CA - Kinross Gold: Margin Recovery On Deck

2023-05-10 14:43:06 ET

Summary

- Kinross Gold released its Q1 results this week, reporting quarterly production of ~466,000 gold-equivalent ounces, a meaningful improvement vs. the year-ago period.

- Unfortunately, costs were higher at $1,321/oz, but the higher gold price should offset the company's higher costs if it can continue to hold on to its gains.

- From a development standpoint, Kinross continues to make solid progress on its Tasiast 24k Project, Manh Choh remains on budget and schedule, and costs should decline as the year progresses.

- That said, while the turnaround story here remains intact, I don't see any margin of safety at current levels, and I would view further strength above US$5.90 before July as an opportunity to book some profits.

We're more than halfway through the Q1 Earnings Season for the Gold Miners Index ( GDX ) and one of the most recent companies to report its results is Kinross Gold ( KGC ). Overall, the company put together a solid Q1 report, producing ~466,000 gold-equivalent ounces [GEOs], a 23% increase year-over-year helped by better grades at Fort Knox, Round Mountain, Paracatu, and a new contribution from the successful ramp-up of La Coipa. And while costs came in above the industry average at $1,321/oz, they should improve as the year progresses, benefiting from the pullback we've seen in fuel prices. Let's look at the quarterly results below.

