CA - Let The REIT Rally Begin!

2023-06-15 07:30:00 ET

Summary

- Real estate investment trusts have experienced a significant decline in the past year.

- Despite these challenges, REIT prices may begin to rally as the market anticipates a recovery in the future.

- We highlight two REITs offering significant upside potential.

Co-produced by Austin Rogers.

Real estate investment trusts ("REITs") have been absolutely pummeled over the past year or so as investors sold out in anticipation of a deep hit to cash flows from:

- Higher interest rates, which will cause interest payments to soar

- Higher vacancy rates due to a weakening economy and remote work

- Declining net asset values ("NAVs") as property owners mark-to-market falling property prices on their balance sheets

Hence we find the wide discrepancy in performance between REITs ( VNQ ) and the SPDR® S&P 500 Trust ETF ( SPY ) over the past year:

But we will let you in on a little-known fact that we have learned from many years of paying close attention to both public and private real estate.

Publicly traded real estate stocks / REITs, like all other stocks, are forward-looking . Investors are always trying to price in what is going to happen to real estate in the future -- specifically, the foreseeable or near future.

Meanwhile, actual property prices rise or fall based on a number of factors, such as the amount of capital still available to be deployed, cost of new capital, the prices sellers are willing to accept, and so on. Because of these factors, property prices tend to lag way behind "real-time" data like interest rates, while REIT prices significantly front-run the "real-time" data.

But everything in the market moves in cycles, including commercial real estate. This means that, at some point, REIT prices will turn back up and begin to rally even as actual property prices continue to trend down.

Why? Because for REITs, the market is trying to price in what is coming in the future, not the prevailing situation today.

And yet, the REIT index has dropped ~30% since its peak at the very end of 2021.

REITs turned down and began trending lower around 6 months before CRE property prices began to fall.

What are some reasons why REIT prices could begin to rally even while the fundamentals are still under stress?

- The market widely anticipates the Fed to pause rate hikes soon and for this pause to be the end of the current rate-hiking cycle.

- Homebuying unaffordability due to high home prices and mortgage rates will keep many would-be homeowners in the rental market, benefiting residential REITs.

- The market is beginning to grasp REITs' resilience in the face of higher interest rates, given their stronger balance sheets than prior to the Great Financial Crisis.

- Office REITs, which have borne the brunt of the pain from deteriorating fundamentals and high debt, have already sold off heavily.

Hence we now find ourselves at or near the shift in trends, from REITs becoming more and more discounted to NAV to REIT valuations normalizing as property prices come down and REIT prices come up.

{kind=link}

On average, REITs are about as discounted to NAV today as they were at the depths of the COVID-19 selloff, although they are not quite as discounted as they became in 2008-2009.

Note that in 2008-2009, the REIT index lost around 2/3rds of its value (~66%), and yet the Green Street CPPI shows that CRE property values only fell about 18% from their 2007 peak to their 2009 low!

Likewise, in 2020, REITs shed about 35% of their value, while the Green Street CPPI fell only about 13%.

Perhaps because REIT stocks are more heavily trafficked by retail investors than the largely even-keeled institutional investors that are heavy in other stock sectors, REIT prices tend to overreact both on the upside and the downside.

That creates fantastic opportunities for investors who are willing to swim against the tide

Where are the best opportunities in the world of REITs?

That question could be answered in lots of different ways. One way to answer is to look at which real estate sectors have become most undervalued relative to the private market valuation of their respective property types.

CenterSquare

As you can see, the five sectors of real estate that trade at the biggest discounts to the private market valuation of their properties are:

- Office: 22.2% discount

- Life Science: 17.4% discount

- Single-Family Rentals: 15.1% discount

- Apartments: 14.4% discount

- Hotels: 12.7% discount.

We remain cautious about office real estate. While we're aware of the ostensibly attractive discounts to NAV, it is difficult to predict the degree of damage to be caused by heavy leverage, upcoming debt maturities, corporate layoffs, and the future of hybrid work.

Meanwhile, we dislike the hotel REIT business model generally, because hotel REITs are highly exposed to the cyclicality of the hospitality industry. Margins are low, as operating expenses are high. Besides, we think we are near the near-term peak in travel and leisure spending for the current cycle, and we don't want to buy at the top.

