NVDA - Lam Research And Applied Materials: Downgrading Semi-Caps To Hold

2023-07-24 18:52:47 ET

Summary

- We’re downgrading Lam Research Corporation and Applied Materials, Inc. to Hold.

- Our downgrade is driven by our belief that the semi-cap sector is at a higher risk profile due to weaker-than-expect end-market demand impacting wafer fab equipment spending.

- Lam Research and Applied Materials stocks are up 51% and 41%, respectively; we think both stocks have captured the expectation of recovery but don’t see the stocks working in 2H23.

- We continue to expect both stocks to outperform in the mid to long term with an upturn in wafer spending in 2024 and 2025, but see no catalyst driving spending in 2H23.

- We recommend investors wait on the sidelines of the semi-cap players in 2H23 as we continue to see macro headwinds weighing on WFE spending.

We're downgrading Lam Research Corporation ( LRCX ) and Applied Materials, Inc. ( AMAT ) to Hold ahead of earnings as we don't expect the semi-cap to outperform in 2H23. This is due to expected macro weakness pressuring end-market demand and, by extension, wafer fab equipment ((WFE)) spending.

LRCX and AMAT operate in the semi-cap business of etching and deposition, which accounts for roughly 46.7% of the semiconductor equipment market. We continue to expect both companies to be well-positioned to outperform in the mid to long run due to the upturn in WFE spending next year and in 2025, driven by the higher capital intensity of future advanced process nodes in logic and memory for AMAT and increased complexity in next-gen 3D NAND, advanced logic and future-gen DRAM patterning for LRCX. However, we see lower WFE spending in 2023 as customers lower capex spending due to the worsening macro condition.

Both LRCX and AMAT have outperformed the S&P 500 (SP500) significantly YTD; LRCX is up 51%, while AMAT is up 41%, outperforming the S&P 500 by 32% and 22%, respectively. We think both stocks have captured the expectation of recovery but don't expect the outperformance to carry into the second half of the year due to signals of weaker end-market demand weighing on customers' WFE spend. In the short term, we don't see meaningful catalysts for the semi-cap spend. We recommend investors stay on the sidelines and explore favorable entry points on pullbacks through 2H23.

The following graph outlines the stock performance of LRCX and AMAT against the S&P 500 YTD.

YCharts

A higher risk profile for WFE spending

We expect the near-term financial performance of both LRCX and AMAT to remain somewhat uneventful due to lower WFE spend in 2H23 driven by end-market weakness. According to a research report by Semi in early June, "fab equipment spending shows a downturn to about US$79B or -20% Y/Y"; we believe the situation may be worse than this. We recently downgraded the lithography leader, ASML Holding N.V. (ASML), on the same sentiment, expecting macro headwinds and a softer EUV growth outlook to weigh on the stock in the near-term. We maintain a negative view of the semi-space heading further into 2H23, specifically after ASML reported earnings last week, highlighting a lower EUV growth outlook for the year from 40% growth to 25%. We think the semi-caps are a leading indicator of what will play out in the broader semi-peer group this quarter.

In their earnings calls last quarter, both LRCX and AMAT vocalized concerns over the lower capex spending in 2023 as customers work down inventory due to the end-market weakness; ASML confirmed the macro weakness this quarter reporting EUV weakness. The narrative has been that China-related demand would help offset the broader macro weakness, and well this looks different for each of the semi-cap companies in our coverage; we don't expect the Chinese-led demand will be enough to drive outperformance for LRCX and AMAT in 2H23. LRCX continues to be specifically pressured by memory weakness, which accounted for 32% of total revenues last quarter, down from 66% in a year ago quarter. Memory business is experiencing lower fab utilization and reduced investments in capacity as customers reduce wafer output to drive down inventory levels.

AMAT is also bearing the brunt of memory weakness as well as pressure in leading-edge foundry logic markets as customers trim spending due to macro headwinds. Customers are dealing with a surplus inventory, which is the result of lower-than-expect end-market demand. We think ASML's earnings report was a signal that the macro weakness will continue into 2H23. We don't expect the A.I. boom cannot offset the end-market weakness.

