CA - Karora Resources: Tracking Well Against FY2023 Guidance

2023-12-03 20:32:38 ET

Summary

- Karora is on track to achieve its goal of 2.0 MTPA mining rates at Beta Hunt by year-end FY24 & is tracking ahead of its FY23 output guidance midpoint.

- Meanwhile, the company continues to add new ounces and make near-mine discoveries, supporting its growth plans and improving what was previously a relatively short mine life.

- In this update, we'll dig into the Q3 results, any recent developments, and how the stock stacks up from a valuation standpoint vs. some of its peers.

Just over five weeks ago, I wrote on Karora Resources , noting that while the stock was undervalued, I didn't see a low-risk buying opportunities and continued to prefer names elsewhere trading at much larger discounts to fair value. And although Karora has done well since this recent update, names that I preferred like Marathon Gold ( MGDPF ) and Victoria Gold ( VITFF ) have outperformed meaningfully, with both briefly trading at under 0.50x P/NAV (10%/5% discount rates, respectively). This has contributed to outperformance in my portfolio (shown below), with my portfolio outperforming the Gold Miners Index ( GDX ) and S&P 500 ( SPY ) significantly since the Q3 2020 peak for GDX, with the GDX actually negative in the same period.

Portfolio Returns (July 2020 to November 2023) - Author's Photo

{kind=link}

I have purposely used the worst possible benchmark for GDX in Q3 2020 when it peaked vs. only showing returns in periods when the benchmark has been positive.

On a positive note, Karora continues to make significant progress on its growth plans and is on track to deliver on its goal of 2.0 million tonnes per annum mining rates at Beta Hunt by this time next year. This should allow the company to ramp up to annual production of ~190,000 ounces per annum in 2025 at sub $1,100/oz AISC assuming the labor situation doesn't worsen in Australia, which could negatively affect costs. Just as importantly, the company continues to add new ounces and make near-mine discoveries, supporting the decision to add a second decline and pull forward ounces for the mine. In this update we'll dig into the Q3 results, any recent developments, and how the stock stacks up from a valuation standpoint vs. some of its peers.

Beta Hunt Operations - Google Earth

{kind=link}

All figures are in United States Dollars unless a C$ precedes the dollar figure.

