JMIA - Jumia: There's Still A Lot Of Uncertainties

2023-05-16 08:00:00 ET

Summary

- Under the new leadership, Jumia will continue to cut costs and improve the bottom line. Top-line growth will take a back seat in FY 2023.

- Better profitability is a step in the right direction, but questions about Jumia's capability to achieve long-term sustainable growth remain.

- Uncertainties linger. I maintain my neutral rating for the stock.

Jumia (JMIA) is a leading e-commerce player in the Pan-African market. Established 9 years ago and became a public company in 2019, the company has seen a fair amount of challenges in navigating the relatively tough business environment in Africa.

Revenue growth has been at +20% over the past few years, with the exception of the COVID period in 2020. Yet, growth has been inconsistent while profitability and cash flow generation continue to be the weak points.

With the shares down by over 8% YTD and 40% YoY, today's ~$3 price level may be attractive to some investors who wish to initiate a long position, though I will maintain a neutral stance for the stock.

I acknowledge that Jumia is more of a long-term opportunity that will benefit from the first-mover positioning to capture consumer growth potential in Africa. It is also well noted that the recent management change and various strategic initiatives, such as product and geographic expansions, are expected to steer the company towards further improvements.

However, the company's financial outlook has been underwhelming since my first coverage in 2020 , raising the long-term question about the commercial sustainability of not only the business but also the market.

Financials

The overall growth outlook reflects the challenge of capturing values in the Africa e-commerce market. Jumia ended FY 2022 with a revenue of +$221 million, a low figure for a typical market-leading e-commerce business. Growth has roughly been +20% on average, a decent figure, yet not been consistent over the years.

{kind=link}

Looking just at the Q4 results, my earlier concern about the overall commercial readiness of the market seems to be validated. So far, Africa has been a challenging environment. After its IPO, Jumia has expanded not only into different geographies but also various adjacent e-commerce verticals, such as payment, membership program (Jumia Prime), online groceries, as well as food delivery, to boost growth. But as much as it seems like the right strategy on the paper, the results have been disappointing . A lot of these programs ended up being terminated due to the lack of adoptions.

{kind=link}

Meanwhile, cash flow generation and profitability have been most affected by the increased operational complexities from the multi-country strategy. Given the lack of infrastructure in the regions where Jumia operates, Fulfillment and General and Administrative / G&A expenses have consistently been the biggest cost drivers. For G&A alone, Jumia typically spends +80% of its revenues every year.

