CA - Kinross Gold Q3: Tracking Well Against 2023 Guidance

2023-11-10 09:30:53 ET

Summary

- Kinross Gold Corporation put together another quarter of solid results in Q3 and is tracking well against its FY2023 guidance of ~2.1 million gold-equivalent ounces.

- Meanwhile, the company has approved Phase S at Round Mountain to extend open-pit operations, and is exploring the potential for an underground opportunity at Tasiast longer-term.

- In this update, we'll dig into the recent Kinross Q3 results, recent developments, and whether the stock is worthy buying after its Q3 beat.

We're more than halfway through the Q3 Earnings Season for the VanEck Gold Miners ETF ( GDX ) and the results have been mixed overall. There have been weaker quarters from Pan American Silver Corp. ( PAAS ), IAMGOLD Corporation ( IAG ), Coeur Mining, Inc. ( CDE ) and Wesdome Gold Mines Ltd. ( WDOFF ), offset by a blowout report from Alamos Gold Inc. ( AGI ) with a meaningful beat on guidance.

Fortunately, Kinross Gold Corporation ( KGC ) was one of the few producers that outperformed expectations, helped by a monster quarter from its two largest assets which combined for over 340,000 ounces, and another solid quarter from its new La Coipa Mine with ~66,000 ounces produced at industry-leading production cost of sales of $629/oz, especially among non Tier-1 assets. In this update, we'll dig into the recent Q3 results , recent developments, and whether the stock is a buy after its Q3 beat.

