XOM - LGI: Global Diversification And Fully-Covered Distribution But Performance Might Disappoint

2023-10-17 10:17:19 ET

Summary

- Lazard Global Total Return and Income Fund offers a current yield of 8.26%, indicating that the market expects that the fund can sustain this payout.

- The fund has underperformed the S&P 500 Index and MSCI World Index, resulting in a 4.76% total loss for investors since May.

- The fund's allocation to cyclical sectors and exposure to technology stocks may pose risks in a potential economic slowdown.

- The fund did fully cover its distributions in the first half of this year, but it had to rely on unrealized gains to do it.

- The fund is currently trading at an attractive valuation.

Lazard Global Total Return and Income Fund Inc ( LGI ) is a closed-end fund that is specifically designed for investors who are seeking to earn a high level of income from the assets in their portfolios. The fact that the fund has a current yield of 8.26% stands as proof of this. With that said, this yield is quite a bit lower than the yields that can be obtained from most junk bond or floating-rate closed-end funds right now. This is not necessarily a problem, as the current yield is a clear indication that the market expects that this fund will have no difficulty maintaining its payout going forward. This is in direct contrast to some other high-yielding closed-end funds that have fears of a near-term distribution cut surrounding them. In addition, the current yield does represent a positive real yield and it is still far higher than most other things in the market.

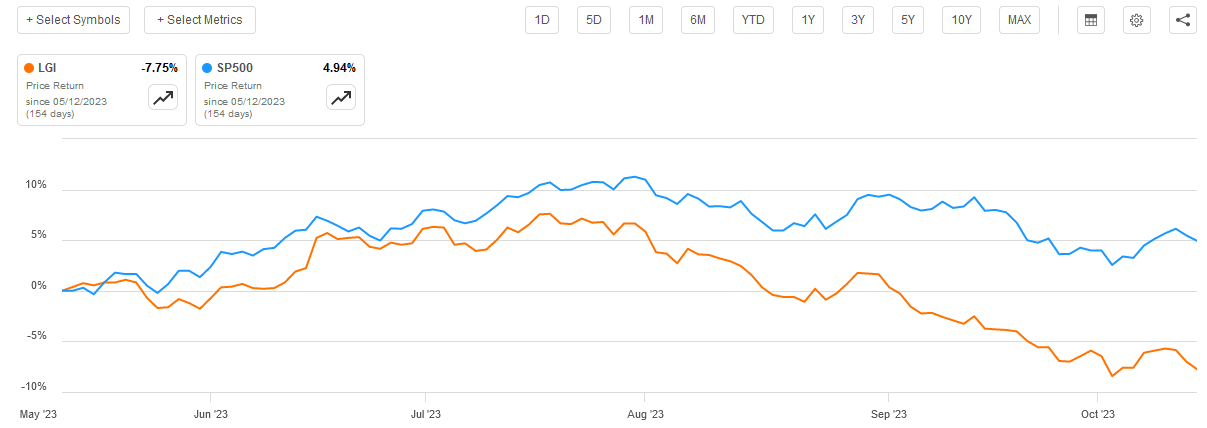

As regular readers may recall, we last discussed the Lazard Global Total Return and Income Fund back in May of this year. Obviously, the market has changed significantly since that time, as investors have woken up to the fact that high interest rates are likely to be with us for a very long time. As such, there has been a switch from long-duration to short-duration assets, which has pushed down the price of long-dated bonds and most growth stocks in favor of things that produce cash right now. This is evident in the fact that the S&P 500 Index ( SP500 ) is down since mid-July while things like the U.S. Energy Index ( IYE ) are up over the same period. Unfortunately, this has generally had a negative effect on this fund. As we can see here, the fund is down 7.75% since we last discussed it. This is a worse performance than the S&P 500 Index:

{kind=link}

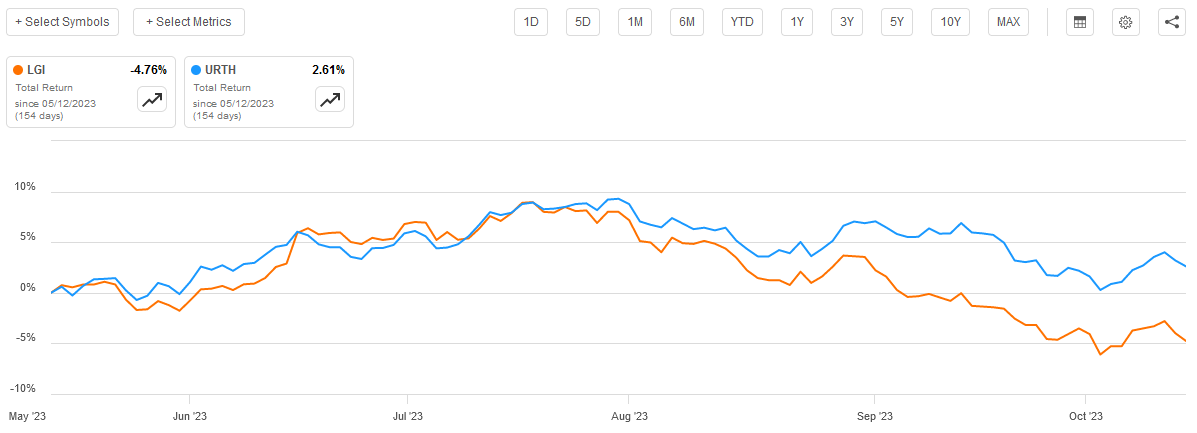

This fund does do a bit better when we consider the distributions that investors would have received from this fund over the period. After all, the distributions would have offset some of the decline in the fund’s share price. However, investors still suffered a 4.76% total loss over the period. This is a disappointing performance, particularly considering that this is an equity fund. After all, the MSCI World Index ( AGG ) is actually up by 2.61% over the same period:

{kind=link}

The question that is undoubtedly on everybody’s mind right now though is whether or not it still makes sense to purchase this fund today. Let us investigate and try to figure that out.

About The Fund

According to the fund’s website , the Lazard Global Total Return and Income Fund has the primary objective of providing its investors with a high level of total return. This certainly fits with the fund’s name pretty well, and it fits pretty well with the fund’s strategy. From the webpage:

Lazard Global Total Return & Income Fund is a closed-end investment management company that seeks total return consisting of capital appreciation and current income. The Fund seeks to achieve its objective by investing in a portfolio by investing in a portfolio of 60-80 US and non-US equity securities, generally with a market cap of $2 billion or greater, at the time of purchase, and may invest in emerging markets. It seeks enhanced income by investing in short duration (typically below one year) emerging market forward currency contracts and other emerging market debt instruments.

As such, we can see that this is a global equity fund. However, the fund’s portfolio is actually more mixed than might be expected from a fund like this. It currently has 87.12% of its assets invested in stocks, but it also has a fairly sizable allocation to both bonds and cash:

CEF Connect

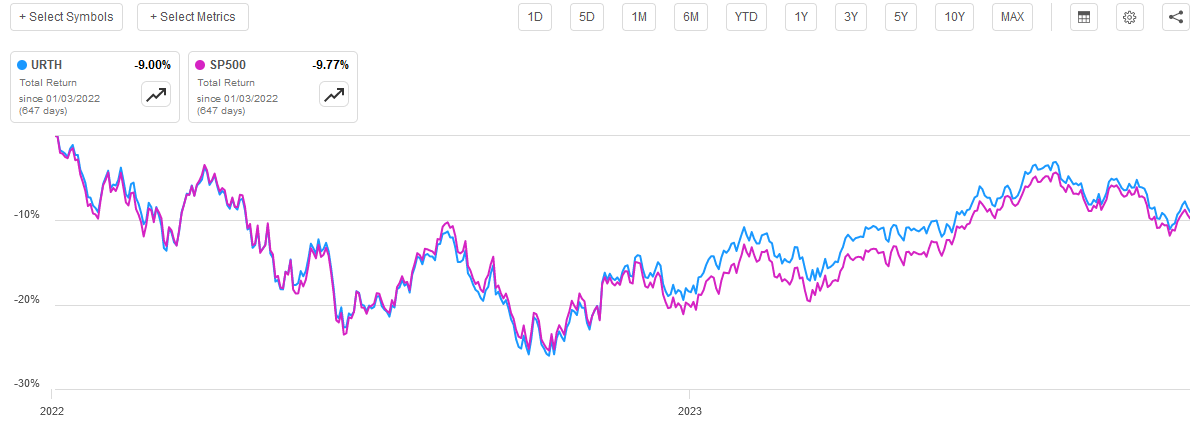

As I have pointed out in numerous previous articles, common equities are by their very nature total return vehicles. After all, investors typically purchase common equities both to receive an income via the dividends that these securities pay out as well as benefit from the capital gains that should accompany the growth and prosperity of the issuing company. However, these capital gains have been somewhat difficult to obtain lately. Since the start of 2022, both the S&P 500 Index and the MSCI World Index have delivered negative total returns:

{kind=link}

There have been small pockets of the market that have done well, but clearly, the indices have both left a lot to be desired. This is mostly because both indices are heavily weighted to long-duration assets such as technology. They are under-weighted to short-duration assets such as energy. We can see this here for the MSCI World Index:

| Sector |

| Current Weighting |

| Information Technology |

| 22.17% |

| Energy |

| 5.16% |

The S&P 500 Index is even more unbalanced between the two sectors. This matters right now because of the market’s increasing preference for short-duration assets due to high interest rates. The majority of technology companies need a number of years in order to grow into their valuations, while energy companies can justify their valuations right now. Over the past twelve months, Google ( GOOG ) (GOOGL) had a net income of $60.953 billion and a market capitalization of $1.74 trillion. During the same period, Exxon Mobil ( XOM ) had a net income of $51.720 billion and a market capitalization of $435.41 billion. Thus, in order for Google to justify its current valuation relative to Exxon Mobil, Exxon Mobil would need to go up to about $400 per share. This is what is meant by long-duration versus short-duration stocks. The expectation is that Google’s net income will eventually grow to the point where its net income is somewhere around $200 billion. As rates go up, investors become less patient, which is the reason why technology tends to fall so much when rates rise while other sectors do not. As technology accounts for the largest individual sector in both the S&P 500 Index and the MSCI World, the weak performance of these stocks more than overpowers the strong performance from energy and other short-duration sectors.

Fortunately, the Lazard Global Total Return and Income Fund is somewhat more conservatively invested. As we can see here, 22.27% of the fund is invested in defensive stocks, which is larger than the 16.40% weighting to technology:

CEF Connect

Despite the fact that technology accounts for a smaller percentage of the fund than it does in the MSCI World Index, we still see that this fund is heavily exposed to cyclical sectors. This may not be a very good thing right now. As I have pointed out in a few recent articles (such as this one ), there are some very strong reasons to expect that the United States may be about to enter into a recession. While only half of this fund’s assets are invested in American companies, recessions in the United States still tend to cause economic problems in the rest of the developed world. As such, there is still a big case to be made for increasing exposure to defensive stocks at the expense of cyclical ones. The fund’s current allocation could cause it to experience more losses than we have already seen over the past several months as the economy continues to weaken.

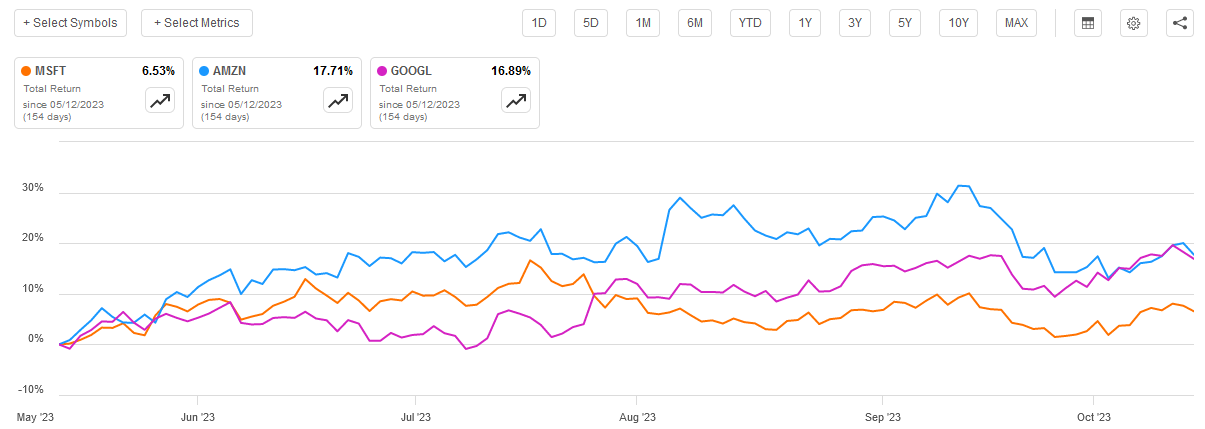

Interestingly, the fund has significantly increased its exposure to the major American technology stocks since we last discussed it. Here are its largest positions as of the end of September:

CEF Connect

Here are the weightings to the top three stocks the last time that we looked at this fund:

As we can see, all three of these stocks saw their weightings in the fund increase by quite a lot. It is uncertain whether this is the result of strong performance relative to the rest of the portfolio or if the fund actively bought shares. All three of these stocks are up since we last discussed the fund, although they have fallen off quite a bit since peaking in mid-September:

{kind=link}

The fund only has a 15.00% annual turnover, so it seems unlikely that it bought more shares to actively increase its position. Most likely the weighting increase is due to the strong performance that these stocks have delivered relative to the rest of the market over the period. However, the recent steep drop-off in Amazon probably reduced its weight somewhat from what is shown in the chart above.

Fortunately, there is nothing here that accounts for so much of the portfolio that it exposes it to idiosyncratic risk. The big concern is that the fund seems to be positioned for a period of strong economic growth and low interest rates, but that is unlikely to be what actually happens. Thus, the fund’s performance might end up being disappointing compared to something that is more weighted toward short-duration assets.

Leverage

As is the case with most closed-end funds, the Lazard Global Total Return and Income Fund employs leverage as a means of boosting its effective total return. I explained how this works in my previous article on this fund:

In short, the fund borrows money and then uses those borrowed funds to purchase stocks and other assets. As long as the total return of the purchased securities is greater than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the overall yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like to see a fund’s leverage exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Lazard Global Total Return and Income Fund has leveraged assets comprising 11.59% of its portfolio. This is a slight increase over the 11.04% leverage ratio that the fund had the last time that we discussed it, but it still remains well below that one-third level. As such, we probably do not have to worry too much about the fund’s leverage, but this will still amplify any losses in the event that rates continue to rise.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Lazard Global Total Return and Income Fund is to provide its investors with a high level of total return. However, this is still a closed-end fund. The way that these funds work is that they aim to maintain a relatively stable net asset value and pay out all of their investment profits to the shareholders in the form of distributions. The fund will pay out both realized gains and any dividends or interest that it receives. When we consider that the market usually goes up by 9% to 11% annually, that distribution can end up giving the fund a fairly high yield.