That said, outside of these two sectors, we see many fantastic discounts in REITdom. Below, we discuss two of them.

Life Science: Alexandria Real Estate Equities, Inc. ( ARE )

We have praised ARE for its strengths numerous times in the last year or so. And there are many of them:

- Fortress balance sheet: BBB+ credit rating, well-laddered debt maturities with none due until 2025, a weighted average remaining debt term of 13.4 years, 96% fixed-rate debt, and total liquidity over $5 billion

- Trophy properties: Class A life science buildings located in the nation's top research & development clusters

- Skilled & shareholder-aligned management: Led by company co-founder Joel Marcus

- Attractive lease terms: Triple-net leases with little to no landlord responsibilities, annual rent escalations of 3%, long lease terms averaging 7.2 years, and strong biotech tenants

This strategy has produced phenomenal results, including the highest quarterly rent growth in company history in the first quarter of this year (including future rent increases).

{kind=link}

And yet, ARE's stock price has performed worse than the average REIT and significantly worse than the SPY since the beginning of 2022.

What is going on?

We think ARE is the victim of a few serious misconceptions.

First, it is often misclassified as an "office REIT," even though its state-of-the-art laboratory / R&D buildings are used very differently by their tenants than traditional office space. Most lab work cannot be done remotely.

Second, many people think that a huge wave of new life science supply is going to come to market soon to compete with ARE's properties. It is often thought that half-empty traditional office buildings are going to be converted into life science space and that developers are continuing to build more life science buildings.

The fear, in short, is that there will soon be an oversupply of life science real estate.

While this will act as somewhat of a headwind, we think the market has overreacted to this fear of oversupply. This is primarily because ARE's high-quality building designs and unbeatable locations cannot easily be replicated.

Here's how CEO Peter Moglia responded on the Q1 conference call to a question about new supply coming online in some of ARE's markets:

Certainly, there are -- there have been -- there has been spec building, especially in Boston. What we are seeing is in areas outside of our core submarkets where we don't own product, there are vacant buildings sitting there. And it's -- we're hearing that there's no tours, there's no activity. So, we don't necessarily think that those buildings are competitive to ours.

... So obviously, '23, a lot of stuff has already been delivered. There's some more coming in '24, there's more coming. We are seeing very little that is starting new today.

... we don't think many, if any, people will start new projects from here on out, at least not in a material manner, but who knows?

These misconceptions have rendered ARE far cheaper than it deserves to be -- and far cheaper than its historically average valuation.

For example, compared to its 5-year average price-to-AFFO (adjusted funds from operations) of 25.5x, ARE currently trades at an AFFO multiple of only 16.7x.

And compared to a 10-year average price-to-operating cash flow (or "cash from operations") of 22.1x, ARE currently trades at a CFO multiple of only 13.9x.

Lastly, compared to a 5-year average dividend yield of 2.7%, ARE's recently raised dividend currently yield 4.2%, the highest level of any time in the last decade.

ARE is one of our highest conviction "buys" today. We expect 50%+ upside as its valuation recovers and believe that the stock is set to produce double-digit total returns from its yield and growth alone.

Single-Family Rentals: Tricon Residential Inc. ( TCN )

