CA - Karora Resources: A Strong Start To 2023

2023-05-26 18:02:36 ET

Summary

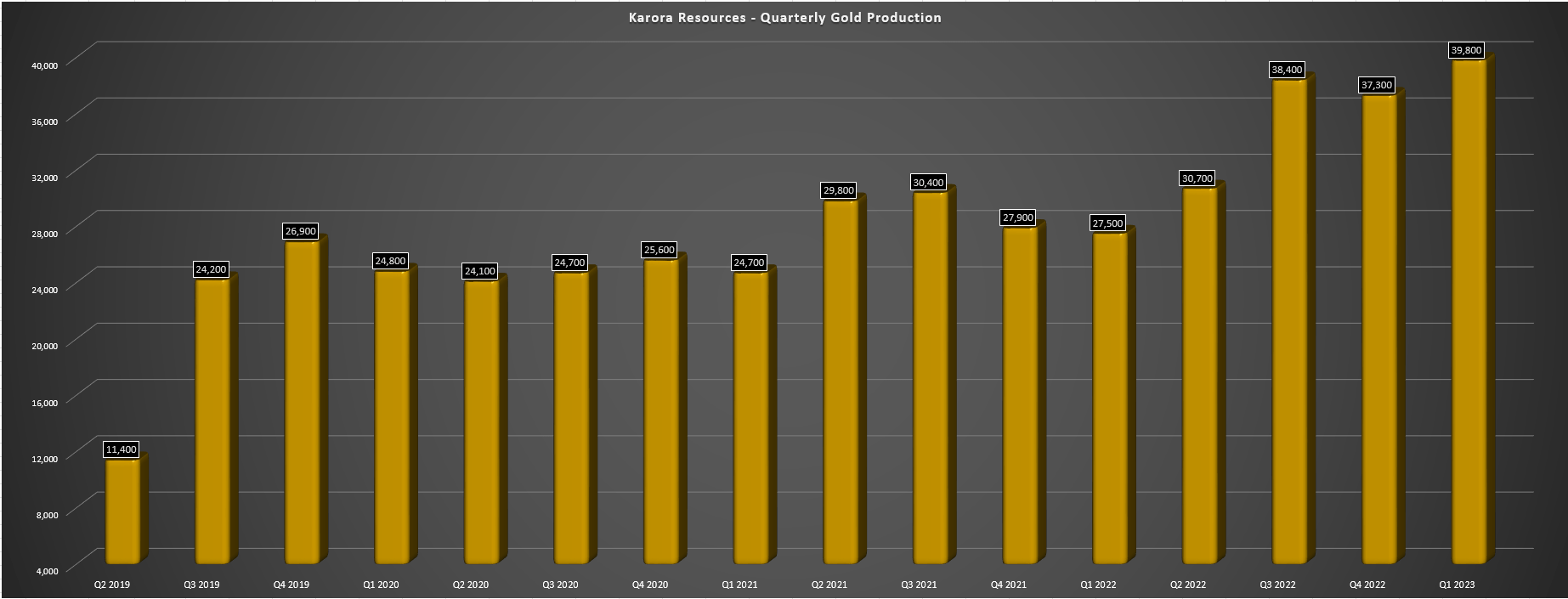

- Karora Resources released its Q1 results earlier this month, reporting quarterly production of ~39,800 ounces of gold, trouncing its previous record of ~38,400 ounces by nearly 4%.

- The strong performance was driven by increased tonnes milled and higher grades at Beta Hunt and Higginsville, and the benefit of an additional mill, where ~121,000 tonnes were processed.

- Given the increased production at lower costs, Karora generated significant cash flow and maintained its strong balance sheet during its growth phase, with higher margins expected during H2.

- With Karora being a fully funded organic growth story with a combination of materially higher output and margin expansion, I continue to see it as a top-15 producer sector-wide.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) has finally ended, and it was a mixed earnings season overall. This is because while production was flat to up for most producers, unit costs were up as well, hit by higher fuel prices, higher labor costs, and increases in some consumables. Combined with a flat average realized gold price year-over-year, we saw continued margin compression (Q1 2023. vs Q1 2022), and most companies struggled to generate any meaningful free cash flow. Fortunately, Karora Resources ( KRRGF ) was an exception, with record production, near-record revenue, and a significant improvement in cash flow year-over-year. Plus, the Beta Hunt #2 decline was completed on budget/schedule. Let's take a look at the Q1 results below.

