TLT - June CPI: Surprise Is Less Than Meets The Eye But Disinflation Trend Intact

2023-07-12 10:20:34 ET

Summary

- We summarize key data and provide an in-depth analysis of the monthly Consumer Price Index report released by the U.S. Bureau of Labor Statistics.

- Both All Items and Core CPI fell short of expectations.

- Today's positive CPI numbers were entirely due to volatile components which are not reliable indicators of longer-term trends.

- Our overall CPI outlook remains positive, with constructive implications for the economy and markets.

Summary Data and Analysis

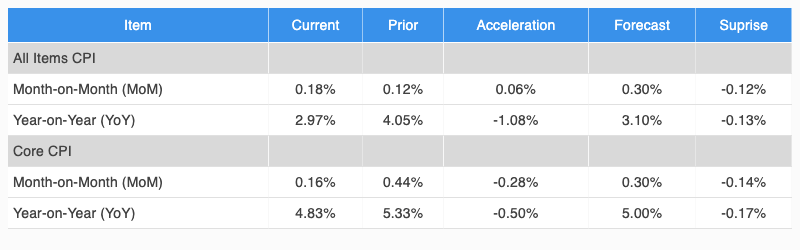

A summary of key data and analysis for this month's CPI report is provided in Figure 1.

Figure 1: Change, Acceleration, Expectations, and Surprise

Core & All Items CPI (BLS, Investor Acumen)

{kind=link}

All-Items CPI accelerated slightly on a MoM basis, but was below expectations. Core CPI deaccelerated on a MoM basis and surprised to the downside.

Analysis of Core and Non-Core Plus Key Sub-Components

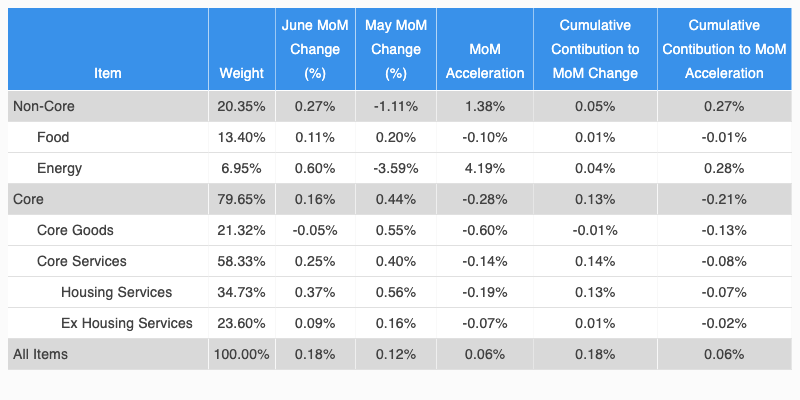

In Figure 2, we break down the analysis of change and acceleration of CPI into Non-Core and Core components. We further analyze two key subcomponents of non-core CPI and three key subcomponents of core CPI. Although all five columns in the table provide important information, we recommend that readers pay special attention to the rightmost column (Cumulative Contribution to Acceleration), as it reveals exactly what drove the MoM acceleration/deceleration in CPI during the current month compared to the prior month.

Figure 2: Analysis of Key Aggregate Components of CPI

Aggregate CPI Component Analysis (BLS, Investor Acumen)

{kind=link}

As can be seen in the table above, Energy accelerated significantly, accounting for most of the overall acceleration in All Items CPI. Yet every other major category deaccelerated.

Core Services except Housing - the indicator the Fed is currently paying most attention to - deaccelerated slightly and has been running at an annualized rate of less than 2.0%.

We now proceed to analyze the CPI report in greater depth. For more detailed information on how to read and interpret the tables and graphs in this article, please see the following Seeking Alpha blog post .

