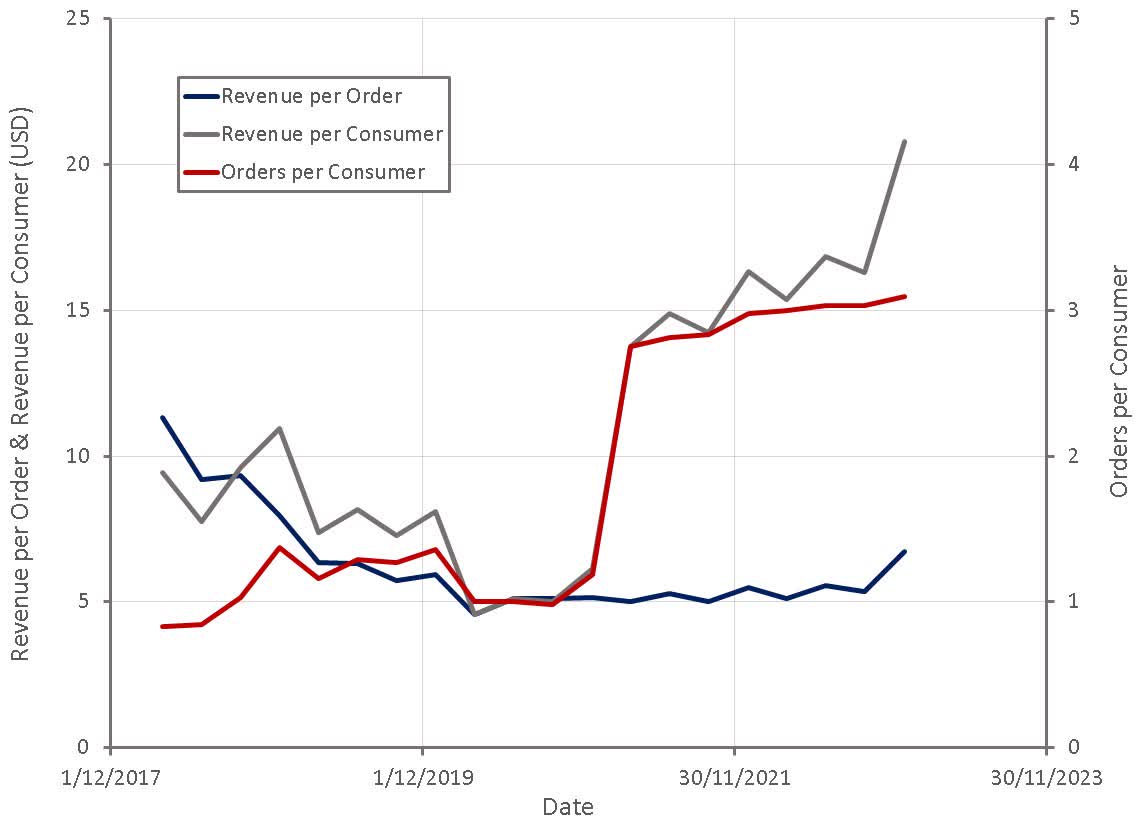

Increasing basket sizes is another way for Jumia to reduce the burden of fulfillment expenses. In this respect, the company must balance its own needs with the demands of consumers and vendors on the platform. If nothing else, an end to the trend of less revenue per order should be more supportive of margins going forward.

