CA - Latest Developments Impact The Bull Case For Frontera But It Remains A Buy

2023-06-08 15:58:56 ET

Summary

- Frontera Energy's share price has declined sharply, but the company remains undervalued with significant upside potential.

- The company's operations in Colombia and offshore Guyana hold considerable exploration opportunities and growth catalysts.

- Despite increased risks and financial pressures, Frontera is on sale, selling at a deep discount to its after-tax 2P NAV per share.

Oil companies operating in Colombia remain deeply undervalued as heightened geopolitical risk weighs heavily on their market valuation. One such company is intermediate oil producer Frontera Energy ( FECCF )( FEC:CA ) which is Colombia’s third largest petroleum producer. Since I last wrote on Frontera on April 17, 2023 the driller has lost 18%, a worrying development which along with recent events brings that analysis into question. Among the key developments are softer oil prices, somewhat disappointing first quarter 2023 results and potentially negative operational events. Over the last month alone Frontera has remained flat compared to Brent, as represented by the United States Brent Oil Fund ( BNO ), which is up by nearly 2%.

Frontera Share Price Chart (Yahoo Finance)

{kind=link}

The sharp decline of Frontera’s share price coupled with speculation the company is up for sale, with Citibank reportedly chosen as a strategic adviser, makes now the time to review Frontera to determine its outlook. This is especially important because in my earlier April 2023 article I concluded that Frontera was heavily undervalued having calculated that the driller has an after-tax 2P NAV of $26.15 per share or three-times the current market value, at the time of writing. Let’s take a closer look at recent events and financial results to determine whether Frontera remains undervalued and is a worthwhile investment.

Financial update

After announcing strong 2022 results, Frontera, like many of its peers operating in Colombia notably Gran Tierra Energy ( GTE )( GTE:CA ) reported disappointing numbers for the first quarter 2023. The most startling being the company’s bottom-line which showed a $11.3 million loss compared to a $102 million profit for the same period a year earlier. Operating EBITDA also fell sharply dropping to $91.9 million from $133 million for the same period in 2022.

The key reasons for this sharply decline in profitability are:

- a 17% year-over-year decline in oil sales revenue to $189.4 million due to a 16% decrease, $82.10 against $97.90 in the average Brent price for the quarter compared to a year earlier.

- weaker Brent price coupled with higher price differentials for Colombia’s Vasconia and Castilla oil blends caused Frontera’s realized price per barrel sold to fall to $64.55 as opposed to $81.36 for the first quarter 2022;

- there was a sharp increase in transportation cost which for the first quarter 2023 totaled $37.4 million a 16.5% increase over the same period a year earlier;

- depletion, depreciation and amortization expense shot up by 72% year over year to $66.7 million due to a fourth quarter 2022 impairment reversal and the acquisition of a 35% working interest in the El Dificil Block in the Lower Magdalena Valley Basin; and

- impairment expenses surged to $30.3 million for the first quarter 2023 compared to a $4 million gain a year earlier because of Frontera’s decision to the VIM-22 Block in the Lower Middle Magdalena Valley Basin.

While those bottom-line results disappointed the market there was plenty of good news in Frontera’s first quarter 2023 earnings, the key positive developments being:

- gross, before royalties, production expanded by 1.8% year over year to an average of 41,586 barrels per day giving net sales volumes a healthy boost; and

- production costs fell by 8.5% year over year to $45.2 million or $12.07 per barrel.

Frontera’s balance sheet has also weakened over the last year. At the end of the first quarter 2023 the driller had cash and cash equivalents of $162.3 million compared to $257.4 million a year earlier, although accounts receivable had increased by 11% year over year to $175 million. The decrease in cash was further offset by a 7% increase in inventories to $91.5 million. Frontera’s long-term debt of $501.5 million was 24% greater than the $403.4 million at the end of the first quarter 2022.

The company’s first material debt maturity is $370 million for the Puerto Bahia debt in June 2025. That is only two years meaning that by halfway through 2024 it will move from noncurrent debt to current debt placing greater short-term pressure on Frontera’s finances, although it is important to note it is non-recourse debt secured against the highly profitable Puerto Bahia port facility in Cartagena Colombia. This means there is every likelihood Frontera will be able to renew the existing credit facility or secure a new one on favorable terms.

Frontera’s financial position has weakened primarily due to an increase in capital expenditures for 2023 with Frontera budgeting $400 million to $475 million for the year compared to spending of $417.5 million during 2022. Nevertheless, overall Frontera possesses a solid balance sheet but with some short-term financial pressures ahead, particularly with weaker oil prices and significant capital expenditure of $400 million to $475 million weighing on free cash flow during 2023.

