CA - Karora Resources: Beta Hunt Might Be A Beast

2023-10-25 08:19:56 ET

Summary

- Karora Resources is a rapidly growing gold producer in Australia with below-average AISC and a strong balance sheet.

- Karora is on track to hit its production guidance for the year and expects another record year of gold production in 2024.

- Beta Hunt might be a beast.

- The accuracy of the resource at Beta Hunt is the main risk, and there are unknowns about the renewal process for the Beta Hunt sub-lease.

There is a lot to like about Karora Resources (KRRGF). It's a rapidly growing gold producer in a good mining jurisdiction (Australia), AISC are below the industry average and costs will decline further as output increases, it has a strong balance sheet that is only getting better thanks to the cash flow generation, and management continues to deliver on targets and create shareholder value.

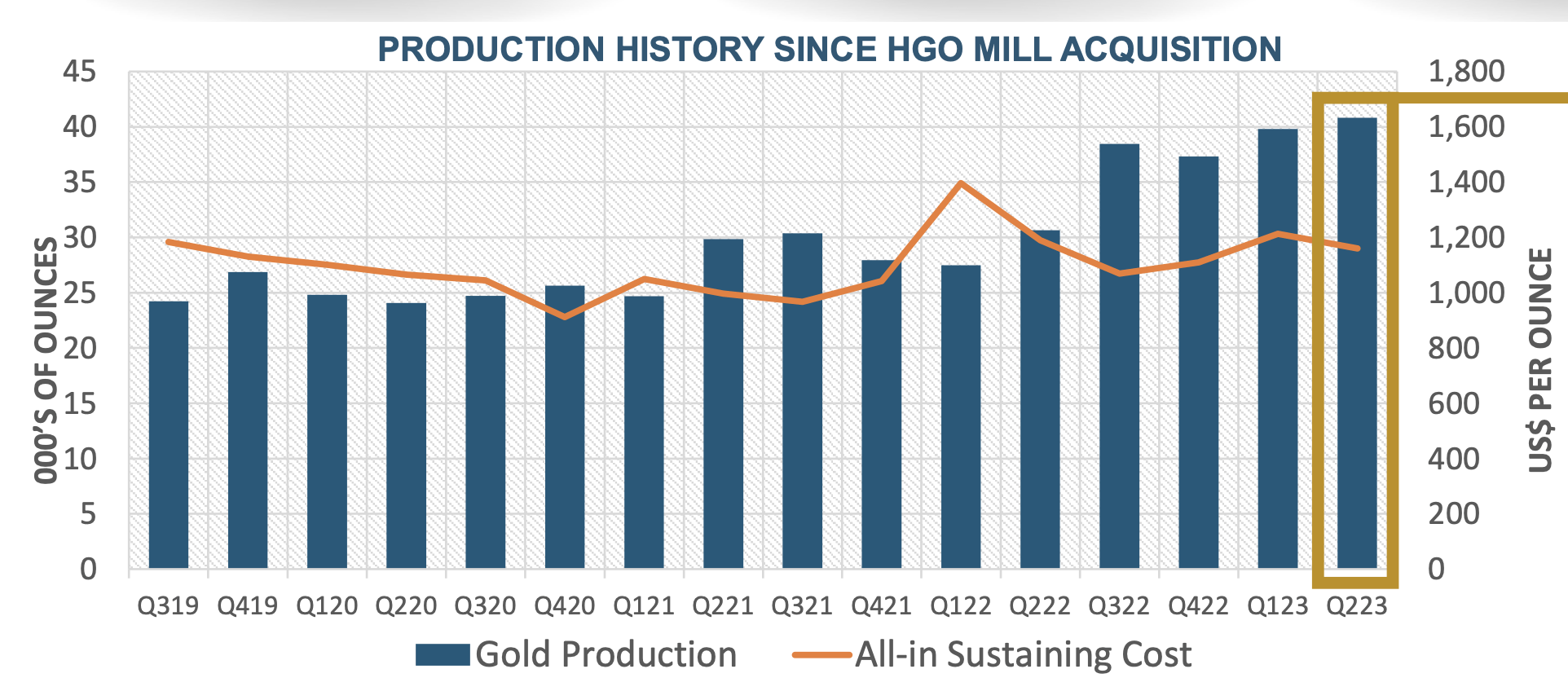

Two weeks ago, the company showed that it remains on this bullish path as it announced another solid quarter of gold production. In Q3 2023, its Beta Hunt and Higginsville mines produced 39,548 ounces of gold, which is just below the record quarterly gold production of 40,823 ounces in the prior quarter, which built on the record production set in the first quarter of the year.

{kind=link}

Karora also announced that its cash balance as of September 30, 2023, was C$84.2 million, which is an increase of C$13 million compared to the end of Q2 2023, as the mines are delivering strong free cash flow despite the increased capital spending to grow production.

KRRGF is in an exceptional financial position with ~C$45 million of net cash (debt was only a modest C$38.8 million at the end of the second quarter), growing production, and generating free cash flow even as it completes substantial upgrades to the underground infrastructure. The company will also receive ~C$30 million if the Dumont nickel project finds a buyer, which KRRGF expects could happen soon. Although Karora left a lot on the table if Dumont fetches a big sum. Still, that C$30 million would cover most of the debt.