Q3 Production & Sales

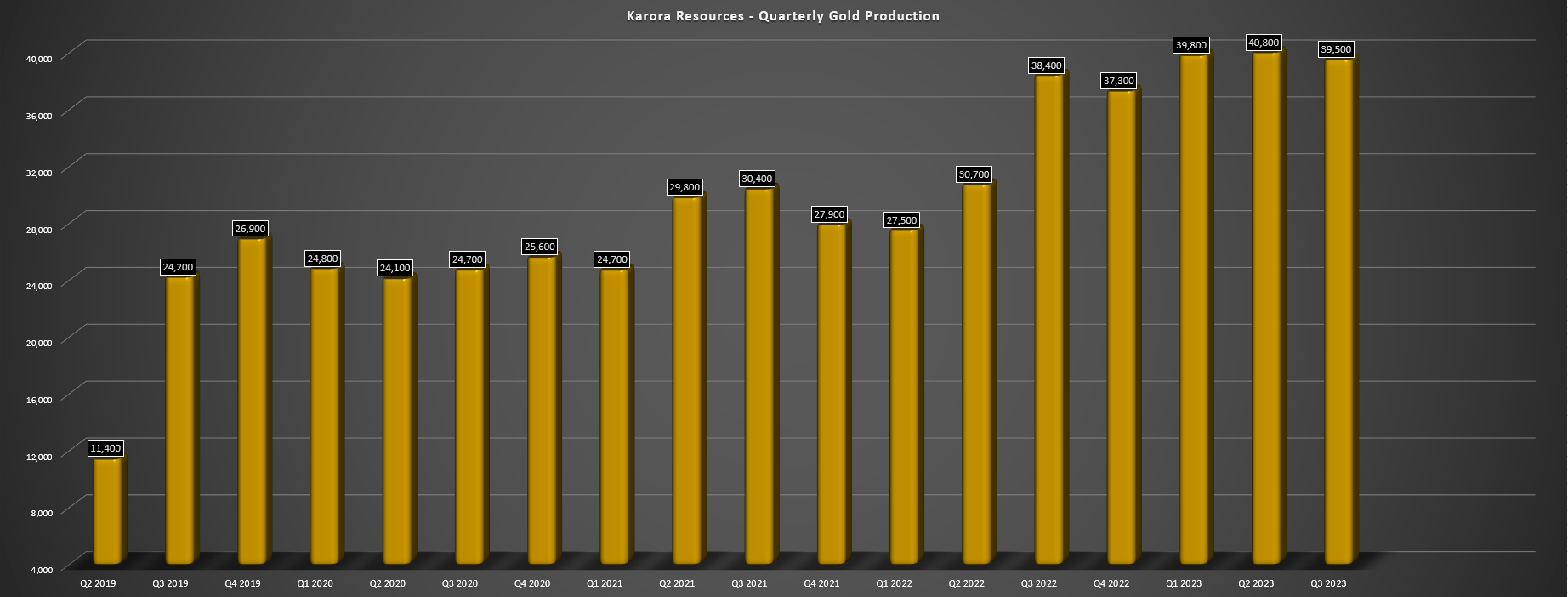

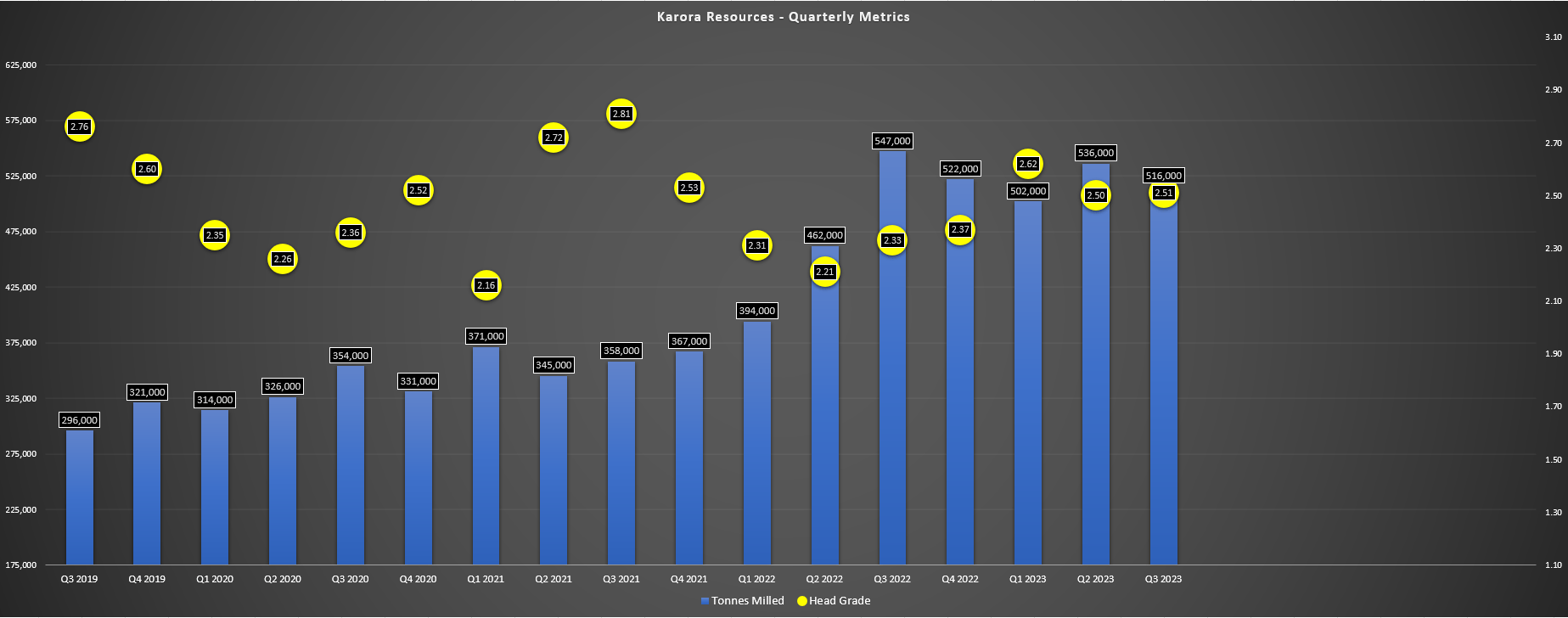

Karora Resources ("Karora") released its Q3 results last month, reporting quarterly production of ~39,500 ounces of gold, a 5% increase from the year-ago period. The increased production was driven by higher grades which offset the lower throughput year-over-year, with its Higginsville [HGO] operations responsible for the uptick in grades thanks to mining at Aquarius Underground (final stoping now completed). Meanwhile, although Beta Hunt mined more tonnes in the period (+14% year-over-year) and benefited from a full quarter with its new Lakewood Mill, the higher throughput was offset by lower grades (2.17 grams per tonne of gold vs. 2.36 grams per tonne of gold), resulting in slightly lower production from its flagship asset. Meanwhile, although Higginsville saw a significant uptick in grades, the asset saw fewer tonnes milled at higher costs due to a crusher bridge failure, with repairs set to be completed by year-end.

