RTX - L3Harris: The Secrets Of Becoming A New Defense Star (And A Caveat)

2023-08-28 13:47:24 ET

Summary

- L3Harris Technologies stock has - surprisingly - returned to bear mode despite improved fundamentals and strong Q2 2023 earnings.

- In this update, I explain what the market is currently overlooking about L3Harris and why the future will be even better than the already very solid past.

- However, I also share why I am not an overly aggressive buyer despite the compelling valuation of this emerging defense industry star.

Introduction

After defense contractor L3Harris Technologies, Inc. ( LHX ) reported strong second quarter results , the stock has somewhat surprisingly returned to bear mode. Given the steadily improving fundamentals, particularly related to supply chain and working capital, the ongoing conflict in Ukraine, pent-up demand from several European countries, one wonders what's wrong with LHX stock. After all, it is flirting with its 52-week-low of $175.

It looks like the market is (once again) souring on the recently FTC-approved acquisition of rocket motor and munitions maker Aerojet Rocketdyne ( AJRD ). After all, LHX made headlines not too long ago with its $2 billion acquisition of Viasat's Tactical Data Links ((TDL)) product line, which the company is still digesting. Spending a total of $6.7 billion is certainly no small feat for a company that is already quite substantially leveraged. The current interest rate environment is also far from ideal for raising significant amounts of debt, especially for a company with a fourth-tier investment grade rating ( Baa2 ).

But is it all that simple and should we avoid reaching into a (modestly) falling knife just because of debt worries? I've covered LHX stock before ( Nov. 2022 , Jan. 2023 , and Jun. 2023 ), so I'm not going to go into much detail about the company's fundamentals in this article. Instead, I explain what I think the market is currently overlooking about L3Harris. However, I also address why I am not a super-aggressive buyer of LHX stock, even at this - arguably compelling - valuation.

What The Market Is Missing About L3Harris

By revenue, L3Harris is the sixth largest defense contractor in the U.S., but does not have as strong a franchise as Lockheed Martin Corp. ( LMT , e.g., F-35 platform), RTX Corp. ( RTX , e.g., commercial and military aircraft engines) or Northrop Grumman Corp. ( NOC , B-2 and B-21 bombers), all of which benefit from a "Gillette" effect, i.e., the companies profit from high-margin service and upgrade revenues.

LHX finds itself in an increasingly fragmented (but still dominated by a few) market of defense contractors, all of whom must negotiate to a greater or lesser degree for their share. As number six, L3Harris is naturally in a comparatively weak position, partly because of its lack of a bold original equipment business.

From this perspective, the 2019 merger of Harris Corp. and L3 Technologies, Inc. makes perfect sense. The merged company is in a better negotiating position with the Department of Defense ((DOD)) and international defense agencies, as well as compared with its competitors. Recall that L3Harris supplies many mission-critical components used in Lockheed's F-35, for example. As more and more parts come from a single company that eventually establishes itself as a reliable "go-to" supplier, it becomes easier to outmaneuver smaller competitors, and pricing power increases. The acquisition of Viasat's TDL business in 2022 makes a lot of sense in this context, as does the recently completed acquisition of AJRD, which is comparatively bold for the still relatively small LHX.

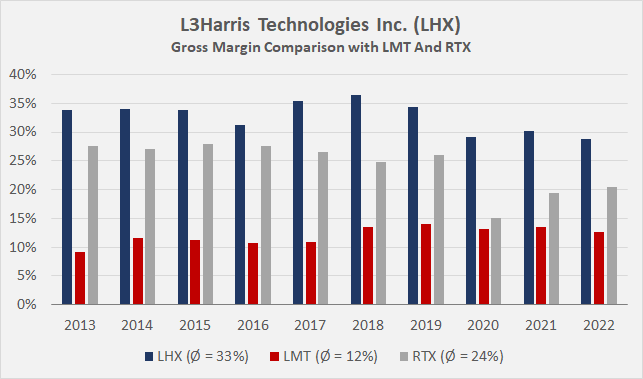

However, there remains the issue of the lack of a "Gillette" tailwind. There is certainly something to be said for owning and maintaining a franchise like the F-35, which is currently in high demand, but it is also important to remember that its development involves enormous upfront costs and high capital expenditures. This is underscored, for example, by Lockheed's comparatively weak gross margin (Figure 1).