{kind=link}

Q1 Production & Sales

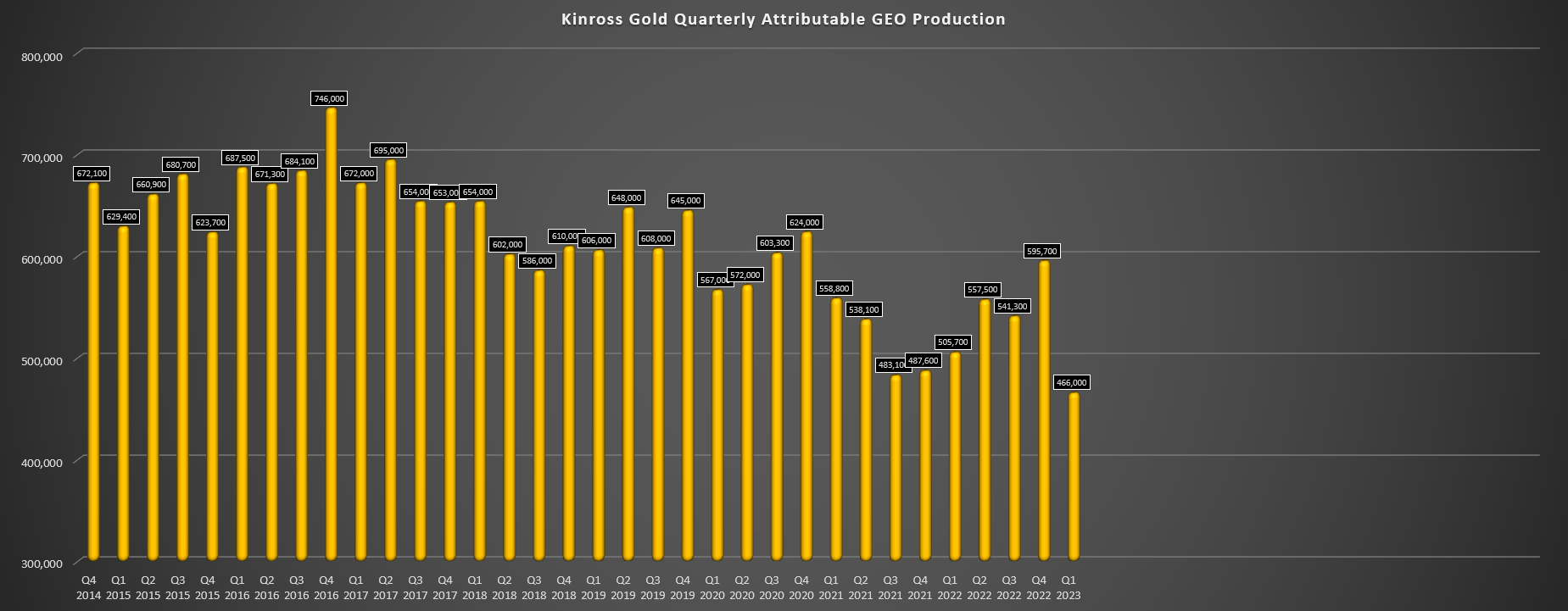

Kinross released its Q1 results this week, reporting quarterly production of ~466,000 gold-equivalent ounces, a meaningful decrease year-over-year on a non-adjusted basis for its sale of Kupol and Chirano, but up 23% year-over-year when adjusting for this ~131,000-ounce headwind from the sale of these two assets in Russia and Ghana. As the chart below shows, this was the lowest quarter for gold production for Kinross in several years, and production is down nearly 35% on a five-year basis vs. the ~672,000 GEOs produced in Q1 2017. Fortunately, there are projects in progress to maintain production at similar levels, but the days of a 2.5+ million-ounce production profile are a distant memory, and the higher margins from Kupol are surely missed.

Kinross - Quarterly Gold-Equivalent Ounce Production (Company Filings, Author's Chart)

