SPY - KRE: Bank Stocks Are Signaling Tough Times Ahead

2023-04-18 13:36:10 ET

Summary

- The 30% crash in KRE signals a recession and credit crunch based on historical evidence.

- The banking panic has receded, but it's nowhere near finished yet.

- The small and regional banks still have more downside despite the recent drop.

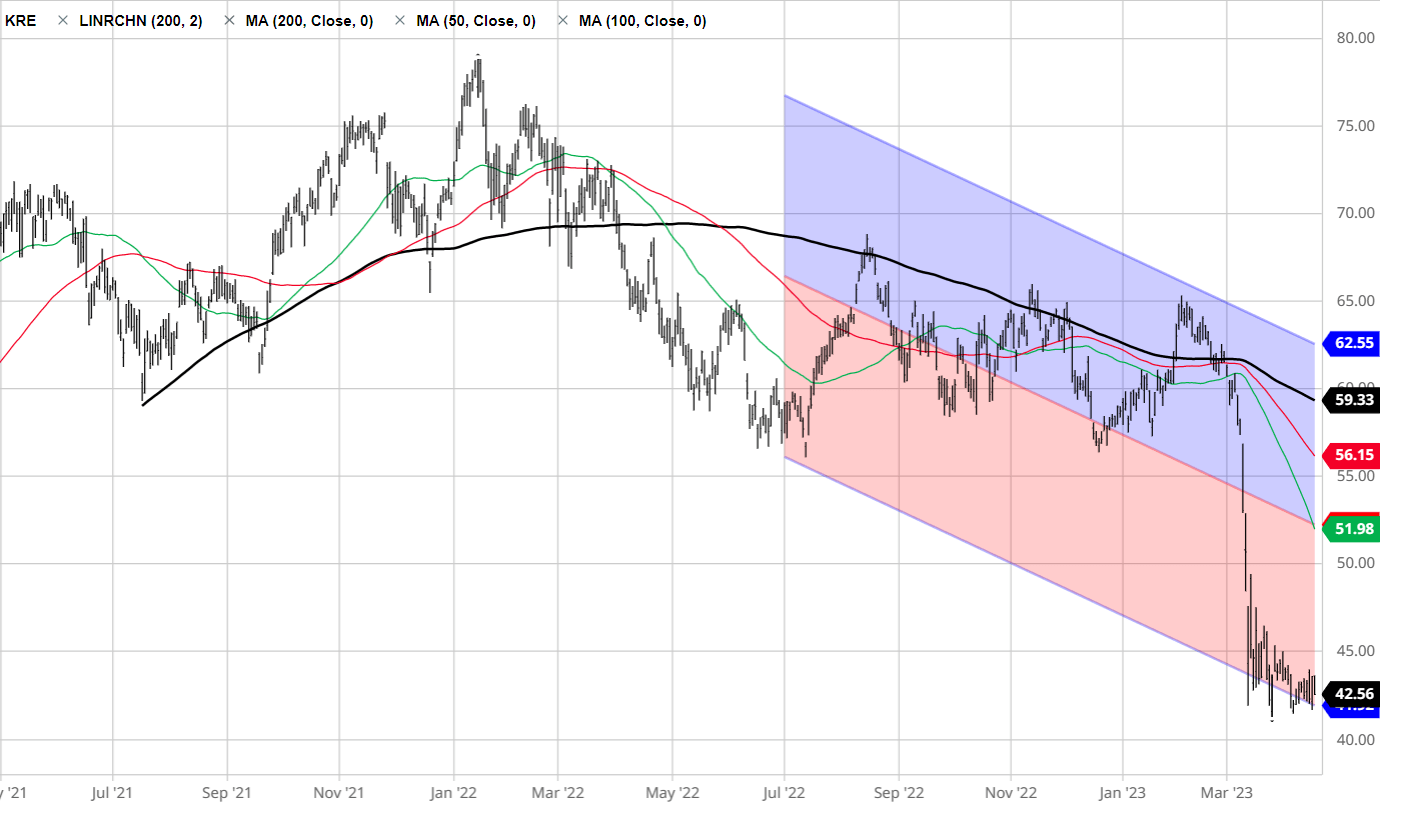

Regional banks down by 30% since the March crisis

It's been more than a month since the onset of the March 2023 banking crisis. Since then, the SPDR S&P Regional Banking ETF ( KRE ) is down by 30%. Is this an opportunity to buy KRE or is there more pain ahead? More importantly, what are the implications for broader stock market ( SPY ) after the significant drop in regional banks over the last month? Here's the KRE chart:

{kind=link}

Barchart

Based on historical evidence, this predicts a recession

The recent study published in the Quarterly Journal of Economics specifically looks at the historical episodes when the bank stocks fall by 30% or more. The authors of the study construct a dataset of bank equity index returns for 46 countries from 1870 to 2019. Overall, the study includes 100 banking crises.

The study finds that "bank equity declines predict large and persistent declines in future real GDP and bank credit to the private sector." Specifically, they find that "a decline in bank equity of at least 30% predicts 3.4% lower real GDP and 5.7 percentage points lower bank credit-to-GDP after three years."

Furthermore, the study finds that large bank equity declines also led to widespread bank failures, and high rates of nonperforming loans. Thus, as the key conclusion, the large bank equity declines are associated with "adverse macroeconomic consequences."

Bank panics are defined as the sudden withdrawal of bank deposits, similarly to what we witnessed in March of 2023. The study finds that the "bank equity crashes with panics tend to be followed by greater credit contractions and lower output growth."

However, the study also finds that the "bank equity crashes without panics also predict substantial credit contractions and persistent output gaps," Specifically, "even in the absence of any creditor panic, a decline in bank equity of at least 30% predicts that after three years, bank credit-to-GDP declines by 3.5% and real GDP declines by 2.7%."

This also predicts a credit crunch

The study also finds that large bank equity declines tend to precede the spike in credit spreads and further banking panics. Specifically, based on the study, "the banking panics occur seven months after the bank equity index has already declined by 30%."

Why is the bank equity decline systematically important?

The banking crisis is usually defined as "an episode in which the banking sector’s ability to intermediate funds is severely impaired". The bank equity is considered as the most important variable that determines banks’ capacity to lend to consumers and business. Thus, the large declines in bank equity limits the banks’ capacity to finance the economy, and thus causes a recession and a possible credit crunch.