Fort Knox Mining Fleet - Company Presentation

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q3 Production & Sales

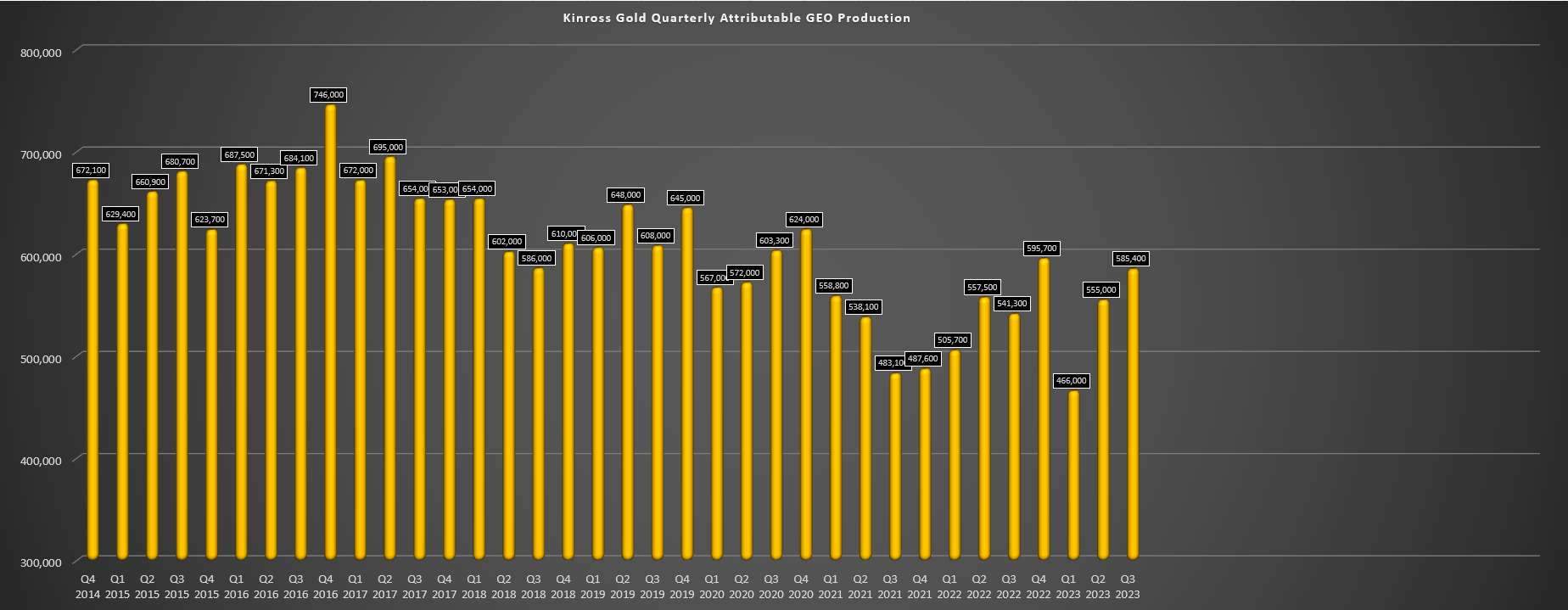

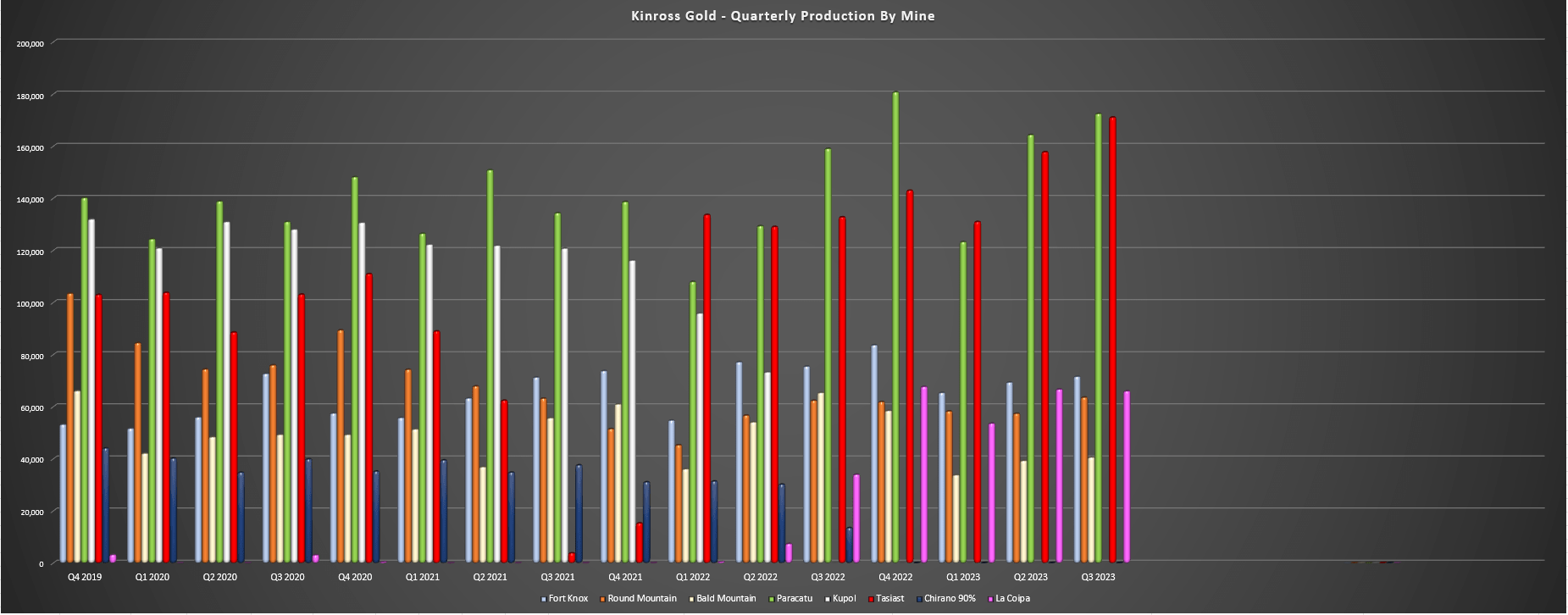

Kinross Gold released its Q3 results this week, reporting quarterly production of ~585,400 gold-equivalent ounces [GEOs], an 11% increase from the year-ago period. The solid performance was driven by exceptional quarters from Tasiast, Paracatu, and La Coipa, with a record quarter at Tasiast (~171,100 ounces), another huge quarter at Paracatu (~172,500 ounces), and a much better quarter at La Coipa year-over-year vs. its ramp-up phase last year and coming off a tough Q2 2022 with commissioning challenges. Meanwhile, although Fort Knox and Bald Mountain saw lower output year-over-year (fewer tonnes placed at the heap leach facility at Fort Knox, lower output because of the timing of recoveries at Bald Mountain), Round Mountain also saw production growth and has a much brighter future with work to deliver a higher-return Phase S successful.