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q1 Production & Sales

Karora Resources released its Q1 results last week, reporting quarterly gold production of ~39,800 ounces, a 45% increase from the year-ago period, and above budgeted levels. The sharp increase in production was driven by a 27% increase in tonnes milled to ~502,000 tonnes, with a higher average feed grade benefiting from better grades at both Beta Hunt and its Higginsville operations. Meanwhile, nickel production increased significantly, with ~7,300 tonnes of nickel mined at 2.22%, up from ~5,200 tonnes at 2.13% in the year-ago period. Finally, tonnes mined were also up sharply at Beta Hunt, with ~300,000 tonnes mined at 2.81 grams per tonne of gold, with mining on A Zone 17 Level responsible for the significantly better grades.

Karora Resources - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

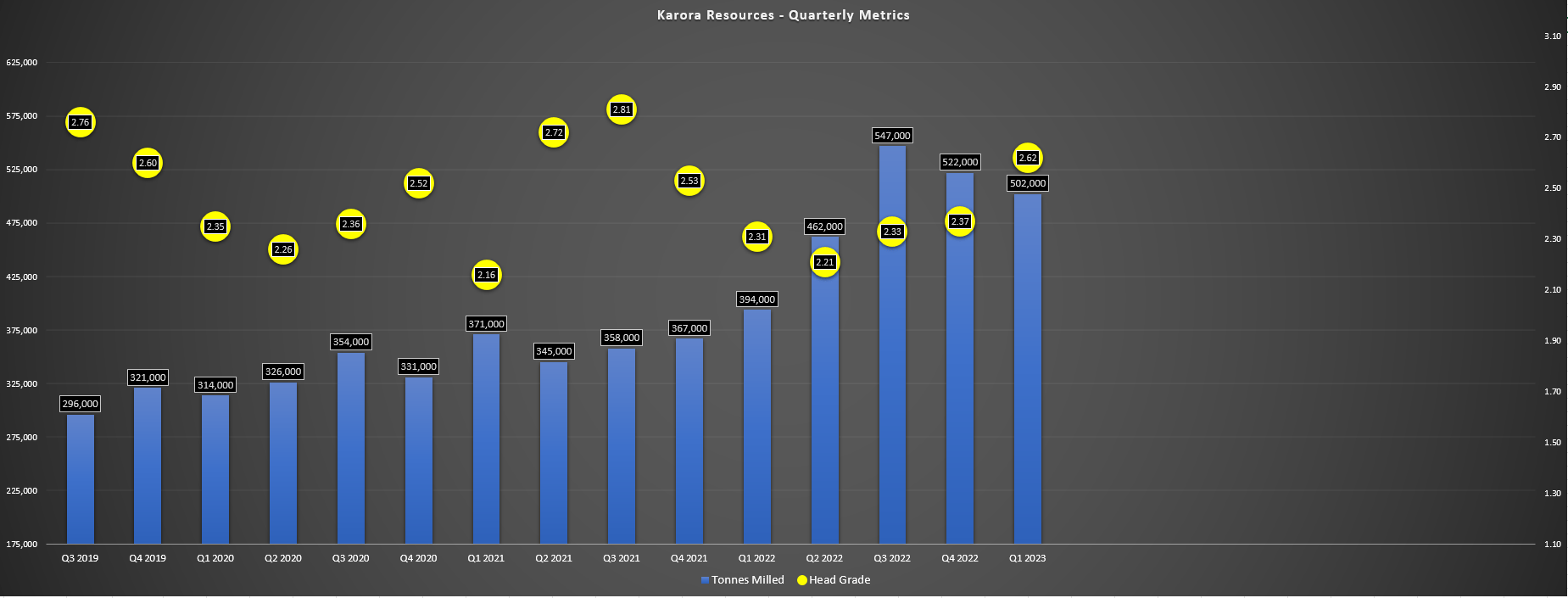

Looking at the chart above, trailing twelve-month production is now sitting at ~146,200 ounces, and annualized production is sitting just shy of ~160,000 ounces, tracking at the top end of the company's FY2023 guidance. This is a considerable improvement from Q1 2022 levels (trailing twelve-month gold production of ~115,600 ounces. As we can see below, the significant increase in gold production can be attributed to higher tonnes processed and higher grades, with ~502,000 tonnes processed in Q1 2023, up from ~394,000 tonnes in the year-ago period at 2.31 grams per tonne of gold. This has been helped by less reliance on stockpiles with an improved labor situation and the addition of a second mill (Lakewood), allowing the company to process well over 2.0 million tonnes on an annualized basis in Q1 2023.

