MCD - Krispy Kreme Still A Buy After The Dip

2023-10-25 12:10:49 ET

Summary

- Krispy Kreme's Q2 2023 results showed strong revenue growth, driven by the U.S. business and Market Development segments.

- The company aims to increase its points of access and improve operational efficiency through its Hub & Spoke model, with a potential partnership with McDonald's.

- Despite some risks, Krispy Kreme's growth and strategic initiatives may make it an attractive investment opportunity.

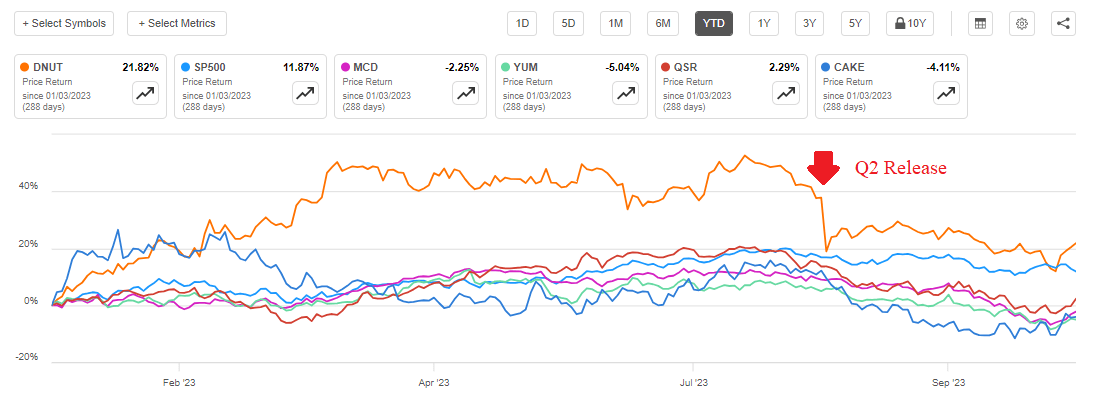

Krispy Kreme's stock ( DNUT ) has increased by nearly 23.5% since the beginning of the year, and it is currently 13% ahead of the S&P 500 index ( SP500 ). The company aims to become one of the most beloved sweet treat brands globally and has taken several actions to prove it. Its management has formed partnerships with companies like The Kroger Co. ( KR ) and Walgreens ( WBA ), but I believe that a potential collaboration with McDonald's ( MCD ) could be the one that will trigger a significant share price rally.

Financial Performance

Krispy Kreme demonstrated impressive performance across all its business segments in the last three months. Revenue increased by 9% to $408.9 million in Q2, and organic revenue increased by an even more impressive 11.4%. In fact, this was the fourth consecutive quarter that the business has seen double-digit organic revenue growth, further highlighting the strength of the business and its omnichannel strategy.

Of all Krispy Kreme's segments, the U.S. market was the most significant contributor to growth. The business in the United States increased by $22.8 million or about 9.3% and $29.8 million and 12.7% on an organic basis compared to last year. Krispy Kreme’s strategy to draw its focus on expanding its DFD strategy, coupled with strong marketing and successful price actions, seems to be a winning combination. However, despite the impressive performance of the U.S. market, it was not the fastest-growing segment within the business.

The “Market Development” section displayed even stronger operational performance. The firm witnessed impressive results from markets such as Canada and Japan, where net revenue increased by $6.4 million or about 17.4% compared to the second quarter of the year prior. Moreover, if we ignore the impact of foreign currency translations, the organic revenue grew by $8.5 million or an impressive 23.2%.

In the last three months, Krispy Kreme has further increased access points by another 462 locations or an impressive 12.8% growth year on year, leading to a total of 1035 since the start of 2023. Altogether, the number of global Krispy Kreme and Insomnia Cookies locations currently number the mind-blowing 12,872 places.

The business reported an adjusted diluted EPS of $0.07, just $0.01 lower than in Q2 of 2022.

Despite the strong business performance, Krispy Kreme's revenue fell short of the market's estimate by only $1.6 million. The difference of just 0.39% may seem insignificant, but it was enough to make investors reconsider the already high-priced shares. As a result, Krispy Kreme's shares plummeted by 13.5% on the same day. Nevertheless, the company still has a trick up its sleeve.

Some of the recent actions the firm has taken could yield much greater results and even make management's projections for the business rather conservative.

Donuts and McDonald's

Krispy Kreme aspires to be one of the world's most loved sweet treat brands, as CEO Mike Tattersfield mentioned during its second quarter press conference.

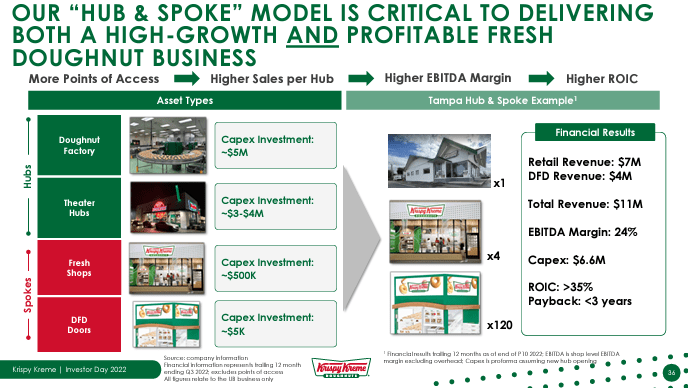

The firm is now leaning heavily towards Delivery Fresh Daily, to increase the number of points of access by as many as possible. As illustrated by the presentation.