Figure 7: Jumia Fulfillment Expenses (source: Created by author using data from Jumia) Figure 8: Jumia Active Consumers and Orders (source: Created by author using data from Jumia)

{kind=link}

{kind=link}

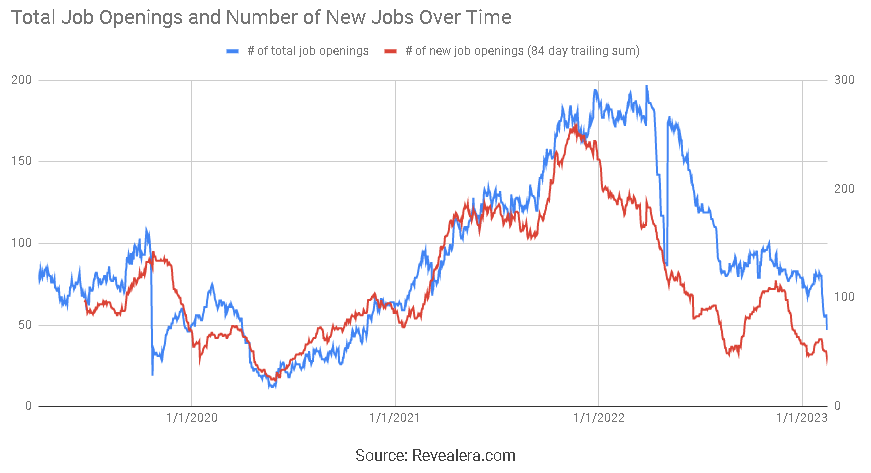

Jumia reduced headcount by 20% in the fourth quarter, but this is yet to impact the company's bottomline. Jumia's presence in Dubai has also been significantly reduced, with the headcount their cut by over 60%. Most remaining staff are being relocated to Jumia's African offices. The implementation of these measures cost the company 3.7 million USD in the fourth quarter but are expected to reduce monthly staff costs by 30% going forward.

