CA - Kinross Gold: Getting Saved By The Gold Price

2023-04-10 09:40:55 ET

Summary

- Kinross has significantly lagged its peers over the past two years, but switched to outperformance in Q1 with a higher gold price and lower oil prices working in its favor.

- Fortunately, these trends have continued into Q2, with the oil price remaining below its assumption of $90.00/barrel and a strong bid remaining under the gold price.

- These two tailwinds should allow KGC to generate over $200 million in free cash flow this year and continue its share repurchases, a more favorable outlook than two months ago.

- That said, the stock is short-term extended and trading only 10% below its historical cash flow multiple, suggesting there are more attractive bets from a relative value standpoint elsewhere in the sector.

The Q4 Earnings Season for the Gold Miners Index ( GDX ) is finally over and it was a disappointing earnings season overall. Not only did several miners miss output guidance, but delivery against cost guidance was not what investors were hoping for, with many gold producers forced to move the goalposts (guidance range) entirely. In fairness, the cost misses were related to stickier than expected inflationary pressures and some miners had tougher years due to supply chain headwinds. That said, the result was that average AISC margins shrunk to ~$510/oz for the year, and have declined over 30% from FY2020 levels despite the slightly higher gold price reported on a two-year basis.

Kinross Gold ( KGC ) was one name that came up short of guidance in the million-ounce producer space, with FY2022 production of ~1.96 million attributable gold-equivalent ounces, marking the third consecutive year of missing its guidance. Meanwhile, costs came in higher than expected ($1,271/oz vs. guidance of $1,150/oz), resulting in a nearly 12% increase in all-in sustaining costs [AISC] year-over-year with the loss of high-margin ounces at Kupol (divested), inflationary pressures, and the slower ramp-up at La Coipa. Fortunately, while Kinross was set up for another year of margin compression, it's getting saved by the gold price, like Equinox Gold ( EQX ), which should help it deleverage and post more respectable margins in 2023. Let's dig into the annual results and the forward outlook below:

Q4 & FY2022 Results

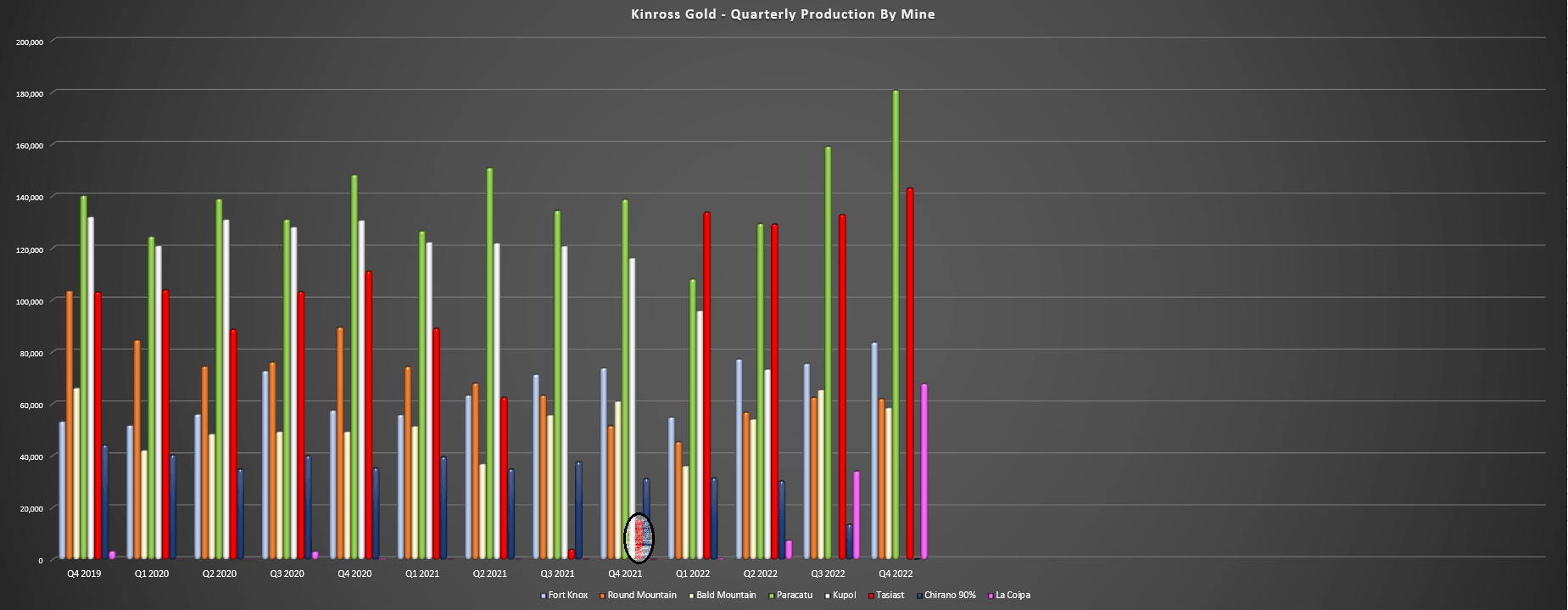

Kinross reported its Q4 and FY2022 results in mid-February, reporting quarterly production of ~595,700 gold-equivalent ounces [GEOs], a significant increase from the year-ago period. However, this was a very noisy quarter from a comparison standpoint, with a tailwind from easy comps at Tasiast following a mill fire last summer and subsequent temporary suspension of operations (Q4 2021 production: 15,300 ounces), easy comps at Round Mountain (Q4 2021 production: ~51,500 ounces), and La Coipa being brought online (no contribution in Q4 2021). A ~147,300 ounce headwind from the divestment of Kupol and Chirano offset these tailwinds but Kinross had a tailwind on balance, with two mines barely contributing/not contributing (Tasiast, La Coipa) and Round Mountain having a very weak quarter.

Kinross - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

So, while Kinross showed significant production growth on a year-over-year basis and there's no disputing that Paracatu and Tasiast had monster quarters with combined production of ~324,000 ounces in Q4 2022, the results were less impressive than they might have looked from a headline standpoint. In fact, production guidance for its Americas region provided in Q1 2022 was ~1.53 million GEOs, and production came up well short at just ~1.42 million GEOs for the year. As noted, this was related to delays in the mill ramp-up at La Coipa, impacted by issues with pumps and supply chain headwinds that affected spare part availability. The result was that Kinross reported its lowest production year since 2008, despite a monster quarter from its two cornerstone assets in Brazil and Mauritania.

The good news is that La Coipa had a strong finish to the year to produce ~109,600 GEOs, Tasiast reported record production and grades in Q4 with ~1.63 million tonnes processed at 3.21 grams per tonne of gold (~143,000 ounces produced), and Paracatu had a massive quarter with ~13.3 million tonnes of ore mined at an average grade of 0.50 grams per tonne of gold. This increased volume translated to Q4 revenue of ~$1.07 billion despite a weaker average realized gold price ($1,732/oz). And even more importantly, the Tasiast 24k Expansion is making solid progress, with Kinross expecting the 24,000 tonne per day goal to be met by summer with consistent throughput at this level by year-end. Plus, the completion of the 34 MW Tasiast Solar Plant is expected in H2-2023, helping to displace some diesel usage at the operation.

