CA - Karora Resources: Too Cheap To Ignore

Summary

- Karora released its Q2 results earlier this month, reporting quarterly production of ~30,700 ounces of gold, a nearly 3% increase from the year-ago period despite significant headwinds.

- Unfortunately, while costs were up due to increased productivity and higher tonnes milled, costs were up sharply year-over-year, leading to a share decline in the stock.

- However, while most producers are seeing costs rise and stabilize without the benefit of growth or by-product credits, I would expect Karora's AISC to dip back below $950/oz next year.

- So, given Karora's industry-leading growth, industry-leading margins (post-2022) and continued exploration success, I see this pullback in the stock below US$2.20 as a gift.

The Q2 Earnings Season was mixed for the Gold Miners Index ( GDX ), with satisfactory operational performance overshadowed by cost creep and cost overruns on projects from a few producers. These headwinds were worst in Western Australia, where labor tightness caused misses for several producers. While Karora Resources ( OTCQX:KRRGF ) managed through the headwinds, it wasn't immune from inflationary pressures and labor tightness, pushing costs higher in H1 2022.

While this is disappointing and might have caused some to scratch Karora off their watchlists, it's important to note that Karora is arguably one of the best-positioned producers to deal with these inflationary pressures and claw back lost margins. Unlike most of its peers, it has an industry-leading growth profile, continues to see productivity gains, and benefits from by-product credits. So, while this has led to short-term pain on the bottom line, I would not be surprised to see costs decline to record levels next year. Given Karora's industry-leading growth coming from safe jurisdictions, I see this pullback below US$2.20 as a gift.

{kind=link}

Beta Hunt Coarse Gold (Company Presentation)

Q2 Production & Revenue

Karora Resources released its Q2 results earlier this month, reporting quarterly production of ~30,7000 ounces of gold, a 12% increase sequentially and a 3% increase from the year-ago period. The culprit for the only slight improvement in production was COVID-19-related headwinds in Western Australia that exacerbated an already tight labor market, coupled with lower grades mined in the period at Beta Hunt [BH]. The good news is that the worst of these headwinds appears to be over as of April; the company reported record tonnes mined of ~290,000 ounces from a single decline at BH in Q2 (~1.16 million tonnes annualized), and we should see a much stronger finish to the year due to higher grades.

{kind=link}

Karora - Quarterly Production (Company Filings, Author's Chart)

