JMIA - Jumia Technologies: The African E-Commerce And Digital Payment Services Opportunity

Summary

- Jumia is a pan-African e-commerce company with a diverse group of 100K sellers offering goods across a wide range of categories.

- Jumia's market valuation has suffered a steep decline of more than 90% from its peak market valuation.

- Jumia presents an attractive opportunity to gain exposure to the African continent, however, this exposure comes with significant risks.

Investment Thesis

Jumia (JMIA) is a unique company with an opportunity to become a major player in the growing African e-commerce market. The company has also made investments into different segments such as food delivery and its own financial services app JumiaPay. These investments combined with its already leading position in the e-commerce market makes Jumia an interesting investment opportunity. About two years ago, Jumia reached its highest market valuation at $5.1 billion, since then the company's valuation has crashed by more than 90% to its current market valuation of $368 million. This also presents an interesting opportunity as investors could gain exposure to the African region at a significant discount compared to two years ago. However, there is a reason for this steep discount, Jumia operates in the African continent where it faces numerous challenges and risks. Further to this, the company has also experienced a slowdown in revenues and has depleted over 50% of its resources on its growth acceleration strategy. Taking these factors into consideration I consider this stock to be a hold. It presents a very attractive opportunity to gain exposure to the African continent which is expected to experience accelerated growth during the next years, but it also presents significant risks which cannot be ignored.

Company Description

Jumia is a pan-African e-commerce company with a diverse group of 100K sellers offering goods across a wide range of categories including fashion and appeal, beauty and personal care, home and living, fast moving consumer goods, smartphones, and other electronics. Additionally, Jumia offers other on demand services to its users such as its Jumia Food platform, including delivery, from restaurants, grocery shops and convenience outlets. Furthermore, JumiaPay app offers a number of digital lifestyle services including utility bills payment, airtime recharge, gaming and entertainment, transport ticketing as well as financial services such as micro-loans, insurance, or savings products. These services help the company derive revenues from its marketplace which is broken into different streams including, sales of goods, commissions, fulfillment, marketing & advertising, and value-added services.

Finally, it should be mentioned that the company is active in three regions of Africa and in a total of eleven countries. These eleven countries collectively represent more than 600 million people, about 70% of Africa ' s internet users and about 68% of Africa ' s $2.9 trillion GDP (2021).

Financial Highlights

Jumia Financial Highlights (Company Annual and Quarterly Reports)

Given Jumia is a company which is still in its growth phase, it remains to become profitable. As such the company has relied on external financing in order to continue operations. The company was able to bolster its balance sheet through proceeds from two different offerings in 2020 and 2021. These offerings helped Jumia receive $570 million and have the necessary liquidity to execute its growth acceleration strategy. This strategy is already in action with investments targeted for increased consumer adoption, advertising, user experience regarding Jumia's platform, and investments in technology and content. These investments have yielded results with annual active reaching 8.4 million, Gross Merchandise Value ("GMV") reaching the $1 billion mark, and orders totaling $39 million at the end of 2022 .

Theses investment have helped Jumia regain its momentum and experience revenue growth as the company suffered a steep decline in revenues during the pandemic. Saying this, the company has also experienced substantial losses during the last three years. Despite these losses management keeps making substantial investments in R&D, spending around 20% to 25% of sales in R&D on yearly basis. Management has been able to keep investing while experiencing losses because of the strong balance sheet it was able to build through the previously mentioned offerings where the company received $570 million. However, the losses are already creeping into the balance sheet and have depleted the company's liquidity position by 55%. This development will hinder management's capacity to keep throwing resources into its growth acceleration strategy.

During 2022 the company increased revenues by ~25% to $222 million, however it also saw a cash outflow of $251 million for the year. This cash outflow results in about $63 million cash burn rate on a quarterly basis. This has decreased the company's liquidity position to $228 million compared to $513 at the end of 2021. Management will need to decrease the quarterly cash burn rate or the company will run out of money within 12 months. Management has already stated that it has put strategic actions in place to reduce the quarterly cash burn rate and gave guidance that EBITDA loss for 2023 will decrease to $100 million to $120 million. This decrease will be accomplished through lower advertising expenses which will decrease by about 50% to between $30 million and $40 million, compared to $76 million during 2022. As well as General & Administrative expenses decreasing to $90 million and $105 million, compared to $122 million in 2022. These are welcomed news by shareholders, however because of the decreasing liquidity position, it is a necessity to follow Jumia very closely on a quarterly basis.