Karora - Quarterly Operating Metrics (Company Filings, Author's Chart)

{kind=link}

Looking at the separate operations, Karora processed ~298,000 tonnes at 2.92 grams per tonne of gold at its flagship Beta Hunt Mine, translating to ~26,600 ounces of gold, which was up 55% year-over-year. This was related to significantly higher grades and tonnes processed, with ~121,000 tonnes processed at Lakewood with an 87%/13% Beta Hunt/Higginsville split for feed. Meanwhile, although fewer tonnes were mined from Higginsville (~72,200 tonnes at 3.85 grams per tonne of gold), Karora noted that this was related to the cessation of open-pit mining at Spargos and delayed development of the Mouse Hollow open pit. And while there are no guarantees, planning is underway for an underground operation at Spargos, providing another high-grade feed source for its upgraded milling capacity (2.6 million tonnes per annum combined with Lakewood and Higginsville).

Costs & Margins

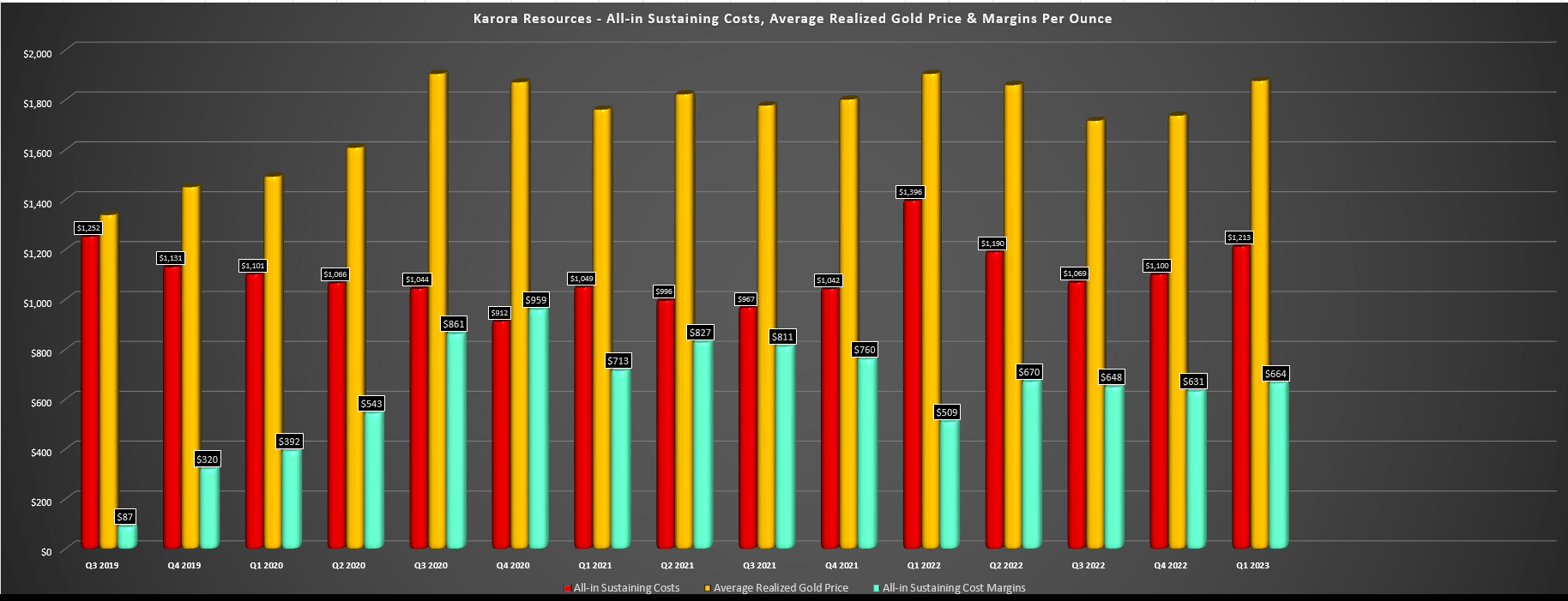

Moving over to costs and margins, Karora reported cash costs of $1,124/oz in Q1 and all-in sustaining costs (AISC) of $1,213/oz, which were both significant improvements from $1,310/oz and $1,396/oz in the year-ago period, respectively. So, despite a lower average realized gold price of $1,877/oz in Q1 and similar levels of by-product credits, AISC margins improved to $664/oz from $509/oz in Q1 2022, with increased G&A expenses offset by lower sustaining capital and higher sales volumes. That said, this significant increase in margins was primarily because of being up against easy year-over-year comps, with Q1 2022 being a very rough quarter for the company with record COVID-19 cases which resulted in labor availability reaching a low of 60% with increased reliance on contract labor and we also saw supply chain headwinds. This doesn't take away from the strong Q1 results, but relative to a more normal quarter like Q1 2021, AISC margins fell 7%.

Karora Resources - AISC, Average Realized Gold Price, AISC Margins (Company Filings, Author's Chart)

{kind=link}

The good news is that fuel prices have continued to trend lower in Q2 and some Australian producers have noted that they're seeing an improvement in the labor situation. Second, the gold price is higher and has averaged $1,980/oz quarter-to-date, providing some tailwind for margins. However, this could be partially offset by sustaining capital tracking well behind guidance year-to-date and nickel prices declining sharply since the end of Q1. That said, while I don't expect a big beat on Karora's AISC guidance midpoint of $1,175/oz, a slight beat looks possible ($1,165/oz), and assuming an average realized gold price of $1,900/oz for 2023, we would see annual AISC margins improve from $735 from $622/oz, with the potential for AISC margins to climb back towards $800/oz in FY2024 using a $1,900/oz gold price assumption.

Karora Resources - Quarterly Revenue & Operating Cash Flow (Company Filings, Author's Chart)