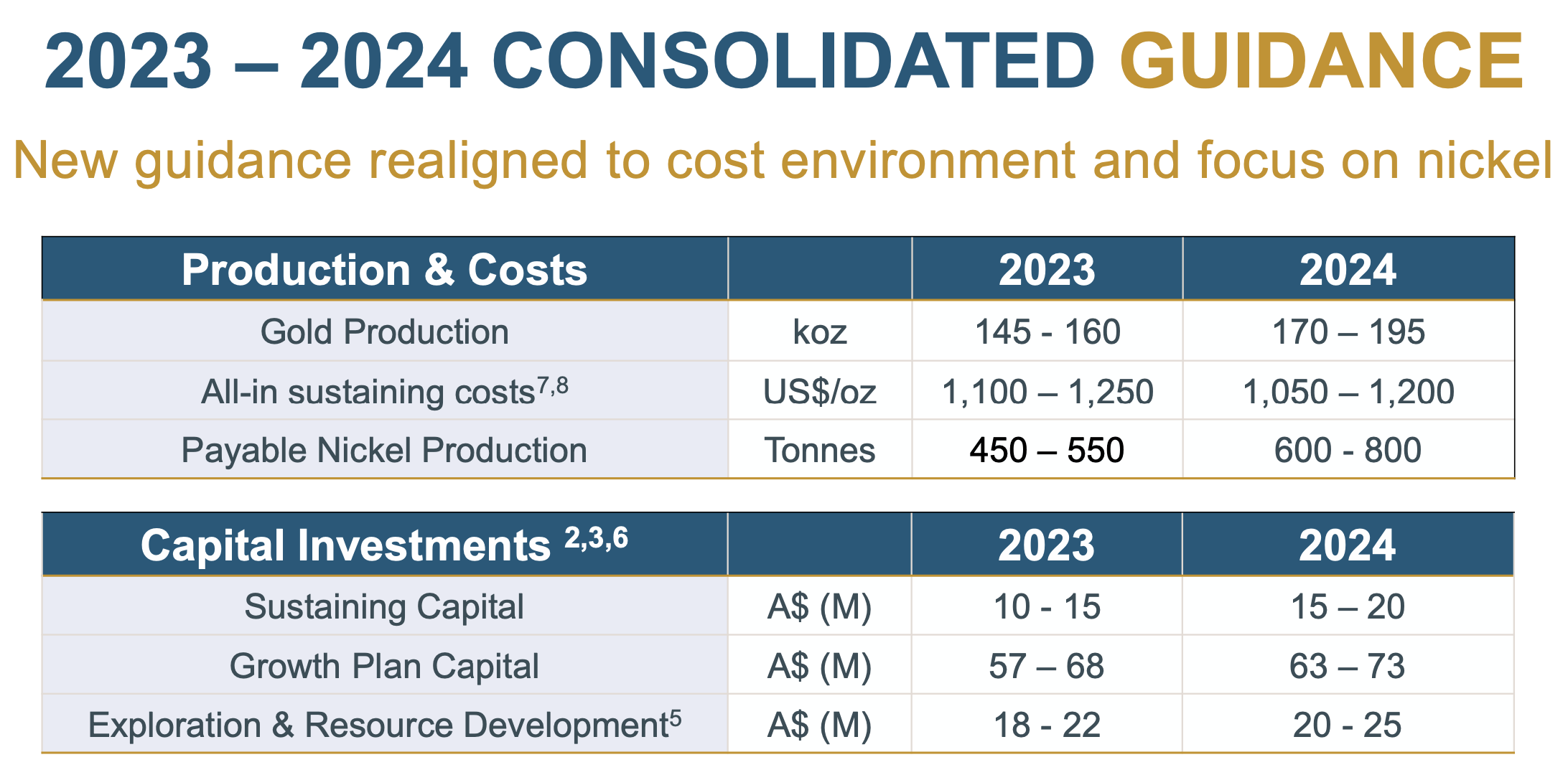

The company is on track to hit the top end of its production guidance range for the year and expects to deliver another record year of gold production in 2024, with estimates of 170,000-195,000 ounces. As reflected in the table, higher production (including nickel production) next year will reduce costs even further. While most producers are struggling to contain costs, and $1,000-$1,200 per ounce AISC is a thing of the past for many of Karora's peers, the company will see margin expansion and 1st quartile cost in 2024, assuming a stable gold price and it delivers on guidance.

{kind=link}

But there is much more to this story, especially on the exploration side and the untapped nickel resources.