Kinross Gold - Quarterly Attributable GEO Production - Company Filings, Author's Chart Kinross Quarterly Production by Mine - Company Filings, Author's Chart

{kind=link}

{kind=link}

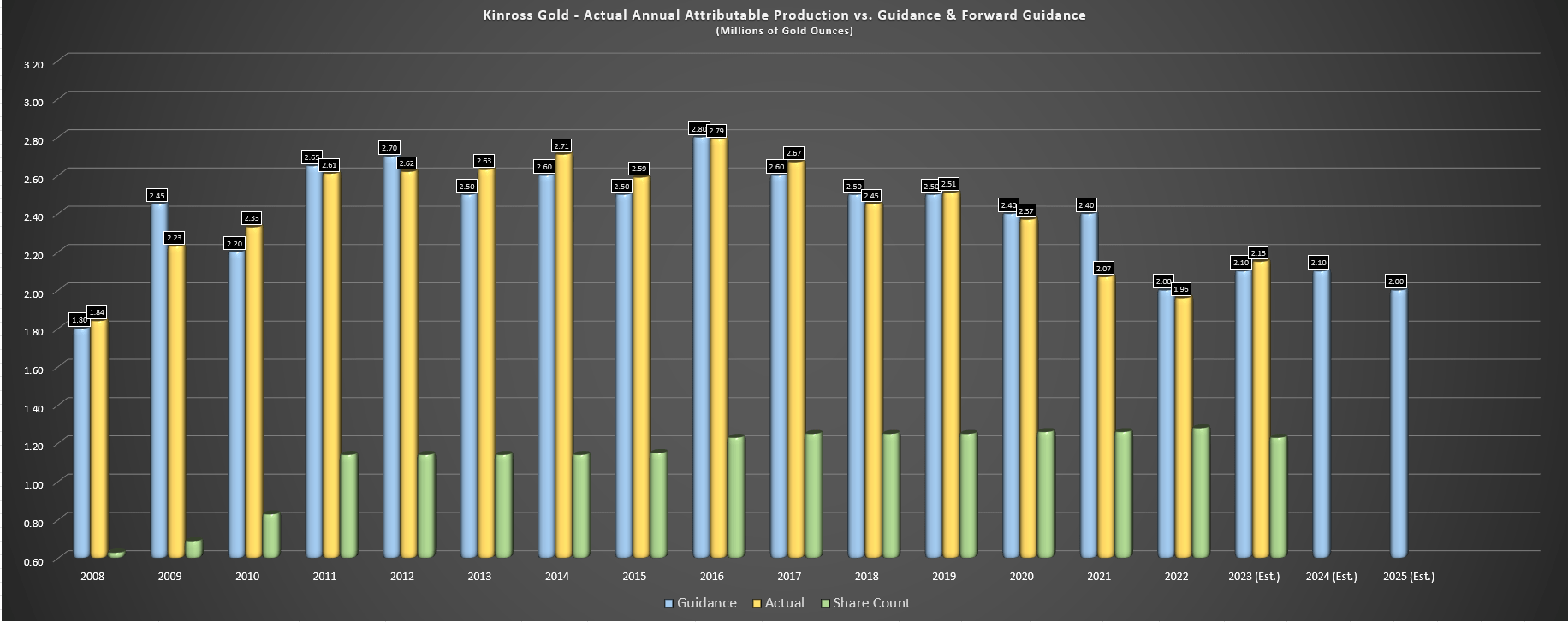

As highlighted in the above charts, this recovery in production is certainly a step in the right direction after a tough 2022 (Tasiast mill fire, delayed ramp-up at La Coipa, sale of Russian/Ghanian assets), and Kinross has produced ~1.61 million ounces year-to-date, leaving it well on track to deliver against its ~2.1 million ounce guidance (+/- 5%) even when factoring in a softer Q4 at Paracatu. Just as importantly, it will please investors to know that major expansion projects are complete (Tasiast 24k, La Coipa), mill throughput at Tasiast will ramp up further in Q4 (~19,600 tonnes per day in Q3-23) and achieve nameplate capacity next year, and progress at other projects is going well, with Manh Choh in Alaska on budget and schedule with pre-stripping underway, with production from this high-grade satellite project set to begin in H2-2024. And for a company with a track record of under-delivering on guidance in most years, the better performance in 2023 (~2.15 million GEO potential vs. ~2.1 million guide) is a welcome change in trend as well.