{kind=link}

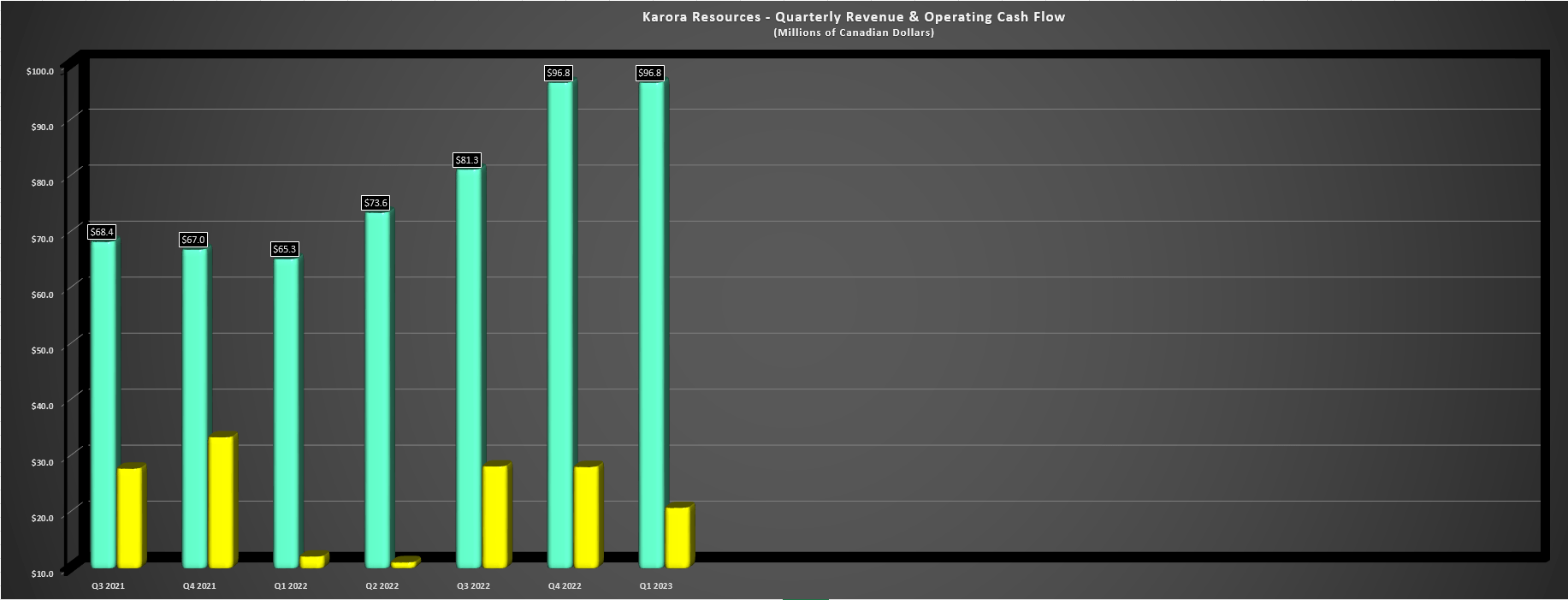

Finally, looking at Karora's financial results, quarterly revenue tied its previous record reached in Q4 2022 of C$96.8 million, and operating cash flow came in at C$20.9 million, up from C$12.2 million in the year-ago period. The increase was driven by a significant increase in ounces sold and slightly better margins, and this was despite unfavorable changes in working capital. Prior to changes in working capital, Q1 cash flow came in at C$28.6 million. After subtracting out C$19.8 million in investment in the period and lease and interest payments, the company saw minimal cash burn in the period and ended the quarter with C$65.9 million in cash (Q4 2022: C$68.8 million).