The Hub & Spoke model of Krispy Kreme (Investor Day Presentation)

{kind=link}

The strategy of the company is simple. The more access points the business has, the more sales the hubs will have as a result. This will improve both operational efficiency and EBITDA margins.

Consumers love fresh doughnuts, so the management is ever-increasingly confident in their ability to scale the fresh points of access by between 10% and 15% annually with the long-term goal of 75,000 points of access.

However, one strategic move could make their current targets way too humble.

In October 2022, Krispy Kreme partnered with McDonald’s to sell donuts as part of the menu. Both parties started modestly with just nine McDonald’s stores in Louisville, Kentucky, selling donuts.

Over nine months later, the test expanded to over 160 McDonald’s restaurants in Kentucky alongside other partnerships with The Kroger Co. ((KR)) and Walgreens ((WBA)). However, a potential successful introduction of Krispy Kreme in McDonald's stores across every country where the doughnut maker has production facilities can be a game changer.

To put it into perspective, McDonald's has over 40,000 stores globally, of which 13,400 restaurants are in the U.S., according to Statista . In addition, Kroger has 1,237 grocery stores , and Walgreens has another 9,000 locations across the U.S. Striking a deal with those companies can provide access to over 20,000 points in the U.S. alone.

Management has also been pleasantly surprised by the success of their attempt to create premium doughnuts. During the first quarter of 2023, the business noted that Krispy Kreme’s Valentine’s Day and St. Patrick’s Day campaigns have been tremendously successful, and Biscoff Doughnuts have resonated well with consumers. Therefore, during the second quarter, the firm released new specialty doughnuts such as Cookie Blast, Minis for Mom, and Fan Favs. This proved to be another successful move, demonstrating the potential for premiumization and expanding the range of options for gifting and sharing.

In its latest financial release, Krispy Kreme stated that it is sticking to its previous outlook for fiscal 2023. The management expects revenue to increase between 8% and 10%, with 9% to 11% as organic revenue growth. Meanwhile, adjusted diluted EPS should come between $0.31 and $0.34, or an increase between 7% and 17%.

Management's expectations are truly ambitious, particularly when they partner with companies. However, their estimates may be somewhat humble if they succeed with the expansion. The potential for growth is enormous, but it comes with a significant cost that raises concerns about whether or not it's worth taking the risk.

Valuation

Krispy Kreme is a brand with huge potential, in my view.

Shares of the company are trading at around $12.91, up 23.5% since the start of the year. However, in mid-summer, Krispy Kreme was trading at $16 a share, outperforming the S&P500 by as much as 33%, before the company released its Q2 results. Although there was a dip in share prices after the report, the company's shares are still 13% ahead of the index.

Krispy Kreme's share performance (Seeking Alpha)

{kind=link}

Krispy Kreme trades a relatively high forward P/E ratio of 39 compared to some of its peers. For instance, a giant such as McDonald's trades at a forward P/E ratio of 22, and other major restaurant brands, such as Yum Brands ( YUM ) and Restaurant Brands ( QSR ), also have forward P/E ratios in the low 20s.

Krispy Kreme's premium valuation is noticeable compared to these companies, which offer much more generous dividends, ranging from a 2.59% forward yield for McDonald's to 3.36% for Restaurant Brands, compared to DNUT's humble 1.11%.

Part of this higher valuation has to do with the different stages the companies are in. None of them are estimated to see a revenue increase of 10.4% and a rise in earnings per share of 11.7%, as Krispy Kreme is.

Chipotle ( CMG ), on the other hand, is more like Krispy Kreme. The firm trades at a forward P/E ratio of 42. The company's sales are expected to grow a few percentage points more than Krispy Kreme's, or about 13.65% this year, and earnings per share by 32.7%. However, the firm does not pay dividends.

Therefore, Krispy Kreme is clearly not as expensive as it may seem. With a major catalyst such as McDonald's that could significantly boost the presence of DNUT across the United States and around the globe, the company has the potential to go much higher in my opinion. However, some macro environment risks should be considered that may pose a threat to high-flying stocks such as Krispy Kreme and Chipotle, for that matter.

Risks

The company trades at a significantly higher P/E ratio than its peers. Although the higher multiple is supported by higher revenue growth than some of the big names in the business, any slowdown in the growth rate could result in a multiple contraction, just like when the company announced its Q2 results.

Furthermore, the risk of Krispy Kreme slowing down its growth seems inevitable. The FED appears unable to stop hiking. In an interview with Bloomberg TV, Jamie Dimon warned that interest rates could rise as high as 7%. This will further add to the monetary tightening.

To make matters worse, on October 1st, congress resumed student debt payments, further constraining the spending power of a part of the population.

Conclusion

Krispy Kreme is experiencing strong growth, and I believe some of its strategic decisions can yield better results than management anticipates. Given the current macroeconomic environment, keeping our eyes open for any unexpected headwinds is important. However, I still believe the company is a "BUY" at its current price.

For further details see:

Krispy Kreme Still A Buy After The Dip