ET - Kinder Morgan: An Appealing Prospect That Has Fuel For Additional Acquisitions

2023-11-20 15:13:58 ET

Summary

- Kinder Morgan, Inc. has announced acquisition of South Texas assets for $1.815 billion, expanding its exposure to natural gas.

- The acquisition is highly complementary to Kinder Morgan's existing footprint in South Texas and offers stable cash flow through take-or-pay contracts.

- Despite mixed financial results recently, Kinder Morgan remains healthy and attractively priced compared to similar enterprises. The bullish thesis still holds.

One of the companies in the midstream/pipeline space that I am most familiar with is Kinder Morgan, Inc. ( KMI ). I have been writing about the company for this platform since 2016. And in the most recent article that I published about the firm, which came out in August of this year, I rated the enterprise a "Buy." Although relative to similar enterprises KMI shares are not exactly cheap, they do look affordable on an absolute basis.

At that time, the company was experiencing some weakness in some key areas. But for the most part, it looked attractive from a valuation perspective. Leverage had been decreasing and management continued to invest in growing the business. Now, three months later, we have yet another acquisition that the company agreed to and updated cash flow figures to account not only for that but for industry conditions more broadly. And while the stock has only remained flat while the S&P 500 (SP500) increased by 1.8%, these data points do suggest to me that the bullish thesis is still very much deserving of consideration.