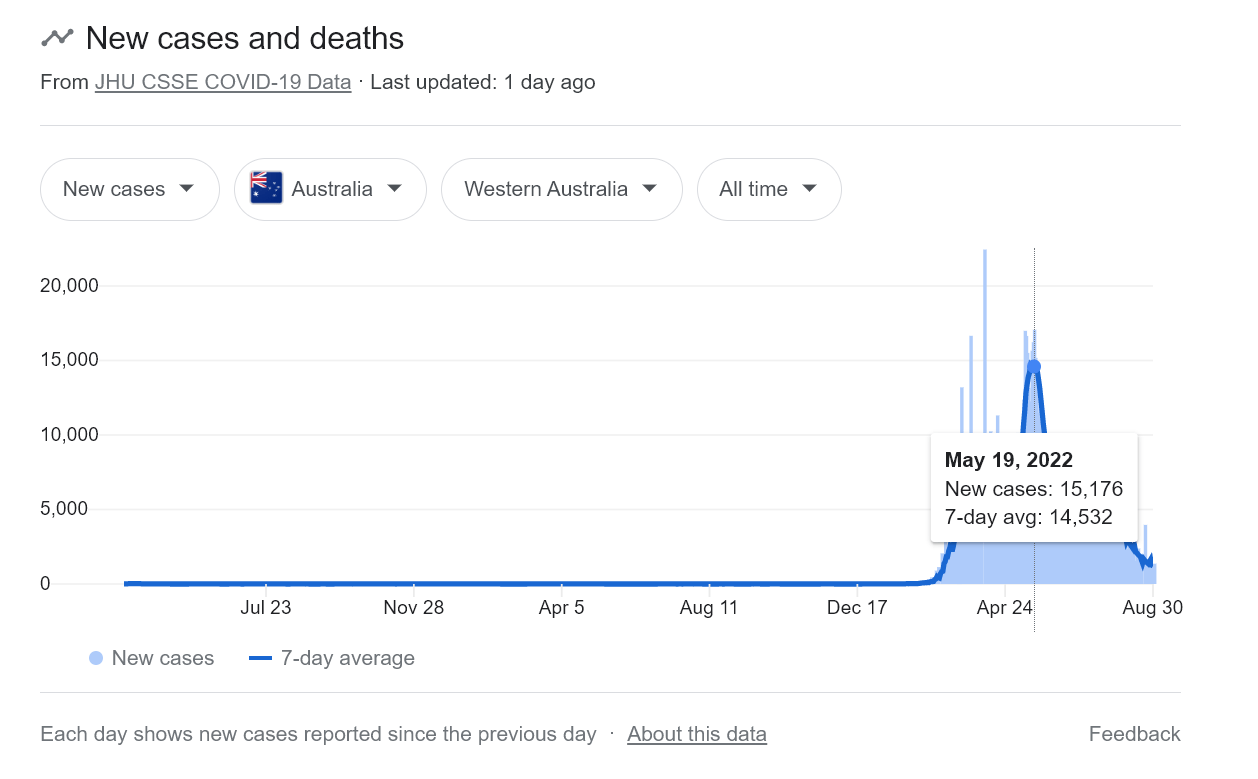

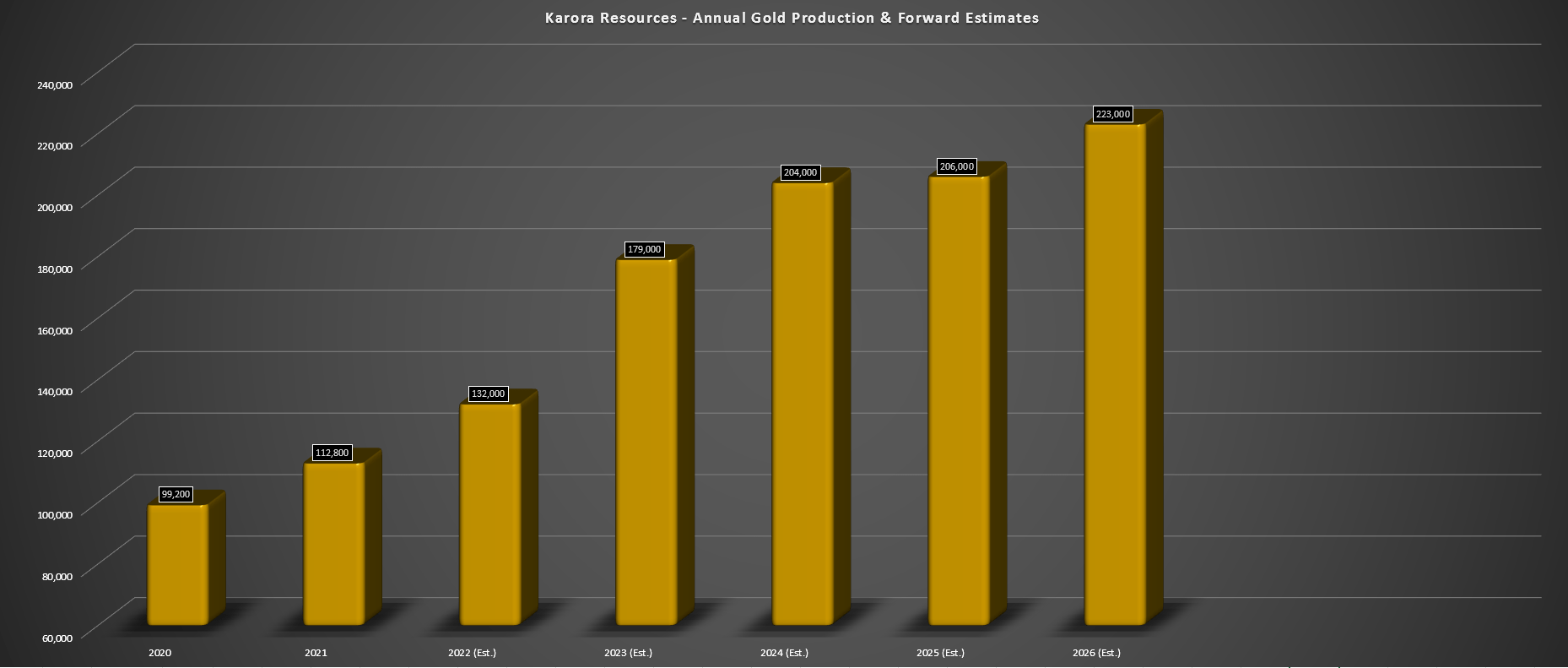

Looking at COVID-19 case counts confirms that the worst is behind us, with Australian case counts having peaked and down sharply and an even more pronounced decline in Western Australia. Combined with higher grades, this should lead to a significant improvement in production in H2, and Karora's increased production guidance (midpoint of 127,500 ounces vs. 122,500 ounces) suggests that we could see H2 production of 70,000+ ounces. Given that Karora has historically been quite conservative with guidance, I would not be surprised to see the company come in above 130,000 ounces for the year, beating its guidance mid-point by 2% or more.