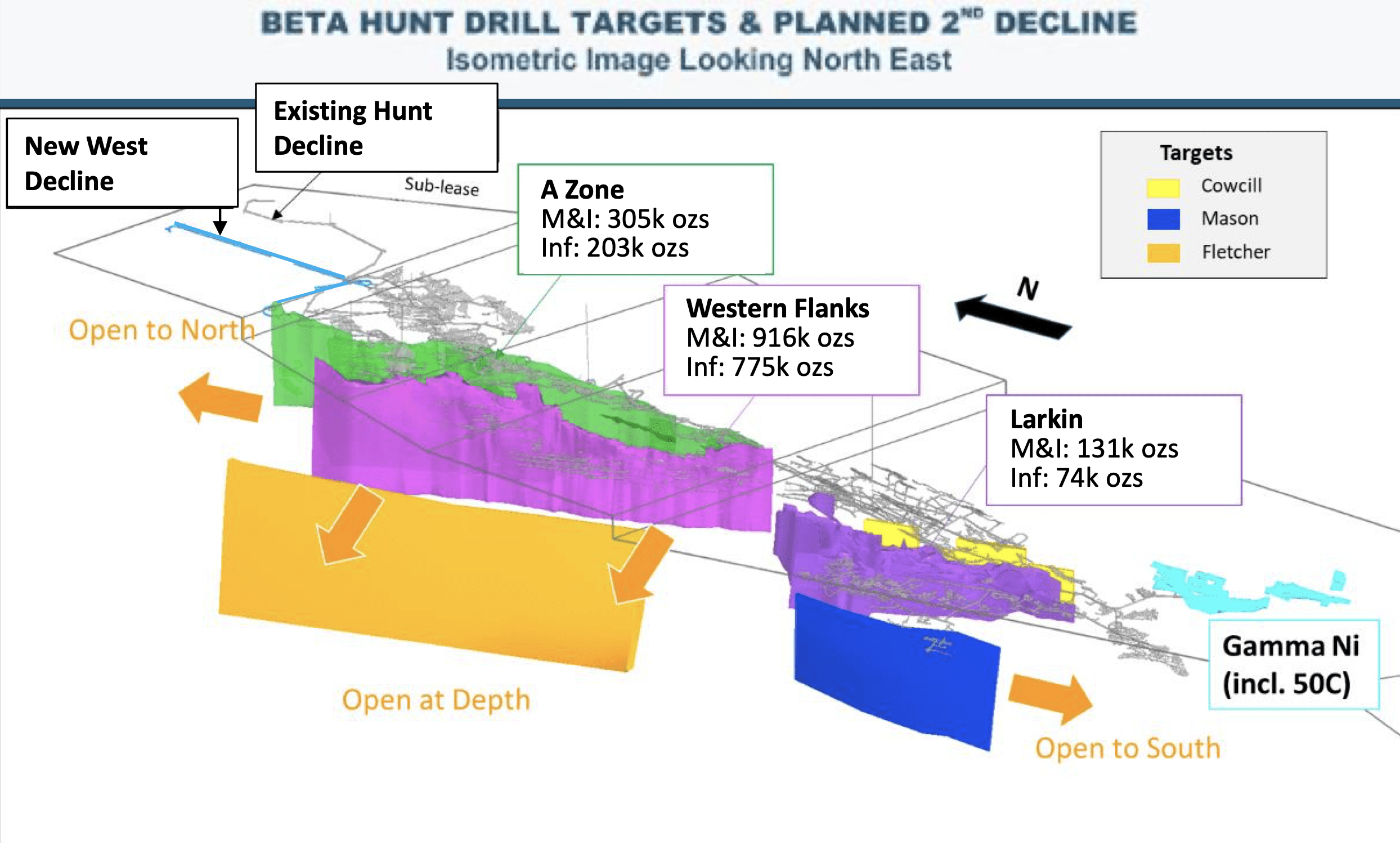

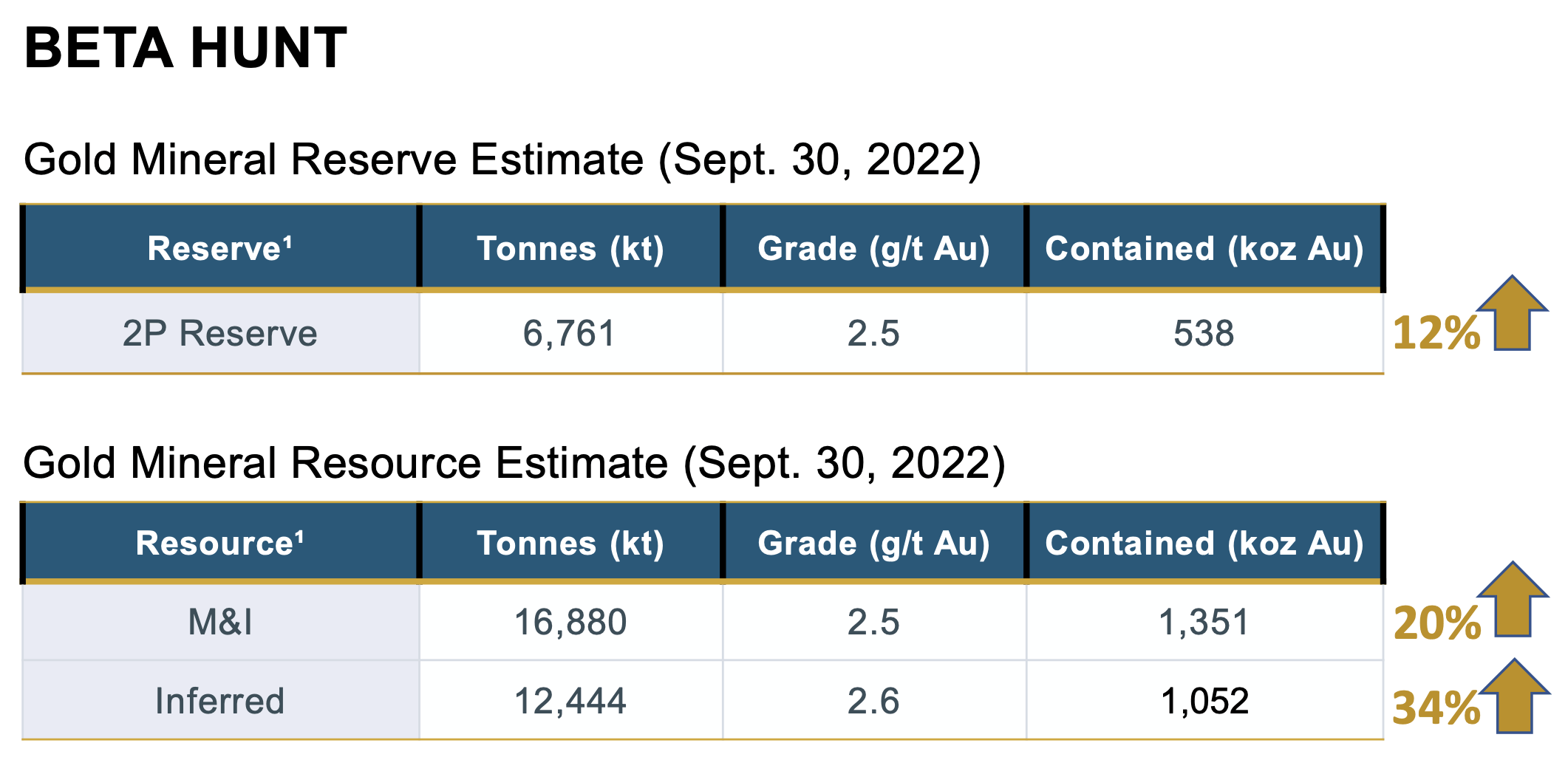

Beta Hunt has a long history of production, but it was mostly nickel. Over the last 5-6 years, gold resources have increased by 6x, or from ~400,000 ounces in 2017 to 2.4 million ounces as of last year. Karora has been drilling aggressively and proving that there is substantial gold exploration upside at Beta Hunt. What was once a nickel mine has turned into a gold mine. Karora is able to discover ounces quickly and get them into production just as fast, as there is over 400 km of underground development already in place, which the company claims would cost over A$2 billion at current development prices. You can see all of the underground workings in the diagram below, as well as the two shear zones currently being mined (A Zone and Western Flanks). The second decline (in blue at the top left) is also now complete.