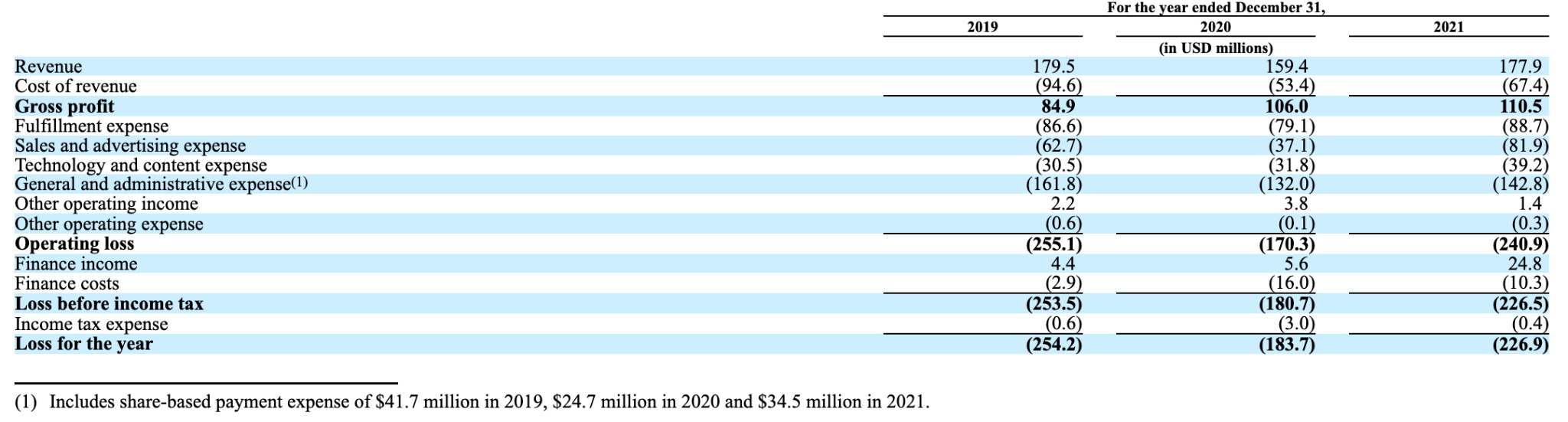

Another key loss driver has been the fulfillment business. Jumia's revenue is made up of 4 key business segments - marketplace, fulfillment, sales and advertising, and value-added services segment. While the marketplace segment ideally represents the largest revenue driver for Jumia as an e-commerce marketplace platform, fulfillment revenue has often been the same size or even bigger than that of the marketplace.

Nonetheless, it has been an unprofitable business. The fulfillment segment, for instance, generated $36 million of revenue in FY 2021, surpassing marketplace revenue of $35 million. However, Jumia also spent over $88 million on fulfillment expenses in that year. It is also important to note that Jumia does not report that fulfillment expense as part of its cost of revenue, despite recognizing fulfillment revenue as part of its total revenue. This effectively inflates gross margins and overstates its operating expenses.

{kind=link}

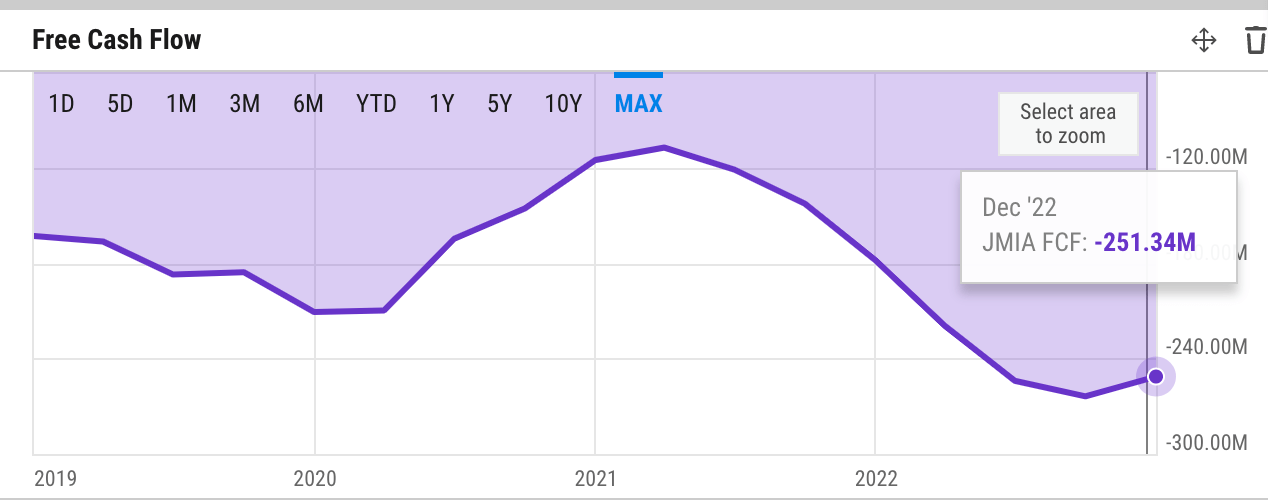

Looking at the FCF trend, we probably will get a better sense of how severe Jumia's financial outlook really is. As it stands, the business is still far away from breakeven. Jumia has consistently burned between $120 million - $240 million every year. At that level, Jumia generates higher cash burn than it does revenue. It is very unsustainable, and yet, we are even seeing an uptrend in cash burn since 2021.

Risk

In my view, the challenging operating environment, weak execution of growth strategies, and the need for continuous external financing raise concerns about the company's ability to deliver sustainable long-term value to its shareholders.

Enabling digital growth in emerging regions like Africa presents significant challenges for Jumia. Despite the theoretical growth potential associated with its multi-country strategy, this approach often introduces layers of operational complexities. Poor and fragmented logistics and mobility infrastructure, diverse customer bases, and a potentially price-sensitive environment all contribute to these challenges. Consequently, relying on geographic expansion as a growth lever is likely to result in weak fundamentals.