Figure 1: L3Harris Technologies, Inc. (LHX): Gross margin comparison with Lockheed Martin Corp, LMT, and RTX Corp, RTX (own work, based on company filings)

{kind=link}

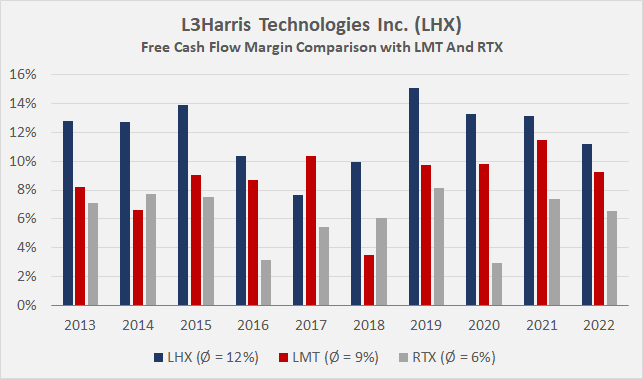

Of course, the business will eventually become more service revenue oriented, which should help profitability and dampen earnings volatility. In this context, I find LHX's performance surprisingly positive. Gross margin volatility is much lower than LMT's over the past decade (8% vs. 13%, relative standard deviation), as is free cash flow volatility (18% vs. 26%, Figure 2). RTX is no different and even slightly worse than Lockheed in terms of profitability and free cash flow volatility. However, as I discussed in my article comparing RTX Corp. to Lockheed, the situation will gradually improve as the company ramps up its GTF engine program (geared turbofan, Pratt & Whitney PW1000 family ).

Figure 2: L3Harris Technologies, Inc. (LHX): Free cash flow margin comparison with Lockheed Martin Corp, LMT, and RTX Corp, RTX (own work, based on company filings)

{kind=link}

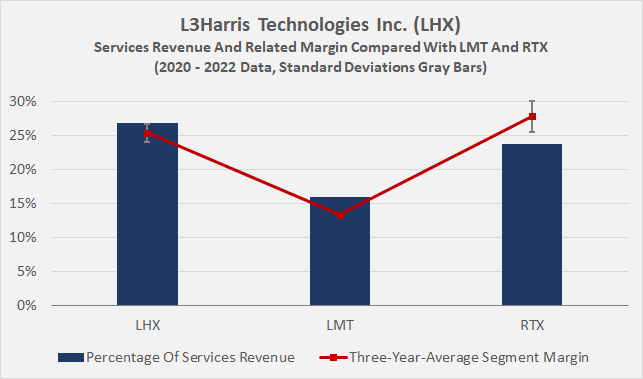

These are surprising findings, considering that LHX does not benefit from a similar business model to its larger competitors. I don't want to be misunderstood here - RTX and LMT are good companies with very strong franchises, but LHX has obviously carved out some really nice niches where it can excel and generate solid margins. In my view, LHX is "riding the coattails" of larger defense contractors, thus benefiting from the high margins of selling "razor blades," without the high upfront costs of developing a new base business. In addition, L3Harris generated between 25% and 29% of its total revenue from services over the past three years (Figure 3), more than competitors LMT and RTX. However, the strong growth in services revenue over the past three years should not be over-interpreted, as supply chain issues (discussed in my January article) resulted in fewer finished products and thus lower segment revenue (but higher book-to-bill).

