C - Lansing Street Advisors Q3 2023 Letter

2023-11-24 02:35:00 ET

Summary

- Lansing Street Advisors is a full-service fiduciary firm specializing in wealth enhancement and financial stewardship, combining decades of personal finance, investment, and life strategy guidance.

- Only a handful of stocks are responsible for all the returns in the S&P index in 2023, while the majority of the stock market remains in a bearish phase.

- Retail investors have a significant overweighting of FAANG+ stocks, leading to questions about diversification and risk management.

- The bond market is facing the possibility of three consecutive years of negative returns, which is unprecedented in U.S. history.

Introduction

The entire stock market comes down to one Dave Matthews song: Seven - song by Dave Matthews Band

Baby when I think about you, All I want to do is be by your side, Take a little ride.

Over the last 24 months, we have been witnessing historical events. In 2022, an uncommon situation unfolded as both stocks and bonds had negative returns in the same year. Now, in 2023, we find ourselves in a story where only a handful of stocks are responsible for all the returns, and we're facing the possibility of three consecutive years of negative bond returns, something that has never occurred in U.S. history.

For the first three quarters of 2023, SEVEN specific stocks have been the sole contributors to returns in the S&P index ( SP500 , SPX ). At the same time, bond markets have struggled, staying in negative territory, which raises the specter of negative bond returns for the third year running-an unprecedented event in the annals of U.S. financial history.

As I write this, it's crucial to note that numerous major stock indices, including the Dow Jones, developed international, emerging markets, small-cap U.S., dividend growers, dividend payers, and certain value indices, have all posted negative returns for the year. Diversifying investments across different equities hasn't provided the expected returns this year, with large-cap growth stocks continuing to dominate, driven by just a select few key players.

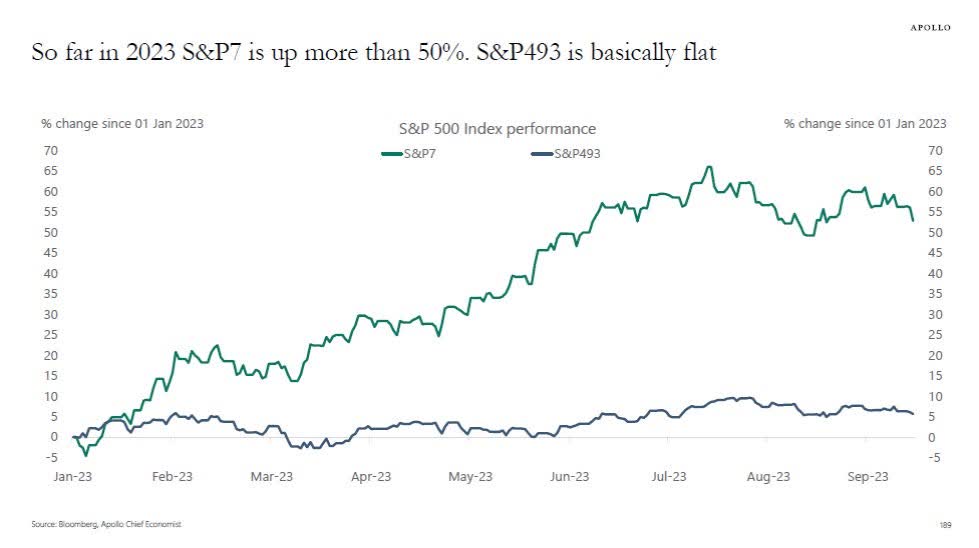

Torston Slok Apollo Group -The seven biggest stocks in the S&P500 are up more than 50% in 2023, see chart below. The remaining 493 stocks are basically flat. The bottom line is that if you buy the S&P500 today, you are basically buying a handful of companies that make up 34% of the index and have an average P/E ratio around 50.

{kind=link}

The significance here lies not only in the fact that the "magnificent seven" are responsible for all the returns, but also that the remainder of the S&P index has dipped below its 2021 lows. This chart holds particular importance for two key reasons: firstly, the majority of the stock market remains in a bearish phase, and secondly, as we will discuss, our current situation does not indicate the presence of a market bubble.