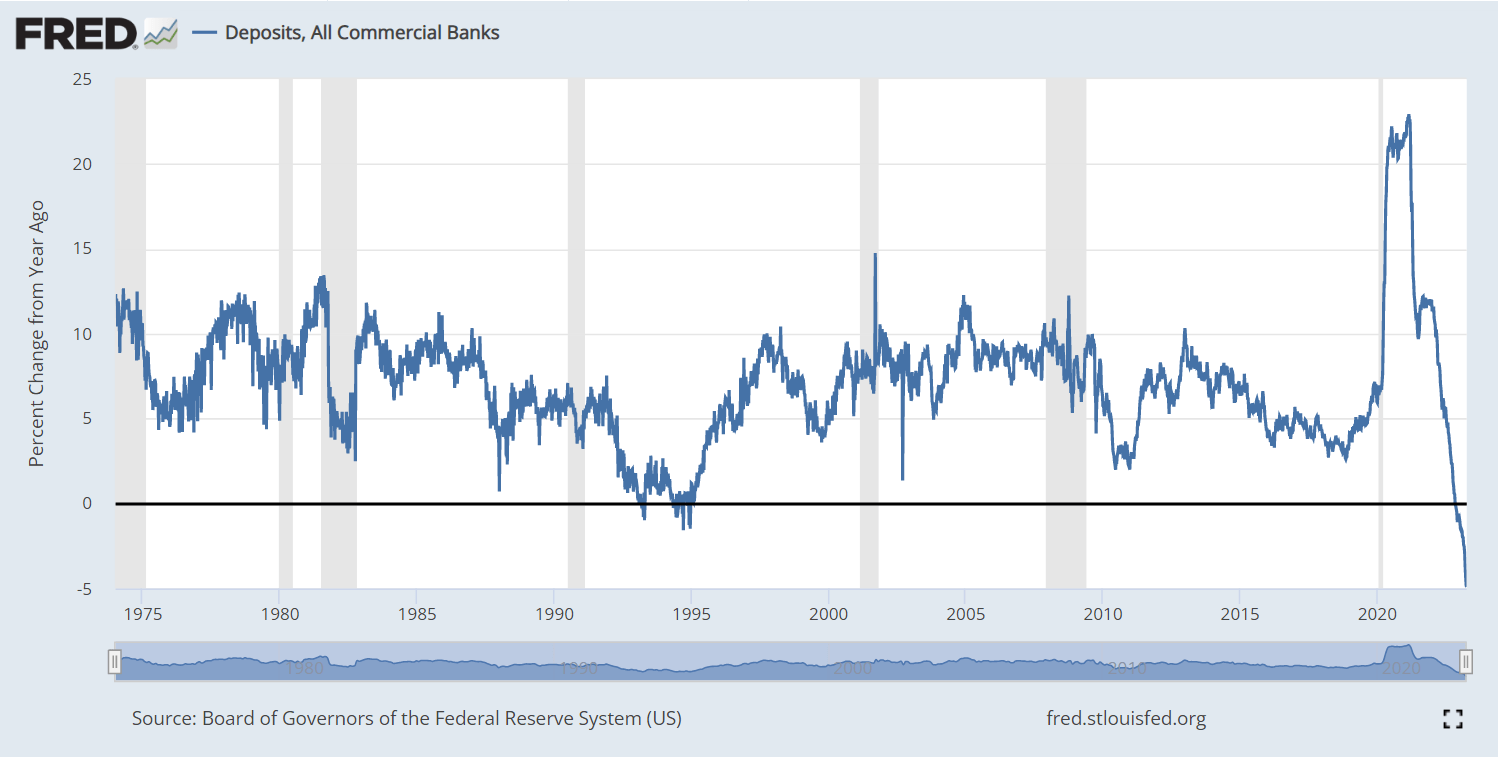

The current banking panic

Here's the chart of the percentage change in bank deposits year over year. The current deposits are 5% below the deposits a year ago. Historically, this is a very rare occurrence. The data here goes only from 1974, and this is the first time that banks are losing deposits, with some near 0% activity in mid 1990s. This is the banking panic, by definition, and based on the historical evidence presented above, it will lead to a recession and possible spike in credit spreads.