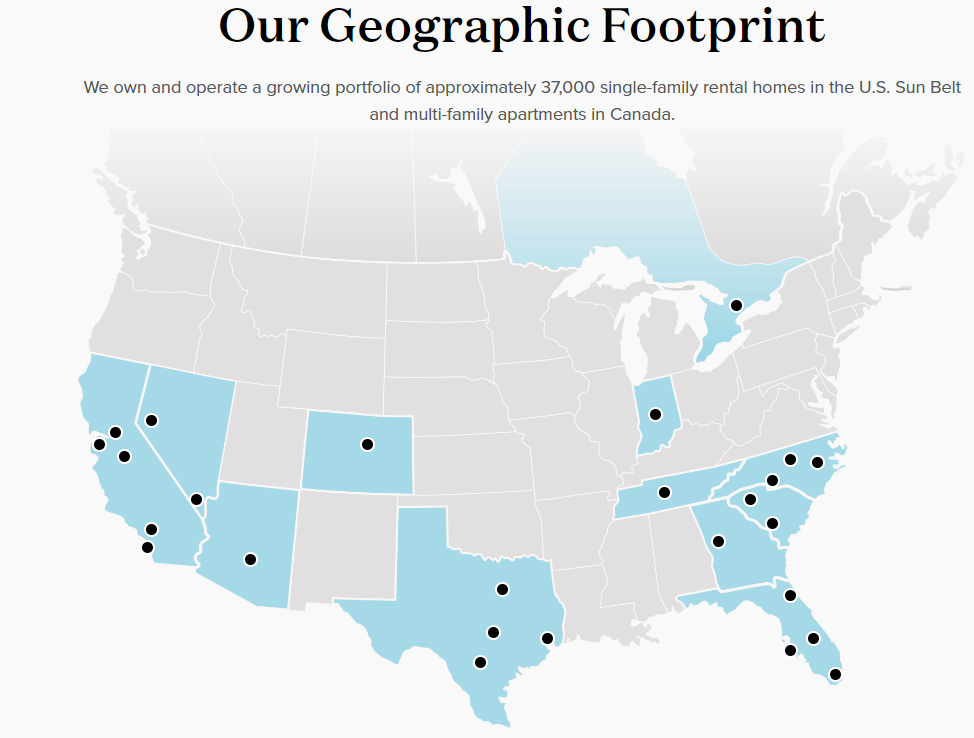

TCN is a residential REIT that owns over 36,000 single-family homes and almost 5,000 multifamily units concentrated overwhelmingly in Sunbelt states like Georgia, Florida, Texas, and the Carolinas.

{kind=link}

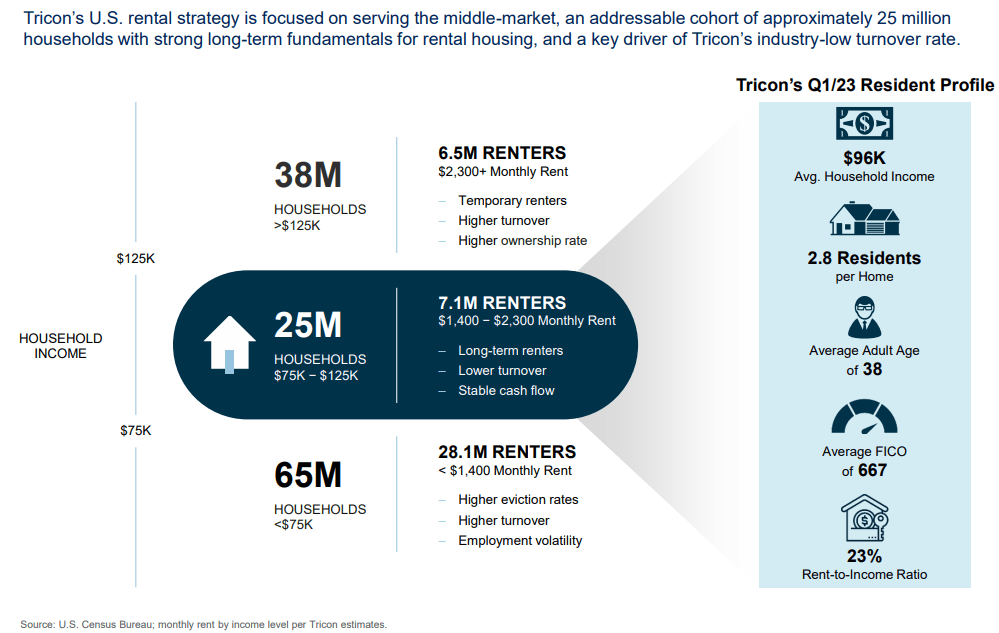

Contrary to the depiction often found in the media of major landlords like TCN buying up the lowest end of single-family homes and hiking rents on hapless, low-income individuals, TCN targets the "middle" of the SFR market.

{kind=link}

These are renters with incomes between $75K and $125K and high credit scores, typically in their 30s or 40s, who want to live in single-family homes but cannot afford to buy one. TCN estimates that there are around 25 million of these households in the U.S.