{kind=link}

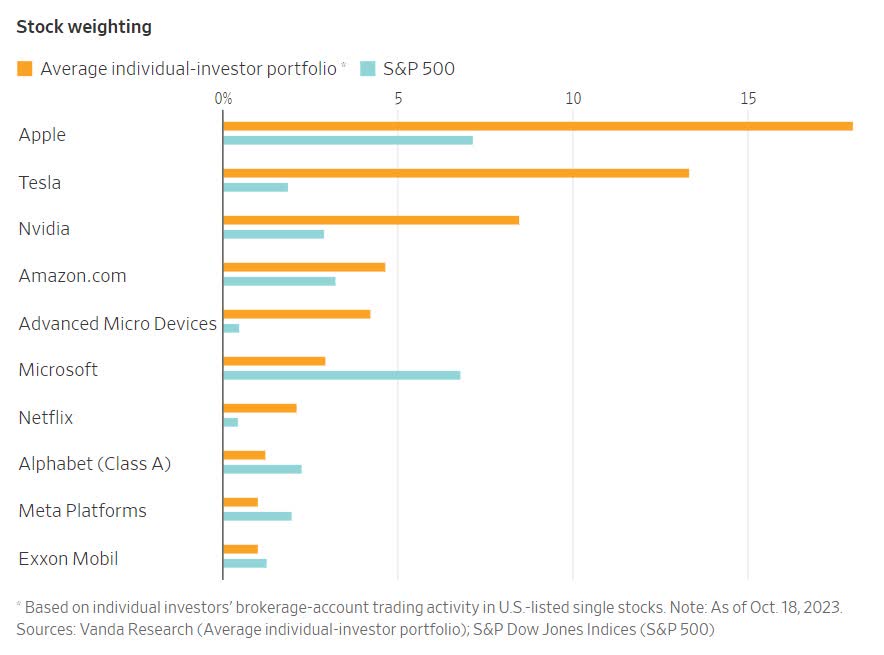

In the typical investor's portfolio, there is a noticeable overemphasis on FAANG+ stocks, with a particularly significant overweighting of Apple ( AAPL ) and Tesla ( TSLA ). This trend is akin to retail investors echoing the sentiments expressed in Dave Matthews' song "Seven," where they seem captivated by these FAANG stocks, as if singing, "baby when I think about you, all I want to do is be by your side."

As illustrated in the chart below from The Wall Street Journal, individual investors have allocated a substantial portion of their portfolios to Apple and Tesla, with these holdings being four times larger than the weightings of these companies in the S&P index. Many of these investors likely also hold the S&P within their 401k retirement plans, further exacerbating their overweight position in these stocks. While this strategy has proven successful for an extended period, it raises important questions about diversification and risk management.

{kind=link}

As our readers know, my mantra is that investing is a psychology game not an IQ game.

The effect of money on your brain is similar to that of cocaine, says Kabir Sehgal, author of the book Coined . Neuroeconomists (scientists who research how the brain is affected by money) have performed several brain scans on individuals who were about to make money, and the results were staggering, says Sehgal. The studies show that these people had the same neurological response to making money in their "pleasure centers" as someone who was high on cocaine.

It's good to keep in perspective the level of volatility around these stocks. From Bloomberg, the average active amateur investor's portfolio was down about 30% in 2022, according to data compiled by Vanda Research , which studies self-directed retail traders globally. By contrast, the S&P 500 Index has lost 17%. Therefore during a correction, you need to withstand a drawdown of double the S&P.

Can the Magnificent Seven last forever? Renowned advisor Peter Mallouk draws on research from DFA to remind us that historical probabilities tend to challenge the notion of FAANG+ stocks enduring indefinitely. While it's true that these are exceptional companies with strong financial foundations and consistent profitability, maintaining a historical perspective is valuable, as it helps us remain mindful of the ever-changing landscape of the financial markets.

Investors should remember that Citigroup's ( C ) stock, once above $500, now trades at $39. Many wellknown companies share a similar trajectory.

{kind=link}

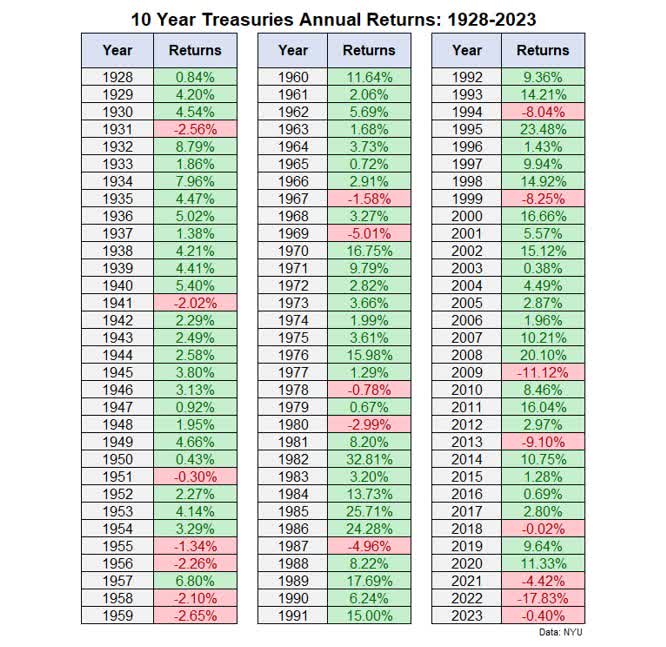

Beyond the "Magnificent Seven," the noteworthy financial narrative unfolds in the bond market. "Safe" bonds find themselves in uncharted territory, confronting the possibility of a three-year stretch of negative returns, an unprecedented occurrence.

