GPRO - Key Takeaways From The GoPro Earnings Results

2023-08-07 14:24:14 ET

Summary

- GoPro's share price has declined by 45% since our last writing in June 2022, underperforming the market.

- The company's financial performance has deteriorated, with declining revenue, increasing expenses, resulting in a net loss for the quarter.

- Increased inventory levels and potential pull forward of revenues from future periods raise concerns about the company's future prospects.

- We maintain our "sell" rating.

GoPro, Inc. ( GPRO ) develops and sells cameras, mountable and wearable accessories, and subscription services and software in the Americas, Europe, the Middle East, Africa, the Asia and Pacific region, and internationally.

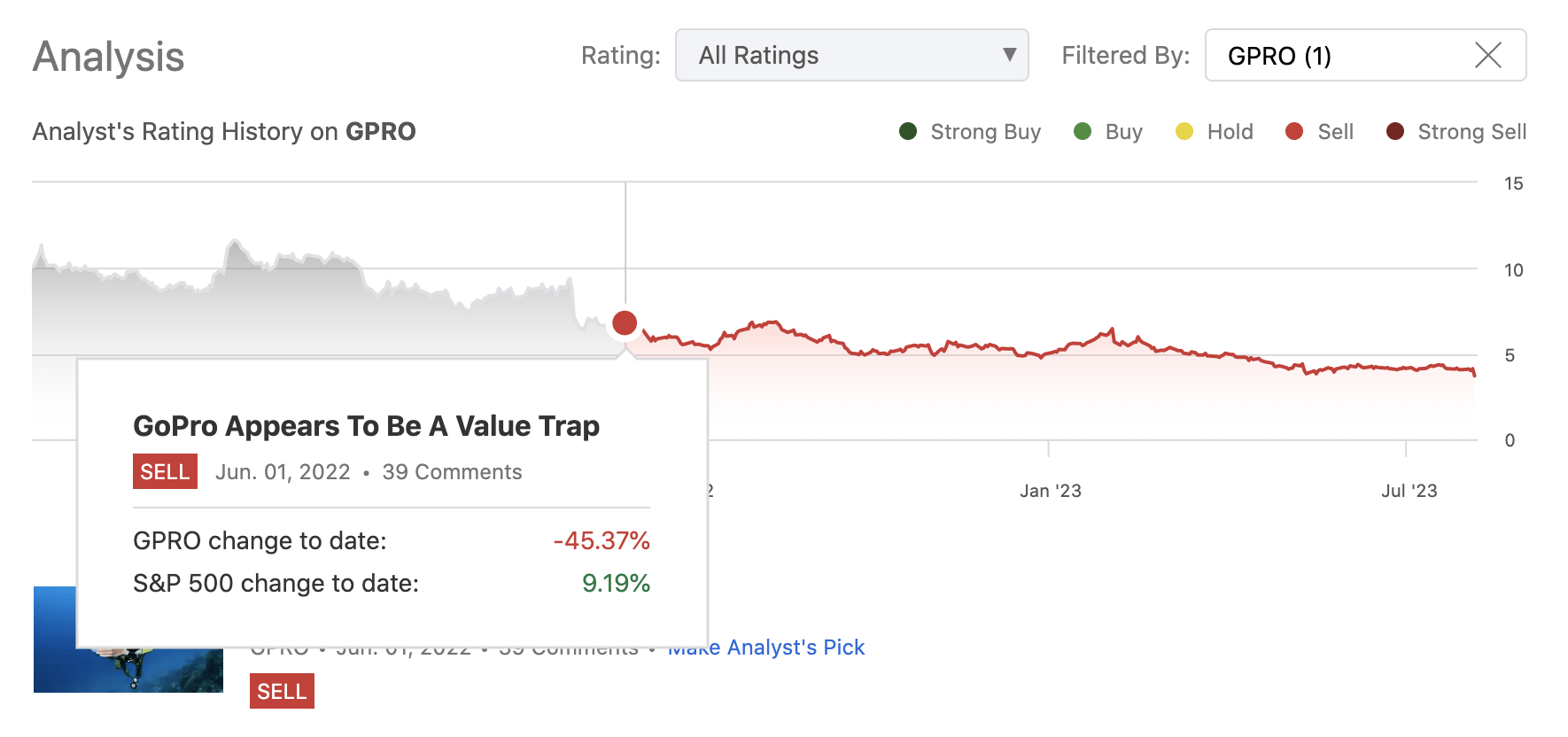

We initiated coverage on the firm in June 2022 with a "sell" rating, claiming that the investment opportunity may just be a value trap. So far, our thesis has been on target. Since our last writing , GPRO has declined by as much as 45%, significantly underperforming the broader market, which has gained 9% in the same time frame.