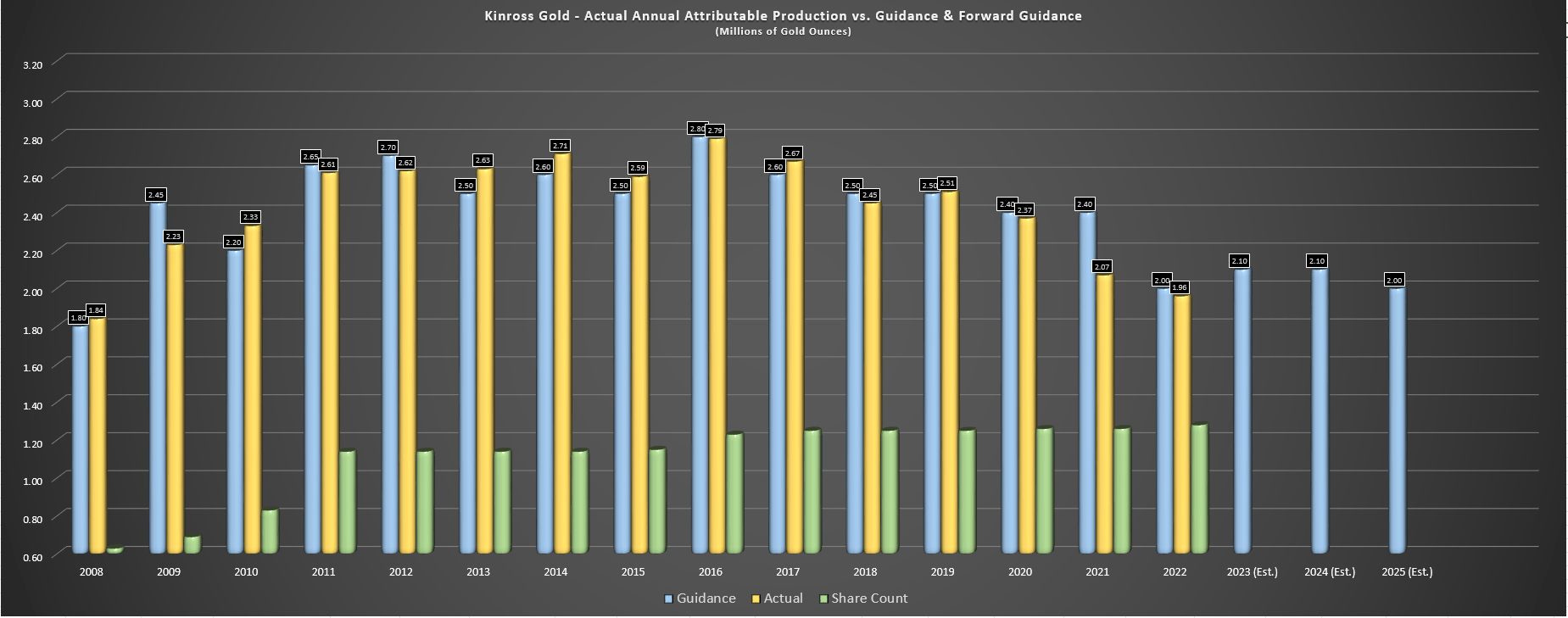

Kinross - Actual Annual Attributable Production vs. Guidance & Forward Guidance (Company Filings, Author's Chart)

{kind=link}

That said, the trend in gold production is not great from a big picture standpoint, with the company's weighted average annual share count doubling since 2008 with only a ~9% increase in annual gold production. Plus, this trend isn't expected to improve much with Kupol, Udinsk, and Chirano out of the picture, with the previous outlook of ~2.80 million GEOs in FY2023 cut down to ~2.0 million GEOs based on current guidance. If we look ahead to FY2025 and the rest of the decade, the outlook isn't any more exciting, with Kinross previously expecting to average at least 2.5 million attributable GEOs per annum looking out to 2030, with the new outlook being ~2.0 to ~2.2 million GEOs from now until 2028, depending on if Phase W3 and Phase S are approved (Round Mountain), and if La Coipa's mine life can be increased given that grades at Tasiast will trend lower even if the grade profile is smoothed out vs. the 2019 Technical Report assumptions.