Karora Quarterly Production - Company Filings, Author's Chart

{kind=link}

Karora - Quarterly Operating Metrics - Company Filings, Author's Chat

{kind=link}

Digging into the results a little closer, Beta Hunt's average mined and processed grades (2.00/2.17 grams per tonne of gold, respectively) were well below its reserve grade of 2.70 grams per tonne of gold, with planned mining of a lower grade section of Beta Hunt. However, while we should see a downtick in grades at HGO with mining moving to the Pioneer Pit (13 kilometers southeast of the HGO plant) and the cessation of mining at Aquarius Underground, the company noted that grades should improve in Q4 at Beta Hunt, helping the asset to deliver ~23,700 ounces assuming ~320,000 tonnes milled and an average processed grade of 2.45 grams per tonne of gold. And with production already tracking at ~79% of its annual guidance mid-point (~120,200 vs. ~152,500), Karora will be one of the few producers to deliver near the top end of its FY2023 guidance (~160,000) assuming a decent Q4 from Higginsville.

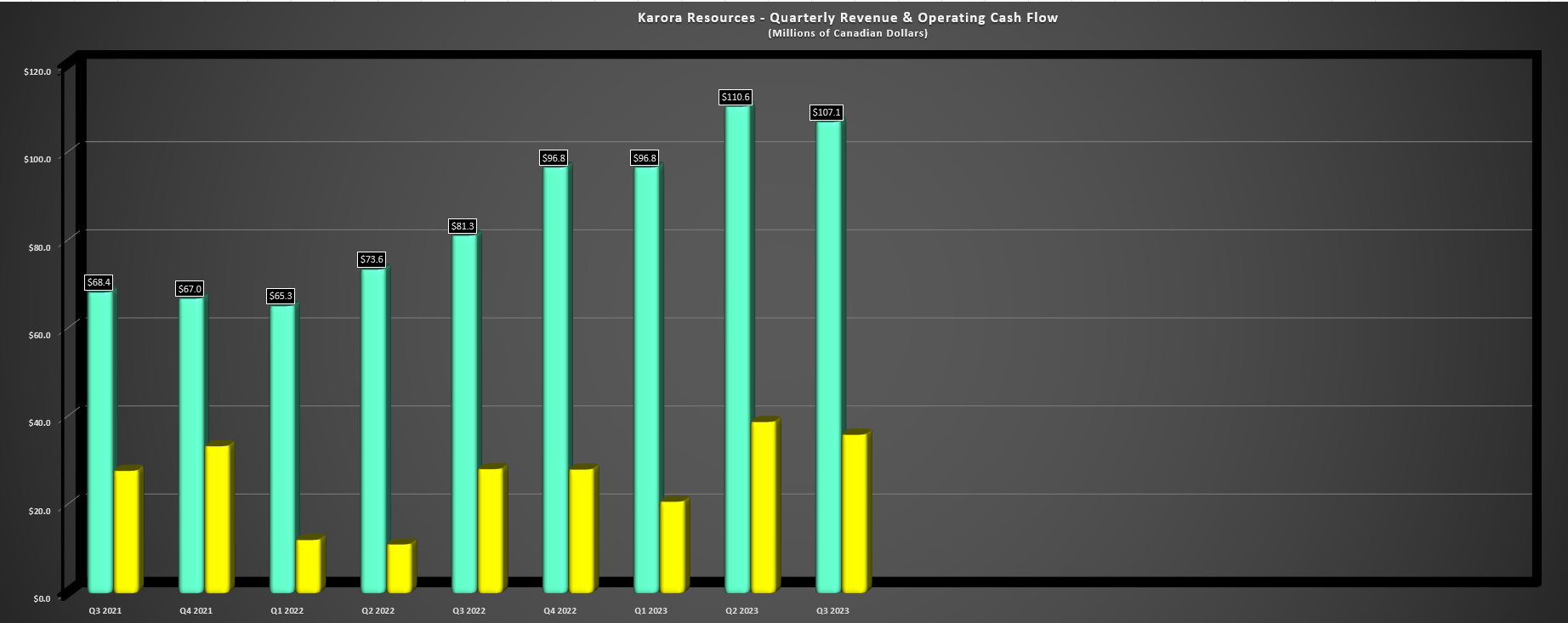

Karora - Quarterly Revenue & Operating Cash Flow - Company Filings, Author's Chart