{kind=link}

Analysis history (Author)

Back then, we have claimed that the macroeconomic headwinds, including elevated inflation levels as well as poor consumer sentiment are likely to hurt GPRO's business in the near term. The increasing competition in the space has also made us somewhat concerned.

Today, we have decided to revisit GoPro and discuss the latest earnings results and its potential implications on our previous investment thesis.

Earnings results

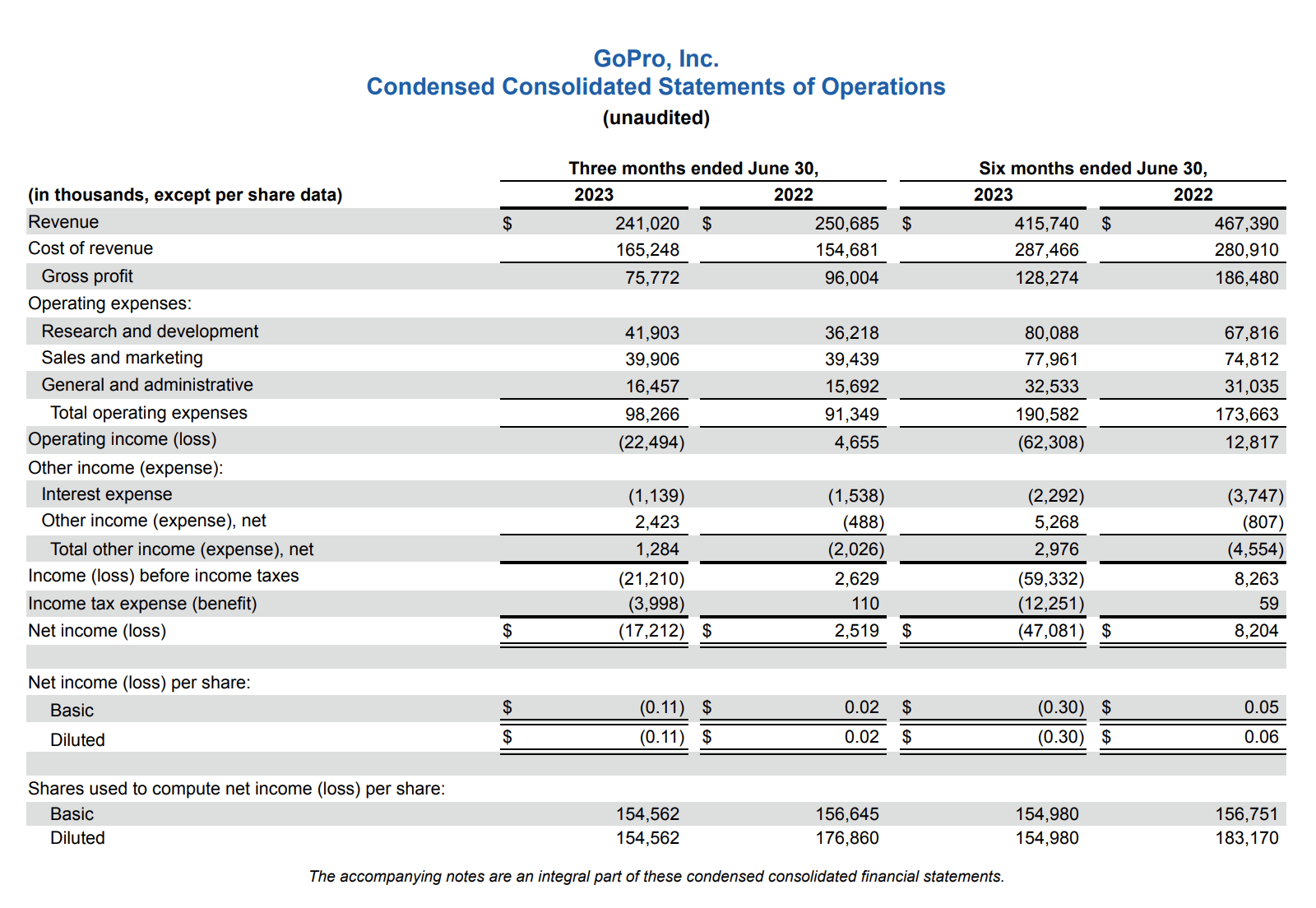

The very first thing that we need to mention is that when we wrote our last article, GoPro was still a profitable company. This is no longer the case today. Despite beating analyst estimates in terms of revenue and meeting expectations in terms of EPS, and achieving revenues above guidance, the deteriorating financial performance of the business is clearly visible.