{kind=link}

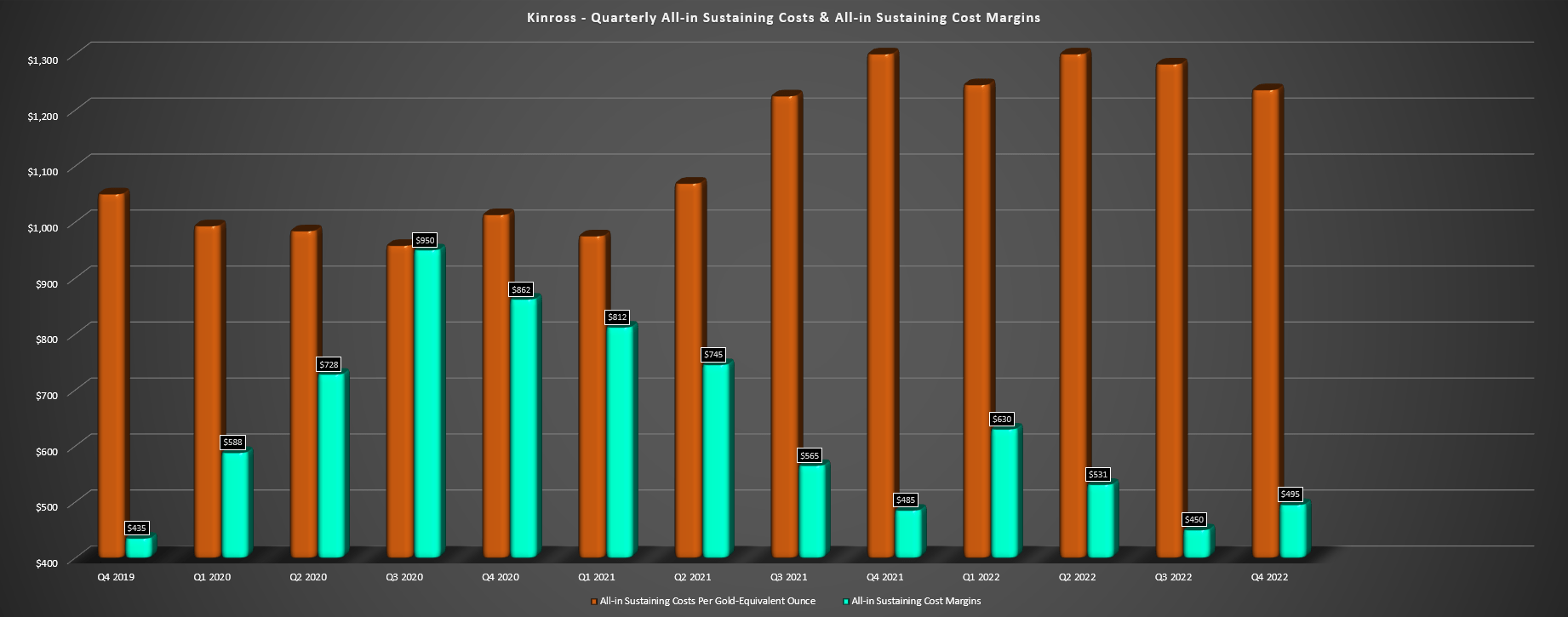

Looking at Kinross' costs and margins, 2022 wasn't much better. As shown below, Q4 2022 AISC came in at $1,282/oz (down 2% year-over-year but up against easy comps), and FY2022 AISC came in at $1,271/oz, a nearly 12% increase from the year-ago period. The increased in operating costs was related to inflationary pressures across the portfolio (and the divestment of the low-cost Kupol Mine), with high-volume and low-grade operations impacted heavily, of which Kinross has several operations (Round Mountain, Bald Mountain, Fort Knox, Paracatu). Meanwhile, Q4 2022 AISC margins sunk to $495/oz, one of the weakest figures over the past three years (Q4 2019: $435/oz), and FY2022 AISC margins came in at $522/oz vs. $787/oz in FY2020, a considerable decline.