{kind=link}

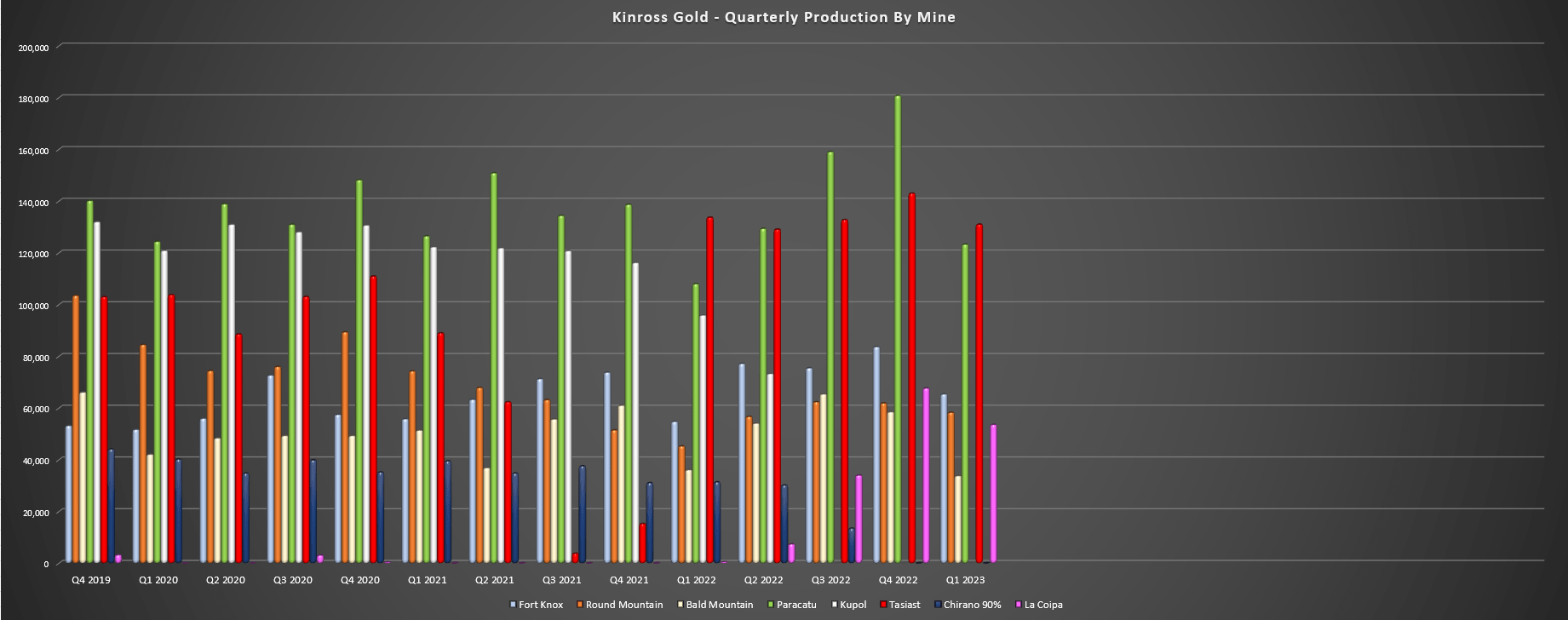

Looking at the operations in a little more detail, Tasiast saw two monthly production records and reported similar production year-over-year despite a shut in February to allow for tie-ins related to its 24,000 tonne per day expansion (24k Expansion) project. Higher grades in the period (~1.21 million tonnes processed at 3.49 grams per tonne of gold) helped to maintain a 130,000-ounce production profile year-over-year, and the 24k Project remains on schedule for mid-2023, with the Tasiast Solar Plant set to come online by year-end. This is a positive development that will help maintain production despite a declining grade profile, and it's also nice to see the project remaining on budget in a period where capex misses have been the norm due to inflationary pressures.

Moving over to Kinross' other assets, Fort Knox and Round Mountain both saw higher production of ~65,400 ounces and ~58,300 ounces, respectively, benefiting from higher grades and throughput on a year-over-year basis. Elsewhere, Paracatu also had a solid quarter, with production of ~123,300 ounces, a nearly 15% increase from Q1 2022 levels. Finally, La Coipa contributed meaningfully in Q1 2023 despite a planned mill shutdown, with ~53,600 ounces produced in Q1 2023 at production cost of sales of $727/oz, well below the company average ($987/oz). In fact, the only meaningful underperformer in the quarter was Bald Mountain, which produced just ~33,800 ounces, its weakest quarter in years related to fewer tonnes stacked on the pads, with difficult weather impacting mining/stacking activities.