A new purchase

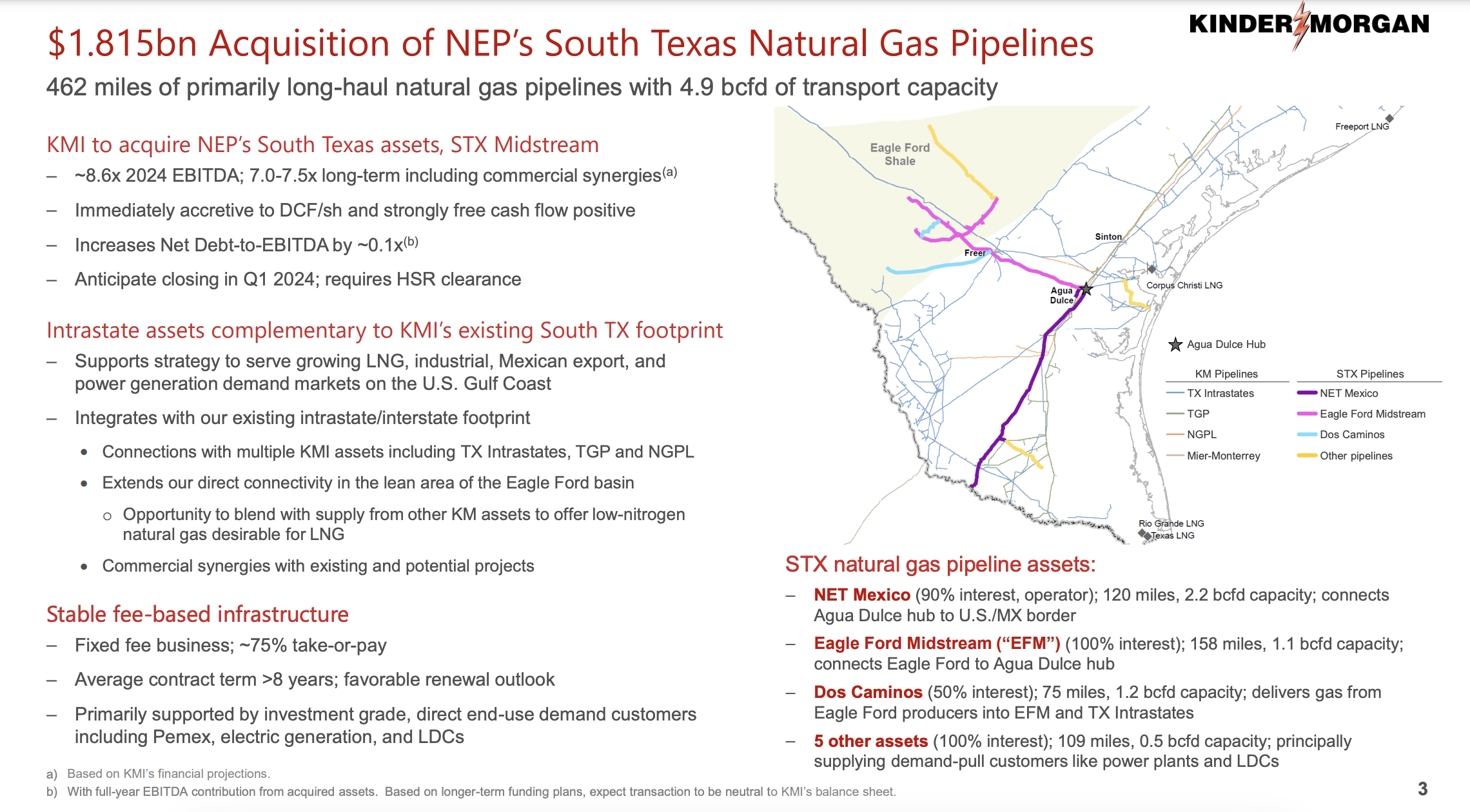

Although I did not mention it in my last article on Kinder Morgan, I do recall thinking recently that management might be ready to make another acquisition. The firm's long-term net leverage target is a ratio of 4.5. And management recently stated that they anticipate net leverage to be around 4 by the end of this year. That means that the company could add on up to another $3.85 billion in net debt before reaching its target.

{kind=link}

Lo and behold, on November 6th, management announced a new purchase. This particular acquisition is of the South Texas assets currently owned by NextEra Energy Partners ( NEP ). Those assets are known as STX Midstream and they consist of a pipeline system that stretches 462 miles and that largely handles the transportation of natural gas. In fact, it handles an estimate of 4.9 billion cubic feet per day worth of the commodity. This furthers the company's exposure to natural gas, which is fine because 62% of the company's business is already focused on that particular commodity.