Kinross - Quarterly AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

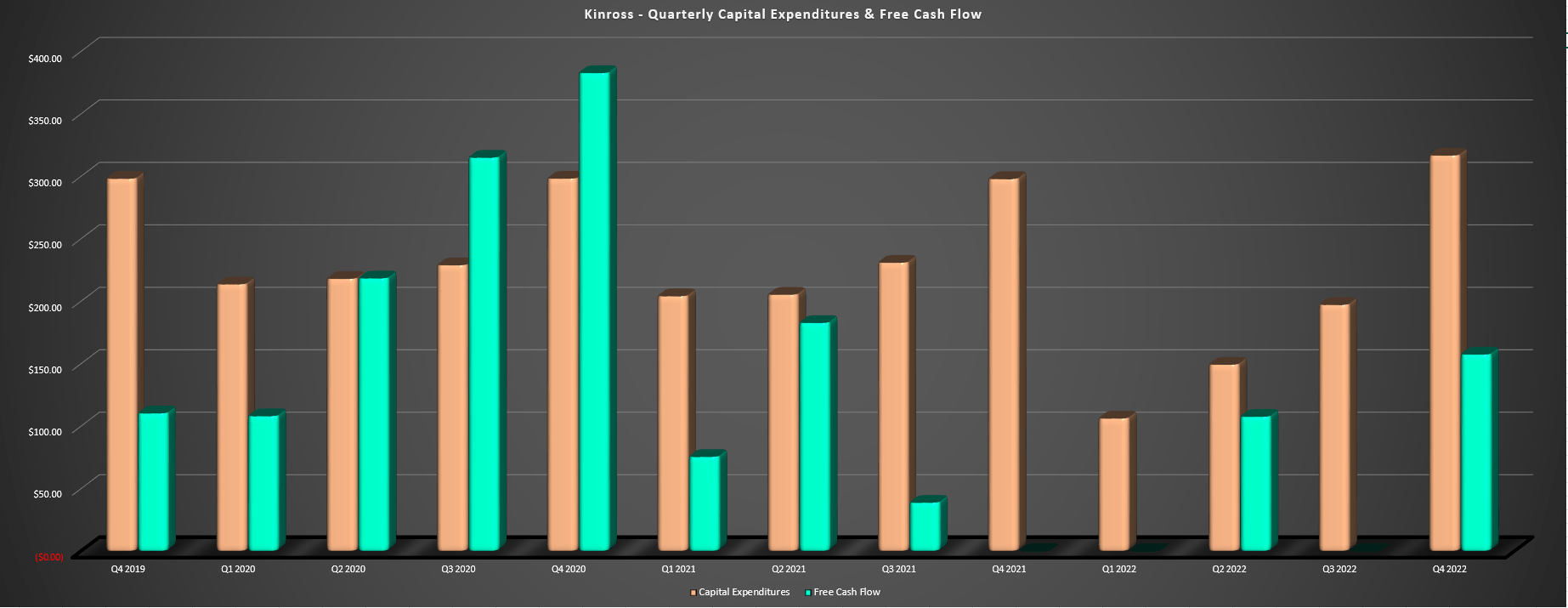

Given the higher cost profile and lower sales volumes, Kinross may have put together a solid quarter from a free cash flow standpoint in Q4 with Paracatu and Tasiast firing on all cylinders, but FY2022 free cash flow came in at just $238.3 million, down from ~$1.04 billion in FY2020. The silver lining is that the weaker financial results and significant dent to forward guidance following the divestments has created a company with a better overall jurisdictional profile and the weakness in the stock allowed the company to repurchase ~$300 million in shares at depressed prices, with room for further buybacks in FY2023 if we see a strong bid under the gold price.

FY2023 Outlook

Heading into February, I noted that Kinross' FY2022 reserve and resource update was disappointing, and that I wouldn't become interested unless the stock dipped to US$3.30. This was because there was the possibility that Kinross could see further margin compression in FY2023 if the gold price didn't cooperate, and its maiden resource at Great Bear came in much softer than I expected, and it also struggled to replace reserves, a clear divergence vs. Barrick Gold ( GOLD ) which posted strong reserve and resource growth. While the stock declined another 10% from US$3.78, it narrowly missed my US$3.30 target and it's clear that I was a little too picky in hoping that we might see a retrace below US$3.30. In fact, the stock has launched higher since, up over 30% since late February.

{kind=link}

Regarding the recent strength in the stock, I believe this is a case of leverage working both ways and the gold price swinging heavily in the company's favor. This is because Kinross had little hope of completing additional buybacks and in a $1,650/oz to $1,750/oz gold price environment, and was actually one of the riskier million-ounce producers, with a significant net debt position like Evolution Mining ( CAHPF ), its cash cow (Kupol) being sold off for a song, but much weaker margins than Evolution. This is evidenced by Kinross noting that FY2023 AISC were expected to come in at $1,320/oz (+5% year-over-year vs. $1,271/oz in FY2022). Assuming a conservative $1,750/oz gold price, this would cause AISC margins to decline further to $430/oz.