Recent Developments

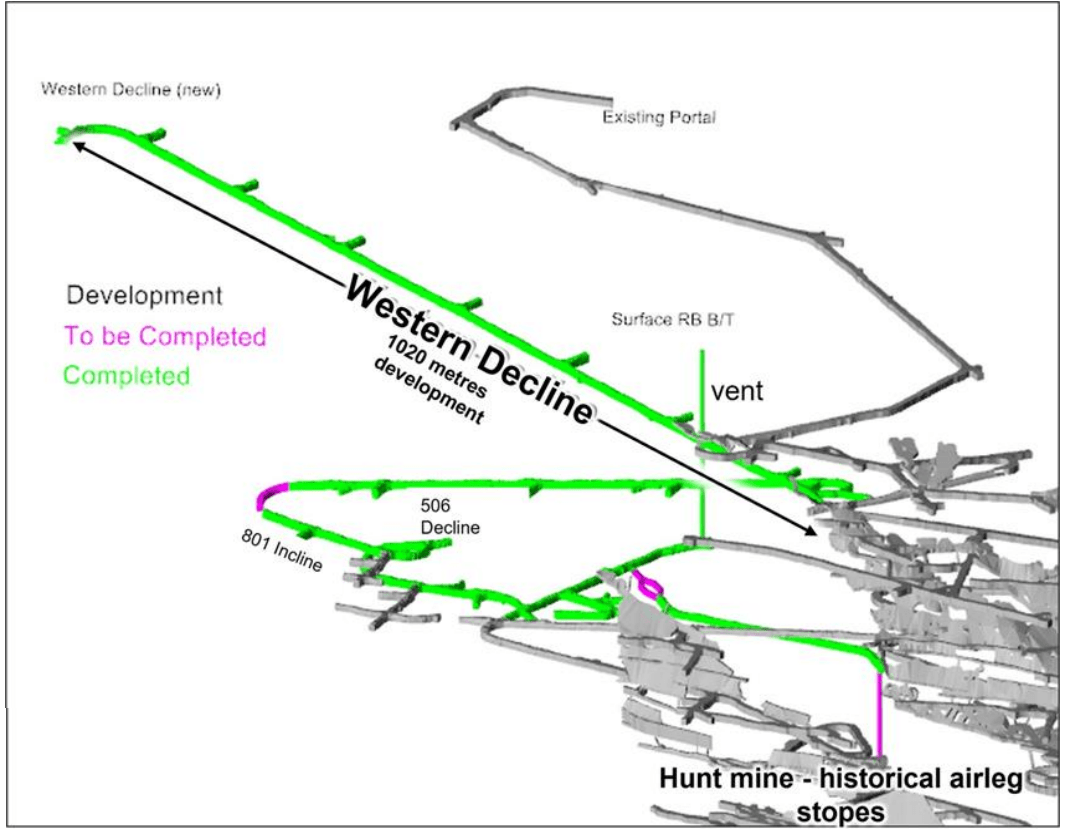

Finally, looking at recent developments, Karora noted it completed its second decline on schedule and budget, in addition to its first of three vent shafts, a commendable feat given the inflationary pressures that have led to double-digit cost revisions at several projects globally, including Tanami in the Northern Territory. This is a key development regarding delivering on its growth plan to increase Beta Hunt mine production to 2.0+ million tonnes per annum and growing company-wide production to 190,000+ ounces per year. The next key item to deliver this growth is the installation of two more vent raises and increased mine development. Karora noted that the third ventilation raise is expected to be completed in H2, with a goal of a 2.0 million tonne per annum production rate (annualized basis) next year.