Figure 3: L3Harris Technologies, Inc. (LHX): Services revenue and related margin compared with Lockheed Martin Corp, LMT, and RTX Corp, RTX (own work, based on company filings)

{kind=link}

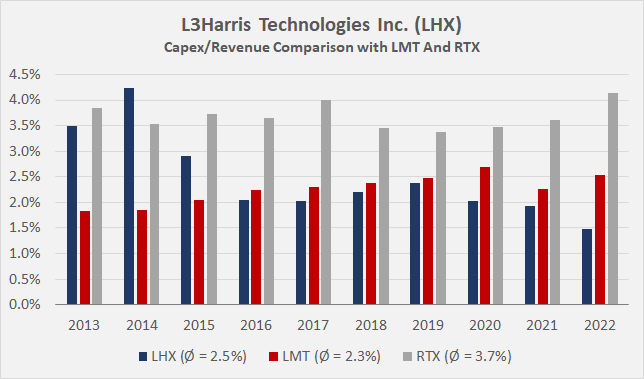

The emphasis on service revenues and the low exposure to capital-intensive base businesses should translate into comparatively low capital expenditures. However, Figure 4 shows that LHX invests about as much as Lockheed relative to revenue. Given Raytheon's recent investments (GTF franchise), the comparatively higher capital expenditure percentage makes sense. At the same time, Lockheed's comparatively low percentage suggests that its platforms are fairly mature, which puts its weaker free cash flow profitability (Figure 2, above) in a different light. Returning to LHX, I think it's worth noting that part of the comparatively high capex is due to the Harris legacy period - between 2020 and 2022, and including the trailing-twelve-months period, LHX's average capex spending fell to 1.8% of revenue, well below Lockheed's corresponding average of 2.5%.

Figure 4: L3Harris Technologies, Inc. (LHX): Capital expenditures in percent of revenue, compared with Lockheed Martin Corp, LMT, and RTX Corp, RTX (own work, based on company filings)

{kind=link}

What Keeps Me From Being Too Aggressive With LHX Stock

The absence of a base business like RTX's Pratt & Whitney unit in turn means that L3Harris' moat is weaker than that of its larger competitors. Pratt & Whitney's GTF engine, for example, was/is a huge long-term project involving a host of new technologies (see my detailed discussion of the turbine disk quality issue) that is still at an early stage from a profitability perspective. Reliance on such a robust base business virtually guarantees a company a long-term economic dividend in the form of high-margin service revenues and because of the more or less mandatory upgrade cycles. The lock-in effects, especially in commercial aviation and defense, cannot be overstated.

LHX is definitely in a weaker bargaining position than its peers and therefore probably has weaker pricing power and suffers from comparatively low long-term cash flow visibility. However, this is where Aerojet Rocketdyne comes in, as it will definitely improve the company's cash flow visibility and strengthen L3Harris' moat - remember that Lockheed was interested in buying AJRD , but the deal was ultimately blocked by the FTC . I don't expect LHX to benefit from the same synergies and increase in monopolistic tendencies as Lockheed would have (e.g., AJRD is a major supplier to RTX ), but the transaction is still an important step in the right direction and strengthens L3Harris' position as a major defense contractor.

Aside from the fact that L3Harris' economic moat is somewhat weaker than RTX's and LMT's, in part due to its much smaller size, it's the risks associated with regular mergers and acquisitions that keep me from being too aggressive with LHX stock.

There are so many moving parts that need to be considered, and much is required to actually unlock operational synergies and reduce overhead costs in a meaningful way. In this context, the somewhat complex portfolio of L3Harris should be mentioned, and the synergies created by the addition of a rocket engine company are far from easy to understand, let alone quantify. At the very least, however, the acquisition should strengthen LHX's position as a single-source provider of trusted goods and services, improve the combined entity's negotiating position, and enable overhead cost rationalization.

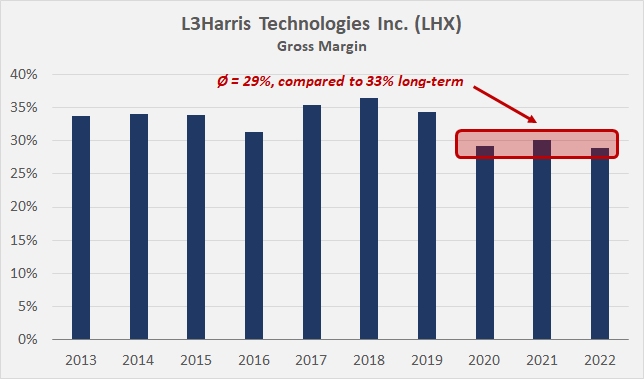

That said, L3Harris' portfolio, which at first glance appears to be poorly focused (but is obviously well managed given its solid profitability), makes me a bit wary. Remember that the company is still in the process of realizing the efficiencies from the L3 Technologies/Harris merger (see the decline in gross margin and apparent stabilization at a lower level, Figure 5), but to be fair, it should be added that the merger occurred at a rather inopportune time, about eight months before the pandemic-related lockdowns hit. It should also be noted that the integration of Viasat's TDL business is ahead of schedule (p. 4, 2023 Q2 Investor Letter ).