{kind=link}

As for Karora's growth plans, investors will be pleased to know that the third vent raise was completed which will allow for much higher mining rates (2.0 million tonne per annum goal by year-end 2024), with primary ventilation fans set to be commissioned in Q2 2024. In addition, two underground trucks and an underground loader were added to the fleet in the quarter, and Karora spent ~$20 million in the period, allowing to generate ~$13 million in free cash flow on revenue of C$107.1 million and operating cash flow of C$45.3 million. And given the solid operating performance, Karora has continued to maintain a net cash position and ended the quarter with C$84 million in cash to potentially support a ramp-up in exploration and any future growth. To summarize, Karora looks well on track to deliver 180,000 ounces next year, with a push closer to 200,000 ounces in FY2025.

Costs & Margins

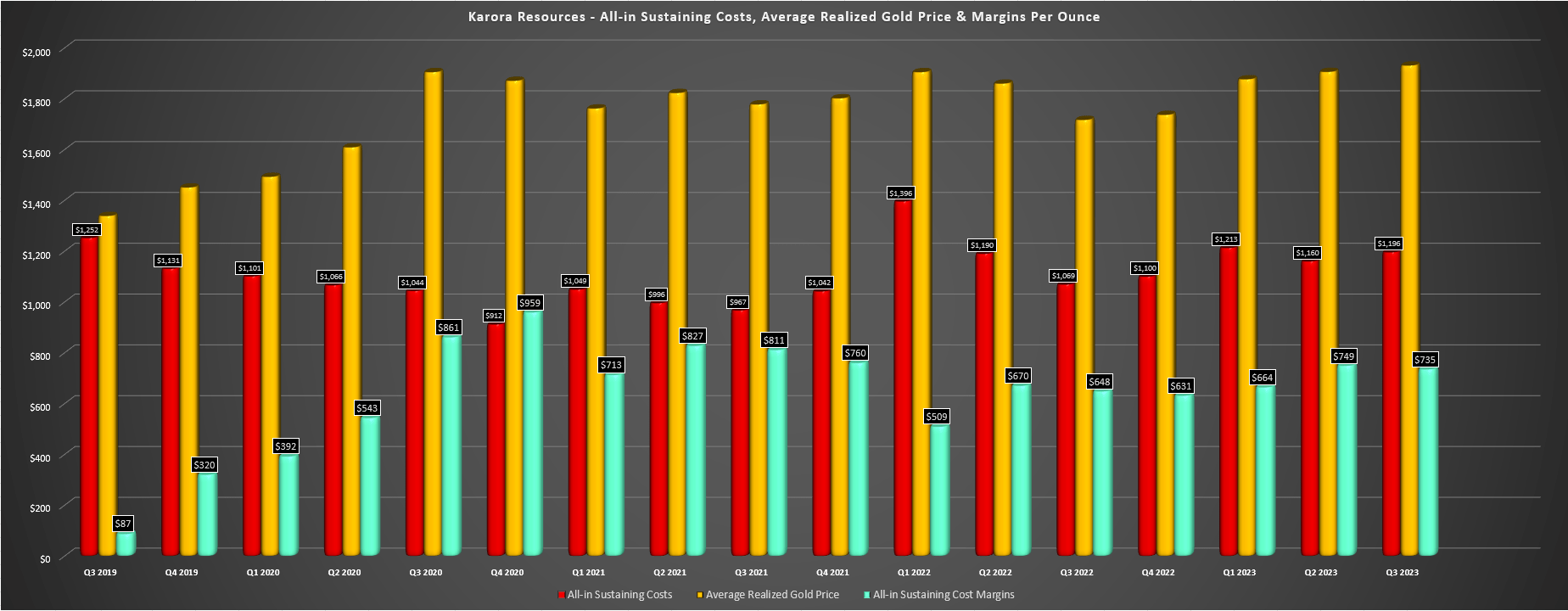

Unfortunately, production may have been in line with my expectations, but margins were weaker than I expected, especially given the higher average realized gold price of $1,931/oz (Q3 2022: $1,717/oz). In fact, AISC margins came in 2% below my estimates of ~$750/oz at just $735/oz, with Q3 cash costs and all-in sustaining costs [AISC] of $1,062/oz and $1,196/oz, respectively. It's important to note that there was a $22/oz impact from no by-product credits due to the timing of nickel sales, and we did see higher sustaining capital in the period. Still, some of the softer margin performance appears to have been from the tight labor market in Western Australia, consistent with what Gold Fields ( GFI ) called out in its Q3 results (Gold Fields is Karora's neighbor at St. Ives) where it stated that a shortage of skilled will remain a headwind for its Australian segment.