{kind=link}

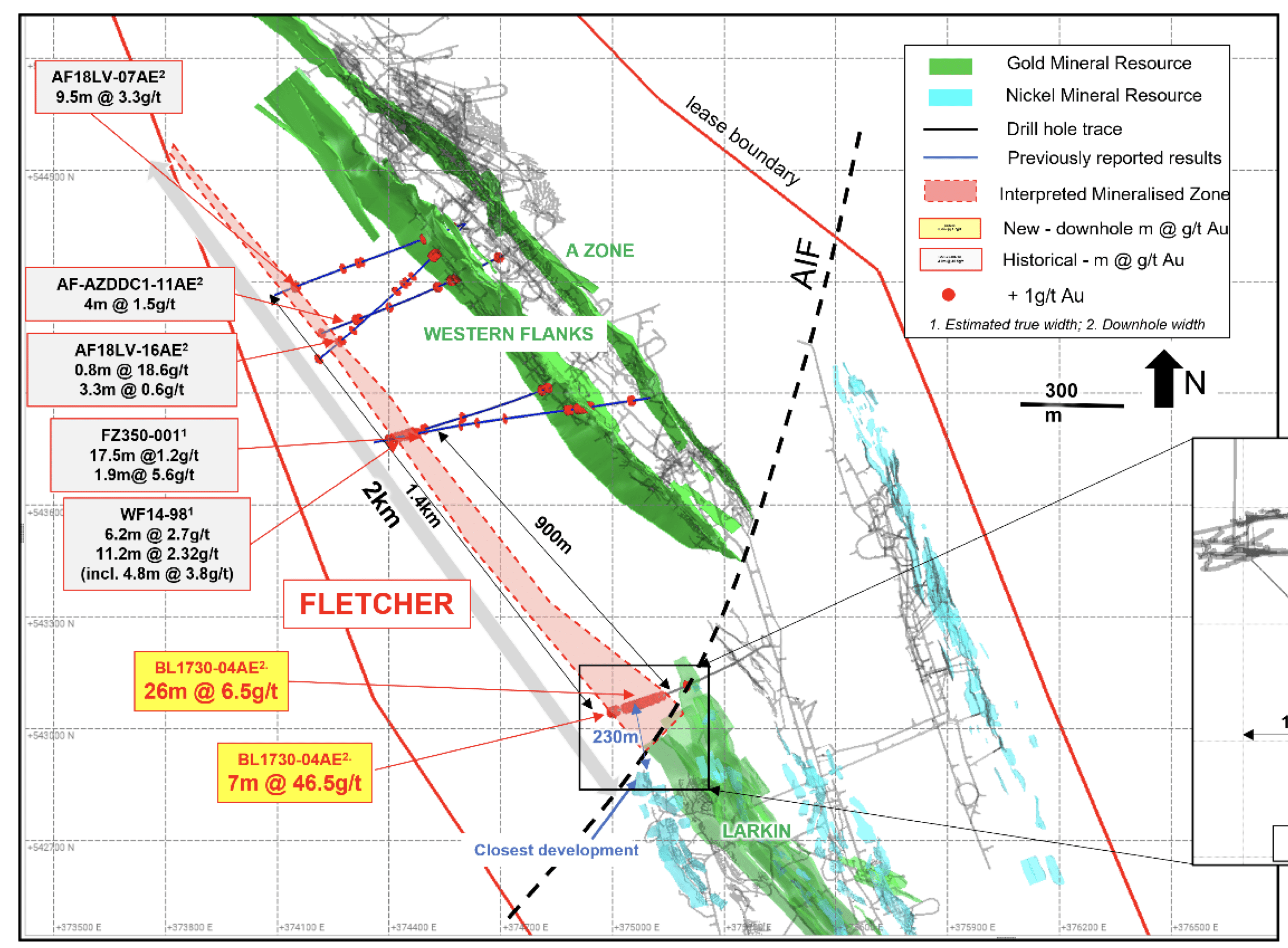

Karora has been constrained to mining on two shears but expects in the future it will mine on a number of shear zones and will be able to blend grades. This overhead diagram shows there are numerous other zones, including Fletcher, which runs parallel to the Western Flanks and A Zone. Also, notice the nickel resources in light blue in the Beta and Gamma Blocks, which I will discuss in more detail in a bit.

{kind=link}

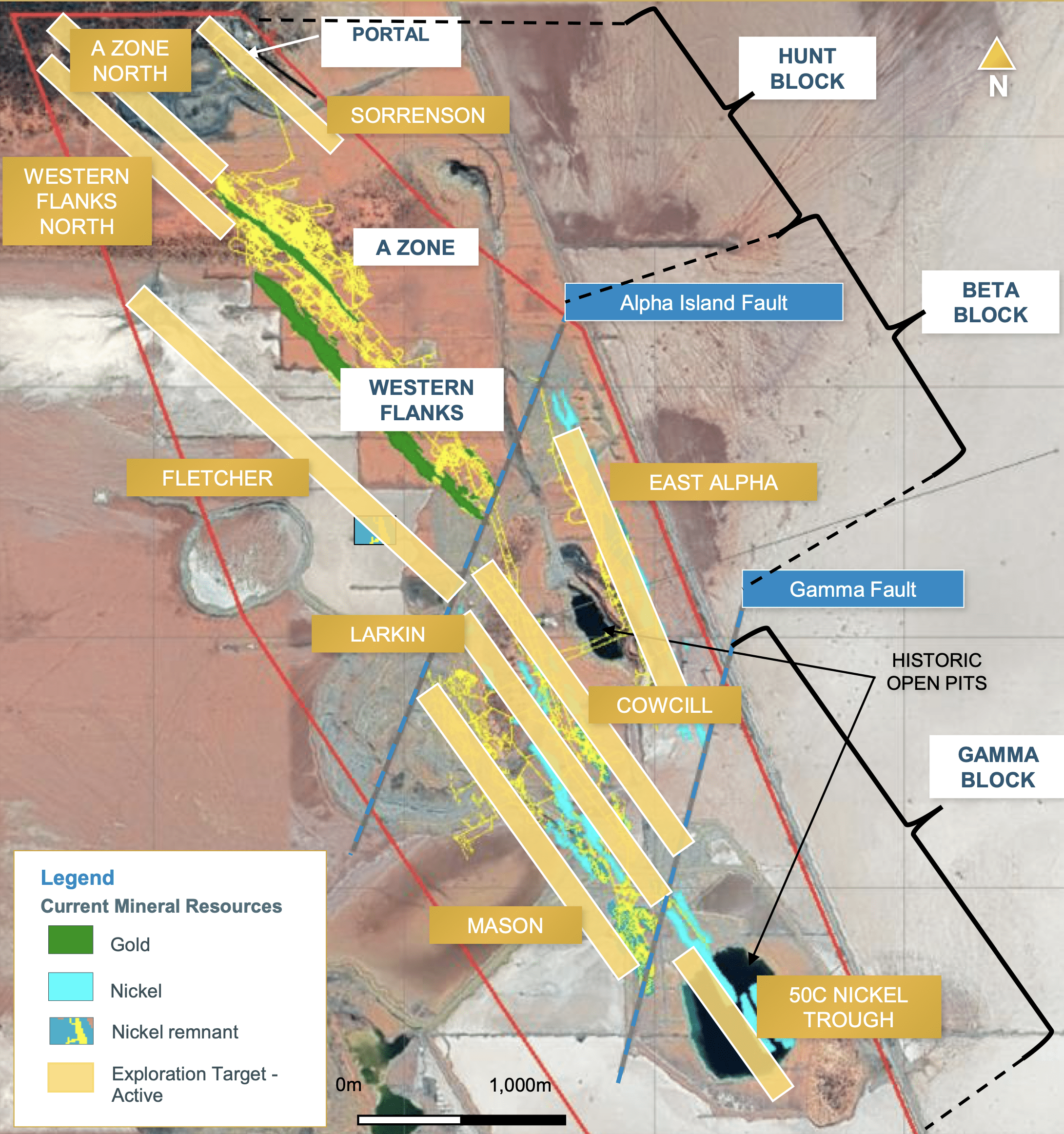

First, I want to focus on the recent drilling on the Fletcher shear, as hole BL1730-04AE intercepted 6.5 g/t over 26.0 meters in one interval and 46.5 g/t over 7.0 meters in another. Not only did this hole increase the strike length of Fletcher by 900 meters, but the grade is dramatically higher than what is mined at Western Flanks and A Zone, as grade from those zones typically averages ~2.5 g/t. We will have to see if the widths hold up, as true width isn't known yet. Karora claims that Fletcher is to be the third major gold system in the Hunt Block after the Western Flanks and A Zone.