{kind=link}

Western Australia COVID-19 Cases (JHU CSSE Covid-19 Data)

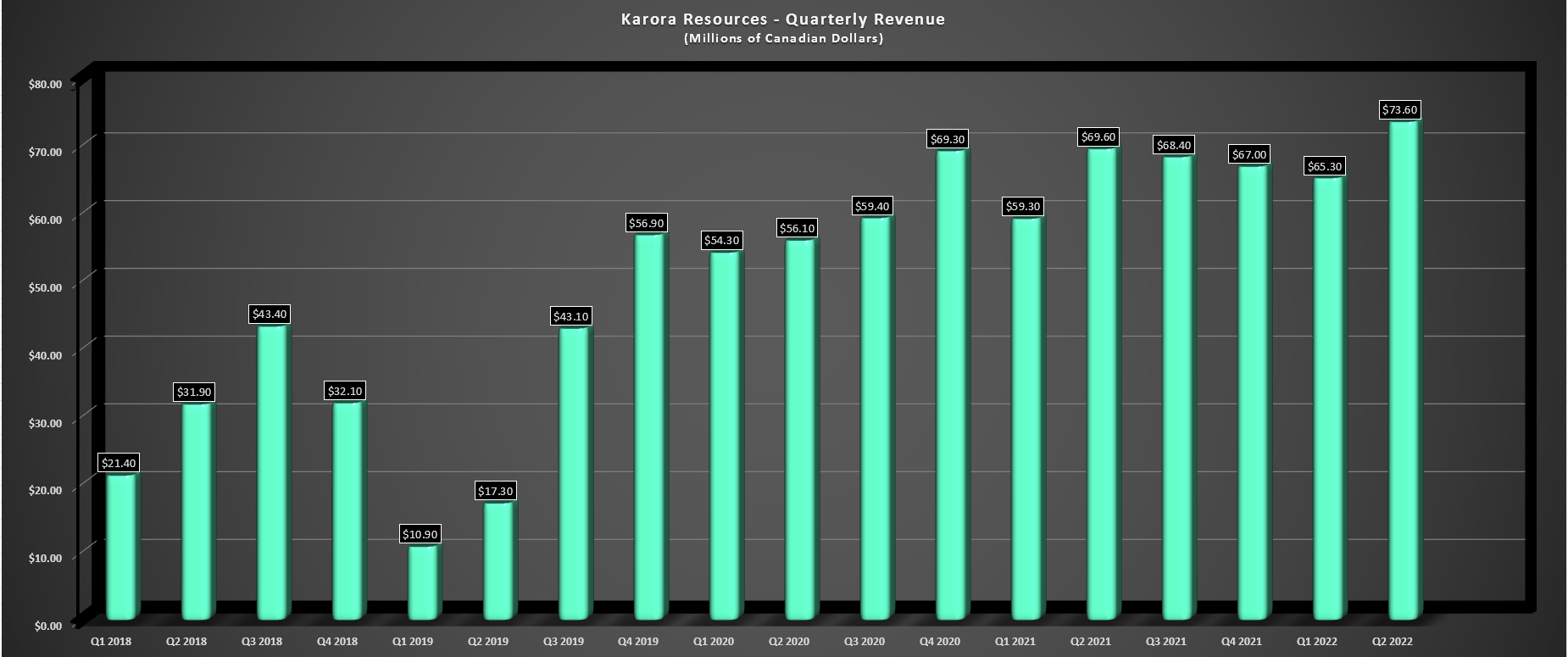

Moving to sales, gold ounces sold declined in the period due to difficult year-over-year comps (more ounces produced than sold in Q2 2021), but by less than 0.1%. Fortunately, Karora benefited from a higher gold price in the period, allowing it to report a record quarterly revenue figure of C$73.6 million [US$58.9 million], a 6% increase from the year-ago period. The gold price will not be a tailwind in Q3 (Q2 gold price: $1,860/oz), but the higher production should offset this in Q3 and Q4.