Given the weak financial performance, it is probably appropriate to put the blame on not just the management but also the board. It seems often that a management team faces substantial pressure to achieve growth, leading to the implementation of unexamined growth strategies. Jumia has frequently expanded its services to new markets prematurely, without first solidifying its fundamentals in existing markets. This approach turns Jumia into an experimental lab rather than a serious business. The failure of Jumia Prime, for instance, creates an appearance of misconception on the part of the management about the true problem the customer is facing on the ground. As it stands, it looks like a misapplication of the western concept to solve the wrong problem.

{kind=link}

Furthermore, as obvious as it is, Jumia's consistently negative operating cash flows indicate a heavy reliance on external financing to sustain its operations, which will continue to dilute shareholders. Since its IPO in 2019, Jumia has consistently raised hundreds of millions of dollars through equity offerings each year, accumulating over $900 billion in funding to-date. Consequently, share dilution has been severe, with the number of average shares outstanding increasing by 37% since 2019 alone.

Catalyst

Under the new leadership, Jumia will commit to driving operational efficiencies and focus on "fundamentals-led growth" . I see this as a big plus for the company at this time. Having burned a lot of cash to perform geographic and vertical expansion trial-and-error experiments over the past few years, demonstrating a path to sustainability and profitability is certainly just what the company needs to drive the market demand for the stock. In the next few quarters, I wish to continue to monitor the implementation of such strategies.