{kind=link}

FRED

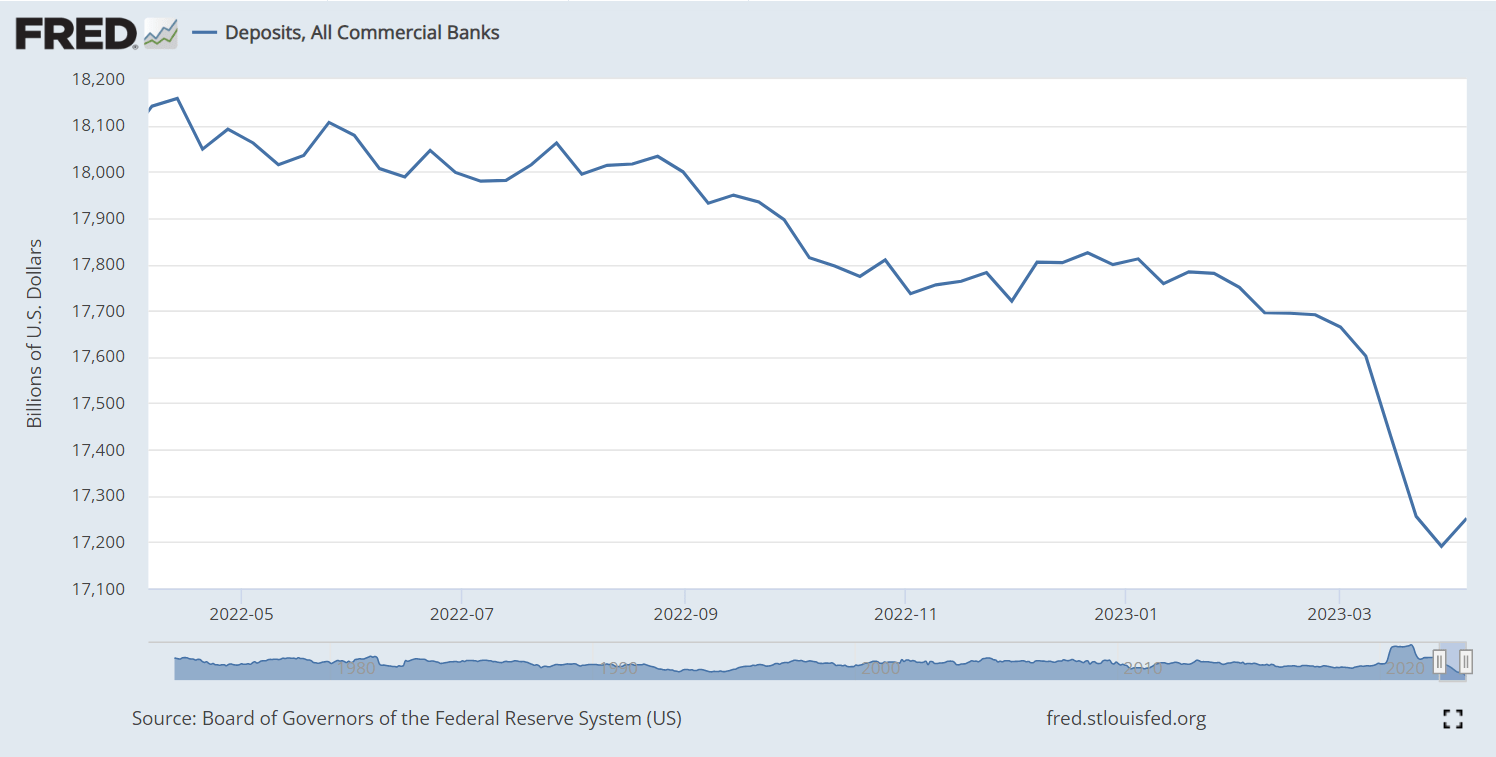

However, it appears that the banking panic has receded somewhat over the last week, with the modest increase in deposits.

{kind=link}

FRED

The current banking panic, as I initially explained , is the function of two variables: 1) the deposit rates in major banks are still near 0%, while the money market rates are near 5%, thus the savers have been withdrawing bank deposits and investing in money market funds, and 2) the banks are sitting on major unrealized losses, as they invested in Treasury Bonds which declined in price in 2022 as long term rates increased.

The current banking crisis is nowhere closed to finished - as long as there's a significant differential between the deposit rate and the money market rate (this will encourage more deposit outflows), and as long as the long-term interest rates stay elevated (this keeps the unrealized losses).

The Fed could end the crisis by lowering the interest rate, but the Fed is nowhere near lowering short-term interest rates back to the 0% level due to still sticky inflation, and long term are likely to stay elevated as long as the Fed is shrinking the balance sheet via QT.

Thus, it's very likely that the deposit withdrawal will continue, especially as the Fed continues to increase interest rates, which widens the deposit rate - money market differential.