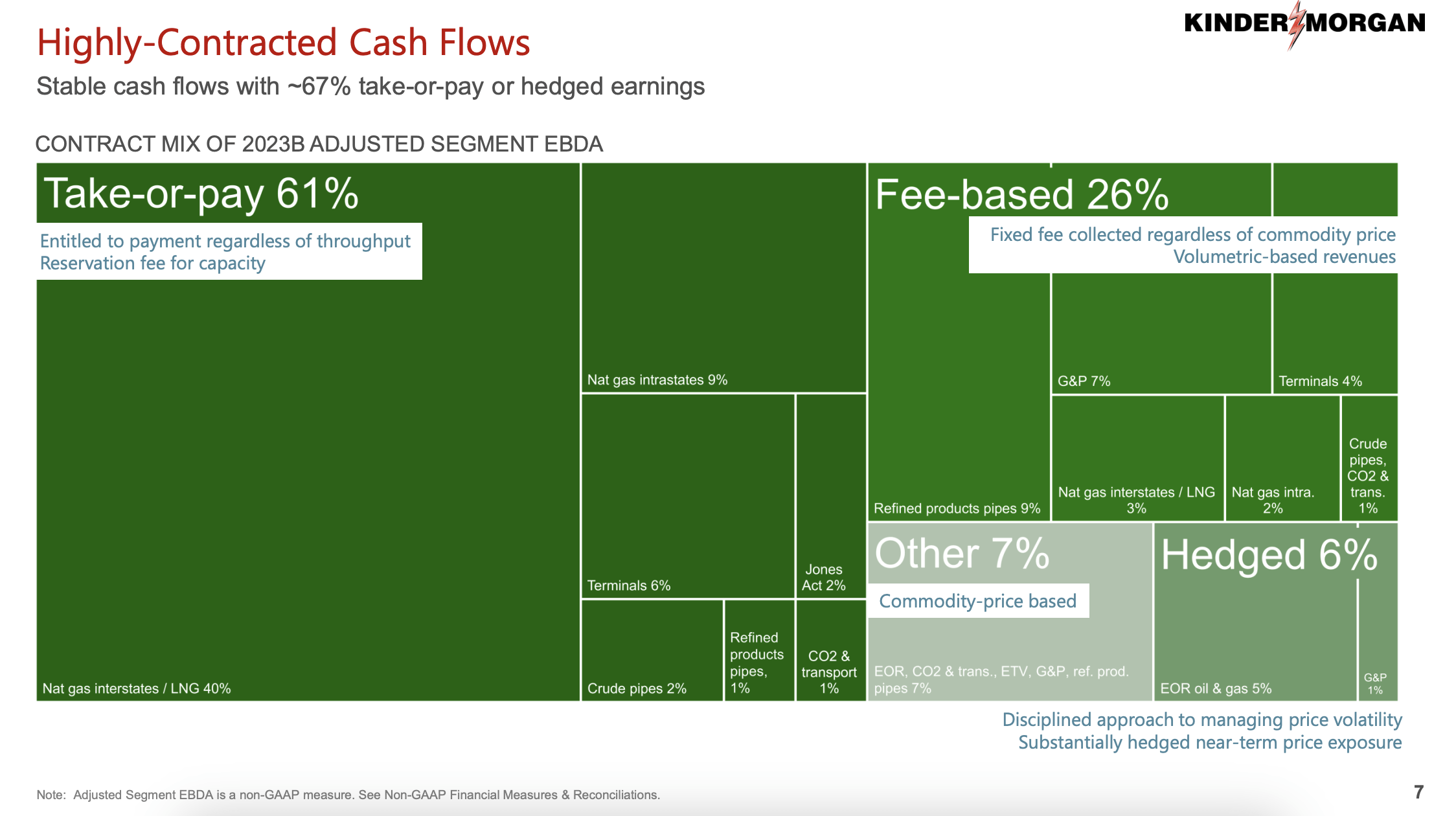

The great thing for shareholders is that this is an asset that is highly complementary to Kinder Morgan’s existing physical footprint in South Texas. It also, because of this, gives the enterprise the opportunity to blend with supply from other Kinder Morgan in order to offer low nitrogen natural gas that is desirable for LNG production. About 75% of the fees associated with this business are take-or-pay. This is great for the company because 61% of its EBITDA estimated for 2023 falls under that same category. For those who don't know, take-or-pay contracts entitle the company to receive payment for its services irrespective of the amount of product that passes through its pipelines. This provides tremendous stability from a cash flow perspective, especially when you add on top of this the 6% of EBITDA that Kinder Morgan is expected to generate that is hedged and the 26% that is based on fixed fees that are collected no matter what commodity prices happened to be but that are volume-specific.

{kind=link}

This transaction is expected to close in the first quarter of 2024. The reason for that wait is because it does require certain regulatory clearances. Assuming it does close, the agreed-upon purchase price is $1.815 billion, which will be paid all in cash. Management stated that the acquisition will be financed with a combination of cash on hand and short-term borrowings. Realistically, none of it will be done with cash because the company only has $97 million in cash and cash equivalents on its books. So investors should anticipate debt increasing by the purchase price, give or take several million dollars.

Based on the data currently provided, this particular purchase is being done at an EV to EBITDA multiple of 8.6. That's based on estimates for 2024. That implies EBITDA of $211 million. However, management does believe that the long-term multiple will be somewhere between 7 and 7.5. That would translate to EBITDA of between $242 million and $259 million. For the purpose of this analysis, I will stick with the $211 million figure. We don't know what the interest expense associated with the debt will be. I looked at the credit facilities that Kinder Morgan has. But none of them have any drawn amounts.

So, instead, I looked at a similar firm, Energy Transfer ( ET ) to see what it is paying on its primary credit facility. For the most recent quarter, we get a reading of 6.29%. If we apply this to the purchase price and assume no taxes are involved, this purchase should add around $97 million in operating cash flow to Kinder Morgan.