{kind=link}

Again, there are multiple other shear zones, and grades are 10% to 200% higher in these zones than what's currently being mined. Once developed, Karora can start blending stopes at Beta Hunt and start mixing some of the ore from the Western Flanks with A Zone, with Fletcher, with Larkin, etc. If the company can take the average head grade from 2.5 g/t to over 3.0 g/t, production just from Beta Hunt would be 180,000-200,000 ounces of gold per year. Paul Huet, CEO of Karora Resources, was mining 20 stopes a month when he worked in Nevada for Newmont early in his career, and he needed to blend all of those stopes in order to get a ~1 oz per ton mill feed. He has the experience and track record to bring more zones into production and maximize the milled grade.

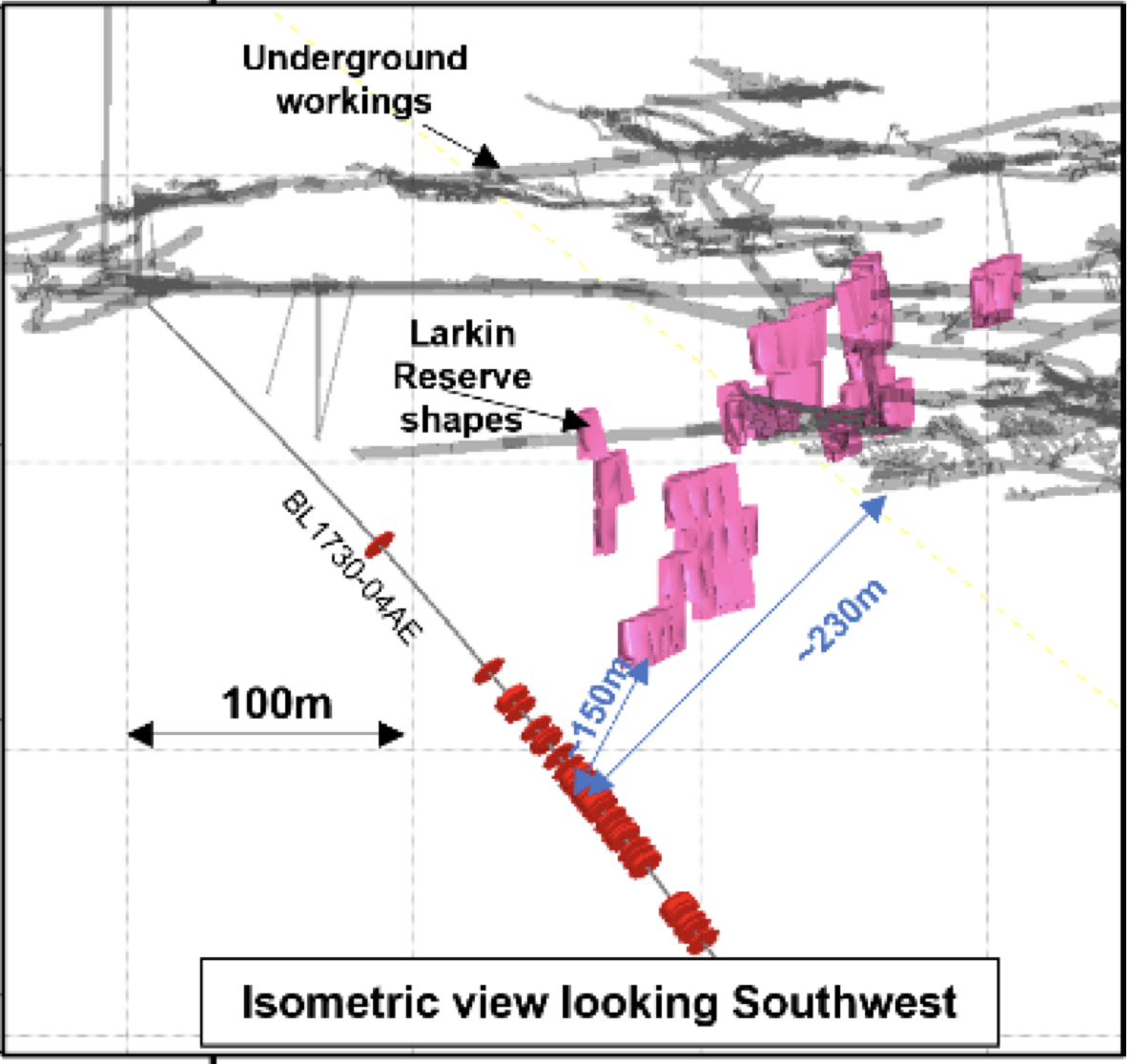

The exploration results at Fletcher also show the value of this underground infrastructure, as the hole I highlighted above was only 230 meters from the existing nickel development and 150 meters north of Larkin mineral reserves, which will allow Karora to gain access to this area of Fletcher quickly and it won't require much capital to bring these ounces online.