2022 was the worst year on record for bonds, according to Edward McQuarrie, an investment historian and professor emeritus at Santa Clara University. "Even if you go back 250 years, you can't find a worse year than 2022," he said of the U.S. bond market.

The first 3-year downslide in American history of 10 year-treasury returns. @charliebilello

{kind=link}

Part I: Bonds

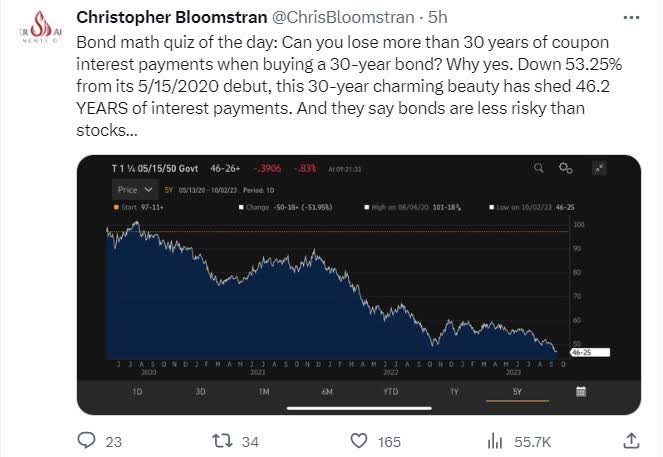

Longer-term bonds, especially the 30-year variety, saw a significant crash, surpassing the sell-off in stocks during the 2008 financial crisis. It's worth emphasizing: bond holdings performed worse than stocks during the most significant financial crisis of our time.

{kind=link}

46 Years of Interest Payments Gone on 30-Year Bond

{kind=link}

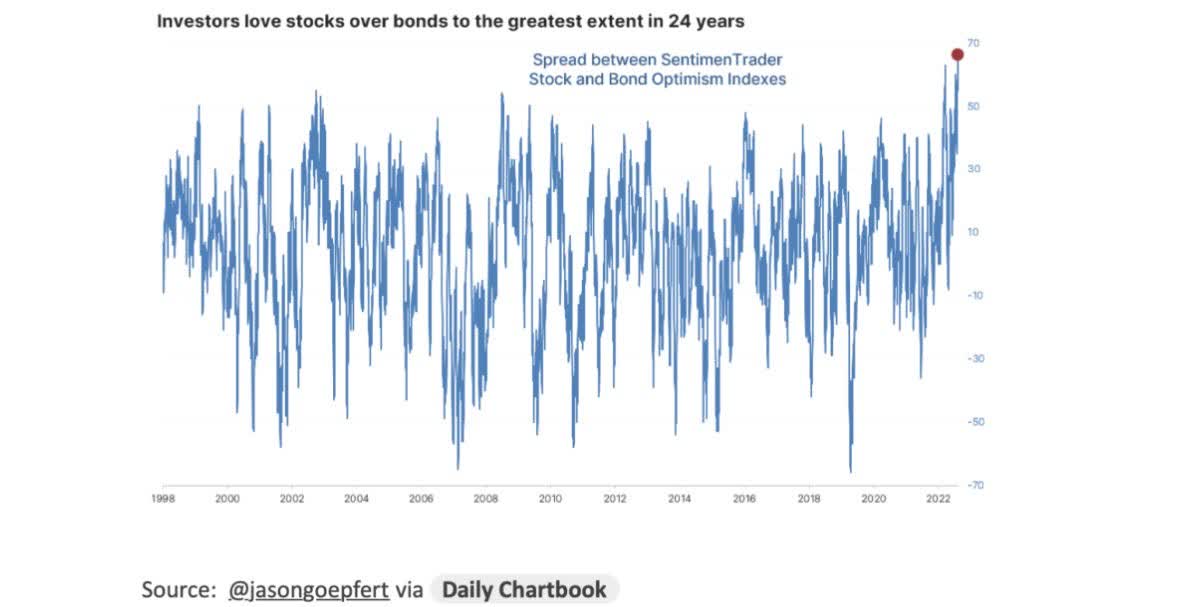

In terms of sentiment, I've observed that this bond market turmoil has led retail investors, including myself, to develop a strong preference for stocks while harboring significant aversion to bonds. This sentiment shift marks the highest level of stock favoritism and bond distrust in the past 24 years. As a side note, it's noteworthy that even a conservative portfolio comprising dividend-paying stocks and municipal bonds has yielded negative returns in 2023.