Figure 5: L3Harris Technologies, Inc. (LHX): Gross margin over the last ten years, comparison of three-year average margin with long-term average (own work, based on company filings)

{kind=link}

Lastly, management isn't just accumulating assets left and right - plans have recently surfaced for L3Harris to divest its avionics products business , confirming management's hints in previous earnings announcements about how they plan to deleverage after the AJRD acquisition. Given the diversity of the company's offering - the avionics sub-segment is part of Space & Airborne Systems (SAS, 35% of 2022 revenue) - I can't judge whether it makes sense from a portfolio perspective to divest these assets. However, considering that there is likely little room for recurring service-related revenue due to the more or less regular replacement of these products, this may have also contributed to management's decision. Finally, it could be that the components as a whole are complex and expensive to manufacture, which would put pressure on otherwise good margins. The SAS segment is one of LHX's weaker segments in terms of profitability.

Conclusion

L3Harris is an excellent and well-managed company that is slowly but surely expanding its presence as a defense contractor and strengthening its moat in the process. Considering that services account for about a quarter of the company's revenue, one can conclude that L3Harris has built several "poor man's" Gillette franchises. In other words, L3Harris generates significant recurring cash flow from upgrading and replacing products that are deeply integrated into several of the well-known commercial and military aerospace platforms.

This in turn means that its moat is comparatively weaker and its pricing power is more modest than that of its competitors, but LHX's margins are surprisingly solid due to its lower capital expenditure requirements and low direct reliance on platforms with high upfront investments. However, because of this approach, the company's cash flow visibility is limited. The recently completed acquisition of Aerojet Rocketdyne will improve L3Harris' earnings and cash flow visibility, but the effect should not be overstated, as the rocket engine manufacturer currently generates annual sales of only slightly more than $2 billion - equivalent to about one-eighth of L3Harris' 2022 revenue.

The current lack of owned major equipment platforms also suggests that LHX's cash flow volatility should be higher than larger competitors such as LMT and RTX. However, based on the data for the last ten years, the opposite is true. This suggests that L3Harris is very well managed, especially given its rather complex product portfolio.

However, despite all the positive aspects, one should be cautious about a comparatively small company that routinely engages in M&A and takes on considerable debt in the process. There is always the risk of imponderables (e.g., the pandemic and related secondary effects), and of course the failure of the expected synergy effects to materialize. For this reason, I have set a smaller position limit - 1.25% - for LHX stock than for LMT and RTX stock (2% each) - the other two defense stocks I hold for the long term.

I also believe that the investment case at hand requires a lot of patience due to the recently completed acquisitions, the related integration work and the significant debt assumed (see my last two articles). In order to maintain the Baa2 credit rating (outlook revised to negative ), share buybacks and dividend growth will likely be quite modest for a few years (as evidenced by the latest increase of only 1.8% versus a five-year CAGR of 15% ) until leverage is back in check.