Kinder Morgan is still healthy

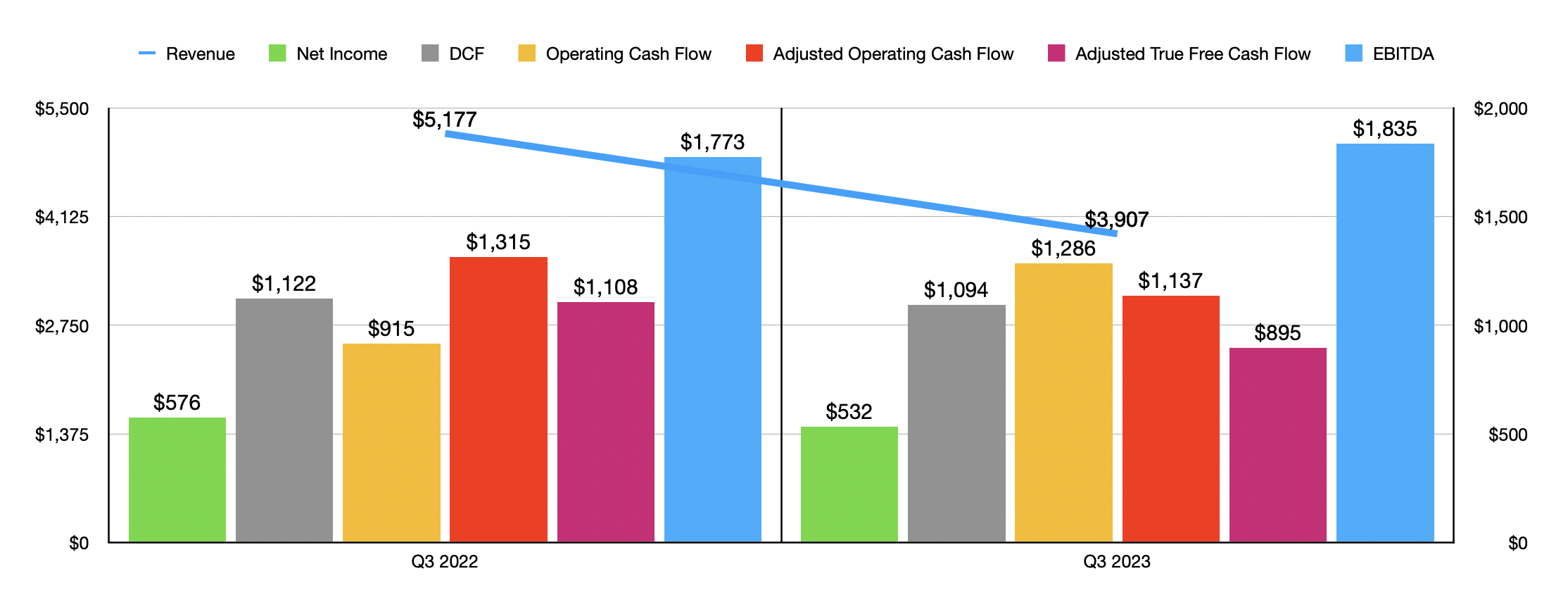

Moving away from the acquisition that was announced earlier this month, I would like to focus some on the core business that is Kinder Morgan. Based on the most recent data provided by management, the company seems to be quite healthy. This is not to say that everything is perfect. As an example, I would like to point you to the chart below. In it, you can see recent financial data covering the third quarter of the current fiscal year compared to the same time last year.

{kind=link}

Given the nature of firms in this space, revenue is not terribly significant. Rather, we should be focusing on the cash flow figures. These seem to be rather mixed. DCF, or distributable cash flow, fell from $1.12 billion last year to $1.09 billion this year. While operating cash flow grew from $915 million to $1.29 billion, on an adjusted basis it actually fell from $1.32 billion to $1.14 billion. There is one metric that I like to add into companies like this. This is what I refer to as the "true free cash flow" of the enterprise. This is essentially what we get when we take adjusted operating cash flow and strip out maintenance capital expenditures so as not to punish the company for its growth initiatives. This also fell year-over-year from $1.11 billion to $895 million. On the other hand, EBITDA for the firm grew from $1.77 billion to $1.84 billion.

