CA - La-Z-Boy Shoots Comfortably Higher

2023-12-02 21:50:09 ET

Summary

- La-Z-Boy's financial performance in Q2 of fiscal year 2024 exceeded analysts' expectations despite a decline in revenue and profits.

- The decline in revenue was driven by weakness in both the Wholesale and Retail segments, as the furniture industry recalibrated after strong demand during the pandemic.

- The company's stock remains cheap, and it has a robust balance sheet, making it a favorable investment option.

Regardless of how your own personal financial situation might be, the fact of the matter is that the economy is currently being impacted by high inflation and high interest rates aimed at combating that inflation. Naturally, during times of difficulty, one of the first things that consumers tend to cut back on is furniture and related goods. So it shouldn't be a surprise to see the financial performance of some furniture companies worsening on a year-over-year basis. But even though there might be a decline, some of these companies are still posting results that exceed analysts’ expectations.

The most recent example can be seen by looking at one of the most famous furniture brands in the world, La-Z-Boy ( LZB ). After the market closed on November 29th, the management team at La-Z-Boy announced financial results covering the second quarter of the company's 2024 fiscal year. Although revenue and profits worsened year over year, both the top and bottom lines came in stronger than analysts expected. Add on top of this how cheap shares of the company remain, and I do believe that the company warrants a soft ‘buy’ rating at this time.