Kinross - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

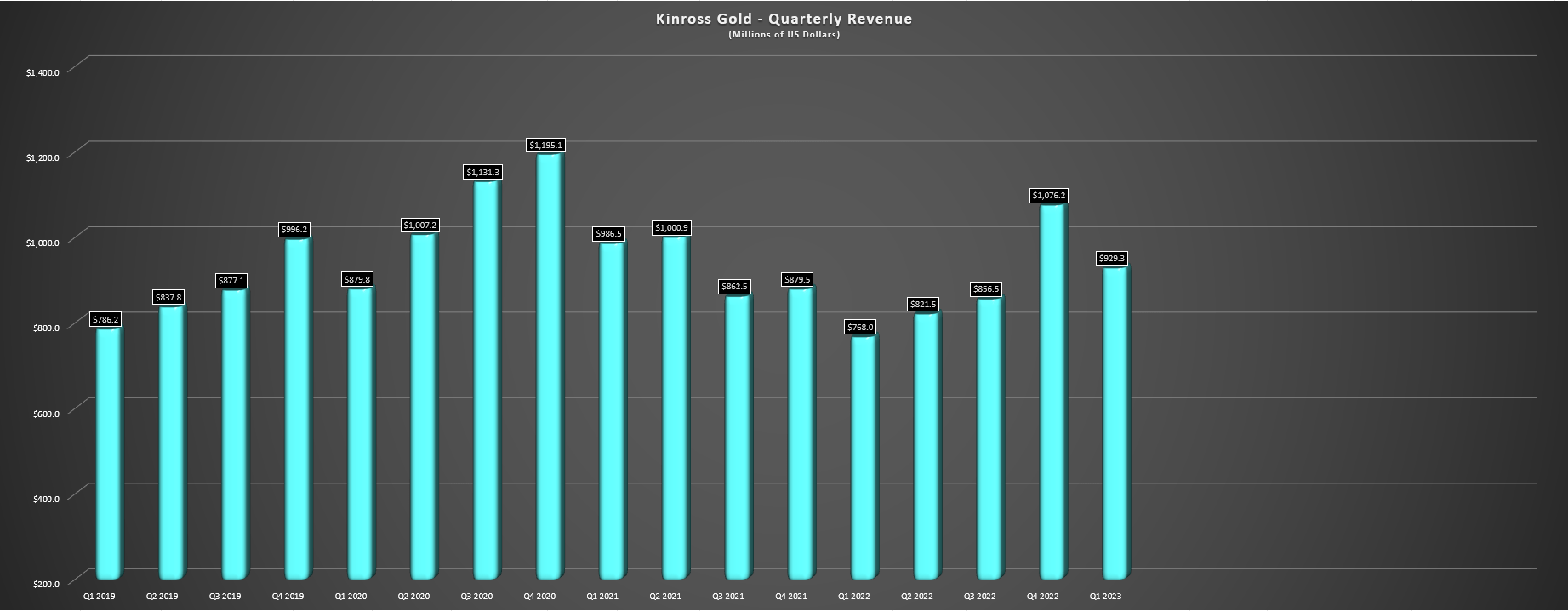

Moving over to sales, Kinross benefited from higher sales than production in the period, with gold sales coming in 5% above production at ~490,300 ounces. When combined with a higher average realized gold price of $1,894/oz (Q1 2022: $1,876/oz), this translated to a meaningful increase in revenue on a year-over-year basis to $929.3 million. Just as encouragingly, operating cash flow improved to $259.0 million (adjusted cash flow: $358.2 million), and while free cash flow was barely in positive territory at $37.8 million, this was an improvement given the higher capital expenditures in the period and impact of inflationary pressures on some consumables.

Kinross - Quarterly Revenue (Company Filings, Author's Chart)