{kind=link}

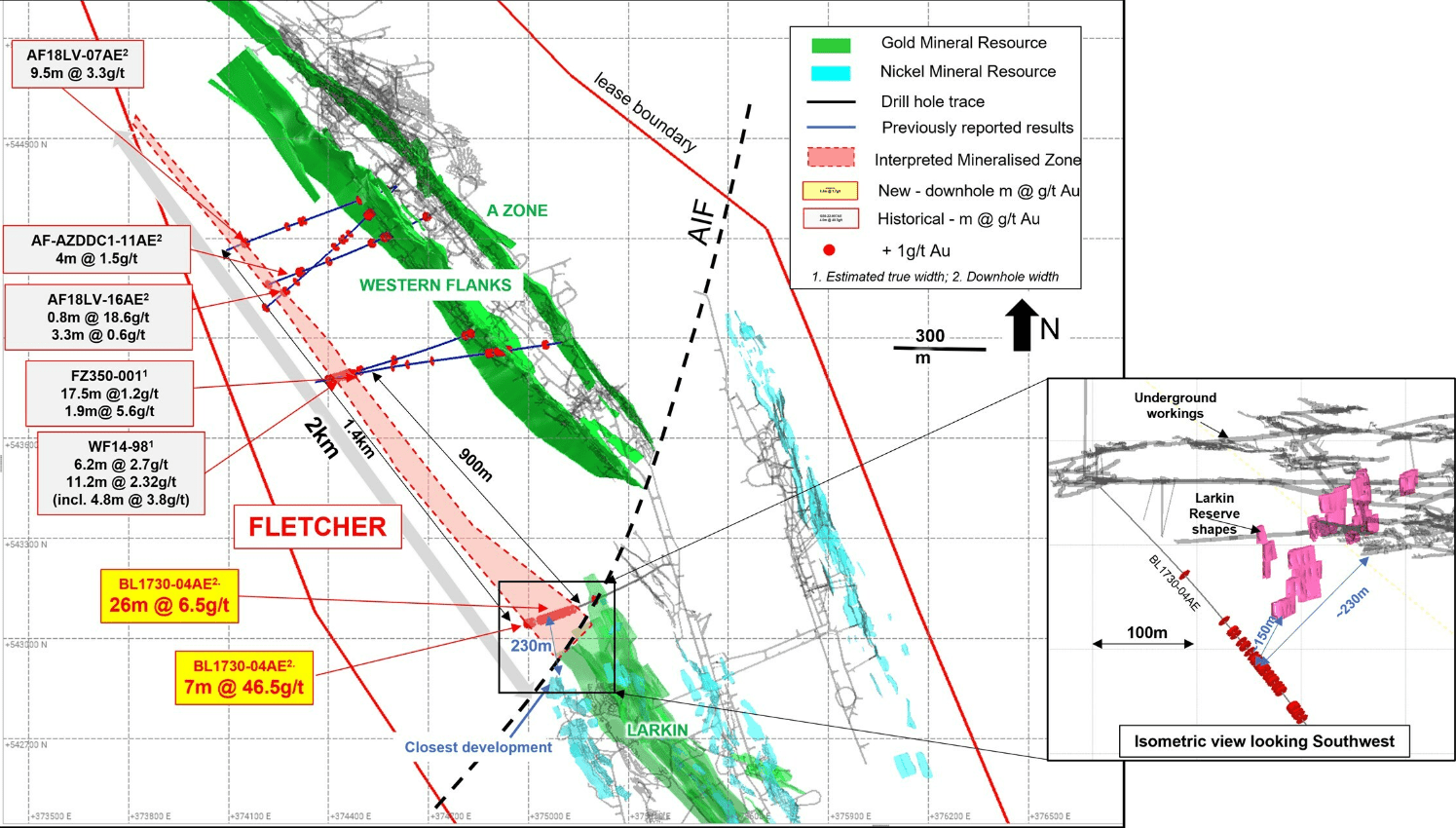

Meanwhile, from an exploration standpoint, Karora's drilling results continue to be quite encouraging, with Karora intersecting 7.0 meters at 46.5 grams per tonne of gold and 26 meters at 6.5 grams per tonne of gold at the southern end of the Fletcher Shear Zone ((FSZ)). Not only are these grades well above average reserve grades over thick intercepts (pointing to resource growth), but they have nearly tripled the strike extent of the FSZ to 1.4 kilometers, and this gold system runs directly parallel to the Western Flanks Zone and just north of the Alpha Island Fault. And while there's no guarantee we see these elevated grades continue, the grades and thicknesses are exceptional relative to previous results drilled along the FSZ (9.5 meters at 3.3 grams per tonne of gold, 0.80 meters of 18.6 grams per tonne of gold). So, with this new discovery being near existing infrastructure, this is an exciting development.

{kind=link}

Elsewhere at Beta Hunt, the Mason and Cowcill zones continue to yield solid results, as do Western Flanks Deep and A Zone North. As discussed by the company in a January release, Karora intersected 11.9 meters at 3.3 grams per tonne of gold and 4.9 meters at 4.4 grams per tonne of gold at Cowcill, and highlight intercepts of 11.0 meters at 5.4 grams per tonne of gold, 23.0 meters of 3.3 grams per tonne of gold, and 11.0 meters at 44.4 grams per tonne of gold at Mason. These hits were overestimated true widths, potentially increasing the strike length at Mason and likely resulting in increased resources east and west of Larkin, which is home to ~1.71 million tonnes at 2.4 grams per tonne of gold (~131,000 ounces).

