CA - Linamar: Good Set Up For Strong Returns

2023-09-25 04:51:55 ET

Summary

- Linamar is an advanced auto parts manufacturing company based in Ontario, Canada, with global operations.

- Despite challenges in 2020, Linamar has consistently grown revenue and EBITDA, with double-digit sales and EBITDA growth forecasted for fiscal 2023.

- The company is more counter-cyclical than in previous years and sees this as a low-risk way to obtain double-digit returns.

Introduction

Linamar ( LNR:CA ) is an advanced auto parts manufacturing company based in Guelph, Ontario but operates globally. It was founded by Frank Hasenfratz in 1967 (recently passed away), father of Linda Hasenfratz who is the current CEO and has been considered one of Canada's top CEOs by Canadian Business Magazine. LNR is comprised of two operating segments; the industrial segment and the mobility segment.

The mobility segment operates as a tier 1 supplier to the automotive industry. This segment derives revenues from the design of transmissions, engines, and driveline systems used in Internal Combustion Engines (ICEs), Battery Electric Vehicles (BEVs), and Hybrid Electric Vehicles (HEVs). Customers are OEMs and suppliers such as Ford ( F ), GM ( GM ), and Volkswagen ( OTCPK:VWAGY ).

The Industrial segment is comprised of three brands; Skyjack, MacDon, and Salford which was acquired in 2022. Skyjack manufactures aerial work (Access) platforms such as boom lifts and telehandlers. MacDon is involved in harvest equipment while Salford manufactures high-quality tillage and precision application equipment.

The Mobility segment accounts for 72% of sales while the ever-growing Industrial Segment Accounts for 28% of sales. While LNR is known for being an auto manufacturing company it is unique due to its exposure to industrial manufacturing which diversifies the risks in its production portfolio which is not the case with Magna ( MG:CA ) or Martinrea ( MRE:CA ).

{kind=link}

I have long been a bull on this company but have not written an article since 2018. Please feel free to read my article New NAFTA Linamar DCF Valuation which does a detailed DCF analysis.

Investment Thesis

As a testament to the quality of LNR, they have managed to grow revenue and EBITDA almost every year since 2010 and managed an ROIC of at least 7% every year. The only exception is fiscal 2020, but what company did beat their 2019 results other than Zoom ( ZM ) or Costco ( COST ).