{kind=link}

Costs & Margins

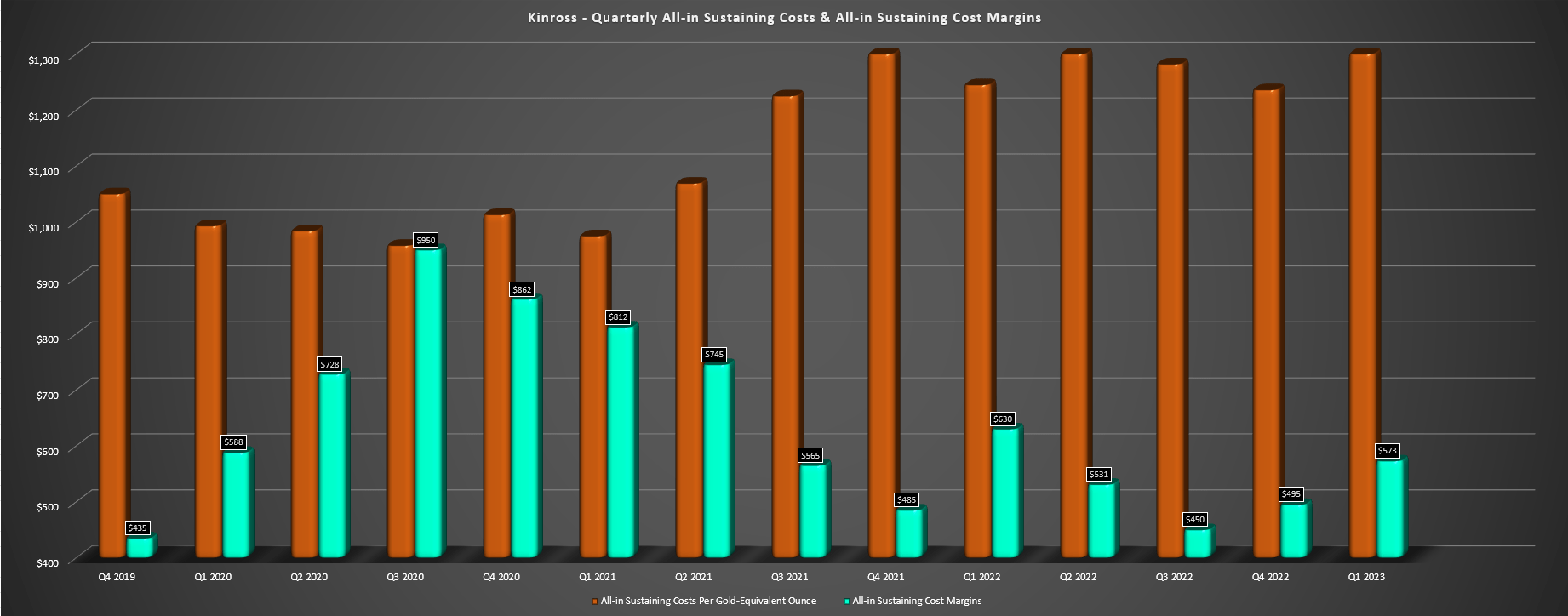

Moving over to costs and margins, Kinross reported all-in sustaining costs of $1,321/oz, a 7% increase from the year-ago period. The company called out higher power and reagents costs at Round Mountain, higher reagent and royalty costs at Bald Mountain, and the company also saw an impact from significantly higher sustaining capital expenditures in the period ($96.6 million). The good news is that costs came in right in line with its full-year guidance in what should be the weakest quarter of the year due to lower production/sales, and its larger operations pulled their weight, helping to offset much higher costs at Round Mountain on a year-over-year basis ($1,657/oz vs. $1,114/oz).

Kinross - Quarterly AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

As for Kinross' margins, we saw AISC margins improve/decline 9% year-over-year to $630/oz, but we should see lower costs as the year progresses combined with a stronger average realized gold price if the metal can hold on to its gains. So, when combined with easy year-over-year comps, we should see a meaningful recovery in margins for Kinross this year, and cash flow should also improve, which the company expects to deploy towards share repurchases. Unfortunately, there were no share repurchases in Q1 and while repurchases should continue in H2-2023, the opportunity has been missed to repurchase another batch of shares at sub US$4.00, which is the ideal time to be retiring shares at an attractive valuation.

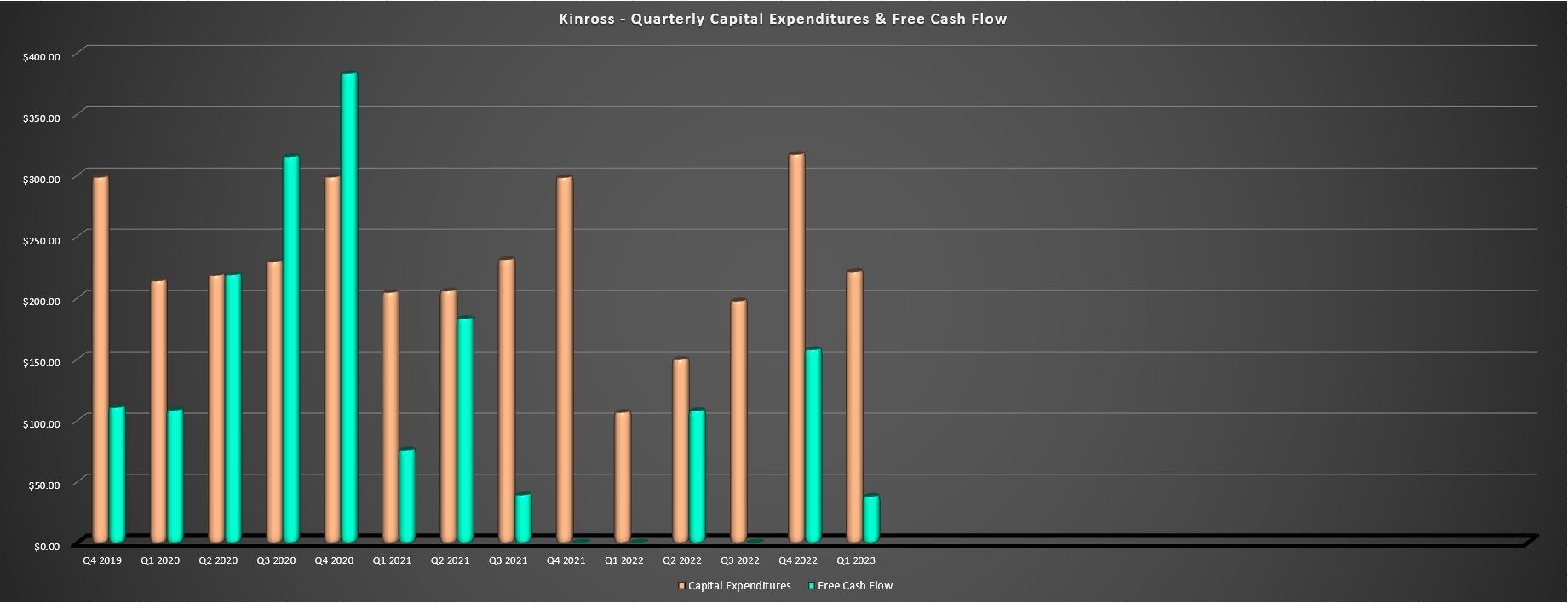

Kinross - Quarterly Capex & Free Cash Flow (Company Filings, Author's Chart)