Contributions to Monthly Change in Core CPI

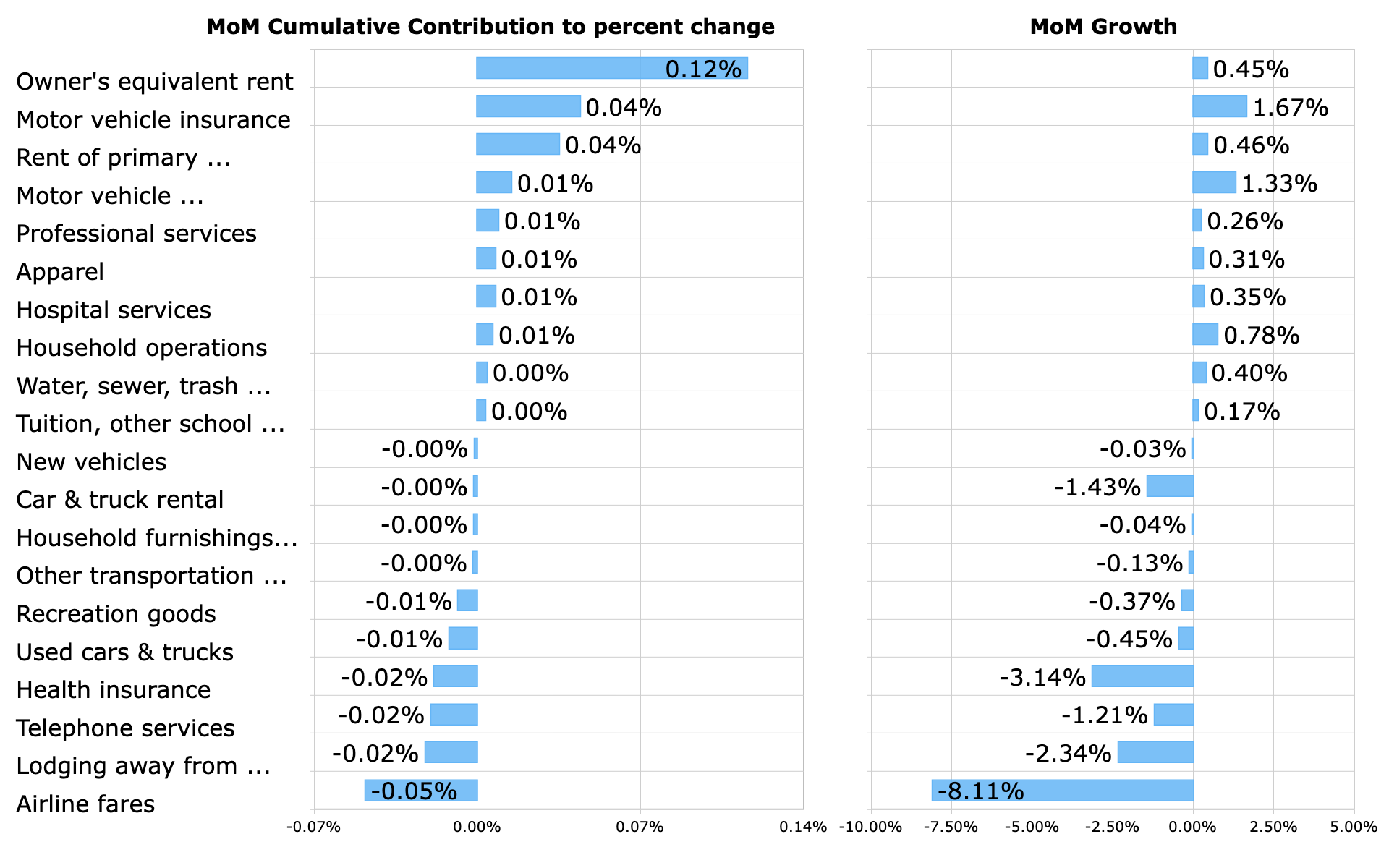

In Figure 3, we provide a bar chart that highlights the major positive and negative contributors to the MoM percent change in Core CPI. These contributions take into account both the magnitude of the MoM change in each component as well as the weight of each component in CPI.

Figure 3: Top Contributors to MoM Percent Change

Top CPI Contributors (BLS, Investor Acumen)

{kind=link}

Once again Owner's Equivalent Rent was the most important positive contributor to the monthly change in CPI. However, in this month Used Cars & Trucks contributed negatively to the monthly change in CPI after being a large positive contributor for multiple months. Real-time indicators suggest that this trend in the used car market may continue.

Most importantly, it should be noted that real-time indicators suggest that there will be significant disinflation in the housing components of CPI for the remainder of 2023.