The banks' performance in 2022

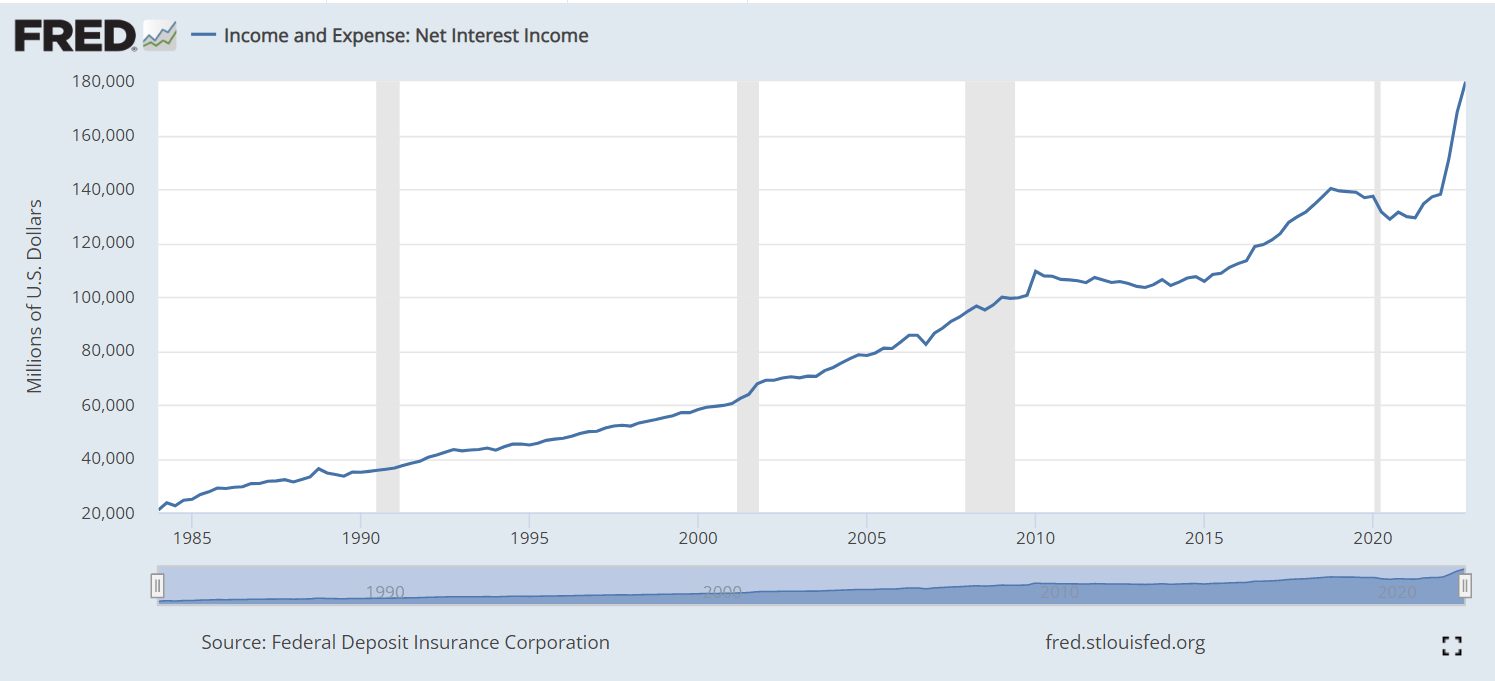

The banks have been reporting earnings for 2022, including the Q1 2023, and generally the performance of large banks, such as JPMorgan ( JPM ) and Bank of America ( BAC ) has been better than expected.

As I already explained, these large banks are able to (for some reason) keep the deposit rate near 0%, and still gain the new deposits. It must be the "too big to fail" benefit. Thus, these large banks had a record net interest rate income NII, taking advantage of "free deposits" and rising loan rates. Here is the chart of NII, with the spike in 2022:

{kind=link}

FRED

However, the smaller and regional banks are being forced to increase the deposit rates to stop the deposit withdrawals, which negatively affects their net interest income.

Furthermore, the Fed's lending facility, established to protect the depositors and ease the banking panic, lends the funds to the banks in need at the market rate, which directly increases the cost of funds. Thus, the profitability of small and regional banks will considerably decrease.