At Western Flanks Deep, Karora hit 7.1 meters at 9.5 grams per tonne of gold and 6.0 meters at 3.0 grams per tonne of gold, plus 9.0 meters at 6.6 grams per tonne of gold and 6.0 meters at 5.3 grams per tonne of gold at A Zone/A Zone Deeps Central. Similar to drilling at the FSZ, these exploration results suggest potential resource growth below the current mineral resource. And while some investors might have thought Karora was a little ambitious to double mine production at Beta Hunt by constructing a second decline with a reserve base of just ~6.8 million tonnes (3.4 years at 2.0 million tonne per annum mining rate), exploration results certainly vindicate this decision, with the potential for this reserve base to ultimately grow to 900,000 ounces at Beta Hunt with new zones and extensions even after accounting for depletion.

Valuation

Based on ~181 million fully diluted shares and a share price of US$3.35, Karora trades at a market cap of US$606 million, well below its peak market cap of ~$1.06 billion in April 2022. That said, the stock never belonged at a $1.0 billion plus valuation given that it's a relatively small-scale producer, and as we learned from recent guidance and despite plans for increased nickel production (by-product benefit), inflationary pressures have derailed the previous plans for sub $950/oz AISC, and while Karora will still be one of the lowest-cost producers sector-wide post Beta Hunt expansion, it's tough to argue that the stock belongs above a $1.0 billion valuation as a ~190,000-ounce producer at $1,150/oz AISC, especially when looking at where some peers trade today.