Finally, it's worth noting that while head grades were much lower, this was partially due to toll-milling ~51,000 tonnes of lower grade ore (1.34 grams per tonne gold) from BH as part of its due diligence process to acquire Lakewood. Hence, grades were artificially low in Q2, and the grade drop year-over-year is not a red flag. In fact, if exploration success continues, BH could see 2.9+ gram per tonne head grades post-2024 (Q2 2022: 2.14 grams per tonne gold) as higher-grade zones are mined.

{kind=link}

Karora - Quarterly Revenue (Company Filings, Author's Chart)

Costs & Margins

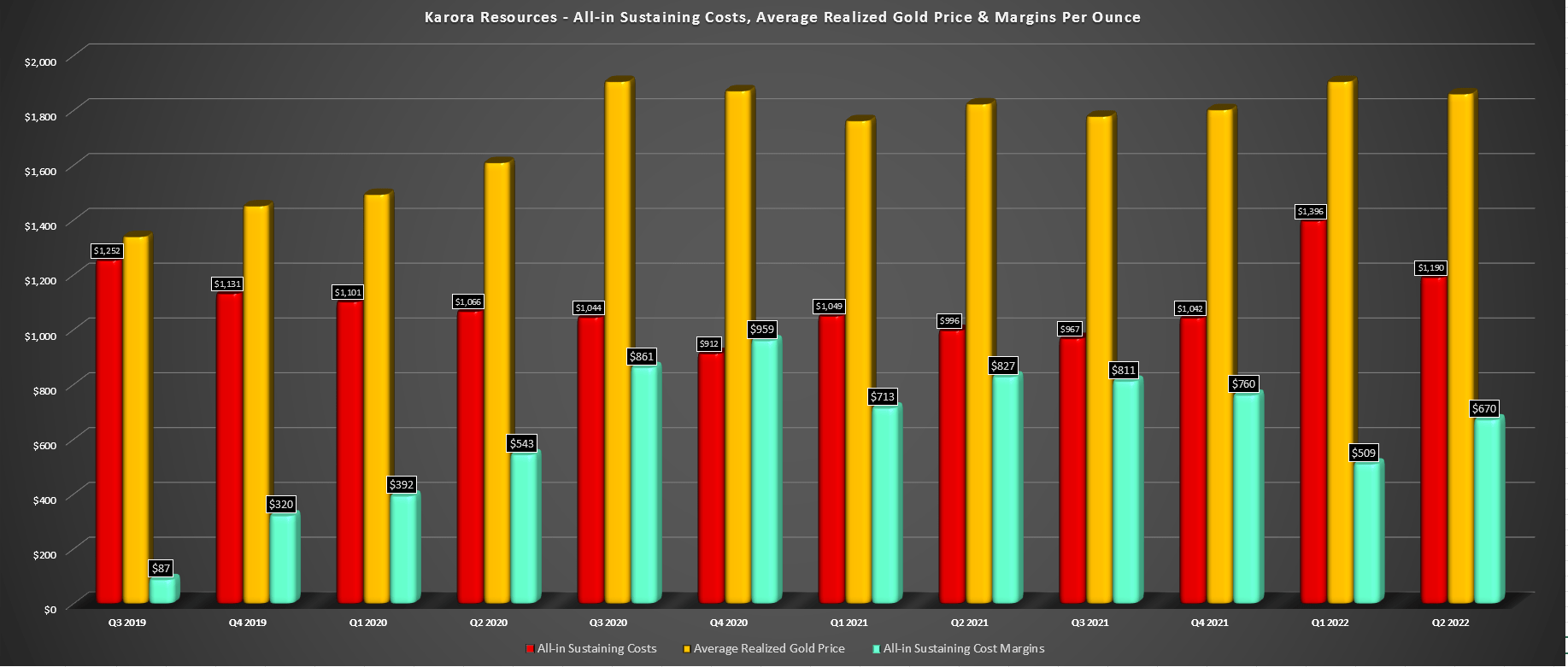

Looking at costs, Karora did a great job of improving costs on a sequential basis ($1,190/oz vs. $1,396/oz) even though it was still a very difficult quarter for its operations from a labor standpoint. This is evidenced by the spike in COVID-19 cases in April (above chart) and relatively high case counts, with additional pressure due to higher diesel costs, increased materials costs, and higher prices for other consumables. However, on a year-over-year basis, all-in-sustaining costs [AISC] jumped 19%, which might disappoint some investors.