Revenue has been declining year-over-year, while the cost of goods sold has increased meaningfully, resulting in gross margin contraction. R&D expenses along with SG&A expenses have also increased, leading to a significant operating loss, compared to an operating income a year ago. The poor operating performance has been slightly offset by some tax benefits, but the EPS turned out to be negative anyway.

The revenue decline can be attributed mainly to strategic pricing decisions and the shift in the camera revenue mix:

Revenue for the second quarter of 2023 was $241.0 million, or a 3.9% decrease from the same period in 2022, primarily driven by the impact of our strategic pricing decisions to reduce the manufacturer’s suggested retail price (MSRP) across our camera lineup, and a corresponding shift in camera revenue mix as we offered entry level cameras at a sub-$300 price point for the first time since 2019. The current entry level price point camera is also our lowest margin product and may remain low margin for the foreseeable future until we are able to replace it with a more cost-effective solution. As a result, our second quarter 2023 average selling price decreased 12.6% year-over-year to $342, and our second quarter 2023 camera revenue mix from cameras with an MSRP equal to or greater than $400 was 75% compared to 93% for the same period in 2022. These factors were partially offset by a 10.0% year-over-year increase in units shipped in the quarter to 704 thousand as unit volume from lower price point cameras experienced increased demand, which was in line with our strategic pricing objectives.

{kind=link}

Income statement (GPRO)

When we are evaluating the development of the revenue, we also need to see how the accounts receivable have developed. The following chart shows how the two metrics have been developing over the past four quarters.

It is clearly visible that accounts receivable have not been moving in line with the developments of the revenue. This may be an indication of potential revenue manipulation, as a result of artificially pulling demand forward from future periods.

Further, despite selling a larger number of units than in the same period in the prior year, there are still some troubling issues with inventory. So let us take a closer look at it.

Inventory

Despite the increased demand and higher sales volume for entry level cameras and the decline QoQ, inventory levels are still up YoY.

This increase has been mainly driven by the amount of finished goods, as shown in the following table.

{kind=link}

Inventory (GPRO)

In our opinion, this is not a too appealing development. Increased inventory levels, while demand is still not particularly strong, especially for higher end cameras, may lead to a need of further discounting to avoid certain goods becoming obsolete. This in turn can further hurt the margins, which are already being depressed.

All in all, there is nothing in these numbers and changes that could make our thesis more bullish than in our previous writing.

Looking ahead

It is also important to look forward and appreciate what the company expects and plans for the future to turn things around. So in order not to be overly pessimistic, let us take a look at the firm's visions and what could support these:

Driving profitability through improved efficiency, lower costs and better execution

While it is important to recognize that this is the right goal to achieve, we have to ask ourselves, will the firm be able to execute? On one hand, the firm appears to be optimistic:

We will continue to cultivate the partnerships with our distributors and retailers in order to further grow sales in the retail channel. Our expectation is sales from our retail channel will continue to increase relative to sales on GoPro.com . We have grown our subscribers and subscription revenue over the past several years and continue to make strategic decisions to enhance our subscription offerings, grow subscribers, and increase subscription revenue.

Also, the improving macroeconomic environment, including higher consumer confidence readings and moderating inflation levels may lead to strong demand for the firm's products in the near term.

But, there are two things to take into consideration. While inflation has indeed moderated, it remains uncertain how long it will still take to get back to historic levels. At the same time, the firm may struggle to pass on the additional costs to its customer, which is definitely bad news to for investors.

Some product costs have become subject to inflationary pressure and we may not be able to fully offset such higher costs through price increases. Our inability or failure to adjust pricing could harm our business, financial condition, and operating results.

Further, as the competition in the space is intense, GoPro will need to spend even more resources on marketing to make sure it can effectively differentiate its products, which may also hurt the bottom-line results even more. And then we are still not sure whether this differentiation will work or not.

We intend to focus our marketing resources to highlight our camera features, subscription and service benefits, and further improve brand recognition. Historically, our growth has largely been fueled by the adoption of our products by people looking to self-capture images of themselves participating in exciting physical activities.

To sum up

All in all, we believe that there is nothing in the latest earnings results that could make us optimistic enough about the firm's financial performance in the coming quarters, and therefore about upgrading our rating from the previously established "sell". Our outlook remains bearish.

While the firm has acknowledged that they need to improve their business to turn things around, including better product differentiation or addressing a wider variety of customers, it will cost significant amount of resources in the near term, potentially further hurting the bottom-line results of the business.

While the macroeconomic environment has somewhat improved, the remaining uncertainty and the fierce competition in the space do not make the execution of the strategic improvements/initiatives easy.

We maintain our "sell" rating.

For further details see:

Key Takeaways From The GoPro Earnings Results