"The operating environment remained challenging as above-inflation cost increases and the shortage of key skills, particularly in the Australia and South Africa regions, persisted. Despite a slight improvement in annualised turnover rates for some critical skills categories during the quarter, the shortage of skilled staff is expected to remain a headwind for the Australian operations."

- Gold Fields, Q3 2023 Results

Karora - AISC, Gold Price & AISC Margins - Company Filings, Author's Chart

{kind=link}

As noted in Karora's remarks, the company was not immune from these cost pressures and the tight labor market, with it disclosing that the tight labor market in WA contributed to increase employee and contract costs and that it's seen continued cost pressure in labor, contractors, power, and fuel. This isn't helped by the fact that nickel has fallen off a cliff since early 2022, resulting in less benefit from a by-product credit standpoint (and especially in Q3 with no sales due to timing). Hence, while Karora is on track to deliver into its guidance of $1,100/oz to $1,250/oz in FY2023 with a better Q4 ($1,188/oz year-to-date), it might be a safer bet to model the company above mid-point of its FY2024 guidance ($1,050/oz to $1,200/oz) with the benefits from a weaker Aussie Dollar being partially offset by a weaker nickel price than what's been modeled in guidance ($22,000/tonne) and what appears to be little improve in the labor market in Western Australia. Let's take a look at Karora's valuation and see whether the stock is offering enough margin of safety:

Nickel Price - BusinessInsider.com

{kind=link}

Valuation

Based on ~186 million fully diluted shares and a share price of US$3.70, Karora trades at a market cap of ~$690 million. This leaves the stock trading at a significant premium to other Tier-1 jurisdiction producers like Victoria Gold ( VITFF ) and Argonaut Gold ( ARNGF ) even when adjusting accounting for their net debt, and also a much higher P/NAV multiple of ~0.75x vs. Victoria Gold and Argonaut Gold at estimated P/NAV multiples of ~0.49x and ~0.38x, respectively. This doesn't mean that Karora can't trade higher and it certainly stands out as one of the junior producers with a unique mix of a strong balance sheet, solid organic growth, and two assets in Tier-1 ranked jurisdictions. That said, the outperformance has made the stock less attractive from a relative value standpoint (estimated fair value of Karora is US$4.50), and I prefer to buy when stocks are hated and at a minimum 40% discount to fair value (US$2.70 or lower for Karora) vs. paying up when they're back in favor. Hence, I don't see enough margin of safety to justify chasing the current rally.

The other point worth noting is that we are seeing a significant divergence in what insiders are doing from a buying/selling standpoint at Argonaut vs. Karora, with Argonaut insiders being net buyers of a significant amount of stock over the past twelve months at prices above current levels (with the most significant purchases by Argonaut's CEO, Richard Young, who purchased ~1.92 million shares at an average price of ~US$0.41 which is above current levels). As for Karora, we haven't seen any meaningful insider buying, but have seen a healthy amount of insider selling over the past twelve months and with these sales done at prices below current levels with sales prices ranging from ~US$3.10 to ~US$3.50. And while this doesn't mean that Argonaut has to outperform Karora from here, it's certainly positive to see management putting their money where their mouth is with the stock trading at a depressed valuation of just ~0.38x P/NAV using conservative estimates for its second mine, Florida Canyon (~$130 million NPV (5%) vs. ~$220 million at spot prices even adjusting for inflationary pressures/shorter mine life).