{kind=link}

Karora - AISC, Gold Price & AISC Margins (Company Filings, Author's Chart)

While it's easy to be negative about this sharp increase in costs that were slightly above the industry average cost increase, it's important to note that the benefit of working in a prolific mining jurisdiction (Western Australia) combined with the border opening worked against it in Q2. However, it still reported respectable AISC margins of $670/oz (36.0%), and this is despite Karora being a relatively small producer that isn't benefiting from the economies of scale it will once its second decline is complete (Q2 2023). For those unfamiliar, this will double mine production at BH to 2.0+ million tonnes per annum, with the possibility of 2.1+ million tonnes mined if productivity rates are maintained.

The good news is that, unlike most producers, Karora has a very clear path to clawing back all of its lost margins and then some, with the potential to report record low costs in FY2023. This is because it is benefiting from higher nickel production (increased by-product credits), it's steadily increasing gold production, and it's now going to see lower diesel costs with 1/90th the trucking distance for nickel. The reason is that it's now hauling material to the Kambalda Mill next door vs. a nearly 400-kilometer trek to Leinster. Finally, diesel prices appear to have peaked, pointing to lower costs for regular operations as long as things don't worsen.

{kind=link}

Annual Gold Production & Forward Estimates (Company Filings, Author's Chart & Estimates)