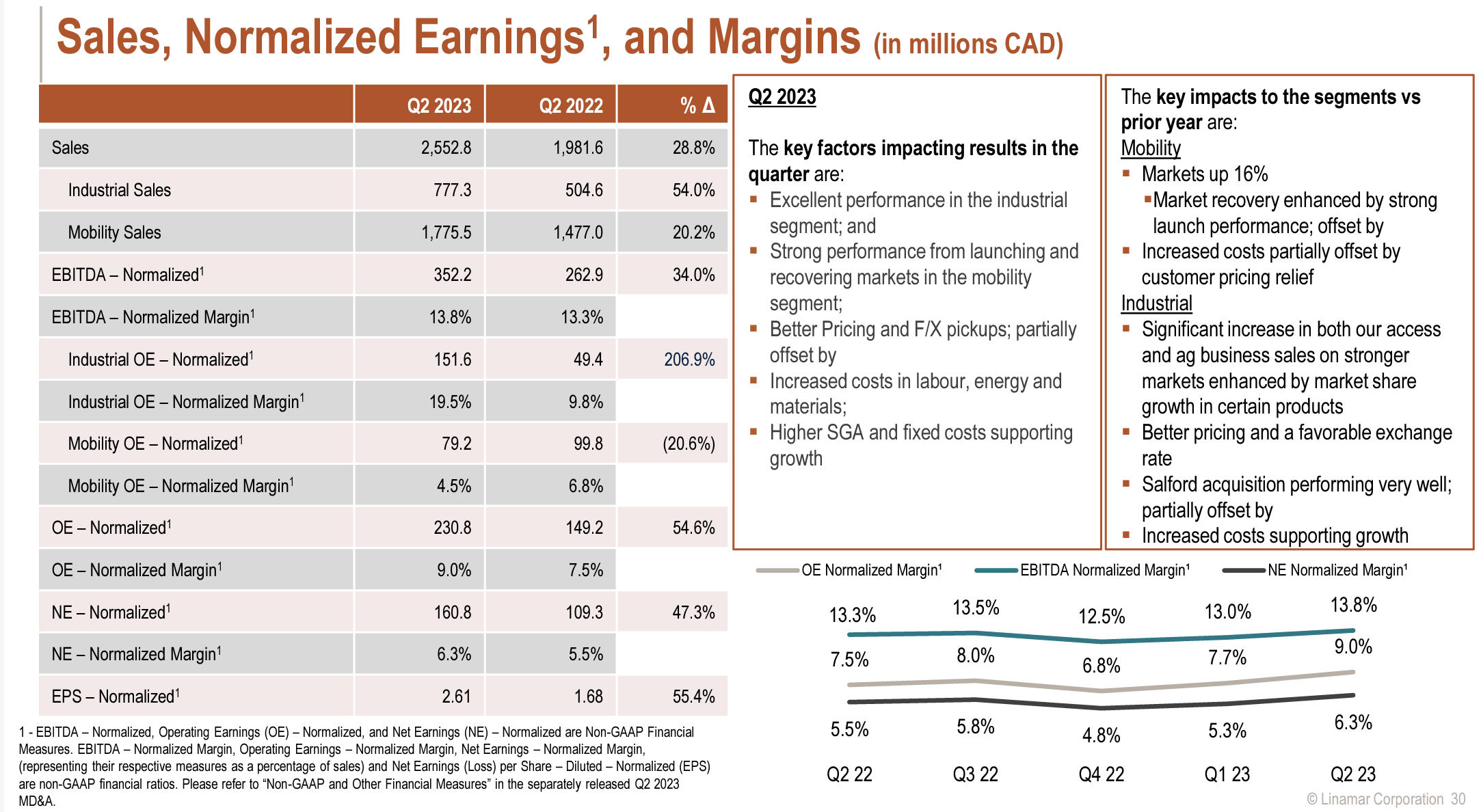

LNR had forecasted double digit sales and EBITDA growth for fiscal 2023 at the end of 2022 and has done exactly that through the first 6 months of 2023. Sales in the mobile segment are up 20.2% but more impressively sales in the industrial segment are up 56% for total sales growth of 28% YoY. This has partially been the result of FX gains but largely increased sales related to launching programs in the mobile segment, increases in agricultural sales from market growth further improved by market share growth in core products, and additional access equipment sales primarily due to increased market volumes in addition to market share growth for booms in Europe which has become one of the larger markets for Access equipment. The only blemish for LNR was that mobility's normalized EBITDA was lower by ~$16 Million, as the margin compressed from ~13% to ~10.6% due to increased costs related to labour, materials, freight, and utilities and SG&A costs supporting growth which could not offset higher pricing in the segment. This has been more than offset by the growth in the Industrial segment.

{kind=link}

Some might wonder if double digit growth is achievable with the prospect of a recession on the horizon. I argue it is.