Kinross - Actual Annual Production vs. Guidance, FY23 Estimates & Forward Guidance - Company Filings, Author's Chart

{kind=link}

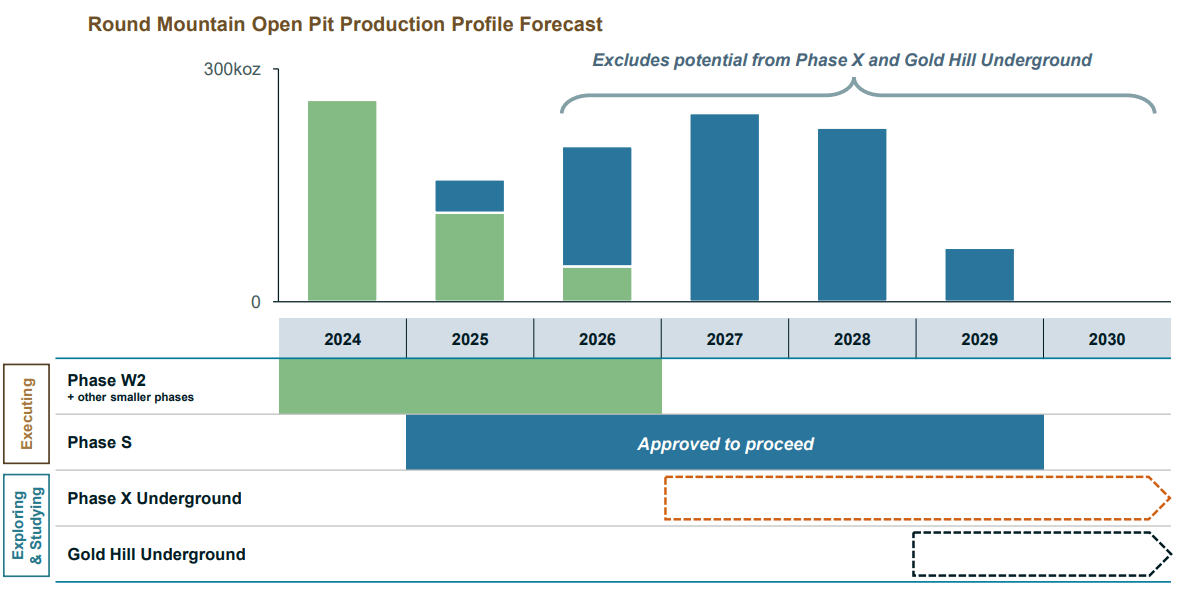

Finally, as for recent developments, Kinross has approved Phase S at Round Mountain in Nevada, a project that will allow Round Mountain to see an incremental ~750,000 ounces of production and average ~215,000 ounces per annum from 2024 to 2028 vs. a previous outlook that would see open-pit operations wind down in 2026. Importantly, the IRR with the new design for Phase S is quite attractive at ~45% ($1,850/oz gold) and a 58% IRR at $1,950/oz gold. Upfront capex for the project is quite modest at ~$170 million (with the bulk of this being stripping and the rest being the expansion of the North Heap Leach Pad and tailings infrastructure), and assuming no upside in gold prices, Phase 3 has a ~$230 million NPV. However, equally important is that Phase 3 will allow for a bridge between Phase W2 (currently being mined) and a potential underground scenario that's being studied at Phase X and Gold Hill.