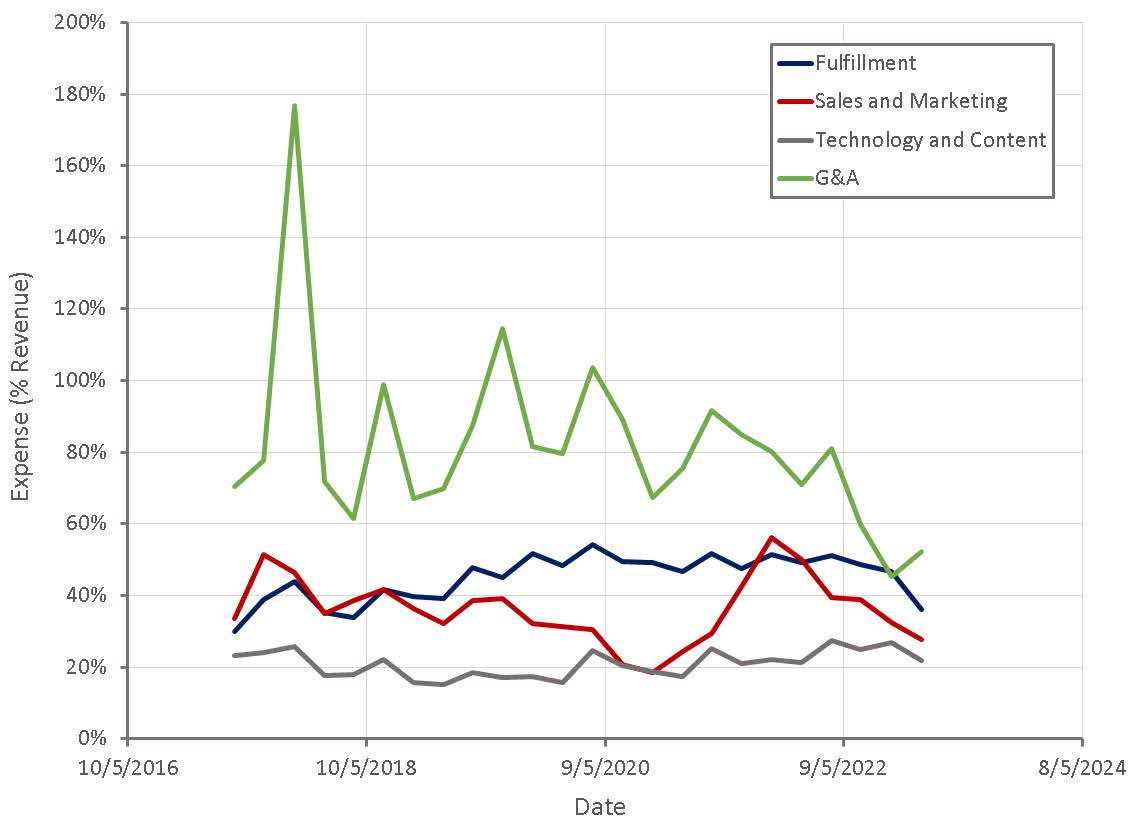

The fact that Jumia's general and administrative expenses averaged around 80% of revenue in the past highlights how the company has never been in a position to achieve profitability, and until the past six months does not really have been trying to.

Figure 9: Jumia Operating Expenses (source: Created by author using data from Jumia) Figure 10: Jumia Job Openings (source: Revealera.com)

{kind=link}

{kind=link}

Valuation

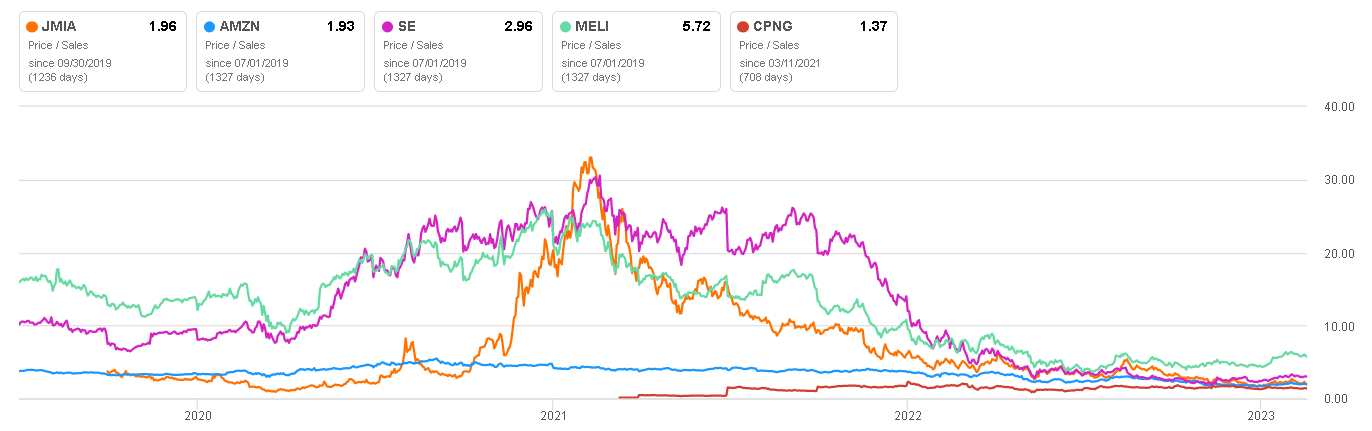

Jumia trades on a P/S multiple that is broadly inline with many ecommerce peers, but it is difficult to draw conclusions from this. There are structural reasons for believing that ecommerce growth is likely to be relatively slow in Africa and that costs will remain high. Ecommerce penetration is still extremely low in Africa though, which could mean that a successful platform is able to achieve an above average growth rate for decades. Based on a discounted cash flow analysis I estimate that Jumia's stock is worth approximately 3 USD per share, but there is a large amount of uncertainty in this estimate. While the new management team is giving the company a fighting chance, Jumia's ability to achieve reasonable profit margins and drive more widespread adoption of ecommerce in Africa remains to be seen.

Figure 11: Jumia Relative Valuation (source: Seeking Alpha)

{kind=link}

For further details see:

Jumia Technologies: Shift In Strategy Creates A Viable Path To Profitability