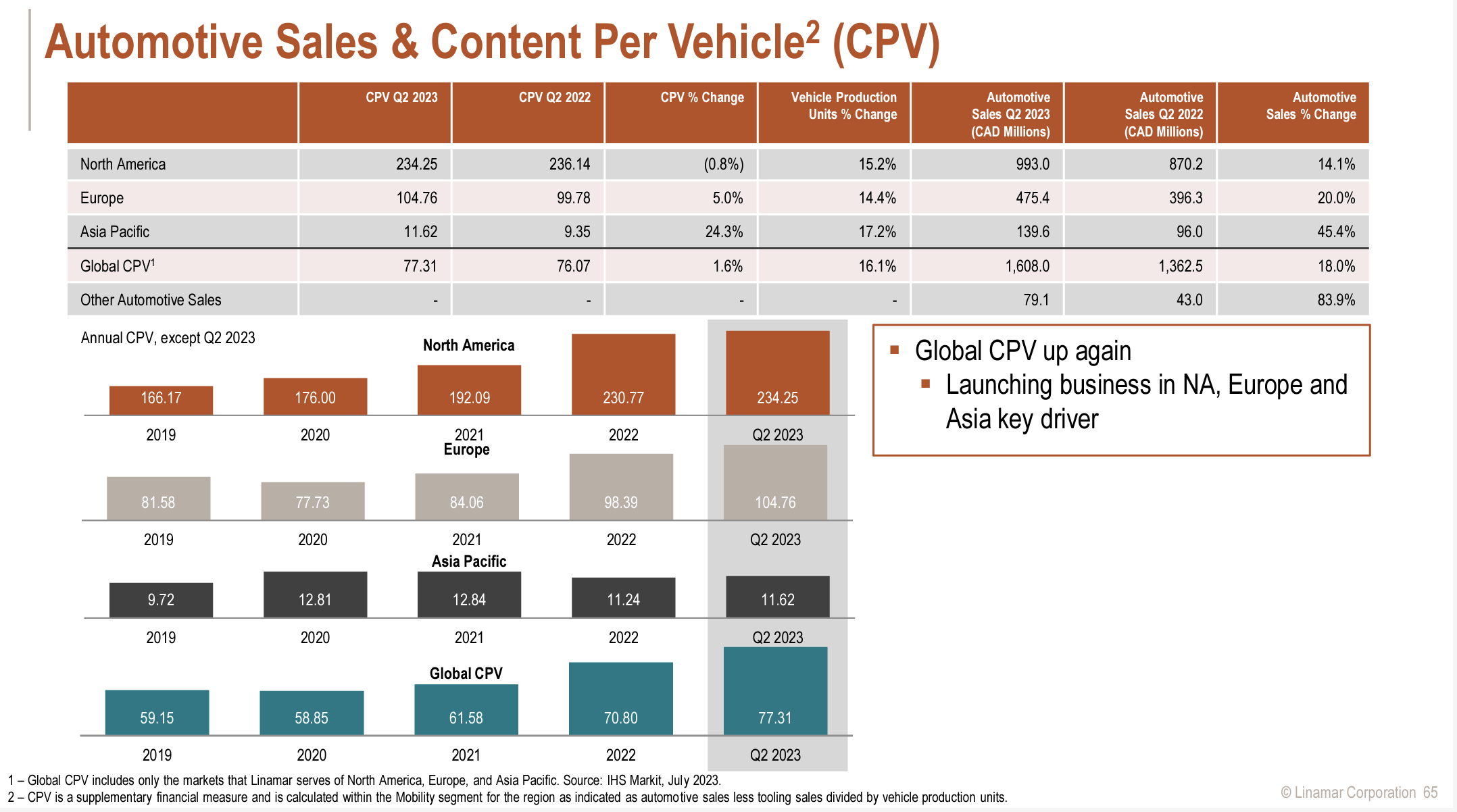

First of all auto inventories are at their lowest levels in a decade in North America with the inventory/sales ratio at less than 1:1. It was as low as 0.5:1 in early 2022 meaning there was only half a car on the lot for every customer. Production has been catching up and will have to get to historical levels of at least 2:1 at some point. According to management, North American automotive sales for Q2 2023 increased 14% from Q2 2022 in a market that saw an increase of ~15% in production volumes for the same period. Europe saw an even greater results as automotive sales for Q2 2023 increased ~20% from Q2 2022 in a market that saw an increase of ~14% in production volumes for the same period. LNR has managed to keep its content per vehicle ((CPV)) at least constant as a percentage of total vehicle sales YoY so even a double digit increase in production volumes would get them there already. LNR's revenues from this segment may end up being countercyclical for the first time in its history