{kind=link}

Finally, if we look at free cash flow and capex above, Kinross saw elevated capital expenditures in Q1, impacting free cash flow generation in the period. However, assuming the gold price can hold up, Kinross should generate well over $250 million in free cash flow this year. And while this isn't a significant amount for a company with an enterprise value of ~$8.80 billion, it's a step in the right direction for the company, which is helping to grow production per share through buybacks and reduce its leverage ratios, with Kinross having one of the weaker balance sheets among its senior producer peers. Let's take a look at Kinross' valuation below.

Valuation & Technical Picture

Based on ~1,230 million fully diluted shares and a share price of US$5.35, Kinross trades at a market cap of $6.60 billion and an enterprise value of ~$8.80 billion. This has left the company trading in line with its historical multiple of ~5.2x cash flow (10-year average), with Kinross currently sitting at ~5.1x cash flow based on FY2023 cash flow per share estimates of $1.05. Using what I believe to be a more fair multiple of 6.50x cash flow to account for its improved jurisdictional profile, I see a fair value for the stock of US$6.60. However, this is contingent on the price of gold holding onto its recent gains, with Kinross more leveraged than most of its peers.

{kind=link}

Although this points to a 22% upside from current levels, I am looking for a minimum 40% discount to fair value for high-cost mid-cap producers, and Kinross' costs are expected to remain above its peer group this year, with all-in sustaining costs expected to come in at $1,320/oz (+/- 5%). After applying this discount to ensure an adequate margin of safety, Kinross' ideal buy zone doesn't come in until US$4.00 or lower, well below current levels. Obviously, there's no guarantee that the stock sinks to these levels, but I prefer to pay the right price or pass entirely, and while the stock was a steal below US$4.00 last year, I don't see an attractive setup here, especially with the stock rallying towards potential resistance near US$5.80.