{kind=link}

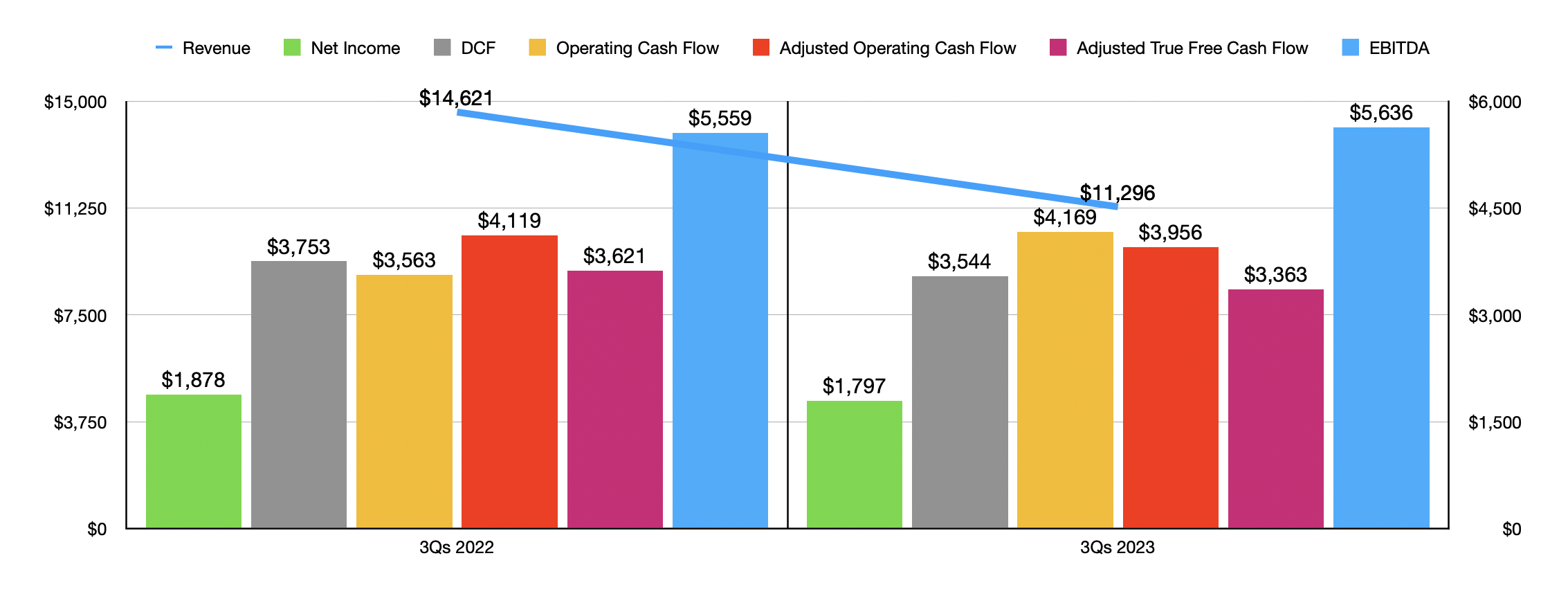

In the chart above, you can see financial data covering the first nine months of this year relative to the same time last year. The numbers do well to speak for themselves. But the important thing to keep in mind is that they, just like with the third quarter, are quite mixed. I would like to note that one thing that the numbers do suggest is that the company is still incredibly healthy. Its distribution, for instance, is comfortably covered. In fact, only 53.6% of the company's DCF and 48% of its adjusted operating cash flow are required to cover the distribution. So even if we do see some volatility, the business still has plenty of cash flow to do well for itself.

{kind=link}

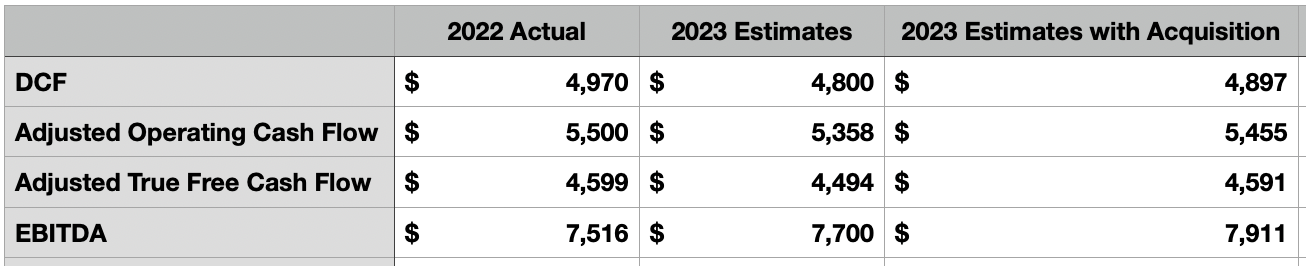

For the 2023 fiscal year, management has provided some guidance. They currently expect, for instance, for the DCF of the business to be $4.8 billion and for EBITDA to be $7.7 billion. No estimates were provided for operating cash flow. But based on my own estimates, adjusted operating cash flow should be just under $5.4 billion, while ‘adjusted true free cash flow’ should be just under $4.5 billion if we take management's guidance for maintenance capital expenditures of $864 million as accurate.