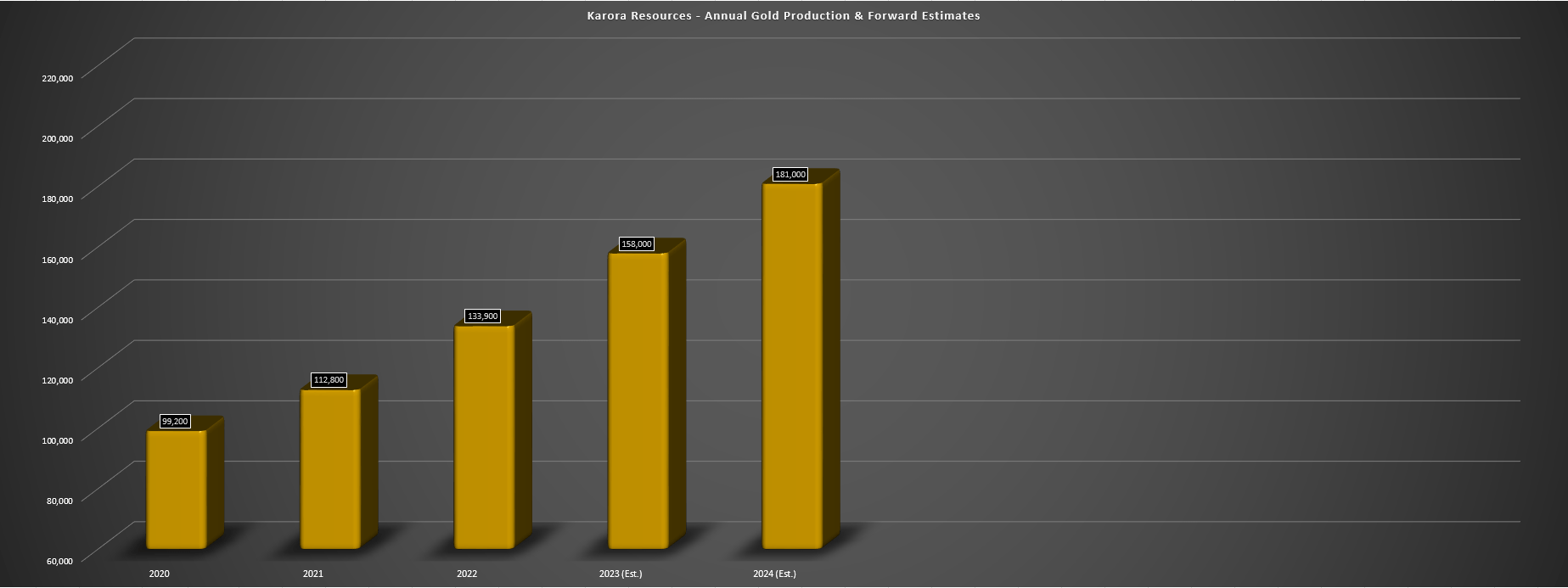

Karora - Annual Production & Forward Estimates (Company Filings, Author's Chart)

{kind=link}

Using what I believe to be a fair multiple of 7.0x cash flow and FY2024 cash flow estimates of $110 million (US$0.62 per share), I see a fair value for Karora of US$4.30, pointing to a 28% upside from current levels. While this makes Karora more undervalued than some gold producers that have enjoyed near-parabolic runs like Torex Gold ( TORXF ) and Lundin Gold ( LUGDF ) where I see limited upside, I prefer a minimum 40% discount to fair value to justify starting new positions in small-cap names. And after applying this discount to Karora's estimated fair value (7x FY2024 cash flow per share estimates), the ideal buy zone for the stock comes in at US$2.60 or lower, suggesting we've yet to move into a low-risk buy zone like we did in July 2022 . Hence, while I continue to see Karora as a top-15 name in the sector, I'm not in a rush to start a position just yet.

Summary

Karora had put together a phenomenal start to 2023, tracking ahead of its guidance midpoint (152,500 ounces at $1,175/oz) on output and costs, and set up to beat its guidance midpoint if it can continue this momentum throughout the year. From a bigger picture standpoint, Karora continues to be unique in the sense that it is growing production at higher margins with a fully funded growth plan, a profile that few producers boast currently, and with a team that has consistently delivered on its promises. That said, there are several other names also on the sale rack within the precious metals sector and the overall market and while Karora is cheap, it's not a screaming buy by any means at current levels. To summarize, while I would view pullbacks below US$2.80 as buying opportunities, I am focused elsewhere currently.

For further details see:

Karora Resources: A Strong Start To 2023