Phase S Approval & Round Mountain Production Profile - Company Website

{kind=link}

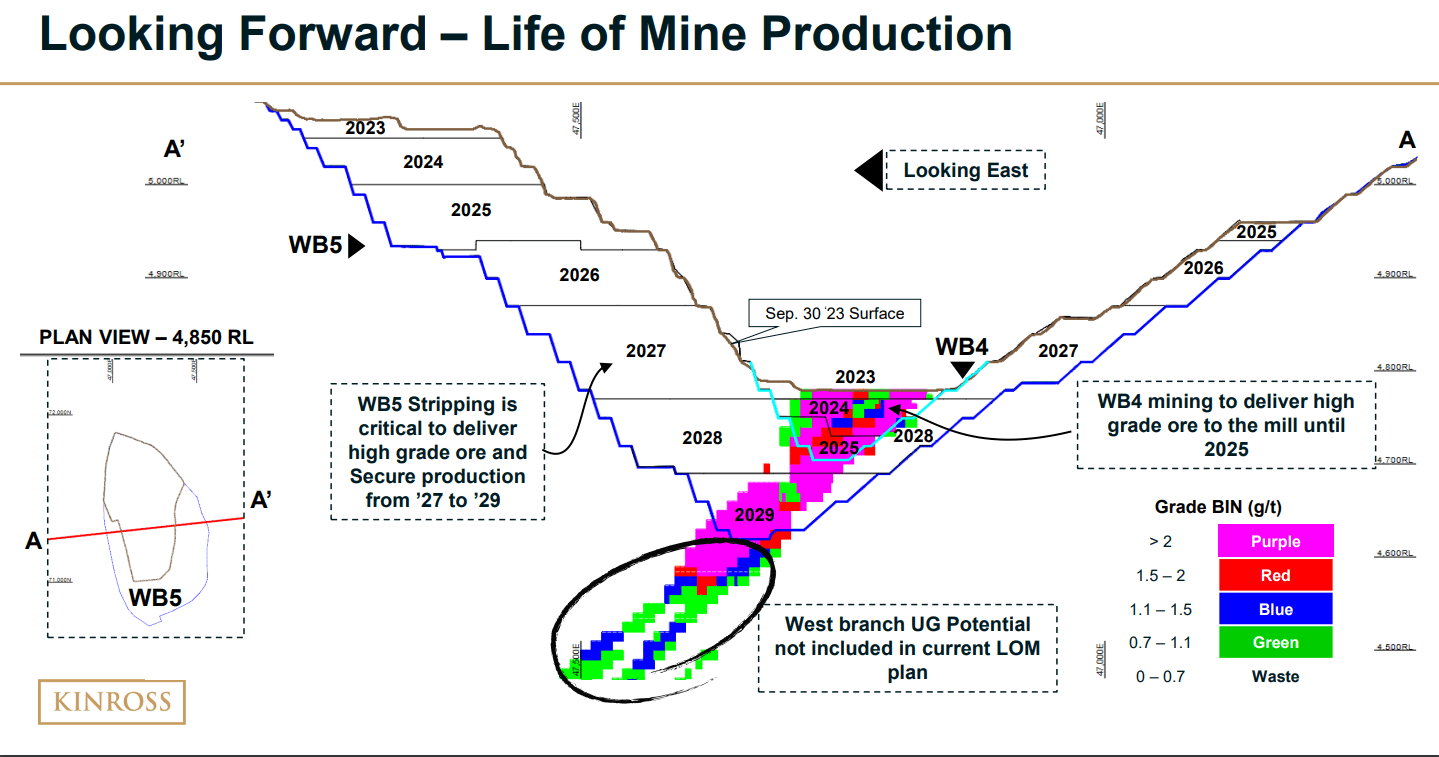

Meanwhile, at the company's flagship Tasiast Mine in Mauritania, Kinross noted that its 34MW solar plant will start delivering power by year-end ($15/oz cost benefit to AISC once fully ramped up), and significant reduction in fuel consumption, and the company is looking at the potential for an underground opportunity at the mine. As the life of mine shows below, production will drop off materially from 2025 through 2027 despite the higher throughput as grades come off, and the mine life is expected to end in 2035 if an underground scenario isn't approved (currently looking at ~1.0 million ounce potential at 2.5 grams per tonne of gold in early studies on the underground) or in other near-mine opportunities.

Hence, while 2023 production of 600,000+ ounces with similar output in 2024 at Tasiast is impressive, current growth opportunities (Manh Choh, Phase S at Round Mountain) will mostly just offset the drop-off at Tasiast in these three lower-grade years vs. allowing Kinross to see production maintain 2.5+ million ounces for the rest of the decade under the previous outlook .

{kind=link}

Overall, the potential for an underground opportunity at Tasiast which is also being explored at Fekola is certainly a positive, but it's still early days on any approvals.