{kind=link}

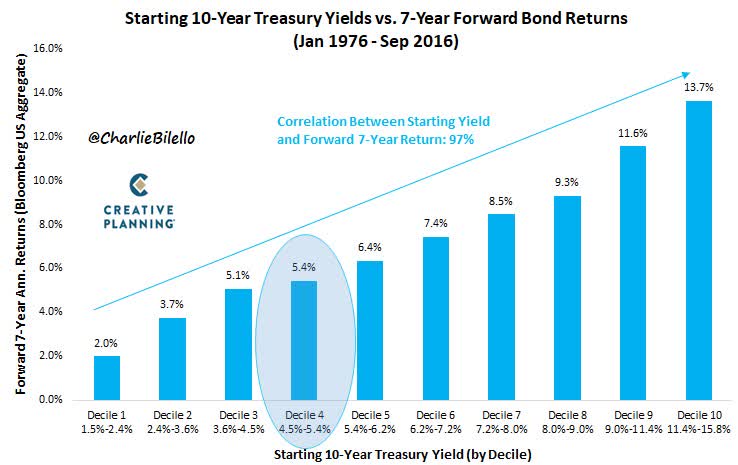

The problem is just when we begin to develop a distaste for bonds, they become increasingly appealing. This is because the 5-year return on bonds exhibits a 97% correlation with the coupon rate, and the recent rise in interest rates is actually enhancing the value of fixed income investments.

{kind=link}

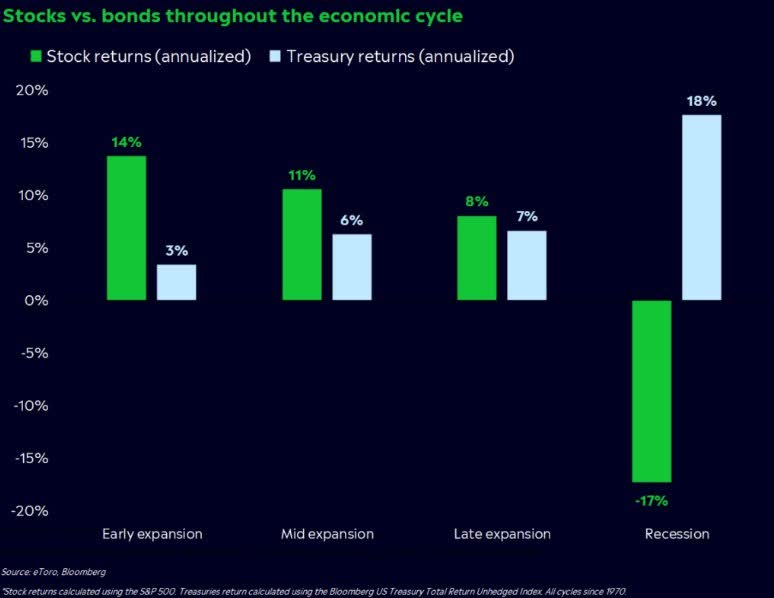

Another reason bonds are gaining appeal is their downside protection during recessions. Historical data shows that bonds tend to outperform significantly during economic downturns, as evident in the chart below, with bonds delivering an impressive +18% return compared to stocks' -17%. Although this trend didn't hold in 2022, as the 10-year yield reaches 5%, we can anticipate that stocks and bonds will cease their simultaneous decline at some point.

{kind=link}

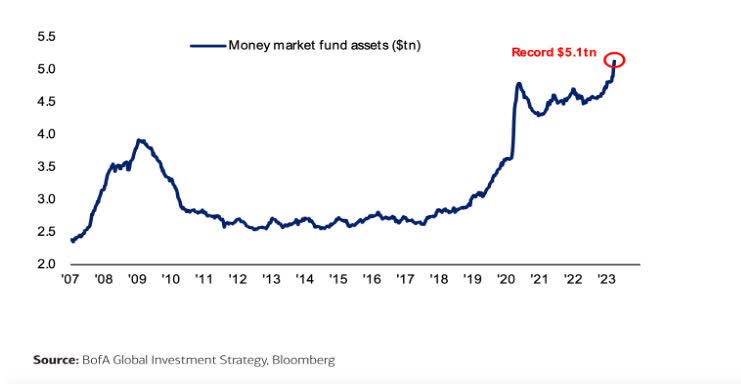

Right now, retail investors are FAANG+ and 5% cash, and that combo has crushed all other diversified portfolios in 2023. Can it last? See the money market chart from our last quarter letter (below) plus my FAANG comments above.