Contributions to Monthly Acceleration in Core CPI

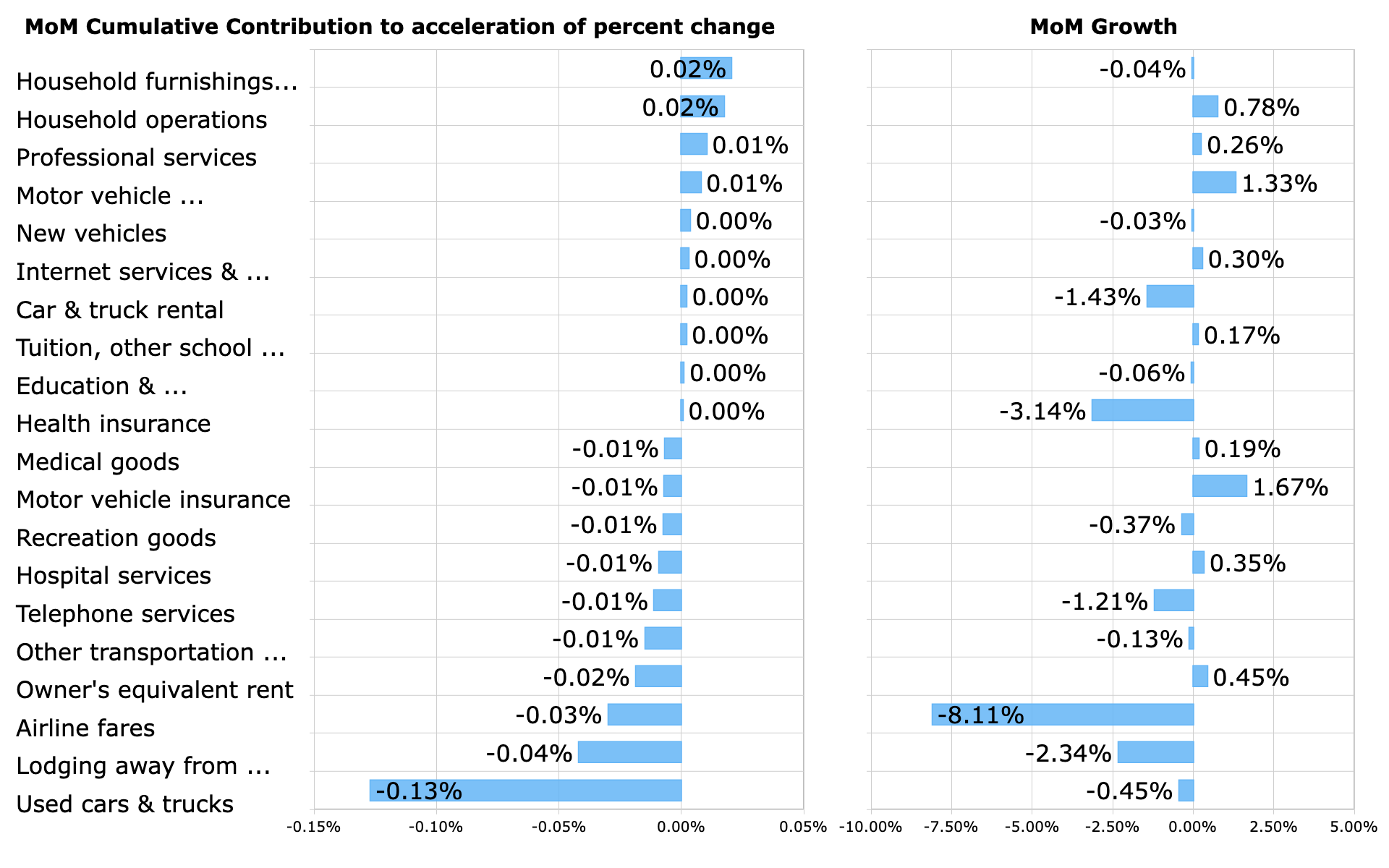

In Figure 4, we provide a bar chart that highlights the major positive and negative contributors to the MoM acceleration in Core CPI. These contributions take into account both the magnitude of the MoM accelerations in the components as well as the weight of each component in CPI.

Figure 4: Top Contributors to MoM Acceleration

Top CPI Acceleration Contributors (BLS, Investor Acumen)

{kind=link}

It's worthwhile to examine this table carefully, as it's likely to include most or all of the items that caused deviations from forecasters' expectations of Core CPI.

The most notable change is the massive contribution to deacceleration from Used Cars & Trucks. This is a volatile item and so its importance should be somewhat discounted. Airfares and Lodging Away From Home are also volatile components, which pushed core CPI down.

Excluding the impact of the three extremely volatile components above, core CPI would have actually registered above expectations, rather than below expectations. While volatile components obviously "count," they are not reliable indicators of the trend of inflation on an intermediate or longer-term basis.

For the complete breakdown, please see the following CPI Breakdown table posted on our site each month.