Costs & Margins

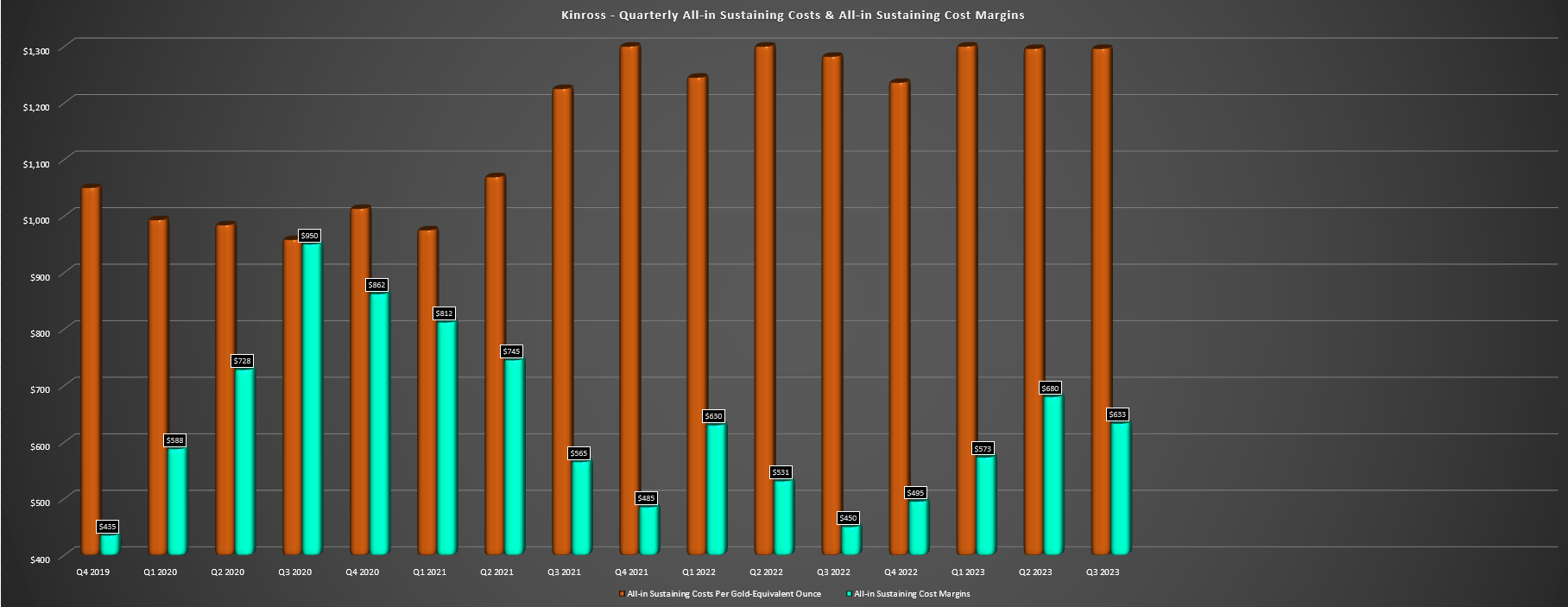

Moving over to costs and margins, Kinross reported all-in sustaining costs [AISC] of $1,296/oz in Q3, slightly below the estimated industry average (~$1,360/oz) and only up marginally vs. the year-ago period. However, Kinross' margins soared despite the higher costs given the help it got from the gold price ($1,929/oz vs. $1,732/oz), with AISC margins improving to $633/oz vs. $450/oz in Q3 2022. These results are impressive and were helped by low-cost production at La Coipa, as well as improved costs at Tasiast with a year-to-date production cost of sales of $668/oz ($763/oz in the same period last year). Additionally, Paracatu also saw lower costs on the back of much higher production (~460,100 ounces at $859/oz year-to-date vs. ~396,500 ounces at $974/oz in the same period of 2022). Given the ~$1,300/oz AISC year-to-date, Kinross should be able to deliver just below its guidance of ~$1,320/oz.