{kind=link}

Part II: Stocks

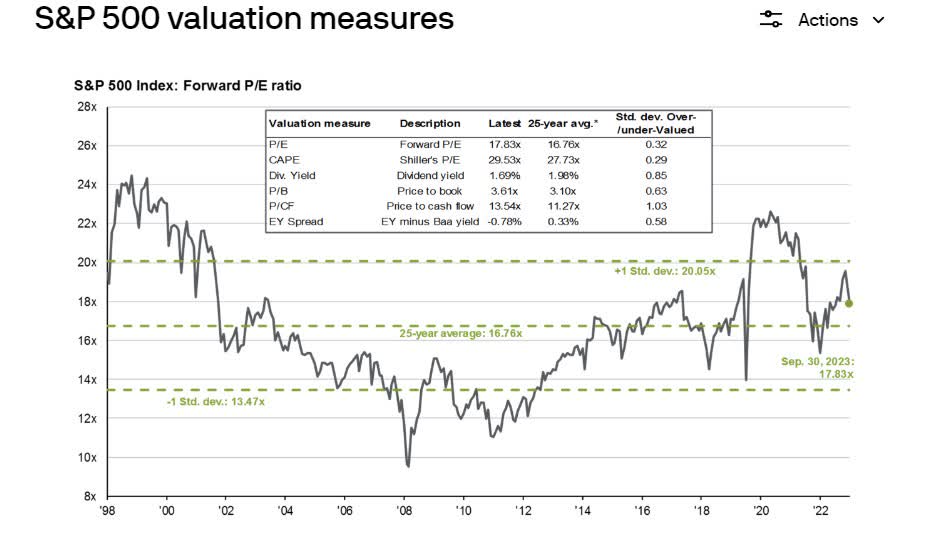

Here is a familiar chart for our readers. The good news is that stocks don't seem to be in a bubble right now. The chart below from JP Morgan uses various fundamental measures to obtain the valuation of S&P versus history. High on the chart is expensive, see 1999 internet bubble and 2021 Covid bubble (red). Low is cheap, see 2008 Great Financial Crisis (green). And to bring us to date, since this chart ends in September, if we consider the further pullback in October, we're now approaching the 25-year median valuation.

{kind=link}

Here's a key point: If we take out the technology sector from the stock market, the rest of the market would be trading below the average over the last 25 years.

Now, the not-so-good news is that interest rates have gone up a lot since the Covid lows, about 1700% higher. This makes it tougher for many companies to borrow money for growth.

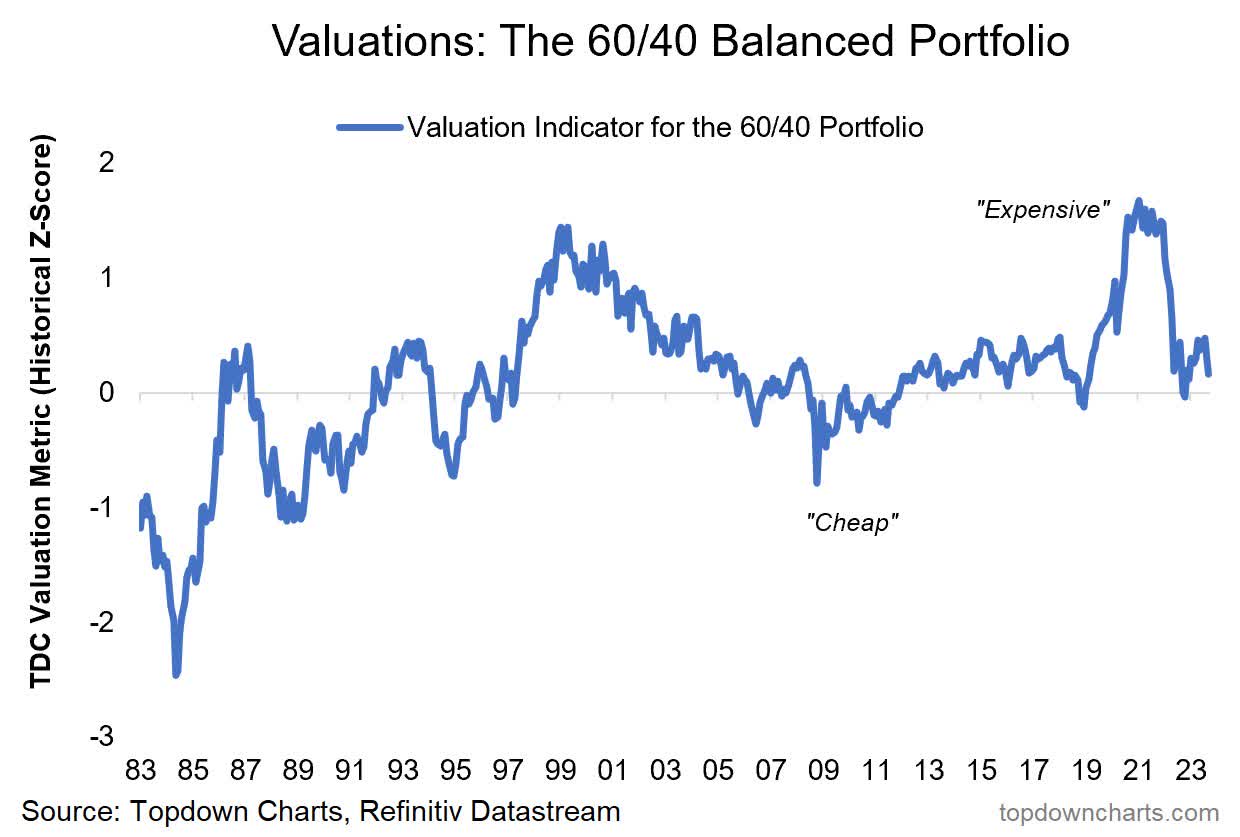

More good news is the classic 60/40 balanced portfolio is also near 25-year median valuations after trading into bubble territory in 2021.