{kind=link}

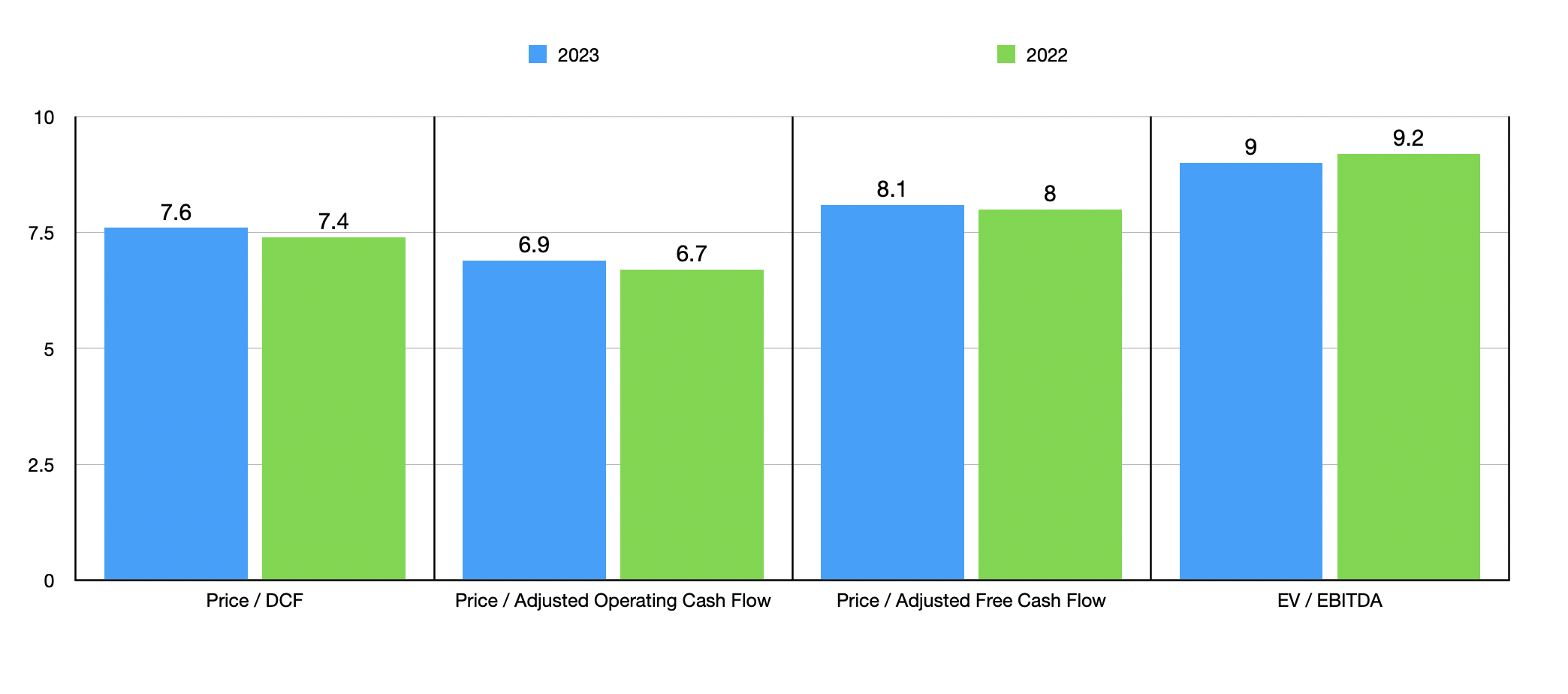

Using these figures, I was unable to value the company as shown in the chart above. Added to these figures is the estimated cash flow associated with the newest purchase and, naturally, the debt associated with it as well. I also included that on a pro forma basis for the purpose of valuing the company using 2022 figures. As you can see, in three out of the four cases I looked at, the stock is a bit more expensive on a forward basis than if we were to use data from last year. But the stock is still attractively priced nonetheless. I then, in the table below, took two of the metrics and compared Kinder Morgan with five similar enterprises. On a price to operating cash flow basis, three of the five companies were cheaper than it. But this number drops to two of the five if we use the EV to EBITDA approach.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Kinder Morgan |

| 6.9 |

| 9.0 |

| The Williams Companies ( WMB ) |

| 8.1 |

| 9.7 |

| Energy Transfer |

| 4.4 |

| 8.2 |

| Cheniere ( LNG ) |

| 4.4 |

| 3.1 |

| MPLX Inc. ( MPLX ) |

| 6.8 |

| 9.7 |

| Enterprise Products Partners ( EPD ) |

| 7.3 |

| 9.7 |

Takeaway

Fundamentally speaking, Kinder Morgan is doing quite well for itself. It is not my favorite player in the space by any means. That spot belongs to Energy Transfer, a company that I have a significant amount of my current worth in. But Kinder Morgan, Inc. stock is attractively priced on an absolute basis and is more or less fairly valued compared to similar enterprises.

I would also like to note that the aforementioned acquisition is, even in the worst case, priced a bit cheaper than Kinder Morgan as a whole, so acquiring it using cash was logical and the purchase in its entirety should be accretive to shareholder value in the long run. Add all of this stuff together, and I do still believe that the "Buy" rating I assigned Kinder Morgan previously holds.

For further details see:

Kinder Morgan: An Appealing Prospect That Has Fuel For Additional Acquisitions