African Market Opportunity

The African e-commerce landscape shows favorable macroeconomic and demographic conditions, which include a strong GDP growth, a young population, and an expected rapid increase in mobile internet penetration. According to the United States International Trade Administration , Africa is set to experience a substantial increase in e-commerce users across the continent. Estimates show that by 2025, there will be about 520 million e-commerce users with an e-commerce penetration rate of 40%. This are fabulous numbers and leave a long runway for growth as penetration will not even be at the 50% mark.

e-Commerce penetration (USA International Trade Administration)

It is important to remember here that as of 2021, Africa comprised approximately 17% of the world's population. More interestingly, sub-Saharan Africa population is projected to double by 2050 and the populations of Northern Africa and Western Africa are expected to grow by 46% by 2050. Not only is the population expected to grow but it will also be mainly composed of young people, which should drive the e-commerce penetration rate.

Jumia is well positioned to take advantage of these trends. For example, according to the Internet World Stats, as of December 2020, Africa had an estimated 590 million internet users and 255 million Facebook users across the continent. 69% of internet users and 75% of Facebook users lived in the regions in which Jumia operates.

JumiaPay Opportunity

As of the end of 2022, JumiaPay services were available in eight markets: Egypt, Ghana, Ivory Coast, Kenya, Morocco, Nigeria, Tunisia, and Uganda. JumiaPay transactions and total payment volume ("TPV") have both increased significantly since the company launch this service. For reference the number of JumiaPay transactions reached 12.5 million in 2022 which is slight increase compared to 12.1 million in 2021 while, TPV reached $285 million, which is an increase of 8.4% compared to 2021.

JumiaPay also has a nice tailwind helping its growth which is that Africa is the leading continent in terms of mobile money technology adoption. According to data from GSMA , Africa was home to 548 million registered mobile money accounts in 2020, 46% of mobile money accounts globally, with a transaction value of $490 billion which equates to 64% of global mobile money transaction volume. Despite this, African nations are still well behind consumer banking habits, with about half of adults without a formal bank account. As a result, many of these economies are still cash based and present not only challenges but also opportunities for electronic payments. The penetration of mobile payments would offer consumers the opportunity to participate in the formal economy, this in turn would drive electronic payments for e-commerce orders.

Payment methods in selected African markets 2021 (USA International Trade Administration)

{kind=link}

Given JumiaPay platform allows customers to pay for goods and services online and many African nations needing more services and opportunities to make payment electronically it gives the platform a promising future. Saying this it remains to be seen if JumiaPay will be able to leverage its geographic footprint and expand its services across the continent.

Keys to Jumia's Survival and Success

Costs Reduction: As it can be seen from the article, Jumia is facing a liquidity problem with its funds decreasing by more than 50% from 2021 to 2022. Further to this, its quarterly cash burn rate stood at $63 million. Just by doing basic math, if Jumia continues burning cash at this rate it will run out of money within 12 months. As discussed earlier in the article, management has taken strategic actions to reduce costs which should give Jumia about two years with its current liquidity position.

Leverage Strengths across Geographical Footprint: Jumia is active in three regions of Africa and in a total of eleven countries. If management is able to leverage its most profitable services across these countries we could see Jumia edge closer to profitability. JumiaPay plays an important role here as it is a win-win scenario for both Jumia and the African population (discussed earlier in the article). Furthermore, Jumia needs to keep enhancing its e-commerce offerings by presenting customers the best product categories specific to each country. For example, in Senegal, earlier in 2022, Jumia stepped up its commercial efforts in the consumer electronics category. This led to a GMV increase year over year of approx 90%.

Attract New Funding: Jumia has many challenges in the African continent, nonetheless it has already acquired deep local expertise, a trusted brand with over 8 million annual active consumers, and powerful data insights. These attributes can help the company become profitable, however what management needs right now is more time. The way to get time is by attracting new funding and give the company the necessary liquidity to remain alive until it becomes profitable. The challenge for Jumia's management here will be to convince investors that profitability is indeed close.

Jumia Faces Numerous Risks

As Jumia is active in one of the most unstable regions in the world, its business faces several risks which could hinder the company's operations and growth. In this section I will outline a few of the risks faced by the company. However, it is important to note that I will only discuss the most important ones in my opinion. This said, Jumia faces more risks and challenges in the African continent than the ones discussed below.

Government Intervention: Governments in Africa frequently intervene in their economies and occasionally make significant changes in policy and regulations. Some governmental actions seen in the past include, nationalizations and expropriations, price controls, currency devaluations, mandatory increases on wages and employee benefits, capital controls and limits on imports, etc. Any of these actions by governments could have a detrimental impact on Jumia. As the company is still in its growth face, it does not have the sufficient resources to face adverse circumstances as the ones previously mentioned.