The 60/40 - Valuation Composite

Another angle on it, using my valuation indicators at Topdown Charts for stocks and bonds - both were showing up as extremely expensive toward the end of 2021 (and a good clue as to the joint carnage both suffered in 2022). Since then, similarly, we have seen a significant adjustment, but the portfolio level valuation indicator remains slightly expensive.

{kind=link}

Great Ideas Versus Making Money

The stock market is a never ending battle of story telling versus profits, lost in that game is a lot of great ideas that secure financing during loose monetary conditions but then struggle to profit. This phenomenon has become more pronounced with the recent increase in interest rates.

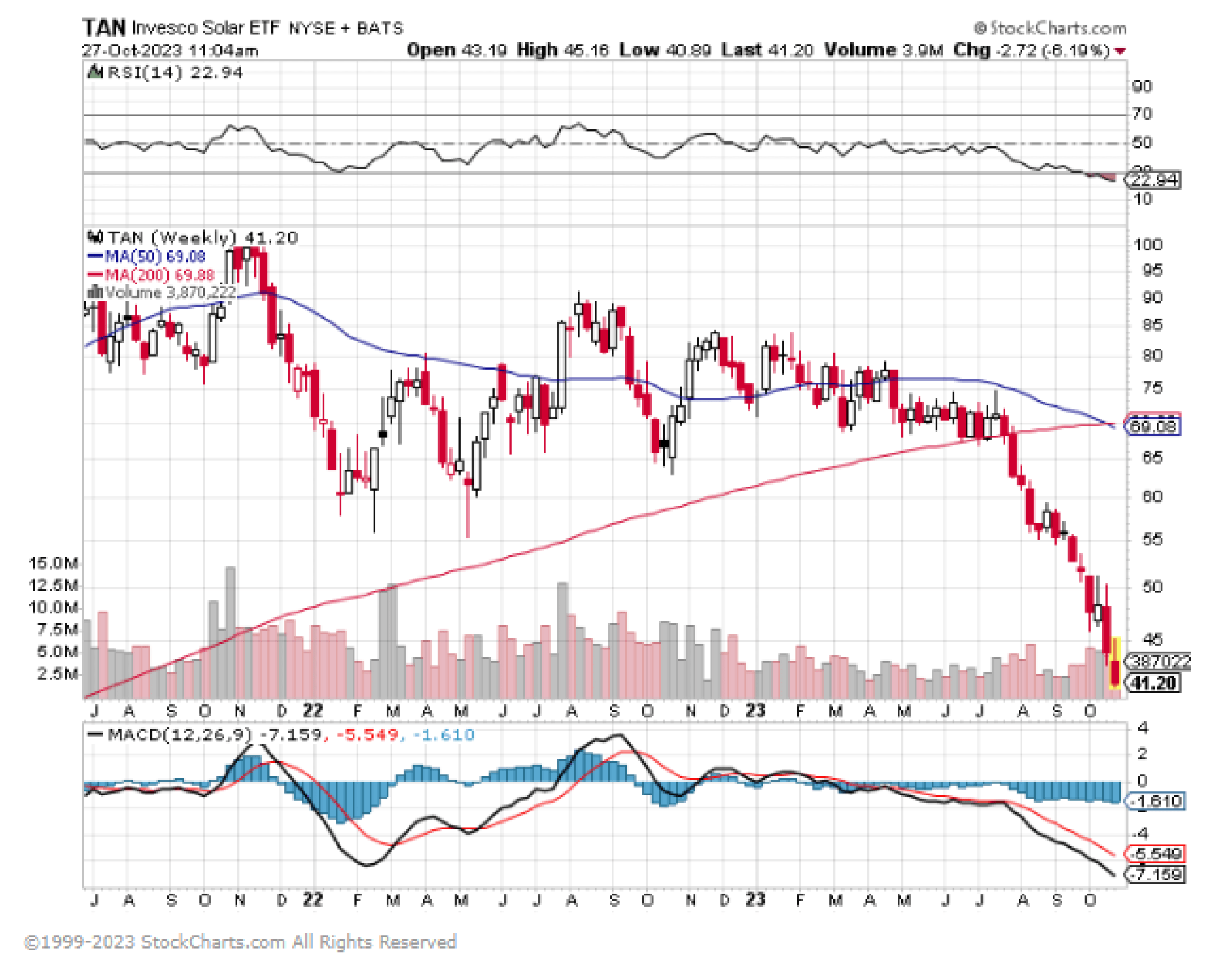