{kind=link}

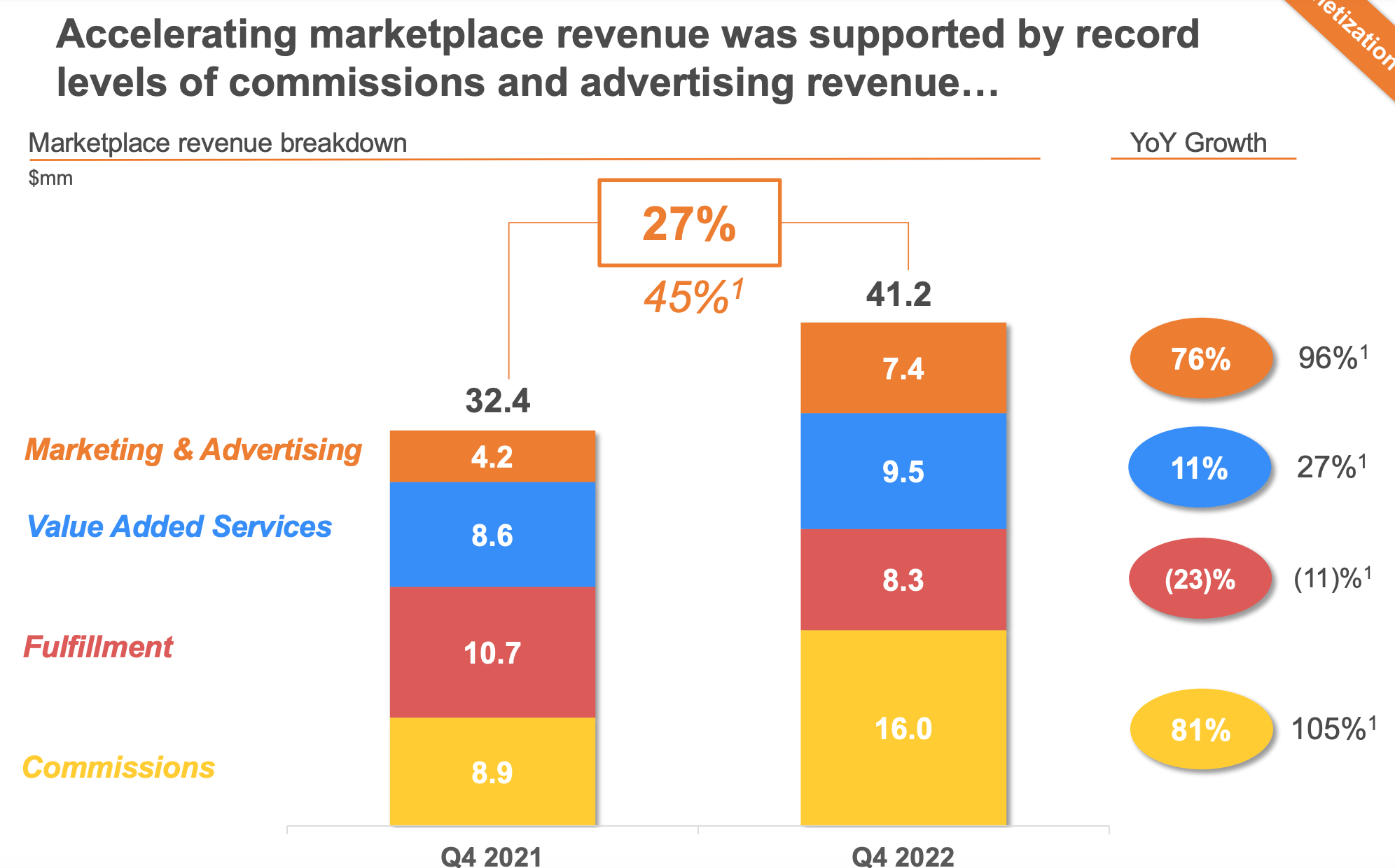

On that note, repositioning its fulfillment business will be a key operational efficiency lever. Jumia's reliance on an unprofitable fulfillment business segment as its largest source of revenue necessitates a reassessment of its positioning in this area. The management seems to have recognized this issue, as evidenced by the shrinking segment in Q4 and a notable reduction in fulfillment expenses. These actions indicate that management is taking steps to address the problem.

JumiaPay, on the other hand, presents a more promising long-term opportunity for the company. I continue to anticipate its business model transformation from simply a payment aggregator into an e-wallet business capable of storing customer and merchant balances on its own. The combination between that and Jumia Lending will form a financial services revenue stream (e.g. lending, payment fees, savings) that comes with higher margins and growth potential. Financial inclusion remains a critical topic in Africa, and with its strong presence in the e-commerce sector and +8 million active users, Jumia is well-positioned to address that problem. Starting with meeting the financing demand from its captive merchant ecosystem, Jumia could sustainably expand its services in this area.

Overall, I consider these catalysts to have the potential to shape Jumia's trajectory and drive its future growth. Monitoring the progress and execution of these initiatives will provide valuable insights into Jumia's ability to capitalize on these opportunities and create long-term value for investors - things that the company has been missing as of today.