{kind=link}

Fortunately, much has changed over the past month. The main tailwind is a higher gold price that's conveniently been coupled with a lower oil price, resulting in a significant change in its FY2023 margin outlook. And even if we assume an average realized gold price of $1,900/oz and FY2023 all-in sustaining costs of $1,300/oz, Kinross should see AISC margins improve to $600/oz, a 15% increase from the year-ago period. If the gold price averages $1,950/oz in FY2023, AISC margins would improve to $650/oz (+25% year-over-year). Given that the gold price has averaged $1,880/oz year-to-date, I don't think an average realized gold price of $1,900/oz is a stretch, suggesting a much better year than previously expected for Kinross.

While Q1 is expected to be much softer due to the shutdown at Tasiast (related to 24k Expansion), a planned mill shutdown at La Coipa and seasonal factors in Brazil and Nevada which will lead to higher AISC and a sequential decline in free cash flow, we should see a much better performance for the remainder of the year. This is because the higher gold price should more than offset the impact of a full year of inflationary pressures, with the potential for Kinross to generate upwards of $1.3 billion in operating cash flow, resulting in annual free cash flow of ~$300 million assuming it spends all of its expected $1.0 billion in annual capex. While this isn't very significant for a company with a ~$8.4 billion enterprise value (~3.6% free cash flow yield), it is worth noting that we should see improved free cash flow in 2024, and this outlook is certainly welcome relative to a previous outlook of negative free cash flow in 2023.

Kinross - Quarterly Capex & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

So, is the stock a Buy?

Based on ~1,220 million shares and a share price of US$5.05, Kinross trades at a market cap of ~$6.16 billion and an enterprise value of ~$8.34 billion. Even under more bullish assumptions that Kinross generates $1.27 billion in cash flow this year ($1.05 per share), the stock is currently trading at ~4.8x forward cash flow vs. a historical multiple of ~5.20x cash flow (10-year average). Given the improvement in its jurisdictional profile (Russia exit) offset by higher costs than its peer group, I believe a fair multiple for the stock is 6.0x - 6.50x cash flow. If we use the low end and multiply this figure by FY2023 cash flow estimates of $1.05, Kinross' fair value comes in at US$6.30.

{kind=link}

Although this translates to 24% upside from current levels, I require a minimum 40% discount to fair value for mid-cap gold producers given that I want to ensure a significant margin of safety. In Kinross' case and given its declining production profile on a per share basis and arguably less capital discipline (over-paying for Great Bear at a cyclical peak for some many gold developers), one could argue that a 45% discount is more suitable as investors can't rule out negative surprises here vs. other producers like Barrick and Agnico Eagle Mines ( AEM ) that have extreme capital discipline and do not engage in over-priced M&A. Still, even if we use a 40% discount, Kinross' ideal buy zone would come in at US$3.80.

As evidence of over-priced M&A, Kinross paid ~$170.00/oz for M&I resources at Great Bear even if 8.5 million ounces are proven up in the M&I category vs. Agnico which paid ~$60.00/oz for M&I resources in a jurisdiction it's already present and with existing infrastructure when it acquired TMac Resources to scoop up Hope Bay and an 80-kilometer greenstone belt.

Obviously, there's no guarantee that the stock drops back to these levels, and it's quite possible that the new floor for KGC is US$4.00 per share given that it came into 2023 at depressed levels and is armed with a massive buyback program that can be put to use if the gold price holds up here (75% of excess cash directed to share buybacks). Still, the price it will be buying back shares is unfortunately less attractive following the recent rally and when it comes to sector laggards, I prefer to pay the right price or pass entirely. Besides, this recent rally in Kinross has left the stock hanging out in the upper portion of its support/resistance range and just shy of resistance at US$5.25. So, from a technical standpoint, the reward/risk is much less favorable here.