Operational update

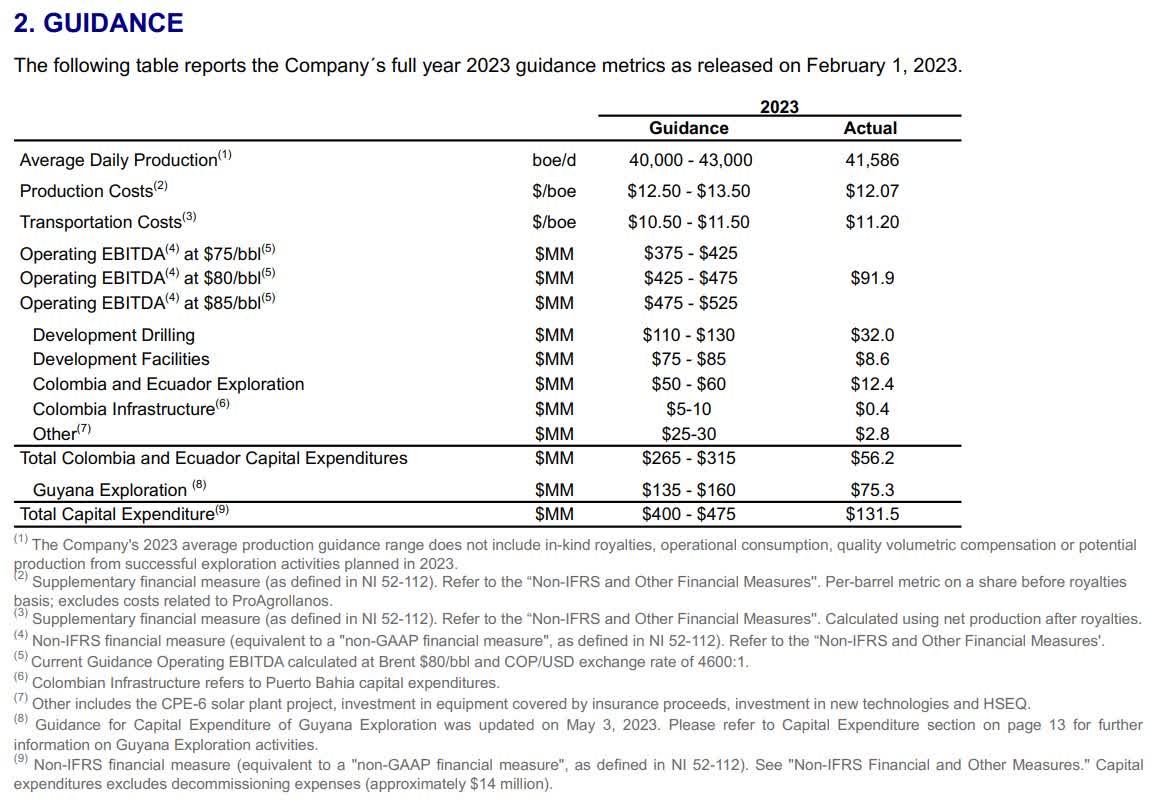

For the first quarter 2023 Frontera reported some solid operational numbers, key being a 1.8% year over year increase in production to an average of 41,586 barrels per day. That number would have been higher if the Quifa and CPE-6 blocks had not been shut-in by temporary roadblocks in Puerto Gaitan during early February 2023. That oil output was still within the budgeted annual target of 40,000 to 43,000 barrels per day, despite the roadblocks, as per the table below.

Frontera 2023 Guidance (Frontera Energy)

{kind=link}

Source: Frontera Management Discussion and Analysis March 31, 2023.

This bodes well for Frontera to achieve its planned annual petroleum output, particularly when it is considered that production will continue rising with the roadblocks lifted and various well development activities completed. First quarter 2023 production costs fell by an impressive 9.5% year over year to $12.07 per barrel while transportation costs of $11.20 a barrel were 15% higher but within the annual budget.

The key risk for Frontera’s 2023 budget is the subdued outlook for oil with recessionary fears and weak economic data, notably from China, continuing to weigh on prices. For the year-to-date Brent has averaged around $80 per barrel with the international benchmark trading at $76 a barrel at the time writing, which is significantly lower than the budgeted base case of $80 per barrel. This coupled with the U.S. EIA in its May 2023 Short-Term Energy Outlook downgrading the annual average forecast Brent price to $78.65 per barrel, indicates Frontera will struggle to achieve its base-case 2023 budget. Nevertheless, with Brent averaging $75 per barrel for the year Frontera will generate operating EBITDA of $375 million to $425 mill for 2023 which accords with operating EBITDA of $91.9 million earned for the first quarter. That, however, will impact free cash flow and could force the company to take on additional debt or revise its 2023 capex lower.