A tough time has been well-rewarded

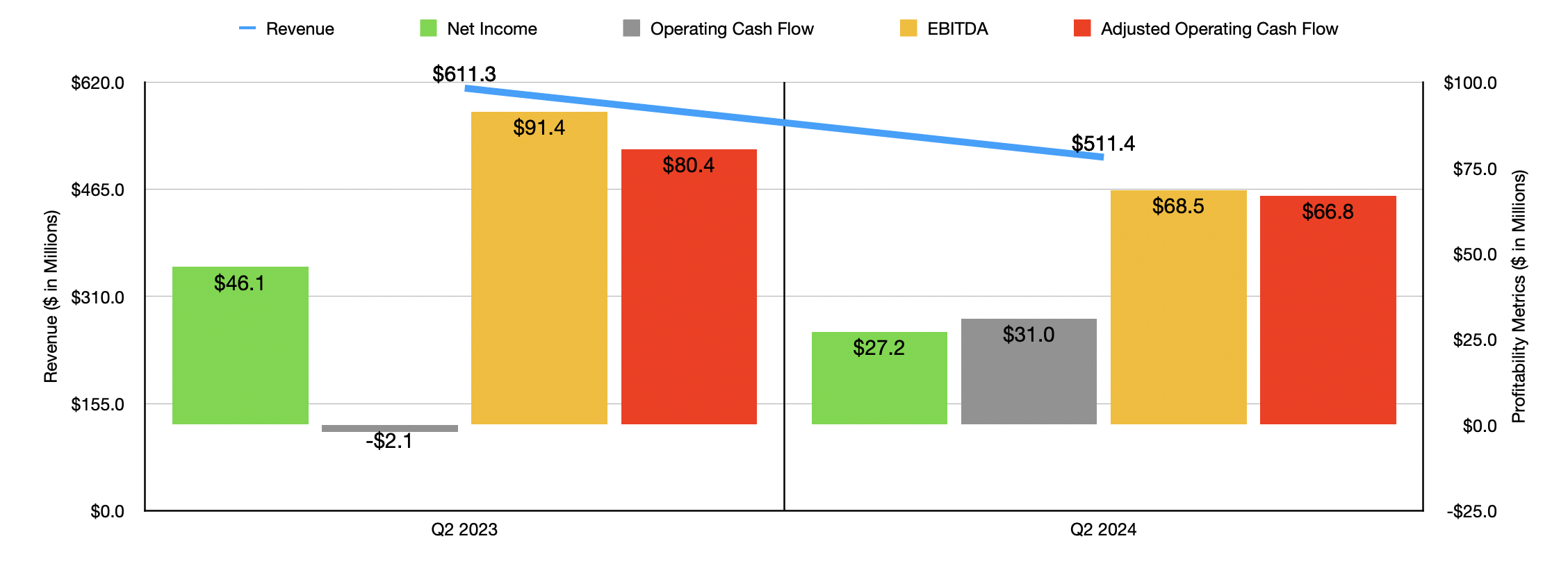

As I mentioned already, after the market closed on November 29th, the management team at La-Z-Boy announced financial results covering the second quarter of the company's 2024 fiscal year. In response to that move, shares rose 11% on November 30th. For that quarter, the company reported sales of $511.4 million. That represents a decline of 16.3% compared to the $611.3 million the company reported one year earlier. Although revenue did fall rather significantly, it did manage to come in at $7.1 million above what analysts expected it to be. This drop in revenue was driven by weakness across the board. For instance, revenue for the Wholesale segment plunged 18.2% from $446.2 million last year to $365 million this year. That decline, according to management, was driven by a reduction in the number of units delivered as the furniture industry recalibrates. That recalibration comes after a couple of very interesting years in which demand was particularly strong because of the pandemic and the spending that occurred during that window of time.

{kind=link}

The subsequent reduction in demand is basically the industry rebalancing to get back to a more typical seasonal business model. Some of the drop in revenue was also driven by changes in pricing and promotional actions implemented by management. The other segment of the company is the Retail segment. Sales there were also hit rather hard, falling 15% from $252.2 million to $214.3 million. Even though the company benefited to the tune of $5.7 million from new stores added to the company’s network, this was more than offset by the same aforementioned rebalancing efforts seen by the industry more broadly.

On the bottom line, the company also saw weakness. For the quarter, La-Z-Boy reported $0.63 in profits per share. That's down from the $1.07 per share reported the same time last year, but it is still $0.09 per share above what analysts were anticipating. The profits per share reported by the company translated to net income of $27.2 million, which was significantly below the $46.1 million reported in the second quarter of 2023. Most other profitability metrics followed a similar trajectory. The one exception was operating cash flow. It managed to climb from negative $2.1 million to positive $31 million. But if we adjust for changes in working capital, we would get a decline from $80.4 million to $66.8 million. Meanwhile, EBITDA for the business managed to fall from $91.4 million to $68.5 million.

{kind=link}

As you can see in the chart above, the first half of the 2024 fiscal year in its entirety was rather rough compared to the first half of the 2023 fiscal year. So the second quarter weakness that we saw was not a one-time blip on the radar. Unfortunately, investors should probably anticipate this trend continuing. In the second quarter earnings release, management stated that revenue for the third quarter should come in at between $515 million and $535 million. That would be down quite a bit compared to the $572.7 million reported for the third quarter of the 2023 fiscal year.

Even for the third quarter, management did not really provide much in the way of guidance. Yes, they reported that range for revenue and they reported some expectations when it comes to margins. But the company did not come out with enough data to allow us to know what earnings should be like. Realistically speaking, earnings and cash flows should continue to worsen compared to what they were in the last fiscal year. Based on my own estimates, net income for this year should come in somewhere around $97 million. Adjusted operating cash flow should be around $216.8 million, while EBITDA should be about $187.2 million.