{kind=link}

{kind=link}

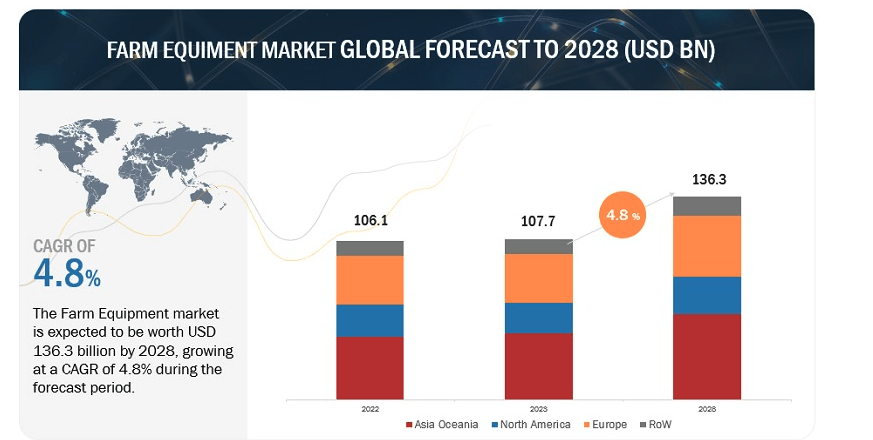

On the industrial side, I expect the current tailwinds to continue. First on the agricultural side, the equipment market is expected to grow from USD $107 Billion in 2023 to USD $136 Billion by 2032 for a CAGR of 4.8% according to Markets and Markets . The rising demand is due to increasing population growth which is projected to be 9.7 Billion by 2050. The increasing food demand requires advanced technology and large-scale farming which necessitates the most advanced equipment. Inventory at agriculture equipment retailers remains below historical levels which continues to drive demand and people still have to eat even during recessions so I believe this segment to largely be recession-proof.

{kind=link}

On the Access side, the market for material handling equipment is expected to also increase by 5% annually from its current levels of $140 Billion according to GMI Market Insights . This is due to the increasing automation technology deployment and e-commerce shopping trends. Consumers have become aware of the inconvenience of manual labour employment which has necessitated the move to automation to decrease costs over time. Much of this growth will be driven by third-party logistics (3PL) applications. The supply chain issues that came about as a result of COVID, have not been entirely resolved so manufacturers are still trying to squeeze the most output possible with the limited space they have which is where access to equipment makes a difference. I don't think a prolonged recession is enough to completely temper demand.

{kind=link}

Verdict

The price to sales ratio is appropriate for determining cyclical turning points. The stock is among the cheapest it has been in the last 10 years aside from 2020. The P/S ratio has fallen to levels witnessed in 2017-2018 when the U.S. Government wanted to renegotiate steel tariffs on North American companies. The outcome had minimal effect on LNR's financial results and continued to improve its financial position over the ensuing years.

The setup is even better than it was in 2017-2018 as LNR does not need a whole lot to go right to at least meet high single digit free cash flow growth as it has become more countercyclical than in previous years. Recall from my previous article New NAFTA Linamar DCF Valuation I had determined that fair value per share at $78/share and LNR's prospects have only improved since then. LNR produced $94MM in free cash flow for FYE 2022 and is on pace to exceed $100M for 2023 which is roughly 4% of its market capitalization. The Net Debt to EBITDA ratio is only 0.4X as the amount of Cash on the balance sheet is almost enough to fully repay debt so isn't hampered by toxic debt. Although LNR has not been too generous with share buybacks and dividends and typically just hoards cash with $1.4MM in cash on the balance sheet it has plenty of optionality with regards to returning capital to shareholders. I still see this as a low downside play given the beaten-down valuation. Worst case scenario there is no multiple expansion and LNR just returns 4% or more of the capital to shareholders which may not be too appealing with 5-year Canada Bond rates at ~4%, but if LNR does come through as promised combined with some multiple expansion this could deliver double-digit returns.

For further details see:

Linamar: Good Set Up For Strong Returns