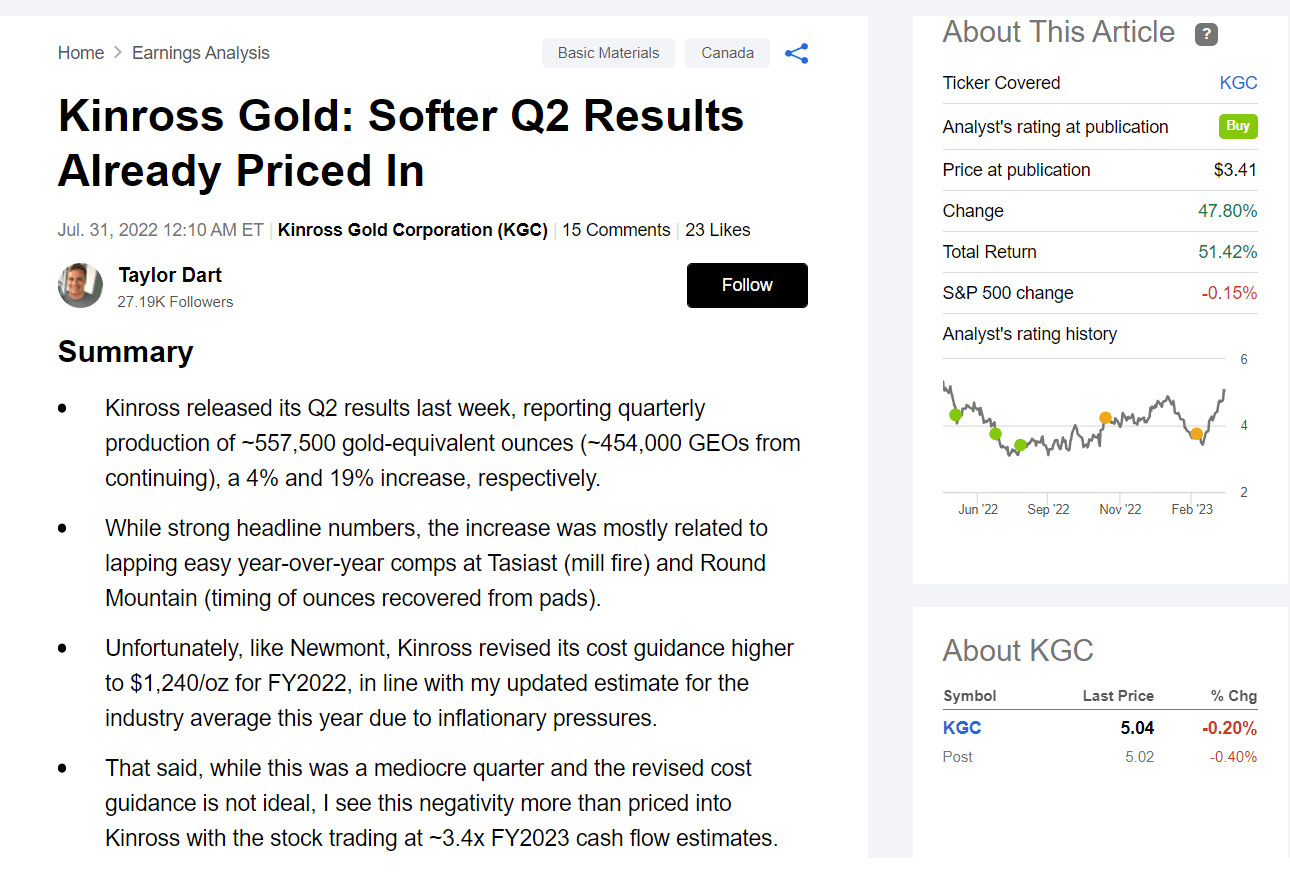

Kinross Article - July 31st, 2022 (Seeking Alpha Premium/PRO)

{kind=link}

Summary

Kinross is certainly a major beneficiary of the recent strength in the gold price and the stock has responded favorably, outperforming its peers in Q1 with a 16% return. That said, I prefer to buy stocks only when they're hated and I want a significant margin of safety, and while Kinross was clearly an attractive opportunity at US$3.40 last July, I don't see anywhere near as attractive of a setup here, even with the higher gold price. Instead, I see more attractive opportunities in developers that have not participated in the recent rally, such as i-80 Gold ( IAUX ) and Marathon Gold ( MGDPF ). Both names trade at well below 0.60x P/NAV, remain out of favor, and I see more than 65% upside in both names to fair value. Hence, I see these two names as more attractive areas to put one's capital to work, and I would view any rallies above US$5.50 in KGC before June as an opportunity to book some profits.

For further details see:

Kinross Gold: Getting Saved By The Gold Price