{kind=link}

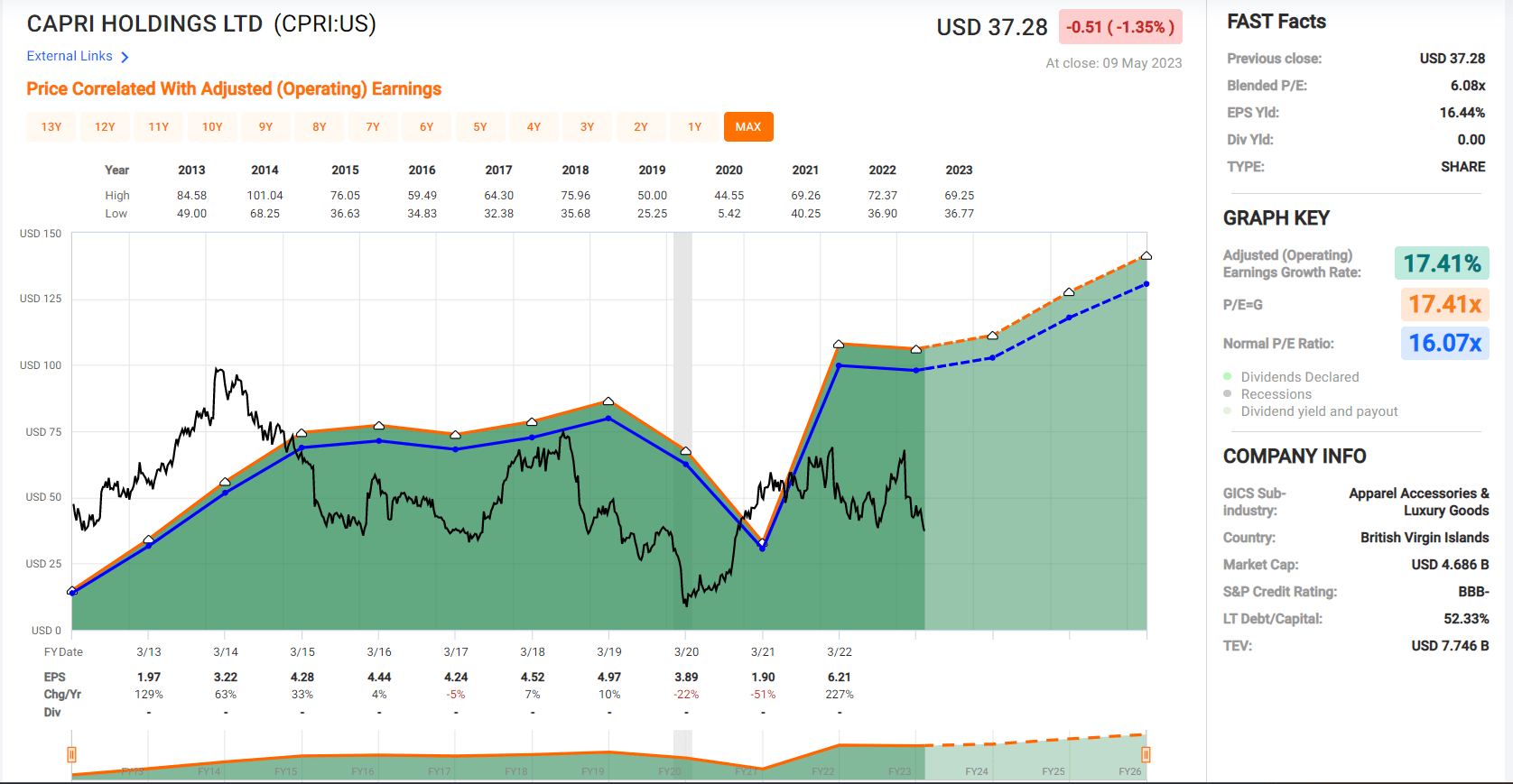

In fact, while Kinross has rallied sharply, other names have become far more attractive from a relative value standpoint, such as some miners that are still trading at deep discounts to fair value, and some retail names that have been thrown out with the bathwater. One name in the latter group that boasts a much larger margin of safety is Capri Holdings ( CPRI ), a luxury-goods distributor and retailer (Versace, Jimmy Choo, Michael Kors) trading at ~5.8x FY2024 earnings estimates vs. a historical multiple of 16.0x earnings. So, if I were looking to put new capital to work, I continue to see more attractive opportunities elsewhere, both in miners and other industry groups.

Capri Holdings - Historical Earnings Multiple (FASTGraphs.com)

{kind=link}

Summary

Kinross Gold put together a solid performance in Q1 and it's positive to see its development projects tracking on schedule, with Tasiast 24k and its Solar Plant set to be operational by mid-year and year-end, and Manh Choh also on budget with construction underway and work beginning on long-lead procurement. That said, the best time to buy turnaround stories is when they're trading at massive discounts to their peer group with a meaningful margin of safety in place. And while this was the case last summer when I highlighted Kinross as attractive below US$3.50, I don't see this being the case with Kinross now ~60% off its lows and trading at a premium on a P/NAV standpoint vs. some of its better-run peers.

{kind=link}

Given the current setup, I believe that deploying capital elsewhere makes far more sense, and I don't see any reason to pay up for Kinross above US$5.50. In fact, if this rally in the stock were to continue, I would view any rallies above US$5.80 before July as an opportunity to book some profits. Some investors might argue that a rising tide will lift all boats and that Kinross is more leveraged, given its higher costs, making it one of the better bets currently. While I agree, leverage works in both ways. Plus, investing without a margin of safety in a cyclical stock rarely works out as intended. Hence, I favor names like Capri or Sandstorm Gold Royalties ( SAND ) Royalties, with the latter trading at a lower P/NAV multiple vs. KGC despite being a royalty/streaming company.

For further details see:

Kinross Gold: Margin Recovery On Deck