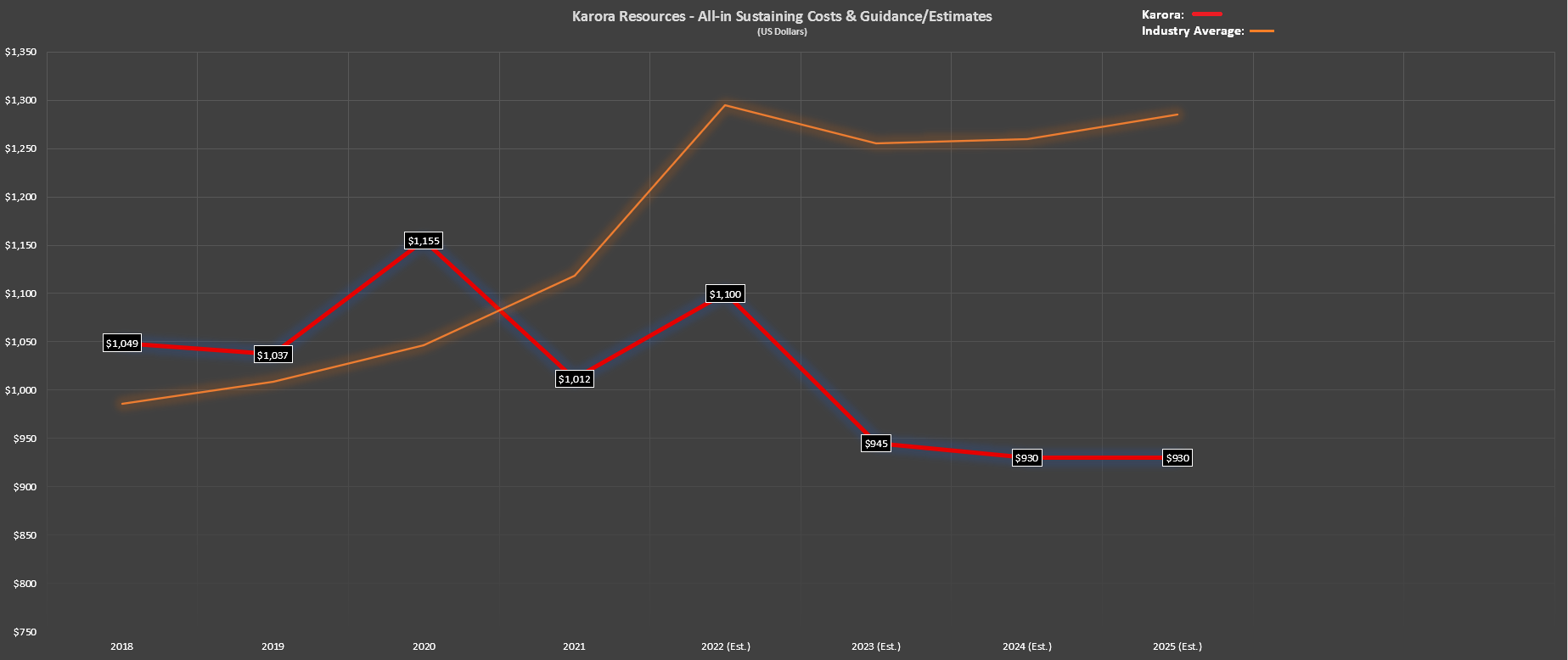

This is important because it means that while the average producer has seen costs spike ~15% vs. FY2020 levels in line with Karora, these producers don't have the tailwinds in place to claw back these margins. The point is best displayed by the below chart, which shows that Karora's costs should decline to $945/oz in FY2023 and $930/oz in FY2024 while the industry average all-in sustaining costs should only dip marginally from the FY2022 peak and then begin to trend back up due to sticky labor inflation in FY2024/FY2025. So, while many producers will see a $70/oz dip in margins if the gold price stays at current levels, Karora will see a 10%+ increase in margins even at $1,750/oz gold.

This is based on assumptions of a $100/oz gold price decrease year-over-year if gold price stays at current levels, offset by a $250/oz decline in AISC ($945/oz vs. $1,100/oz).

{kind=link}

Karora - Annual AISC & Forward Estimates vs. Industry Average (Company Filings, Author's Chart)

Given this unique margin profile, I believe Karora should trade at a premium to its peer group, especially since it's a top-10 growth story sector-wide. However, despite continuing to push out exciting news, including the appointment of a new Chief Operating Officer from the St. Ives Mine next door, Karora has found itself at lower prices than a month ago, a case of the baby being thrown out with the bathwater. Let's dig into the valuation below:

Valuation

Based on ~178 million fully diluted shares (year-end 2023) and a share price of US$2.20, Karora trades at a market cap of $392 million or an enterprise value of approximately $300 million. If we compare this market cap figure to an estimated net asset value of $1.02 billion, Karora is currently trading at 0.38x P/NAV, a valuation typically reserved for early-stage developers or producers in jurisdictions one would prefer not to venture into from an investment standpoint (Guatemala, Venezuela, South Africa, etc.). However, buying at this valuation has been made possible due to a market environment where great news is sold into, good news is sold into, and bad news often leads to violent gaps lower.

In Karora's case, it's been consistently reporting great news, with the six most recent developments being as follows:

- a second mill to de-risk its growth plan

- news that the second decline is ahead of schedule & under its original budget

- a new coarse gold find, which could boost H2 production

- high-grade gold intercepts in zones parallel to Larkin (Mason/Cowcill)

- hiring a new COO, Bevan Jones, whose done an exceptional job next door at St. Ives

- a robust nickel PEA paving a path towards much higher by-product credits at Beta Hunt & lower trucking costs with BHP ( BHP ) restarting its Kambalda Mill

