BBBY - Kimco Provides Weak 2023 Guidance But Shares Remain Undervalued

Summary

- Kimco delivered excellent 2022 results, and a relatively decent Q4. What was somewhat disappointing was the weak 2023 guidance.

- The company should significantly benefit from the Albertsons monetization, and its strong balance sheet positions the company well to invest in growth.

- Shares appear undervalued, with a well-covered and attractive dividend yield, and trading at low P/FFO and P/CFO multiples.

After reviewing Kimco's ( KIM ) Q4 and full-year 2022 results, we maintain our opinion that shares are undervalued. The REIT saw strong leasing activity, which produced an increase in occupancy and positive leasing spreads, but same-site NOI growth was disappointing and higher interest expense caused funds from operations to go down 2.2% year over year to $0.38 per share in Q4.

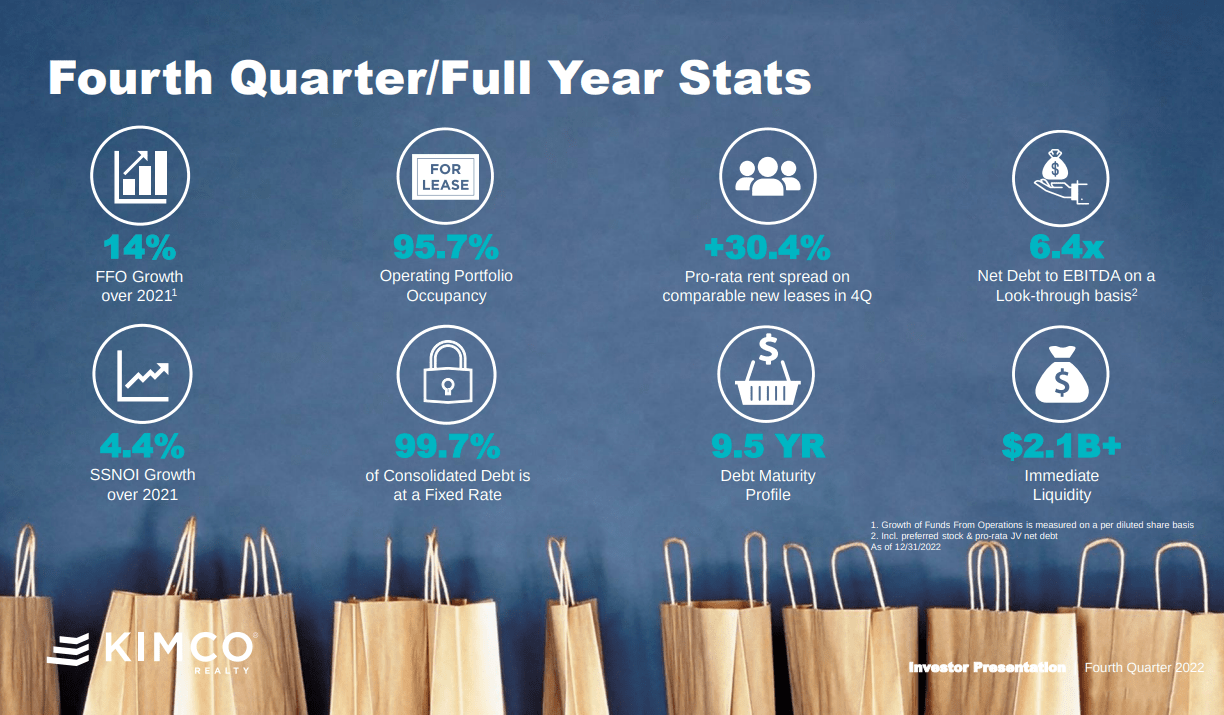

Occupancy ended the year at 95.7%, only 70 basis points below the company's all-time high. Year over year occupancy improved 130 basis points, which is quite remarkable, and the recovery has included small shops which are now at ~90%. In 2022, Kimco leased ~11.5 million square feet, which was a record for the company. New lease spread were very strong at 30.4%, including new grocery leases with Whole Foods ( AMZN ) and Albertsons ( ACI ). The spread on renewals and options was 4.6% during the quarter. Additional positive news included the fact that the percentage of annualized base rent from mixed-use assets is now over 13% and the company continues making good progress in the development of new apartment units.