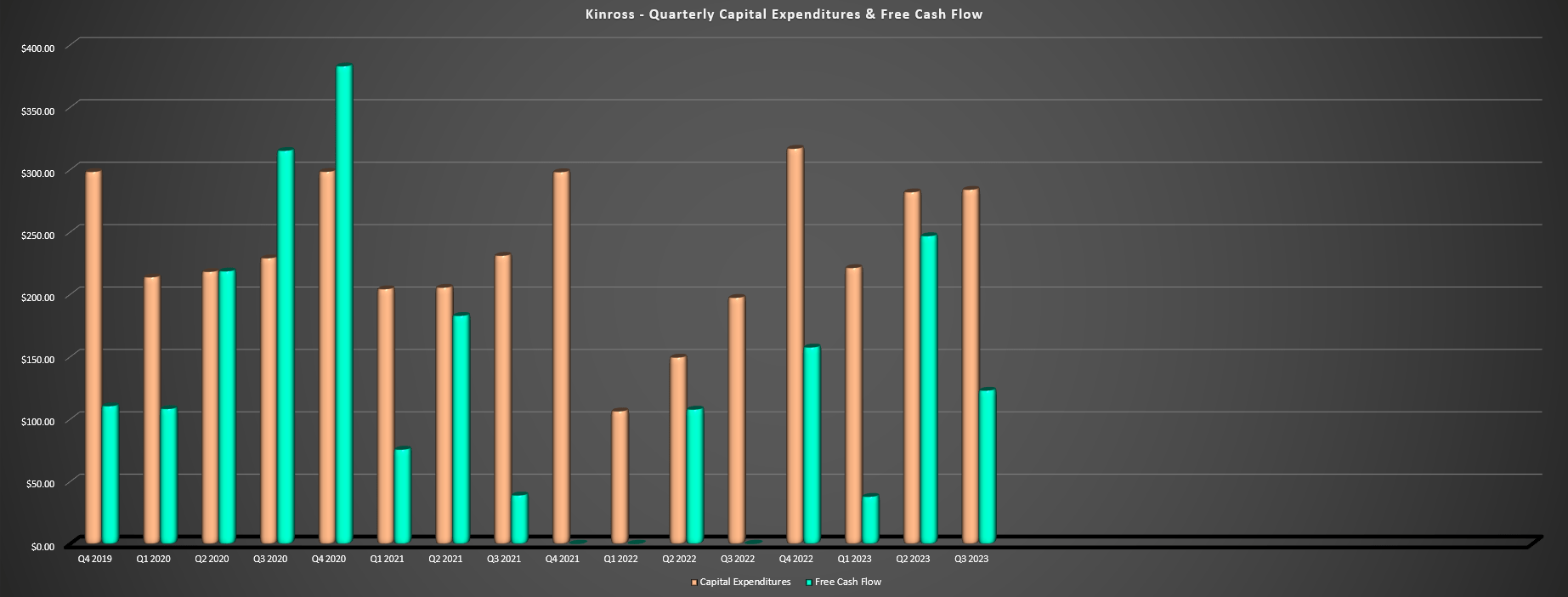

Kinross Quarterly AISC & AISC Margins - Company Filings, Author's Chart Kinross Quarterly Capex & Free Cash Flow - Company Filings, Author's Chart

{kind=link}

{kind=link}

Finally, looking at revenue, cash flow, and free cash flow, Kinross had an impressive quarter with revenue increasing over 27% to ~$1.1 billion, operating cash flow improving to ~$407 million, and free cash flow coming in at ~$123 million despite higher capital expenditures in the period. This has pushed trailing-twelve-month free cash flow to over $550 million and the strong free cash flow has helped Kinross to improve its balance sheet to just ~$1.9 billion in net debt despite significant share repurchases last year (~$79 million), leaving Kinross net debt to EBITDA ratio near ~1.1x, a significant improvement from last year.

Let's take a look at KGC's valuation below and see whether the solid results and improved balance sheet are priced into the stock after its outperformance vs. peers.

Valuation

Based on ~1.23 billion shares and a share price of US$5.50, Kinross trades at a market cap of ~$6.77 billion and an enterprise value of ~$8.67 billion. This leaves Kinross back to trading closer to its peers like AngloGold Ashanti plc ( AU ) and Endeavour Mining plc ( EDVMF ) after its recent outperformance. Meanwhile, from a valuation standpoint, Kinross remains reasonably valued despite doubling off its lows, lending to it briefly trading at one of the lowest multiples last summer before the stock finally bottomed out.

This is evidenced by Kinross trading at just over 5x FY2024 cash flow estimates on an enterprise value basis, and slightly below 1.0x P/NAV. That said, this outperformance has significantly reduced its relative value compared to peers, with it now trading at a similar cash flow multiple to Barrick and actually a higher P/NAV multiple despite Barrick Gold Corporation ( GOLD ) being more diversified, having a larger scale and a higher growth rate looking out to 2030 vs. a more flat profile for Kinross (Great Bear will offset lower production at Tasiast and Round Mountain unless underground expansions are approved at these assets).