{kind=link}

But the gold is only half of the story, as there are ~34,000 tonnes of nickel resources at Beta Hunt.

Beta Hunt was a nickel mine for 35 years and produced 3,500-4,000 tonnes annually, year after year.

Nickel production this year is expected to be 500 tonnes, and it will increase to 600-800 tonnes next year as Karora increases the ventilation in the mine and proves up the resources.

Huet states that there is no reason that they can't get nickel production back to 3,500-4,000 tonnes, which on a gold equivalent basis, would be another 40,000-45,000 ounces and would likely be used as a by-product credit, making Beta Hunt one of the lowest cost gold mines in the world.

Huet claims Beta Hunt is a beast. If he can deliver on the gold production side, add in a substantial amount of nickel, and keep expanding the resources, then he might be right.

At a market cap of US$532 million and EV of $500 million, while also considering KRRGF is a soon-to-be ~200,000-ounce gold producer with cost in the first quartile of the industry, the valuation remains compelling. Karora would be clearing ~US$160 million a year of mine-site pre-tax cash flow at that run rate and current gold prices, and that's using an AISC of $1,150. A producer like this should be trading at a market cap of over US$1 billion. I do believe KRRGF will eventually get to that point if the company delivers on targets, and that's without any help from gold.

Of course, no gold miner is without risks, and the main one I see with Karora is what happened earlier this year with the resource at Larkin. Karora reported a robust increase in resources at Beta Hunt, but it also stated that Inferred resources at Larkin declined by 54% (88,000 ounces) due to a " geological re-interpretation of the north end of the resource which downgraded the size and grade of the previous interpretation based on new drilling data. " This news wasn't impactful as there weren't many ounces at Larkin and these were Inferred resources. Larkin also wasn't the main exploration target. While it's not a big deal if it occurs at Larkin, it is a big deal if it occurs at the Western Flanks (which contains 1.7 million ounces of gold resources). Only 538,000 ounces of the 2.4 million ounces of total gold resources at Beta Hunt are reserves. So, the accuracy of the majority of the Inferred resource (maybe even the majority of the M&I resource as well) is the biggest risk at this point, at least until there is more closer-spaced drilling.

{kind=link}

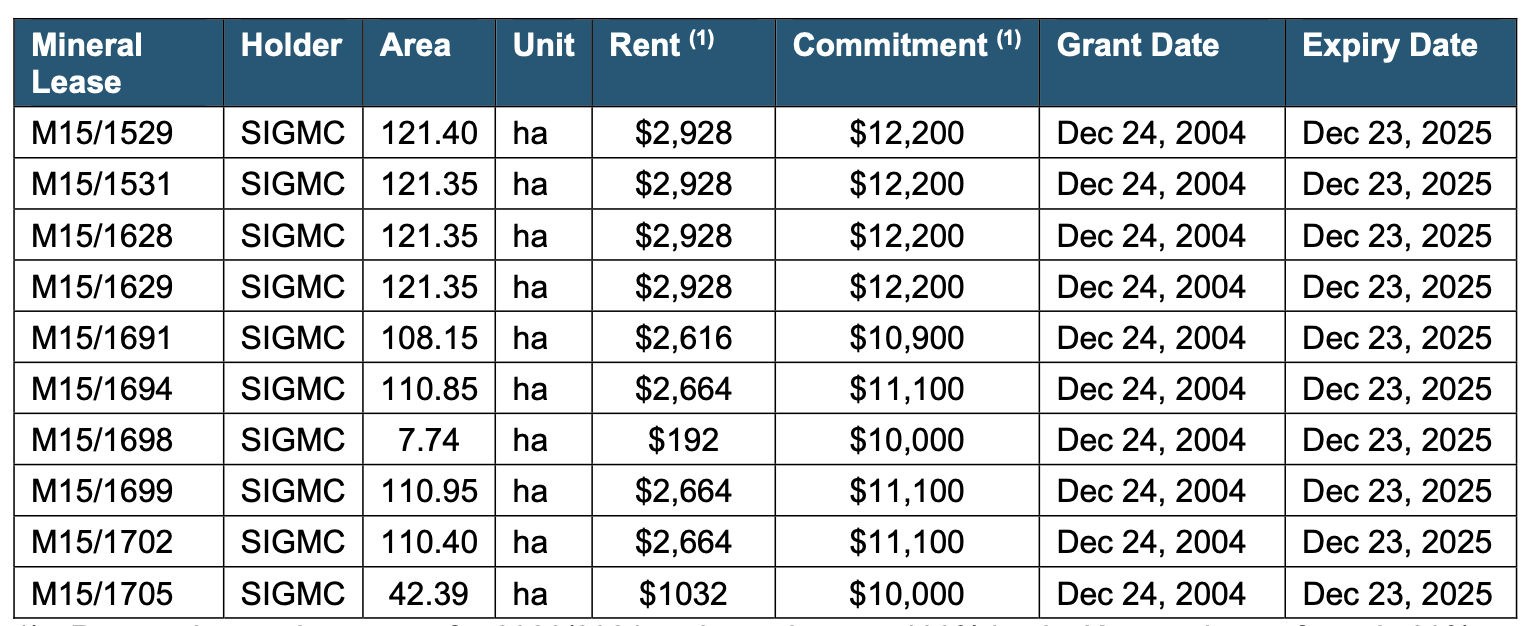

There is one aspect that I would like the company to provide clarity on as well, and it has to do with the Beta Hunt mineral rights.