Guyana update

One of the key growth catalysts for Frontera is its 68% working interest in the Corentyne Block offshore Guyana with the remaining 32% held by CGX Energy, which is 77% owned by Frontera, giving the company a 93% consolidated interest in the block. CGX announced that the Wei-1 well despite various problems and delays will be completed on schedule. The company also hinted in its early May 2023 update that oil had potentially been found stating that Wei :

“ encountered multiple oil-bearing intervals in the western channel fan complex of the northern portion of the Corentyne block in formations of Maastrichtian and Campanian ages. A comprehensive logging campaign in the Maastrichtian interval indicated the presence of medium sweet crude oil of 24.9 API. Downhole fluid analysis confirmed light sweet crude oil in the Campanian interval. Logging while drilling (LWD) and cuttings indicated the presence of hydrocarbons in the upper portion of the Santonian; ”

While it has yet to be confirmed whether the oil discovered with Kawa and Wei well is commercially viable to exploit, this is a positive development for Frontera. Despite this good news and the considerable potential held by the Corentyne Block in offshore Guyana, which analysts are calling the world’s most exciting frontier offshore oil play, Frontera’s stock has failed to pop.

Colombia midstream

Frontera’s Colombian midstream assets, comprised of the Puerto Bahia terminal in the Bay of Cartagena and the 300,000 barrel per day ODL pipeline, are a cash generating machine for the company. First quarter 2023 midstream segment income shot up by a notable 48% year over year to $16.9 million. This can be attributed to solid revenue spikes from Puerto Bahia, which rose 44% year over year to $3.4 million and the ODL pipeline where revenue surged 49% year over year to $13.6 million.

The ongoing rationalization of operations at Puerto Bahia as well as expansion of the port facilities along with securing new permits and licenses coupled with growing demand for the liquid cargo terminal will drive higher utilization and hence revenue. Frontera’s increased ownership interest in the ODL pipeline and rising transportation volumes will also drive higher midstream income.

Corporate restructuring

This development explains the recent restructuring of the intermediate oil producer which was effectively bundled into three separately contained sellable entities. These are comprised of Frontera’s:

- onshore upstream oil exploration and production operations in Colombia and Ecuador;

- the standalone Colombian midstream business; and

- offshore exploration operation in Guyana.

Since mid-April 2023 there has been considerable speculation that Frontera is seeking to sell assets or the entire business . Reputedly the driller has asked Citibank to explore the option of a partial or total sale , but no offers have reportedly been forthcoming. Frontera is 41% owned by Toronto based Catalyst Capital which in 2016 provided a $500 million debtor in possession loan to the company, then known as Pacific Exploration or Pacific Rubiales, which had filed for bankruptcy protection.

Apparently, Catalyst has been seeking a sale for some time, since at least early 2022, as it seeks to generate a sizable return on its initial investment. There is considerable difficulty associated with selling Frontera because of recent geopolitical and regulatory developments in Colombia, where the company’s core assets are located. This essentially relates to the significant uncertainty surrounding Colombia’s energy patch sparked by Leftwing President Gustavo Petro’s plan to end contracting for oil exploration and ban hydraulic fracturing coupled with recent oil industry tax hikes.

Colombia, since Petro’s July 2022 electoral victory, has fallen into disfavor with international energy investors and is even seeing companies like Exxon Mobil ( XOM ) exit the country and seek compensation from the national government. Higher taxes on oil producers coupled with fears that the industry does not have a long-term future in Colombia have seen a sharp reduction in investment in the country’s oil patch. According to industry body the Colombian Petroleum Association has seen private investment in exploration activities in Colombia fall by 33% for 2023 compared to a year earlier. These factors are also weighing on Frontera’s market valuation and that impact is magnified by attempts to sell the company in such a difficult geopolitical environment.

Key company specific risks

There are a number of risks specific to Frontera and its operations in Colombia that investors must consider before investing. I have discussed the geopolitical risks associated with Colombia and the country’s leftwing president Gustavo Petro’s plans to end awarding contracts for hydrocarbon exploration at length in my earlier article. That also included the impact of the November 2022 oil industry tax hikes which saw the effective tax rate for exploration and production companies operating in Colombia rise from 36% to around 50%. Nonetheless, there is an additional company specific financial risk that emerged from Frontera’s first quarter 2023 financial statements.