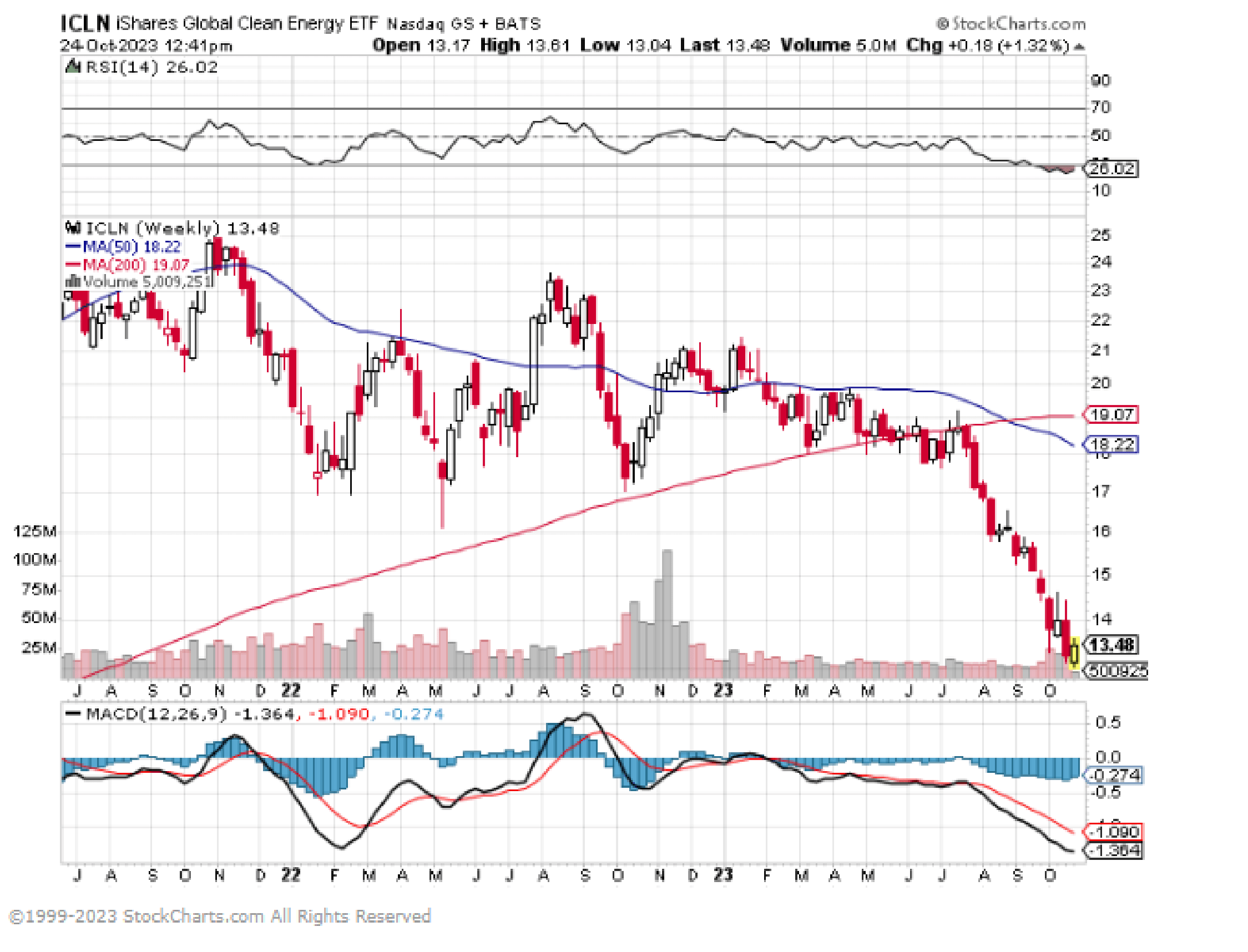

I'm not singling out alternative energy, but it's worth noting that, like all energy investments, it has experienced significant volatility. Take a look at the charts for ETFs representing the alternative energy sector: TAN (solar), LIT (lithium), and ICLN (clean energy). Each of them has seen substantial drawdowns of around -50% from their respective highs. This serves as a reminder of the unpredictable nature of the market and the importance of diligent risk management.

TAN Solar Stock ETF Hit $300 at one point leaving it -85% since inception.

{kind=link}

LIT Lithium ETF -30% in One-Year but still positive since inception. Lithium is key component to EV cars and batteries.