Another aspect of TCN that is interesting to us is its burgeoning and highly scalable asset management business through joint venture partnerships with institutional investors who want access to the hot SFR real estate sector.

In the past ten years, TCN has proven to be one of the fastest growing players in this space. From 2012 through Q1 of 2023, TCN grew its portfolio of homes at a compound annual growth rate of 36%.

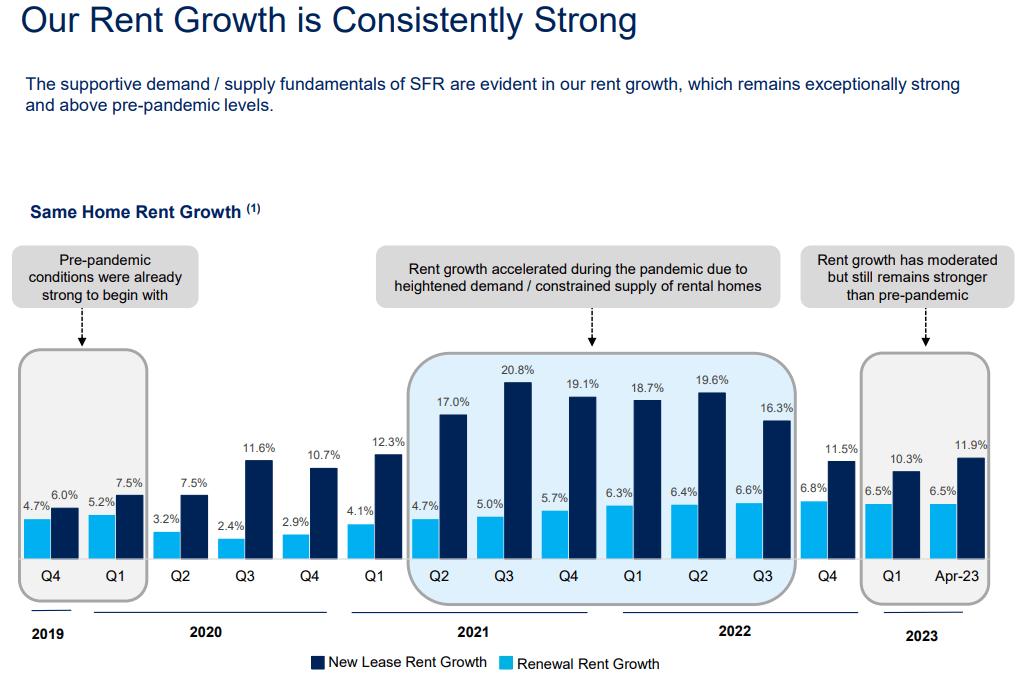

On top of that external growth, TCN also boasts a strong history of organic growth in the form of rising rents.

{kind=link}

The biggest problem the market sees with TCN is its balance sheet . The REIT does carry a fairly large debt load (although its loan-to-value ratio is actually lower than what an equivalent private residential landlord's would be).

The good news is that TCN has demonstrated an ability to deleverage fairly quickly. For example, in Q1 2020, net debt to asset value stood at 60%, and in Q1 2023 that had dropped to 36%. In Q1 2020, net debt to EBITDA was 15.3x, and by Q1 2023 that had dropped to 8.2x.

{kind=link}

But the market appears to have overlooked this significant deleveraging as the company continues to trade at a roughly 40% discount to its NAV and a 7% FFO yield, which is an exceptionally low valuation for such defensive and desirable assets.

Even using a more conservative estimate of the NAV, we think that the stock has at least 30% upside to its fair value.

Bottom Line

There are many more examples of REITs trading at big discounts to their NAVs. We discuss these two simply as examples of how REITs are heavily discounted right now.

While the fundamentals may continue to cool in terms of property prices and rent growth rates, we think REIT stock prices will continue to be forward-looking by pricing in the eventual recovery well in advance of it.

We are not market-timers and cannot time either the top or bottom of the market, but we recognize when there are good deals in the market. And right now, heavily discounted opportunities are abundant in the realm of REITs!

For further details see:

Let The REIT Rally Begin!