There were also some bad news shared during the earnings call as well, such as the exposure to 25 Bed Bath & Beyond ( BBBY ) units. So far, Bed Bath & Beyond is planning to close six stores. Kimco is taking quick action and already has two leases executed for those locations, two ready for execution, and two on active negotiations. Still, the company is expecting high credit losses for the year, ranging from $15 million to $22 million. Additional bad news include expectations that interest expense will go up in 2023 compared to 2022.

Looking at the big picture, Kimco continues to trade with a relatively high dividend yield of ~4.2%, which is very well covered by FFO. Its valuation is very reasonable, trading at a forward P/FFO of ~14x, the balance sheet is very strong, and the company will have significant liquidity coming in from its Albertsons investment. Kimco already monetized $301 million by selling 11.5 million ACI shares and still has 28 million shares under lock-up until May 16, 2023. Kimco also received a $194 million special cash dividend received in January 2023 and is assuming further monetization of this investment of ~$300 million in 2023. What this means for investors is that Kimco will probably not have to issue any equity this year to finance growth.

Q4 and FY2022 Results

In Q4, FFO was $234 million or $0.38 per diluted share, which was less than the $240 million or $0.39 per diluted share it delivered in the fourth quarter of 2021. The main reason for this disappointing result was that the modest NOI increase was offset by higher interest expense.

Same-site NOI growth was 1.9% in the fourth quarter of 2022, while full year 2022 same-site NOI growth was much better at 4.4%.

{kind=link}

Kimco Investor Presentation

Leasing spreads were quite healthy in Q4, at ~8.7%. As already mentioned, they were particularly strong for new leases. The strong leasing performance by the company is one of the key reasons why we remain optimistic on Kimco's prospects.

Kimco Investor Presentation

FFO Growth Drivers

Kimco continues to benefit from some tailwinds, such as relatively low new retail developments in first-ring suburban markets, and new store openings currently outpacing store closings.

Kimco Investor Presentation

Kimco has several FFO growth drivers, including rent bumps, leasing and mark to market opportunities, its development and re-development pipeline, reinvestment of the Albertsons monetization, and accretive acquisitions. It should also benefit from the tailwind resulting from its economic occupancy spread of 260 basis points. This represents approximately $43 million of annual base rent that is not yet contributing to cash flow. Approximately $21 million of this spread is expected to start contributing to cash flow by the end of 2023.

Kimco Investor Presentation

Balance Sheet

Kimco currently has the strongest liquidity in the company's history with $150 million in cash, and full availability from its $2 billion revolving credit facility. It should also benefit from continued monetization of the Albertsons investment.