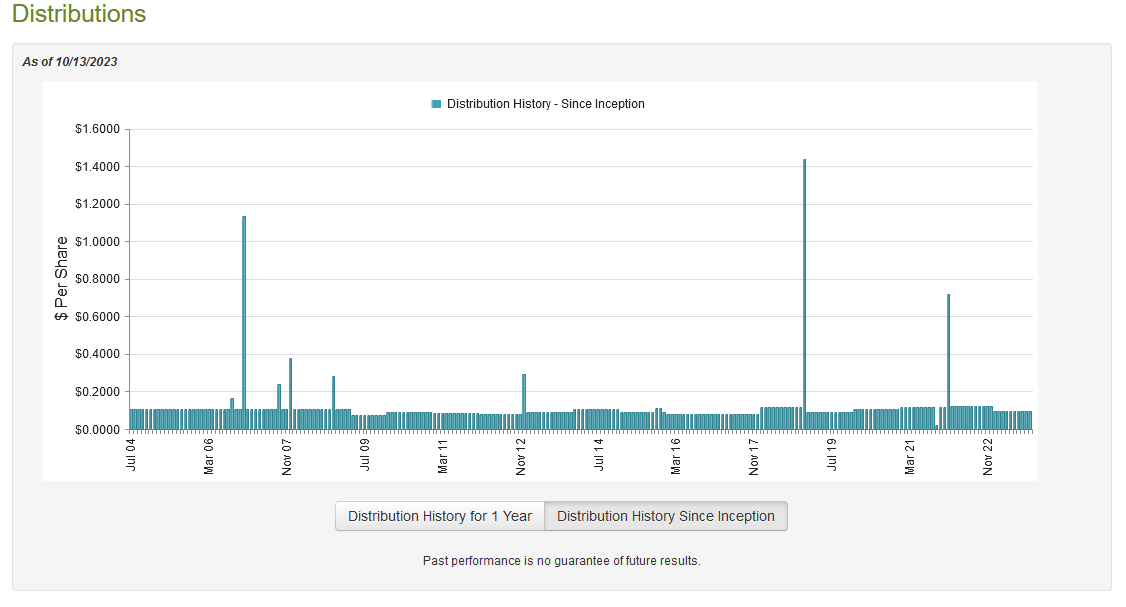

This fund is not an exception to the high-yield rule. It currently pays out a monthly distribution of $0.0934 per share ($1.1208 per share annually), which gives it an 8.26% yield at the current share price. This is not an especially high yield compared to some other funds available in the market, but it is still respectable. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. As we can see here, it has both increased and decreased numerous times:

{kind=link}

The fact that the fund has changed its distribution fairly frequently over the years might reduce its appeal in the eyes of those investors who are seeking to earn a secure and safe distribution that can be used to pay their bills and finance their lifestyles. However, the fact that this is an equity fund means that we should not always expect stable distributions over the long term. While it is true that some funds manage to deliver them, investment returns will vary over time so the fund will need to adjust its distribution to ensure that it is not paying out more than it manages to earn and depleting its assets. That is, after all, unlikely to be sustainable in the long term.

Let us investigate the fund’s finances to see how well it is covering its current distribution.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ends on June 30, 2023. This is a newer report than the one that we had available the last time that we discussed this fund. This is nice because it covers the first half of this year. That was a good period for long-duration assets due to the mania surrounding artificial intelligence technology and the expectations that the Federal Reserve would shortly pivot and slash interest rates. While it seems quite certain that no significant near-term rate cuts will be coming, the market sell-off did not occur after the period ended. Thus, the period that is reflected in this report was one that presented the fund with some opportunities to earn some capital gains. The report will give us a good idea of how well it managed to accomplish this.

During the six-month period, the Lazard Global Total Return and Income Fund received $2,018,611 in dividends (net of foreign withholding taxes) and $880,501 in interest from the assets in its portfolio. This gives the fund a total investment income of $2,899,112 over the period. It paid its expenses out of this amount, which left it with $557,114 available for shareholders. That is obviously nowhere close to enough to cover the $7,291,672 that the fund paid out in distributions during the period. At first glance, that might be concerning as the fund clearly failed to cover its distribution out of net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might have been able to realize capital gains during the period that could be paid out. The fund did have some success in this area, as it reported net realized gains of $3,926,577 and had another $23,109,339 in unrealized gains during the period. The fund’s net assets increased by $20,301,358 during the period after accounting for all inflows and outflows. Thus, the fund technically did cover its distribution.

However, as we can see, the fund’s net assets only went up because of unrealized gains. It is quite possible for unrealized gains to be erased in a market correction. As such, we do not want to depend solely on these to cover the distribution. It is uncertain how sustainable it will prove to be over the second half of this year. We should pay close attention to the fund’s financial report when it is next released in order to make sure that it did not lose too much in the recent market correction.

Valuation

As of October 13, 2023 (the most recent date for which data is currently available), the Lazard Global Total Return and Income Fund has a net asset value of $15.93 per share but the shares only trade for $13.63 each. That gives the fund a 14.44% discount on net asset value at the current price. This is better than the 13.72% discount that the shares have had on average over the past month. Thus, the current price looks like a reasonable entry point if you want this fund.

Conclusion

In conclusion, the Lazard Global Total Return and Income Fund is a somewhat under-followed closed-end fund that is fairly well diversified internationally. Unfortunately, it has been underperforming both the S&P 500 Index and the MSCI World Index even when its distributions are considered. This is concerning, as is the fact that the fund does not appear to be positioned for an economic slowdown. This could cause this fund’s performance to disappoint as the United States starts to descend into a recession.

For further details see:

LGI: Global Diversification And Fully-Covered Distribution, But Performance Might Disappoint