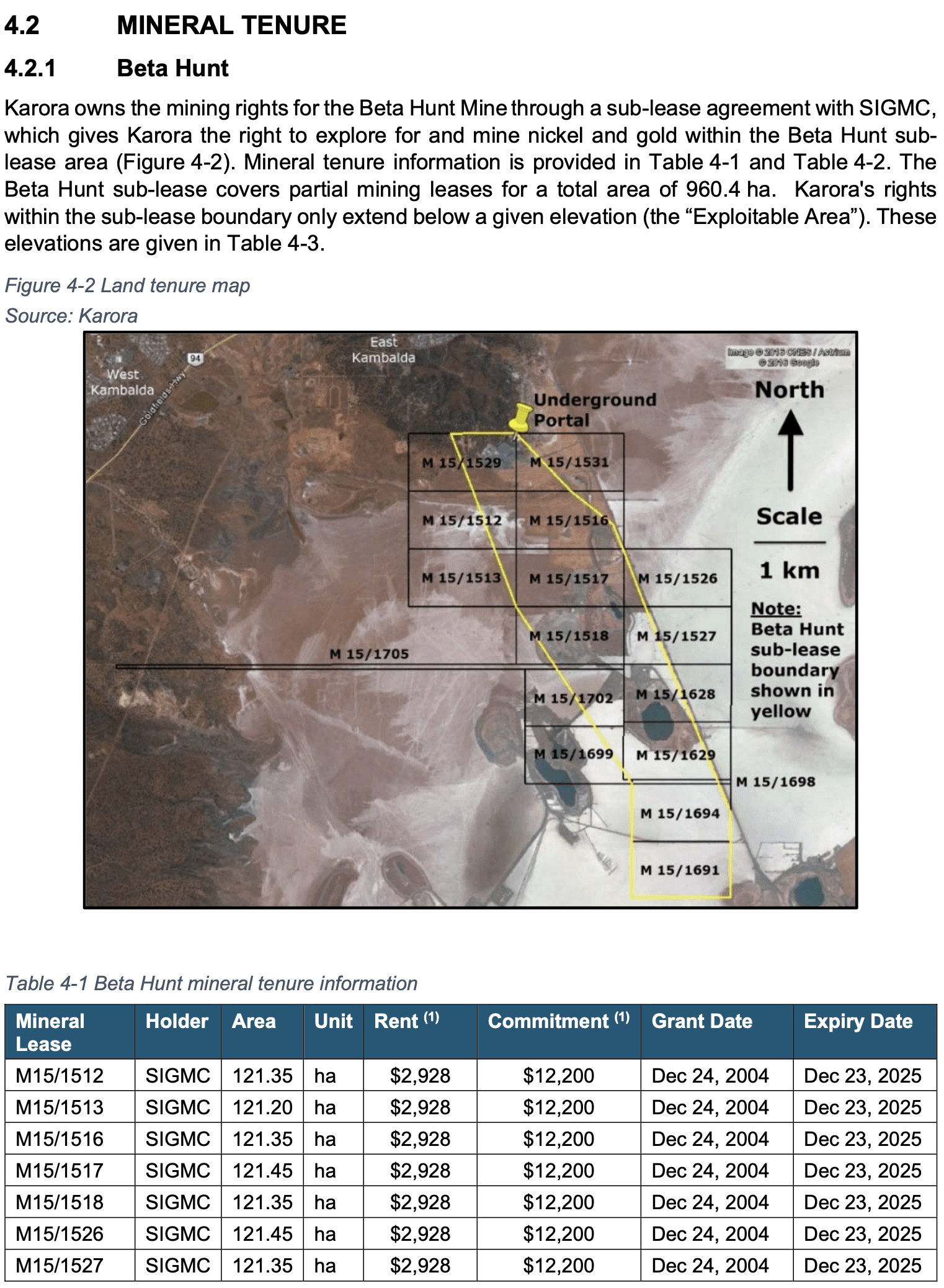

Karora operates Beta Hunt under a sub-lease agreement with Gold Fields ( GFI ), and per the latest technical report released earlier this year, the sub-lease expires on December 23, 2025 (originally granted on December 24, 2004, with a term of 21 years).

Karora Resources Karora Resources

{kind=link}

{kind=link}

The technical report says the lease " may be renewed for further terms ," but it's not clear if that's referring to the sub-lease or lease that Gold Fields has on the property, nor does it give any other information on the company's rights when it comes to further terms. The renewal process could be a formality and a non-event. Obviously, KRRGF is spending a considerable amount of money on Beta Hunt, and it's unlikely it would be doing so if it weren't able to renew the sub-lease, at least on favorable or similar terms. Still, I think it's important for the company to provide further details on the process and its expectations for the renewal of its mining rights. I would want to make sure the renewal is not a concern before heavily buying the stock.

For further details see:

Karora Resources: Beta Hunt Might Be A Beast