{kind=link}

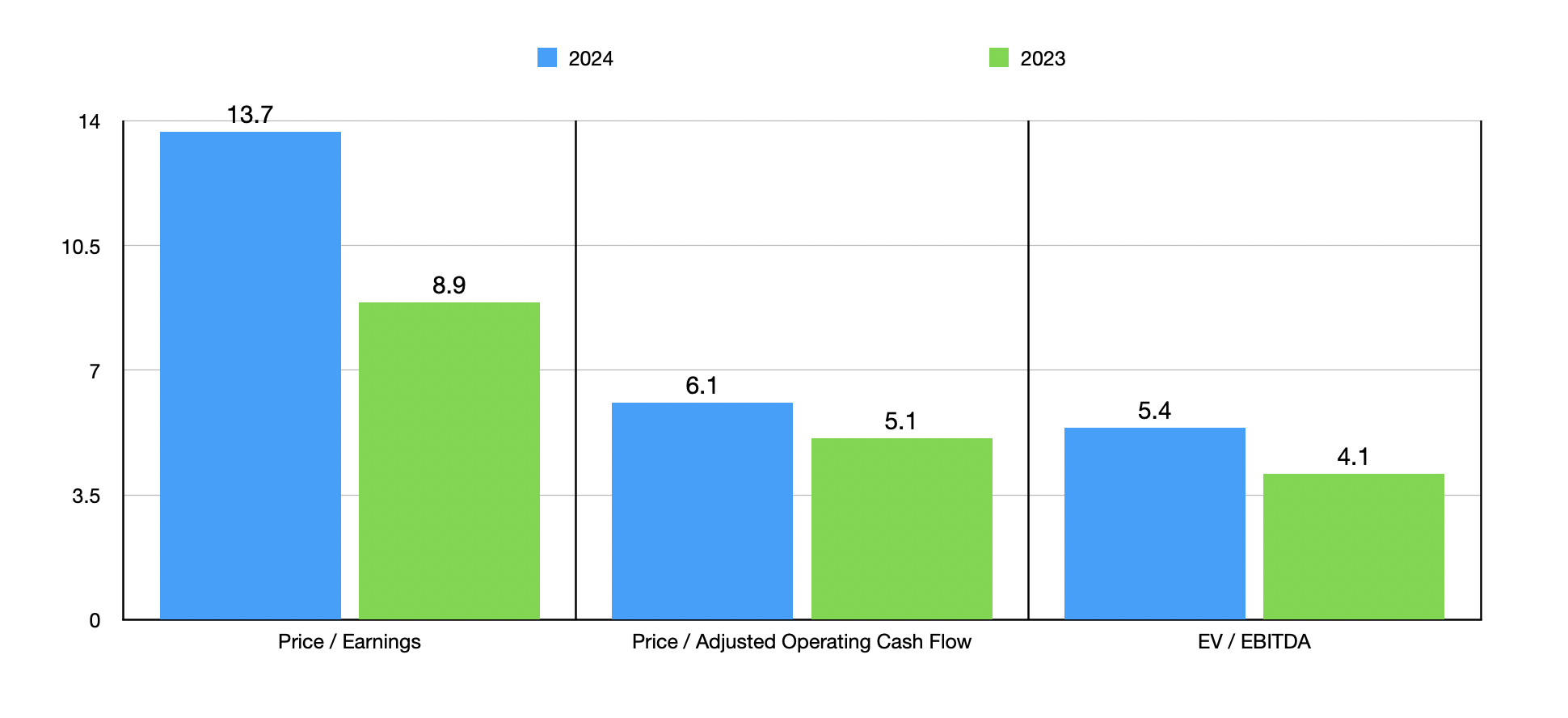

Using those figures, I was able to value the company as shown in the chart above. I also valued the company using data from the 2023 fiscal year. While the stock does look pricey on a price to earnings basis, it does look quite cheap when it comes to the other profitability metrics. What's more, the stock looks to be more or less fairly valued compared to similar firms. In the table below, you can see that I priced the company next to five similar enterprises. On a price to earnings basis, two of the five firms were cheaper than our target. This number increases to three of the five using the price to operating cash flow approach. Meanwhile, using the EV to EBITDA approach, I found that one of the four companies that had positive results was trading cheaper than La-Z-Boy happens to be.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| La-Z-Boy |

| 13.7 |

| 6.1 |

| 5.4 |

| Ethan Allen Interiors ( ETD ) |

| 7.7 |

| 8.8 |

| 3.9 |

| Tempur Sealy International ( TPX ) |

| 18.4 |

| 12.5 |

| 12.2 |

| Dorel Industries ( OTCPK:DIIBF ) |

| 0.7 |

| 1.2 |

| N/A |

| The Lovesac Company ( LOVE ) |

| 23.3 |

| 4.6 |

| 8.8 |

| Mohawk Industries ( MHK ) |

| 321.2 |

| 4.4 |

| 31.7 |

There is one other thing to mention about La-Z-Boy at this time. And that is that the company has an incredibly robust balance sheet. It has no debt on its books and it enjoys $333.5 million in the form of cash and cash equivalents. This means that the business has a tremendous amount of flexibility should times get difficult. And even during these tough times, cash flows remain positive. So the probability of it needing to tap into any sizable portion of cash is quite low in my opinion. In fact, if cash balances remain elevated, some greater usage for that cash, whether it is growth-oriented or focused on returning capital to shareholders, might not be unrealistic to expect.

Takeaway

Operationally speaking, the picture for shareholders of La-Z-Boy is nowhere near as great as it could be. Having said that, shares have achieved remarkable performance since I last wrote about the company in an article published on November 22nd of last year. In that year or so, shares have seen upside of 39.3% at a time when the S&P 500 has increased 14.8%. Naturally, that returned disparity makes me happy that I rated the company a ‘buy’. As for what the future holds, I do recognize that the picture is worsening. But given how cheap the stock is and the robust balance sheet the business enjoys, I would argue that a bit of additional upside from here is likely warranted. Because of that, I have decided to keep the company rated a soft ‘buy’ for now.

For further details see:

La-Z-Boy Shoots Comfortably Higher