Valuation/Pricing

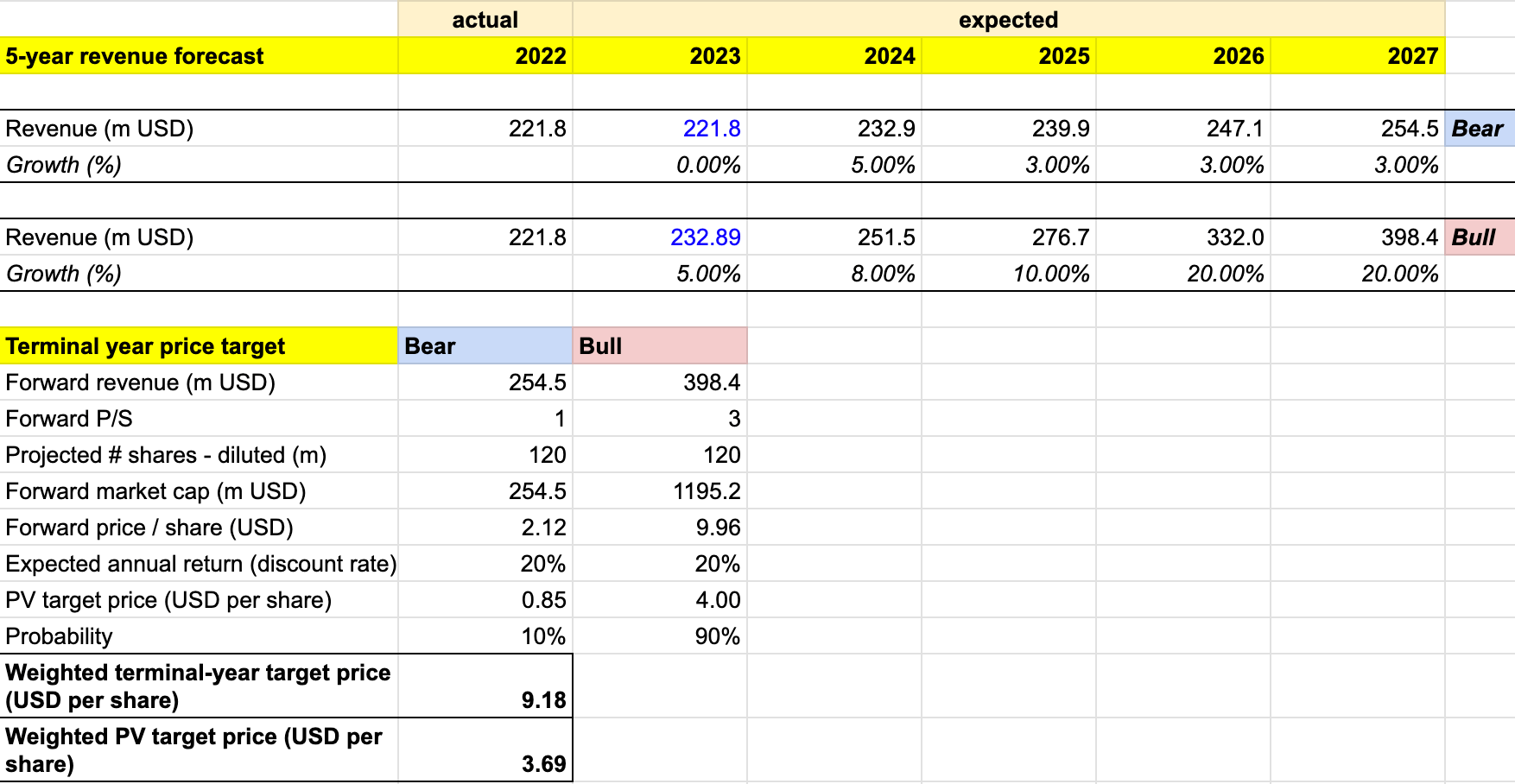

In estimating the price target for Jumia, I consider the following probability-weighted bull vs bear scenario-based 5-year revenue forecast:

-

Bull scenario (90% probability) - Given that Jumia will focus on operational restructuring to improve profitability in the near term and does not give FY 2023 revenue guidance, I choose to assign a revenue growth of 5% for FY 2023. As a comparison, Jumia experienced a 7% revenue growth while undergoing a major operational efficiency plan under the new CEO in Q4. I would expect Jumia to do more aggressive cost-cutting in FY 2023 and FY 2024, resulting in a 5% and 8% growth respectively. Growth will start accelerating under the new cost structure in FY 2025 onwards, with Jumia finishing FY 2027 as a 20% grower, driven by the transformation of JumiaPay into an e-wallet business in select geographic markets.

-

Bear scenario (10% probability) - Jumia to see highly aggressive cost-cutting measures that result in no growth in FY 2023. It continues to see constant challenges in growing the business under the new cost structure due to the difficult market. Initiatives with good fundamentals remain few in number, and growth continues to be difficult without promotional activities. Jumia to see 3% growth into FY 2027.

I assign a P/S of 3 for the bull scenario, implying a multiple expansion closer to the e-commerce industry P/S average due to improved growth and profitability outlook. For the bear scenario, I assign a P/S of 1, which means that Jumia's valuation is basically the same as its annual revenue. In this case, the bear scenario also represents a failure scenario for the business. In the model, I assume a 10% chance of that happening.

author's own analysis - target price model

{kind=link}

Consolidating all the information above into my model, I arrived at an FY 2027 weighted target price of +$9 per share in FY 2027. Discounting that target price with a 20% discount rate, I arrived at a Present Value/PV weighted target price of ~$3.7 per share. The 20% discount rate represents the expected annual return.

The ~$3.7 per share is the highest price point at which investors can purchase the stock to realize a projected 20% annual return if Jumia shares reach the FY 2027 target price of +$9. As Jumia currently trades below $3 per share, my model indicates that the stock is undervalued.

Conclusion

Despite the current decline in Jumia's stock price, which may attract some investors doing bottom fishing, and the fact that the stock is undervalued according to my model, I maintain a neutral stance on the stock.

I acknowledge that Jumia presents a long-term opportunity due to its first-mover advantage in capturing the growing consumer market in Africa. The recent management change and strategic initiatives, including product and geographic expansions, are expected to drive improvements, especially on profitability.

However, it is important to note that Jumia's financial outlook has remained underwhelming. Furthermore, I expect Jumia to continue facing operational complexities on its way to drive sustainable e-commerce growth in Africa. This raises concerns about the long-term commercial sustainability not only of the company itself but also of the market it operates in.

For further details see:

Jumia: There's Still A Lot Of Uncertainties