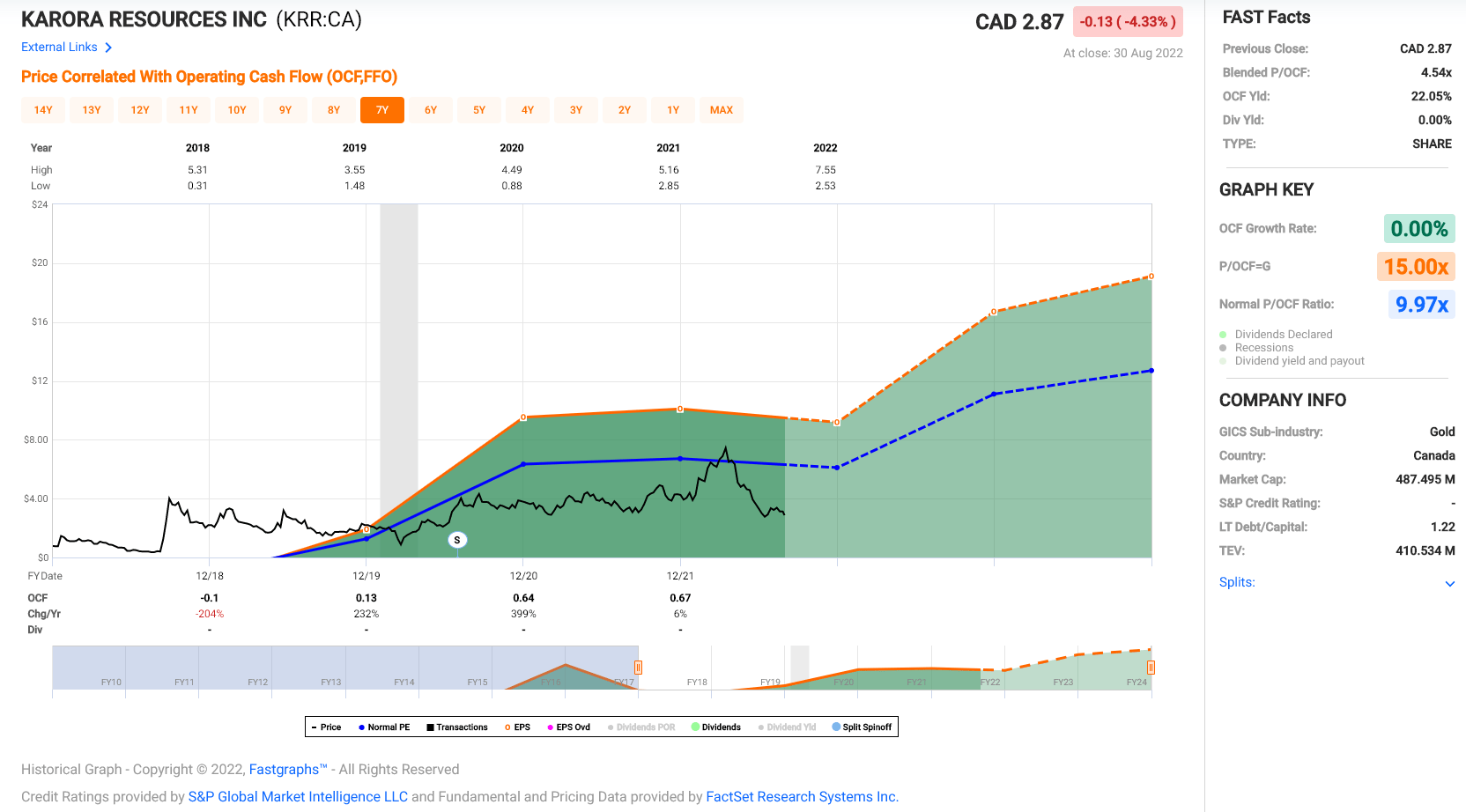

Given the irrational selling we're seeing sector-wide, and in Karora, I see this as a rare opportunity for investors to buy the stock with more than 180% upside to fair value (18-month price target: US$6.30). This is based on what I believe to be a fair multiple of 1.10x P/NAV to account for the company's industry-leading growth and Tier-1 jurisdictional profile, as well as the fact that it's a top-10 exploration story among sub-million-ounce producers sector-wide. The valuation is just as attractive from a cash flow standpoint, with Karora trading at just ~2.2x FY2023 cash flow estimates ($1.02).

{kind=link}

Karora Resources - Historical Cash Flow Multiple/Current Valuation (FASTGraphs.com)

While a significant upside case is important when considering stocks to purchase, what's even more important is the risk profile and possible downside potential when considering that upside case. In my view, Karora has a very simple growth strategy, does not have jurisdictional risk, and is one of the best-positioned producers to deal with inflationary pressures. So, I don't see much uncertainty regarding not meeting its plans or a jurisdictional risk standpoint, especially with a new COO and a new mill.