That concern is the sharp increase in Frontera’s non-current debt. By the end of the first quarter 2023, Frontera’s long term financial obligations totaled $685 million, a 29% increase compared to the previous quarter. There is the likelihood that long-term debt will increase once by the end of 2023. You see, total current liabilities at the end of the period totaling $514 million exceed Frontera's cash on hand plus inventory and receivables totaling $492.5 million.

Frontera has also allocated $400 to $475 million to be invested in annual capital expenditures for the year to fund exploration and development drilling program as well as infrastructure improvements. This means after accounting for capex at the top end there is a considerable shortfall of $497.5 million which is well in excess of projected 2023 free cash flow of $75 million at the top end of guidance based on Brent averaging $80 per barrel for the year. Those numbers indicate that Frontera could be forced to take on additional debt to fund current operations, the amount required may be even greater if Brent averages less than $80 per barrel which is a possibility at this time. That is one of the main reasons Frontera’s stock price is under pressure despite the company trading at a deep discount to its after-tax net asset value per share.

Finding Frontera’s fair value

Using the first 2023 numbers I have recalculated Frontera’s after-tax NAV for its 1P and 2P reserves using the same methodology as my earlier articles. This methodology takes Frontera’s after-tax NPV-10 for its proven (1P) and proven plus probable (2P) oil reserves and then deducts net-debt which is then divided by the shares outstanding to find the 1P and 2P NAV per share.

To do this I have made the following adjustments based on the latest numbers:

- Frontera’s 2022 after-tax 1P NPV-10 of $1.66 billion and after-tax 2P NPV-10 of $2.2 billion remains unchanged;

- Long-term debt is $501.5 million as per the company’s First Quarter 2023 Financial Statements;

- Cash is $162.3 million as the driller’s First Quarter 2023 Financial Statements;

- Outstanding diluted share count of 88.5 million as of May 2, 2023.

Using Frontera's 2022 1P after-tax NPV-10 of $1.66 billion, which includes a 10% discount as per accepted industry methodology, and accounting for the numbers listed above I calculated that the driller has an indicative fair-value of $14.92 per share as shown below.

After-tax 1P NAV Calculation (Author's own work)

Source: Frontera Statement of Reserves Data December 31, 2022, Interim Condensed Financial Statements March 31, 2023, Corporate Presentation March 2023 and Author’s own work.

That number, while 14% lower than the earlier 1P NAV of $17.34, it is still 1.8 times greater than Frontera’s market value at the time of writing. This indicates that there is considerable upside available with a solid margin of safety, especially when it is considered that is the after-tax NAV of Frontera’s 1P reserves.

Frontera's indicative value per share rises even higher when calculating the after-tax 2P NAV and accounting for the numbers listed above. The driller’s after-tax 2P NAV comes to $21.57 per share as the chart below shows.

After-tax 2P NAV Calculation (Author's own work)

Source: Frontera Statement of Reserves Data December 31, 2022, Interim Condensed Financial Statements March 31, 2023, Corporate Presentation March 2023 and Author’s own work.

While this is significantly lower, nearly 18% less, than the $26.15 per share calculated in my earlier April 2023 article on Frontera it is still 2.6 times greater than Frontera’s share price at the time of writing. When it is considered that the after-tax 2P NAV of an upstream oil producer is the accepted industry standard valuation methodology this indicates that Frontera is heavily undervalued by the market with considerable upside and a wide margin of safety available.

Final thoughts

Frontera remains a high-risk investment which has the potential to deliver outsized returns to investors, particularly with the intermediate oil producer trading at nearly a third of its 2P NAV of $21.57 per share. The company is beset on all sides by risks and the impact is being magnified by the April 2023 announcement that Frontera in its entirety or in parts is up for sale. These developments are sharply impacting the driller’s market value. Nonetheless, the perceived degree of risk is heavily overblown in my view.

Frontera holds a transformational opportunity in offshore Guyana where recent drilling results appear positive. The company operates quality producing oil acreage in Colombia, which possesses considerable exploration upside, that Petro has confirmed will not be impacted by plans to end hydrocarbon exploration. For these reasons, despite the subdued outlook for oil, growing onshore production in Colombia and Ecuador coupled with the considerable potential for a major discovery in offshore Guyana points to Frontera being heavily undervalued.

NB: Frontera is a U.S. pink sheets stock with its primary listing on the TSX where it has an average daily trading volume of 80,357 shares.

For further details see:

Latest Developments Impact The Bull Case For Frontera, But It Remains A Buy