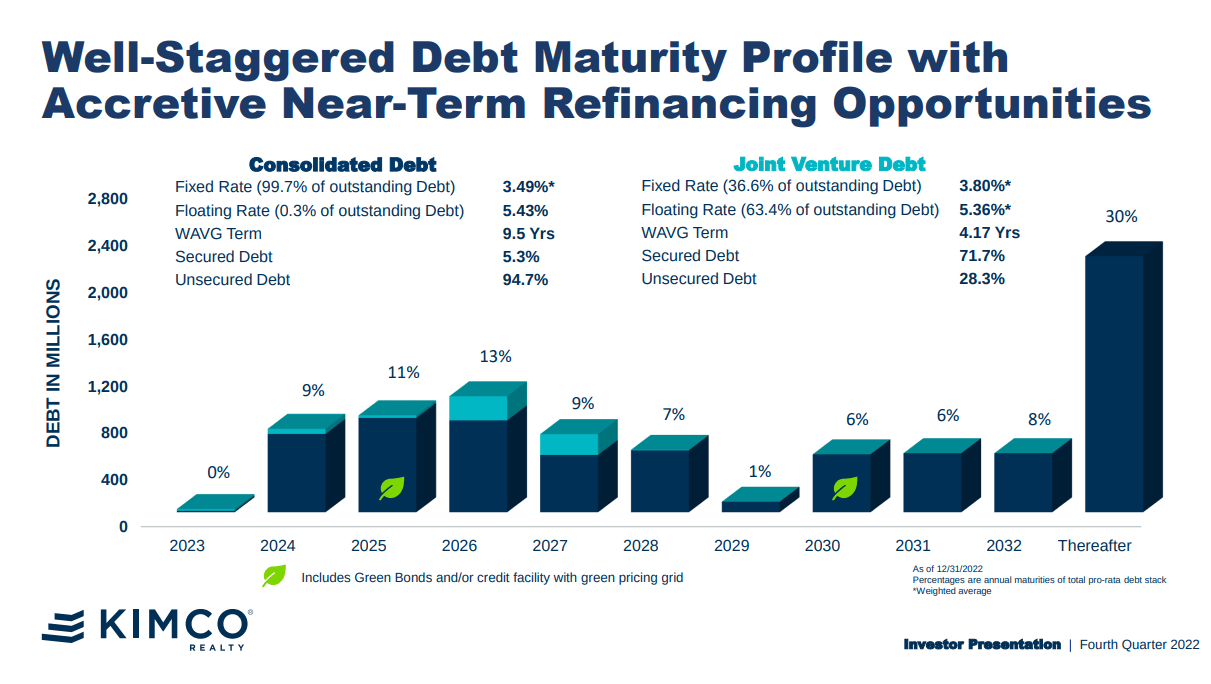

At year end, its look through net debt to EBITDA, which includes their pro rata share of joint venture debt and preferred stock outstanding, was 6.4x and represents an improvement of 0.2x from the 6.6x level at the end of 2021. Kimco has a weighted average debt maturity of 9.5 years, and only $50 million of mortgage debt will be maturing in 2023.

{kind=link}

Kimco Investor Presentation

Guidance

Guidance for 2023 was somewhat disappointing, and the company expects some headwinds due to higher levels of credit losses and higher interest expense compared to last year. For 2023 FFO per share is guided in the range of $1.53 to $1.57. This guidance assumes positive same-site NOI growth of between 1% to 2%, which includes a credit loss assumption ranging from $15 million to $22 million. Importantly, the $194 million special dividend received in January will not be included in FFO. After dividends and CapEx, free cash flow expectation is around $150 million for 2023.

Valuation

With a well-covered ~4.2% dividend yield, and trading at only a ~14x multiple of expected 2023 FFO, we believe Kimco's valuation remains undemanding. After a period of strong recovery following the Covid crisis, growth appears to be stalling. Still, at the current valuation, we do not believe investors are assuming much growth in any case. The price to cash flow from operations remains below the ten-year average.

Average analyst estimates for 2024 FFO is modestly higher compared to 2023, at $1.65 per share, and $1.71 for 2025. We think these are reasonable estimates based on the positive developments on leasing and occupancy, the reinvestment of the Albertsons monetization, re-investment of the free cash flow, partially offset by higher credit losses and higher interest expense. Adding the dividend yield and a potential 3-5% in FFO growth for the next few years, we believe Kimco is priced to deliver long-term investors with a high single-digit total return.

Seeking Alpha

Risks

In the short to medium term, we believe the biggest risk for Kimco investors is a potential recession. That could reverse some of the occupancy gains the company has made in recent years, especially in the small shop category. Longer-term, some of the company's tenants will continue to face headwinds from e-commerce continuing to take market share, as well as the risk of interest rates remaining high for longer than expected, resulting in the company having to refinance much of its debt at higher rates.

Conclusion

Kimco delivered excellent 2022 results, and a relatively decent Q4. What was somewhat disappointing was the weak 2023 guidance, but we believe the company is being very conservative. Shares appear undervalued, with a well-covered and attractive dividend yield, and trading at low P/FFO and P/CFO multiples. Other positives include the Albertsons monetization, a very strong balance sheet, and very strong leasing performance. Based on the most recent results, and the relatively low valuation, we are maintaining our 'Buy' rating.

For further details see:

Kimco Provides Weak 2023 Guidance, But Shares Remain Undervalued