{kind=link}

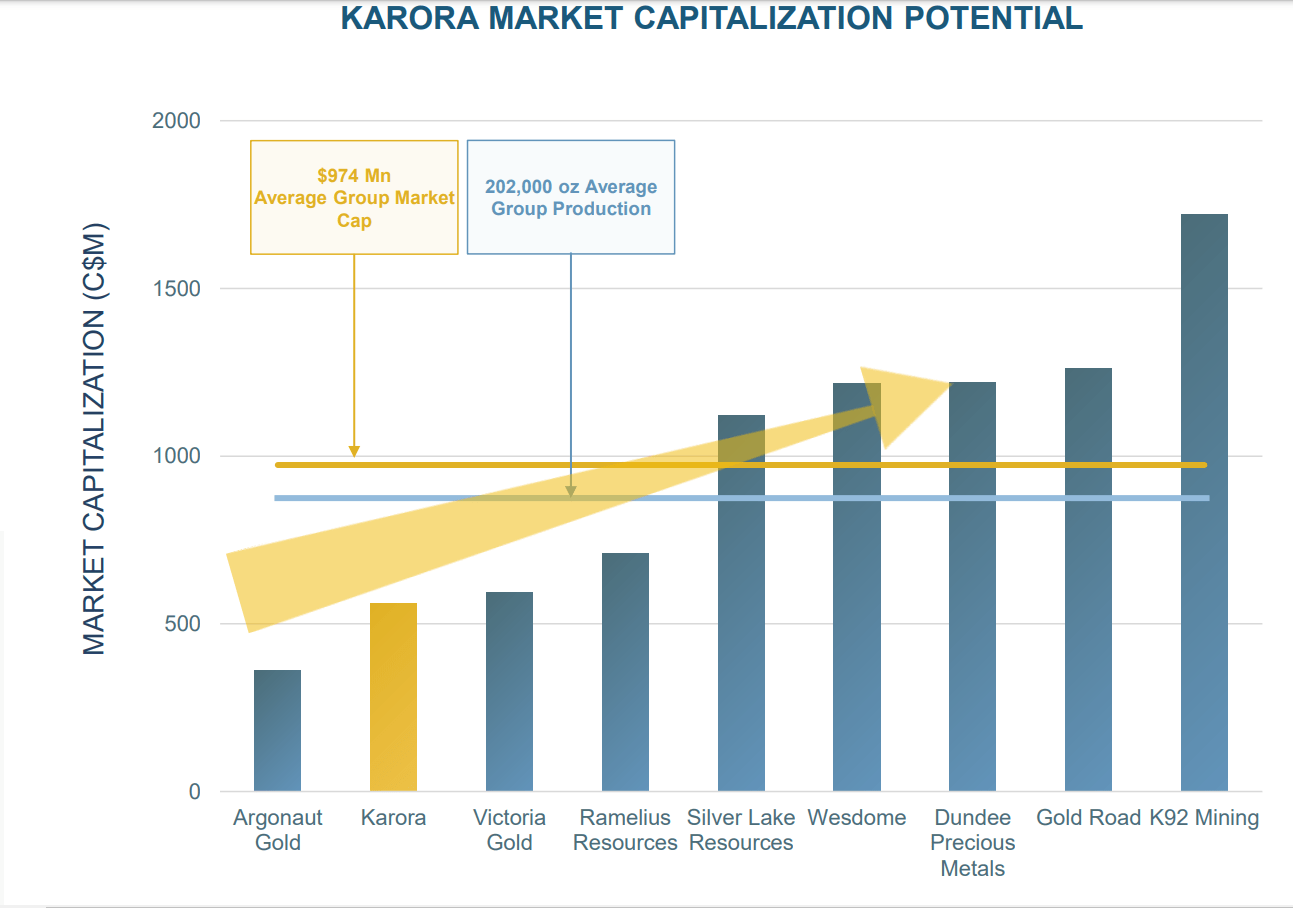

Karora - Market Cap vs. Peers (Company Presentation)

To summarize, while the upside case is extremely attractive, I see the downside as very limited from current levels. In my experience, this is what makes for the best investment opportunities. Given the attractive reward/risk setup, I recently added to my position, and I continue to see Karora as a top-10 producer sector-wide. It's also worth noting that given the added mill capacity (2.8 million tonnes per annum in total if a small expansion completed at Lakewood), the current growth plan looks to be under-selling the true potential here. In an upside case, this could be a near doubling of production to 220,000+ ounces if we continue to see exploration success at Beta Hunt (2.90+ gram per tonne head grades). The current growth plan mid-point is 195,000 ounces.

Summary

In a sector where we've seen significant capex blowouts, and relatively poor cost controls among the industry laggards, the wheat has quickly been separated from the chaff. Some investors may prefer dumpster-diving for cheap names, but low-quality names are cheap for a reason, and they're sure to deliver additional disappointments since it's in their DNA. However, Karora has proven that it can under-promise and over-deliver under new leadership with CEO Paul Huet. Even with near unprecedented headwinds, the company is doing a phenomenal job tracking against its growth plan and keeping costs below the industry average (FY2022 estimate: $1,290/oz).

So, rather than dumpster diving for the Argonauts ( OTCPK:ARNGF ), Great Panthers ( GPL ), and Iamgolds ( IAG ) of the sector, I think it makes far more sense to focus on quality, and Karora easily makes the top-10 list from a quality standpoint. This is especially true given that while low-quality names often find themselves on the sale rack, high-quality companies rarely ever head to absurd valuation levels outside of violent bear markets, which is where Karora has found itself today (~0.40x P/NAV, ~2.2x cash flow). In summary, I remain very bullish on Karora despite the share price weakness, and I see it as one of the most attractive ways to get exposure to the gold price.

For further details see:

Karora Resources: Too Cheap To Ignore