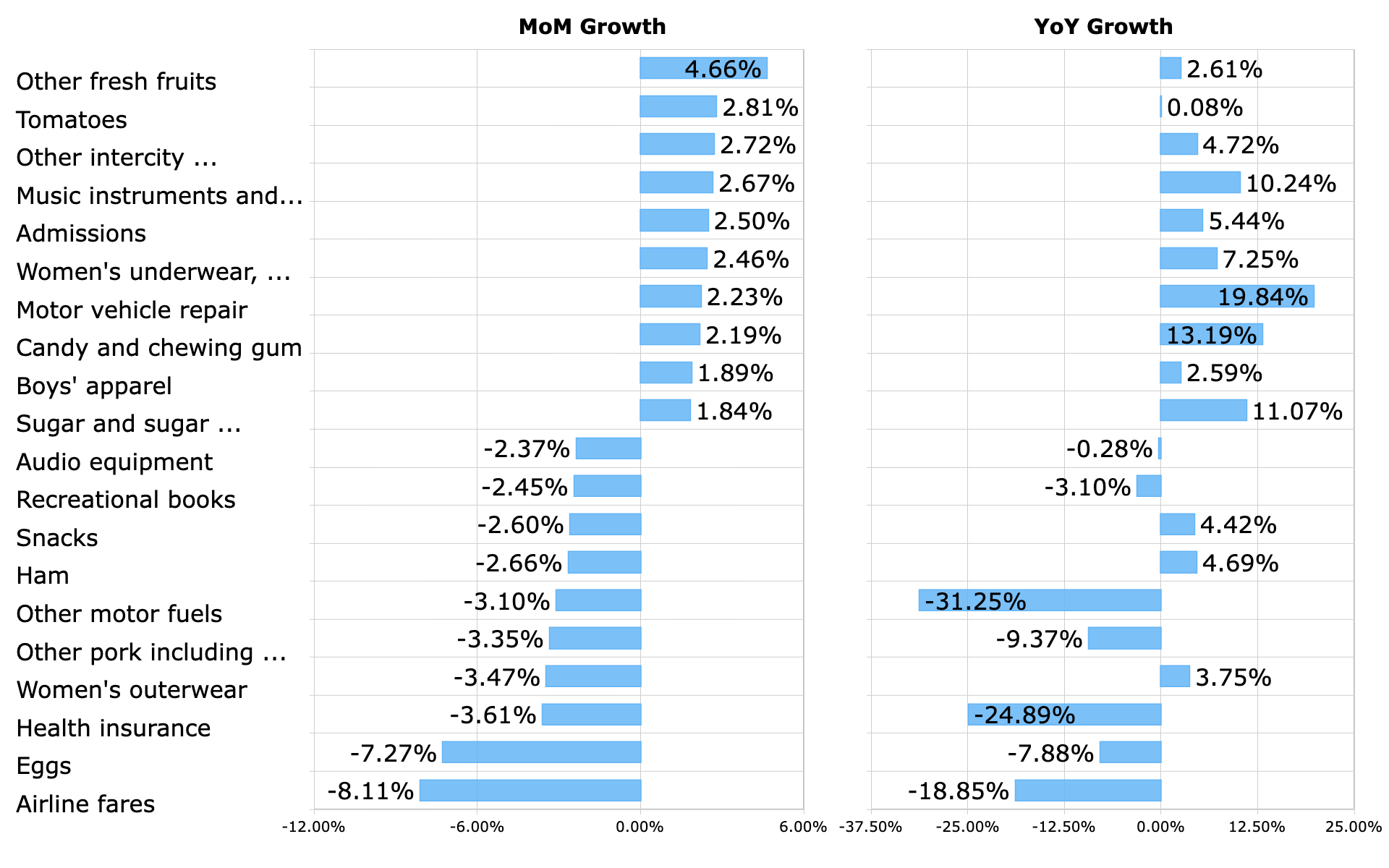

Top Movers

For general interest purposes, in Figure 5 we highlight the CPI components (most granular level) that exhibited the largest positive and negative change during the month. The YoY change in these particular components is displayed to the right.

Figure 5: Top Movers MoM Percent Change

Top CPI Movers (BLS, Investor Acumen)

{kind=link}

In June, Other Fresh Fruits registered the largest price increase. Egg prices continue to collapse, after experiencing a prolonged period of high inflation. Airline fares saw the largest MoM decline in prices this month.

Implications for the Economic Outlook

The fact that overall inflation and core inflation are deaccelerating is very good news for the economy as it takes pressure off of the Fed. Having said that, the Fed needs to be careful. First, deacceleration this month was entirely due to volatile components that are typically not indicative of the medium and longer-term trend. Secondly, with labor market conditions extremely tight, there is a risk that inflationary pressures could reignite at any time. This is particularly true if food and/or energy prices were to experience a surge.

We have been saying for several months that the US would be experiencing disinflation for most of the rest of 2023. This continues to be our base-case outlook. However, a case could be made that the Fed should consider taking out some "insurance" in the form of another rate hike, given the tightness of conditions in the labor market.

Implications for Financial Markets

Inflation has ceased to be a major source of risk for markets. Only a "shock" in energy or food prices could re-kindle inflationary risk. Unless and until such a shock emerges financial markets should benefit from the lack of inflationary risks to the outlook.

The overall inflation outlook is currently a positive for markets.

In the short-term, we feel that an overly positive reaction to today's report is probably not be warranted given that the numbers were not particularly positive excluding several highly volatile items (e.g., used cars, air fares, lodging away from home). In this specific context, we would not be surprised if some of the early post-CPI gains were reversed.

For further details see:

June CPI: Surprise Is Less Than Meets The Eye, But Disinflation Trend Intact