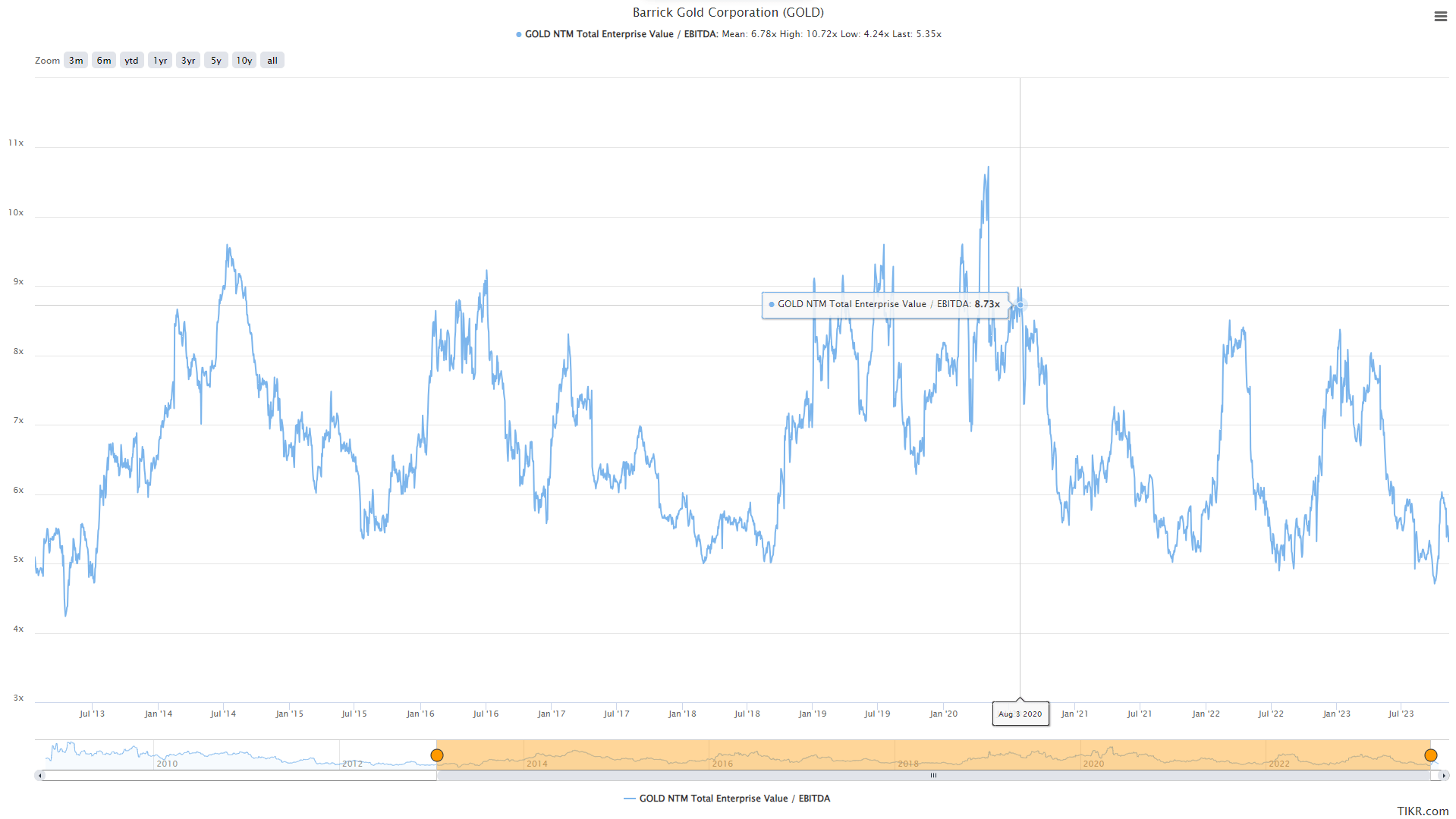

As the charts below show, Kinross went from trading at the low end of its 10-year range for EV/EBITDA to above the mid-point while Barrick has now found itself at the low end of the range, and an area where it has typically found support.

Barrick Gold EV/EBITDA Multiple & 10-Year Average - TIKR.com

{kind=link}

{kind=link}

Using what I believe to be a fair multiple of 1.0x P/NAV and ~7.0x cash flow to factor in Kinross' improved pipeline and jurisdictional profile and a 65/35 weighting (P/NAV vs. P/CF and using FY2024 estimates), I see a fair value for Kinross Gold of US$6.40. Based on an estimated fair value of US$6.40, I see a 16% upside from current levels for KGC, which may be attractive to some investors. However, this isn't nearly enough upside to get me interested in a cyclical business that lacks growth and this is especially true when there are some large-cap producers with over 60% upside to fair value and some small-cap producers with over 100% upside to fair value.

Hence, while KGC was an attractive bet below US$4.00, I don't see nearly enough of a margin of safety at current levels. Therefore, if this rally in the stock were to persist, I would view any rallies above US$6.15 before February as an opportunity to book some profits.

Summary

Kinross Gold put together another solid report in Q3, and its two largest mines have combined for an impressive ~920,000 ounces year-to-date while La Coipa continues to drag down company-wide all-in sustaining costs. Meanwhile, the company has done a solid job completing its growth projects vs. minor setbacks for peers at projects like Obuasi and Pueblo Viejo, and it is one of the few producers that will deliver above its guidance mid-point (~2.1 million ounces).

That said, the time to buy KGC was when it was hated and down over 60% from its 2020 highs last summer, and I think it's much more difficult to argue for chasing the stock at US$5.50 when it's one of the favored producers sector-wide with sentiment actually being quite rosy. To summarize, I continue to see far more attractive bets elsewhere in the sector and I would view any rallies above US$6.15 before February as an opportunity to book some profits.

For further details see:

Kinross Gold Q3: Tracking Well Against 2023 Guidance