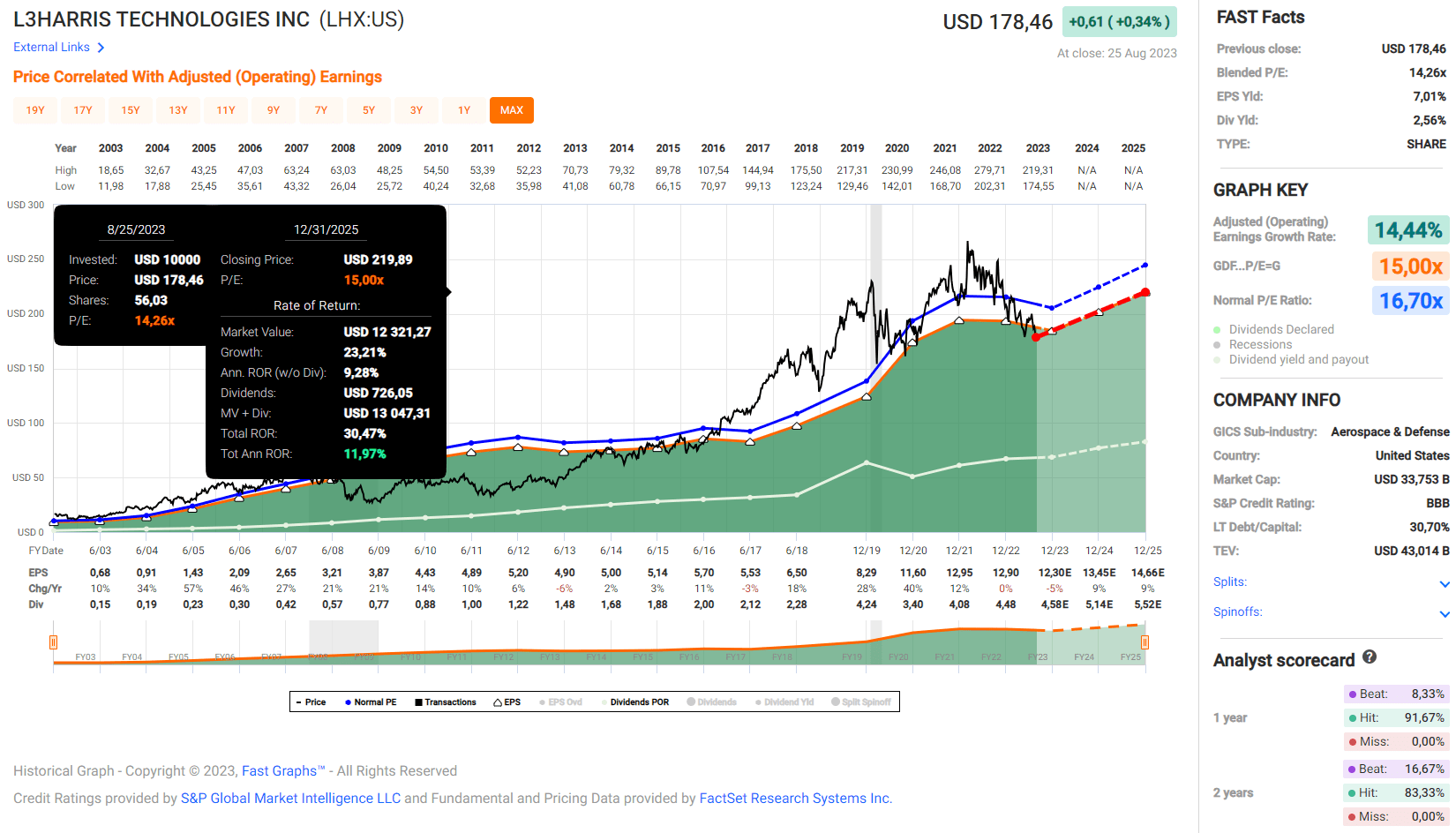

With Mr. Market - largely unjustified in my view - once again focusing on the uncertainties and risks associated with the AJRD acquisition and disregarding L3Harris' mostly solid operating performance, I added to my position last Friday. With a blended price-to-earnings ratio of 14 (Figure 6), a dividend yield of nearly 2.6% ( five-year average of 1.8% ), and a free cash flow yield of about 6%, I think LHX stock is a compelling value opportunity with good growth prospects and a solid track record (long-term earnings and cash flow growth of 14% and 11%, respectively).

As always, please consider this article only as a first step in your own due diligence. Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well.

Figure 6: L3Harris Technologies, Inc. (LHX): FAST Graphs chart, based on adjusted operating earnings per share (FAST Graphs tool)

{kind=link}

For further details see:

L3Harris: The Secrets Of Becoming A New Defense Star (And A Caveat)