Terrorist Activities: To whomever follows the African region, it is no surprise to see the terrorist group Boko Haram in the news. This group has caused economic instability in Nigeria for multiple years, causing markets, shops, and schools to close and people to migrate out of the region. This group's harmful activities could have a negative impact on the region's economies as it weakens consumer confidence, diminishes purchasing power and harm businesses which operate in this region.

Economic Downturns: As Africa is a less developed region and economy, economic downturns are usually more significantly felt than in developed economies. Economic downturns in the region can cause currency volatility, steep declines in economic activity, difficult financial conditions for countries as a whole, among others. As Jumia operates in multiple African countries at the same time, the company is at a greater risk of an economic downturn in one of these countries. Saying this, Africa is expected to grow handsomely in the coming years, somewhat mitigating this risk.

Currency Volatility: As previously mentioned currency fluctuations are a risk for Jumia. As a result of operating in different countries, Jumia needs to work with currencies such as the Nigerian Naira, the Egyptian Pound, the Kenyan Shilling, and the West African CFA Franc. Fluctuations in these currencies can impact the company's financial results, the value of its assets, liabilities, etc. Jumia's management needs to have a protection scenario for all these currencies which is a difficult task for any management team.

Competition by Major Players : It is no secret that the biggest global e-commerce companies, such as Amazon and Alibaba already have their eyes set in the African region, such competitors have greater financial resources, technological advantages, as well as a well-known brand. In the on-demand services, Jumia also faces strong competition from well know players such as Glovo and Uber Eats. Finally, with JumiaPay, the company faces competition from various financial institutions in Africa. As it can be seen the competition is fierce in all segments, however Jumia is also a strong competitor with deep local expertise, a trusted brand with over 8 million annual consumers, and powerful data insights of the markets it operates in.

Valuation

Jumia's market valuation has experienced substantial volatility and a steep decline over the past two years. The company has gone from reaching its highest valuation at $5.1 billion, to crashing by more than 90% to its current market valuation of $368 million. This steep decline in valuation does not mean Jumia can't go lower, the company faces several risks one of them being running out of money in the next couple years. So, even if the company has already suffered a steep decline in its market valuation it does not mean it can suffer another 90% decline. Saying this, the company could also go back to its glory days and appreciate in market valuation giving investors solid returns.

With the current market valuation, the company's price to revenues multiple stands at 1.7x. I would argue that this is quite attractive when compared to 2 years ago when this multiple stood at 22.6x.

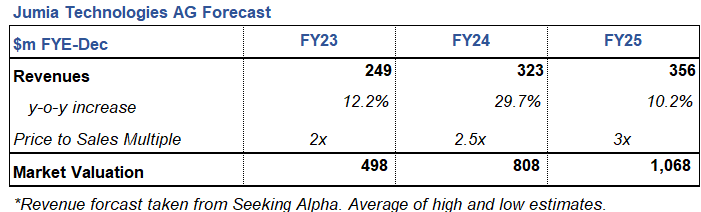

For the valuation of the company, I have used the market multiple method of price to revenues using future forecasted revenues. I have obtained the analysts' revenues forecast from Seeking Alpha data and have progressively increased the market multiple from 2x to 3x by 2025. I have increased the market multiple through the years as the tight economic environment we are currently in will fade away and multiples will start increasing again. If Jumia is able to stay solvent and is able to keep increasing its market share in the African e-commerce and other segments, we could see its market valuation reaching $1.1 billion by 2025. This is nowhere near its all-time high however it is a nice improvement compared to its current market valuation.

{kind=link}

Conclusion

Jumia presents an interesting opportunity to gain exposure to the African continent, the company is well positioned to take advantage of the markets it is currently active in and has the potential to become a leader due to its deep local expertise, trusted brand with over 8 million annual active consumers, and powerful data insights it is able to acquire from these customers. Jumia also benefits from Africa's large, fast-growing, and young population, growing mobile internet penetration, and increasing smartphone adoption. However, Jumia also faces significant challenges and risks including, government intervention, competition by global major players, currency volatility, economic downturns in different African nations, terrorist activities in the region, among others. Taking into account all these factors I believe it is better to be patient and see if Jumia's management is first able decrease its current quarterly cash burn, if management is able to secure external financing in order to secure the company's survival for the next three to five years and have a better picture of the company's results from its growth acceleration strategy. As such I consider this stock a hold and will keep monitoring it on a quarterly basis.

For further details see:

Jumia Technologies: The African E-Commerce And Digital Payment Services Opportunity