{kind=link}

ICLN Clean Energy ETF -60% from Highs

{kind=link}

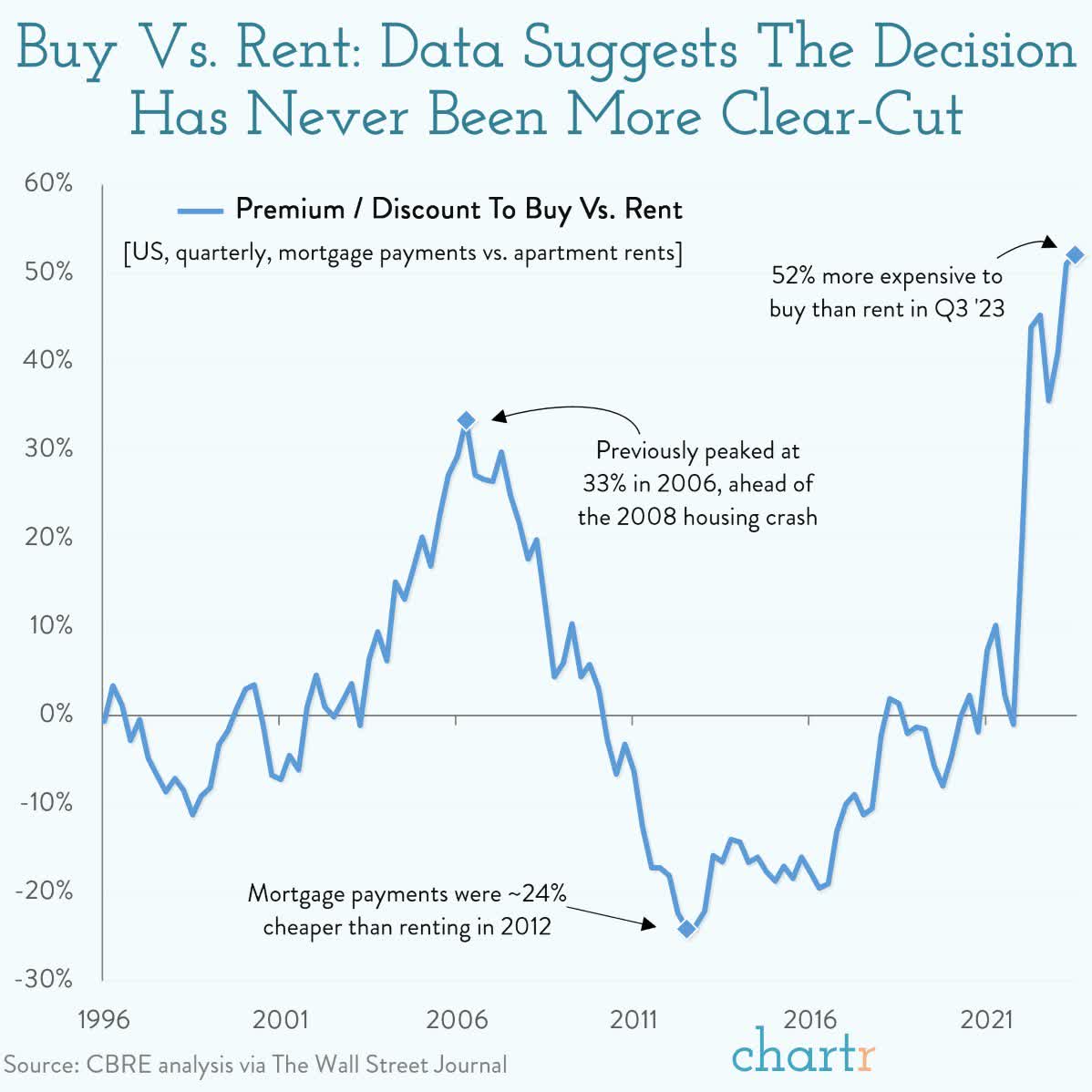

Real Estate

One commentregarding the real estate market, an important observation to make is that the buy-versus-rent equation is currently at its most expensive point ever, surpassing even the levels seen in 2008. This situation has arisen due to insufficient housing construction following the Global Financial Crisis. Adding to the complexity is the unprecedented increase in interest rates, with homeowners opting to stay in place, holding onto mortgages with rates below 4%

{kind=link}

Conclusion

Since the inception of Lansing Street Advisors, we've navigated through a series of significant market events, including the Covid crash and rebound, the 2022 dual stock and bond crash, the year of the Seven, and the potential for a record three years of negative bond returns. While these events have certainly added stress, they've also provided ample material for discussion.

Despite the most talked-about recession in history being postponed yet again with a 4.9% GDP number in Q3 2023, the inverted yield curve-a historically reliable recession predictor-still looms, so I don't expect market events to get more benign.

Turning to the Seven, it's becoming increasingly challenging for the U.S. government to pursue these tech giants as monopolies due to widespread public ownership. These stocks are responsible for driving S&P returns in many 401k plans and are among the most widely held individual stock names by middle-class citizens who vote. While tech regulation has made headlines, full antitrust actions may not be a popular political card to play.

Now, let's talk bonds. While bonds aren't necessarily my specialty, they're becoming an increasingly intriguing asset class. At some point, we might witness a shift of Warren Buffet's old adage, "stocks are the only thing people don't buy when they are on sale." Currently, bonds find themselves at a 25year low in terms of valuations, coupled with historically low sentiment levels. This juxtaposition may lead to a novel scenario where "bonds are the only thing that people don't buy when they are on sale." Keep an eye on high-yield bonds-they could offer enticing 10% coupons in the near future.

Seven - Song by Dave Matthews Band

Mama told me boy someday a STOCK will take your mind

And then you'll know

I never knew but I do now

I never knew but I do now

Let me go let me go Let me go down

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Lansing Street Advisors Q3 2023 Letter