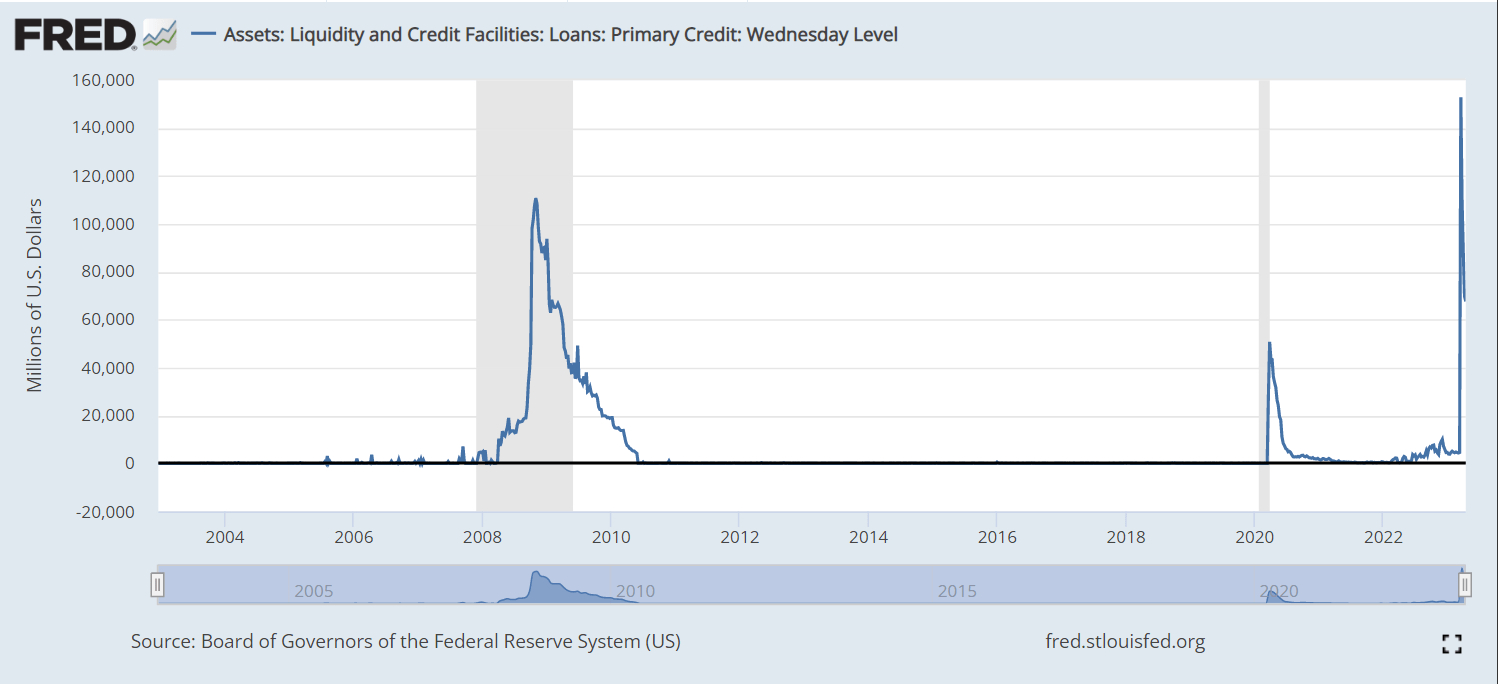

The chart below shows the magnitude of the 2023 banking crisis in relation to the 2008 Great Financial Crisis - the primary loans by the Fed.

{kind=link}

FRED

Implications

The 30% decline in bank stocks ( KRE ) is likely the trigger for the widely expected recession. It signals a much tighter credit, and it will likely lead to the spike in credit spreads and the credit crunch, based on the historical evidence.

The small are regional banks are particularly exposed to the upcoming financial crisis given that 1) their cost of funds has significantly increased, and 2) they have heavy exposure to real estate and commercial real estate loans, which many expect to be the next shoe to drop. Further, these small and regional banks don't have the trading divisions to take the advantage of the market volatility, unlike large banks.

Thus, despite the large drop in KRE, I still expect more downside in price.

For further details see:

KRE: Bank Stocks Are Signaling Tough Times Ahead