Florida Canyon Estimated NPV (5%) - 2020 TR

{kind=link}

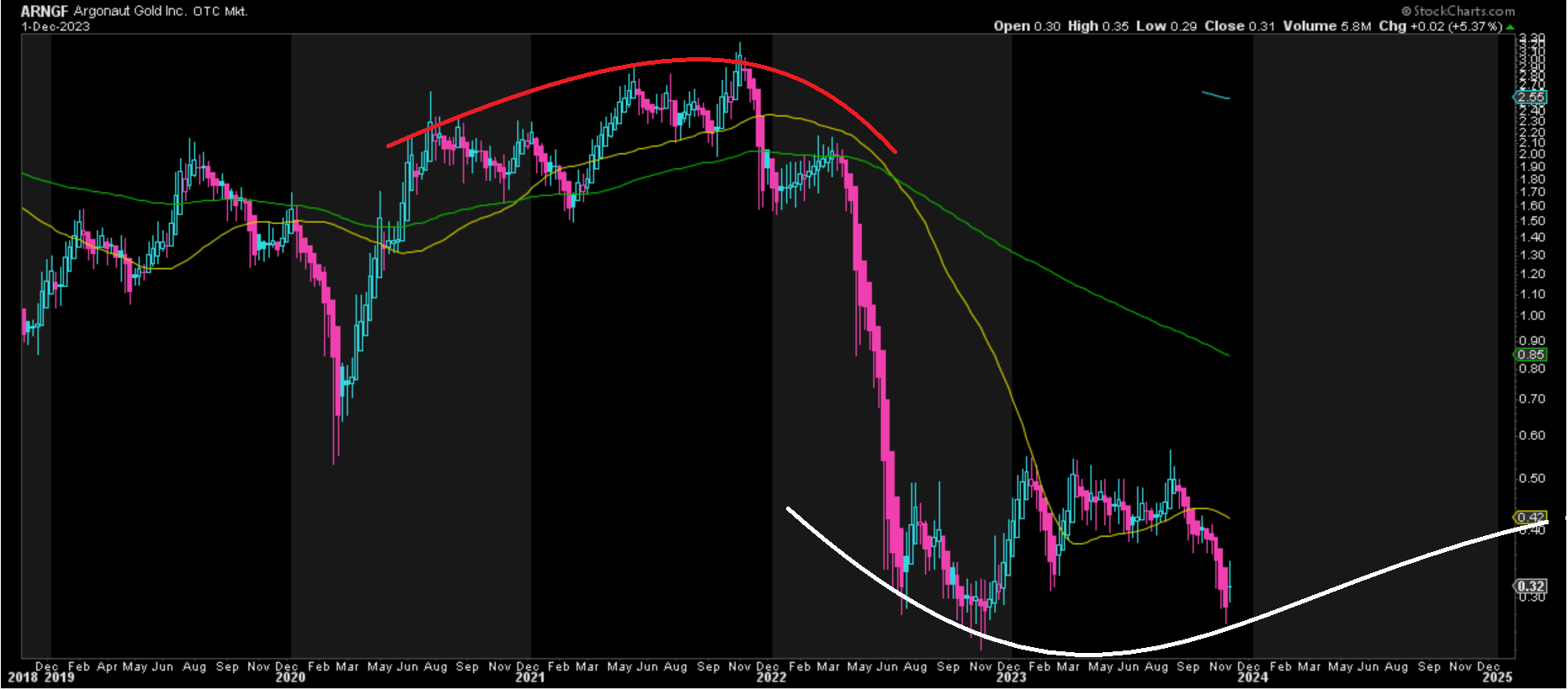

This divergence in valuation could take time to correct itself and with Magino still in the ramp-up phase, the stock may remain out of favor until investors become more confident it can deliver consistently at nameplate capacity and at expected grades. However, I would argue that Argonaut is the more likely takeover target here (providing two paths to a potential re-rating) and it's trading at a larger discount to fair value. To summarize, while Karora is a solid name and easily a top-5 junior producer, I continue to see more attractive bets elsewhere in the market like Argonaut Gold which has yet to participate in the sector-wide rally.

Argonaut Gold Weekly Chart - StockCharts.com

{kind=link}

Summary

Karora had another solid quarter in Q3, generating ~$13 million in free cash flow during its growth phase despite no contribution from its nickel production (timing of sales) and mining well below its reserve grade during the period. Meanwhile, the company has continued to enjoy exploration success across its property, with ~18% growth in M&I ounces (even without upcoming contribution from the Fletcher Shear Zone), and additional growth in its nickel resource to ~776,000 tonnes at 2.9% vs. ~745,000 tonnes at 2.8% previously. That said, some of this looks priced into the stock after a 110% rally off its September 2022 lows, and I continue to see more attractive reward/risk bets elsewhere in the sector. Hence, if this strength in Karora were to persist, I would view any rallies above US$4.02 before February as an opportunity to book some profits.

For further details see:

Karora Resources: Tracking Well Against FY2023 Guidance