We continue to believe not all players will benefit from the A.I. boom; we think Nvidia Corporation ( NVDA ) will be the primary beneficiary as it leads design wins in 2023 and 1H24. We maintain a grim outlook on the semi-cap sector in 2H23 and recommend investors hold the stocks due to the short-term uncertainty and revisit after the weakness plays out.

Valuation

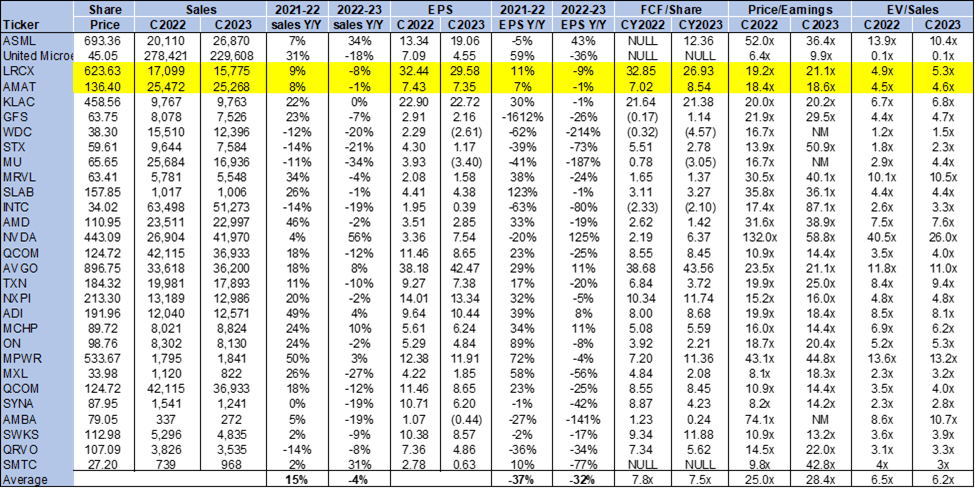

LRCX and AMAT are trading below the peer group average. On a P/E basis, LRCX is trading at 21.1x C2023 EPS, $29.58, and AMAT is trading at 18.6x C2023 EPS, $7.35, compared to the peer group average of 28.4x. Turning to EV/Sales, LRCX is trading at 5.3x C2023 while AMAT is trading at 4.6x versus the peer group average at 6.2x. While the valuation of both stocks is relatively attractive, we don't recommend investors buy in on weakness, as performance in the second half of the year should be weighed down by the weaker-than-expected end-market dynamics.

The following chart outlines the valuation of LRCX and AMAT against the peer group.

{kind=link}

Word on Wall Street

Wall Street is bullish on both LRCX and AMAT. Of the 27 analysts covering LRCX, 15 are buy-rated, and the remaining are hold-rated. The stock is currently priced at $624 per share. The median sell-side price target is $581, while the mean is $600, with a potential downside of 4-7%.

The following charts outline LRCX's sell-side ratings and price-targets.

TSP

Of 32 analysts covering AMAT , 20 are buy-rated, ten are hold-rated, and the remaining are sell-rated. The stock is currently priced at $136 per share. The median sell-side target is $143, while the mean is $142, with a potential 4-5%.

The following charts outline AMAT's sell-side ratings and price-targets.

TSP

What to do with the stocks

We don't expect the semi-cap names in our coverage to outperform in 2H23 due to the macro headwinds pressuring WFE spending as end-market demand continues to be weaker-than-expected. We believe both Lam Research Corporation and Applied Materials, Inc. stock will outperform in the mid-to-long run once WFE spending re-accelerates, but don't see catalysts driving semi-cap spending in 2H23; hence, we recommend investors wait on the sidelines for the weakness to play out before exploring favorable entry points into either of these stocks.

For further details see:

Lam Research And Applied Materials: Downgrading Semi-Caps To Hold