SAH - Lithia Motors: Worth A Ride As Earnings Near

2023-04-09 04:59:07 ET

Summary

- The management team at Lithia Motors is due to announce financial results for the first quarter of the company's 2023 fiscal year in the coming days.

- Recently, shares have underperformed the market even as sales climb, and this is due to concerns over worsening market conditions.

- While weakness could lie ahead, I believe it's unlikely that the company would look worse than fairly valued.

- This translates to a favorable risk-to-reward prospect right now.

Most investors in the market seemed to respond to expectations of what the near-term future holds. For instance, if a segment of the market is expected to weaken moving forward, they might sell stock that they own in companies that are dedicated to that segment. While this makes sense to some degree, those who are longer-term in their focus and who believe that any weakening is only temporary, might do the opposite and buy into that weakness. One really good example of a market that is experiencing pain but that offers opportunity as that pain builds is the automotive retail space. And one of the companies that is trading near the lower end of the spectrum from a valuation perspective is Lithia Motors ( LAD ). Although I fully expect the next few quarters to be weaker for the enterprise than the past several have been, I do think that the company offers attractive upside in the long run.

The picture is changing

Back in the middle of December of last year, I revisited my prior thesis on Lithia Motors. In that article , I kept the company rated a 'buy' to reflect my view that shares should outperform the broader market for the foreseeable future. This assessment was based on the continued rapid growth that management was achieving, thanks not only to higher prices in the automotive retail space, but also thanks to various acquisitions the company had engaged in. Even at that point, the company had been showing signs of weakness. But the stock was cheap enough, in my opinion, to justify a bullish outlook. Since then, things have not gone exactly as I had hoped. While the S&P 500 is up 4.2%, shares of Lithia Motors have seen downside of 3.4%.

{kind=link}

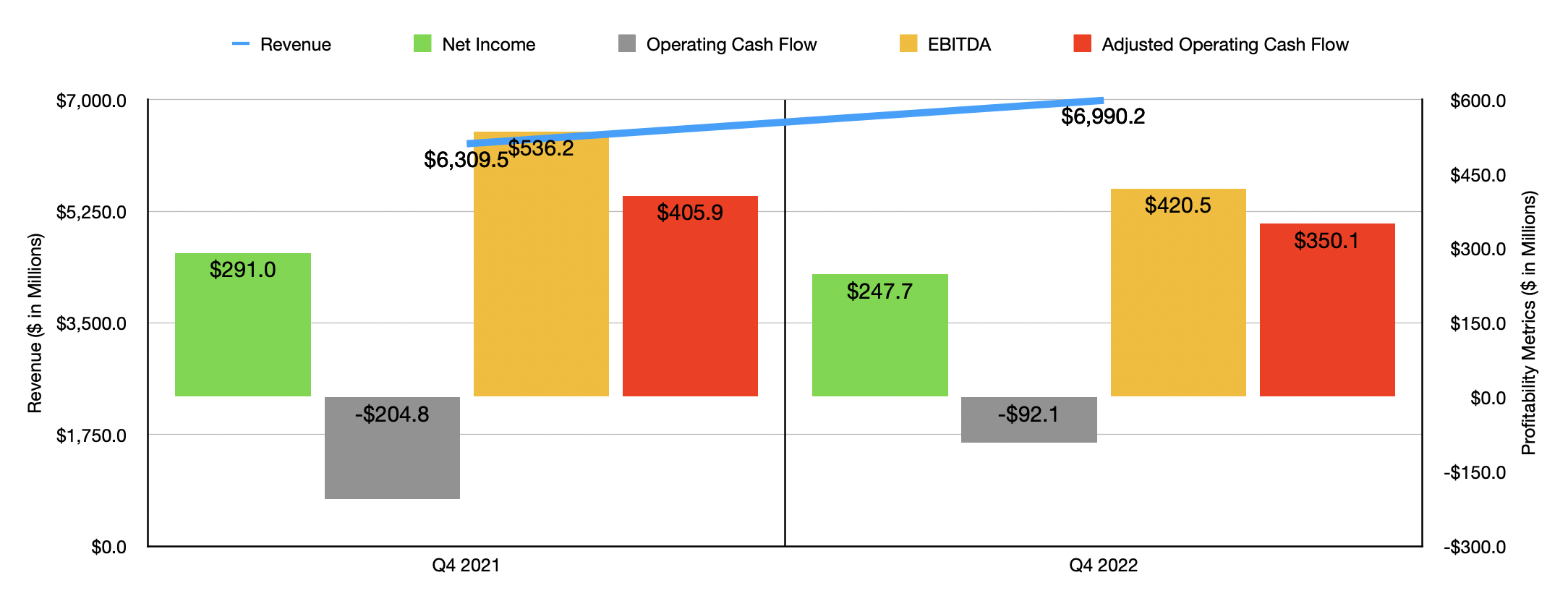

In a sense, this return disparity is logical. When you look at the financial performance that the company has achieved recently, perhaps some near-term downside should have been expected. To see what I mean, we should look at financial results covering the final quarter of the company's 2022 fiscal year . During that time, revenue came in strong at $6.99 billion. That's 10.8% higher than the $6.31 billion the company reported the same quarter one year earlier. In overall dollar terms, the greatest upside for the company came from its new vehicle retail sales. Revenue there spiked 10.6%, climbing from $2.96 billion to $3.28 billion. This rise came because of two primary factors. First and foremost, the number of new vehicles sold by the company jumped 5.2% from 64,812 units to 68,159 units. Along the way, the average selling price per vehicle grew 5.2% from $45,671 to $48,051. The company saw strength elsewhere as well. Used vehicle sales rose 10.4%, with the number of units sold rising 8.5%, while the average selling price grew only 1.8%. Other parts of the company also expanded, though they were less significant in the grand scheme of things than new and used sales.

So far, everything here looks great. But it's important to keep in mind that the company has been focused in recent years on rapid growth by means of acquisition. In the fourth quarter of last year alone, the company acquired nine different stores, with annual revenue expected from them of $560 million. And in 2022 as a whole, the company acquired 31 stores, with expected revenue from them each year of $3.5 billion. By comparison, it only sold 13 locations that accounted for $663 million in revenue per year. When you look instead at same-store results, the picture is a bit different. New vehicle retail sales in the final quarter of the year dropped 6.6%, while used vehicle retail sales declined 0.1%.

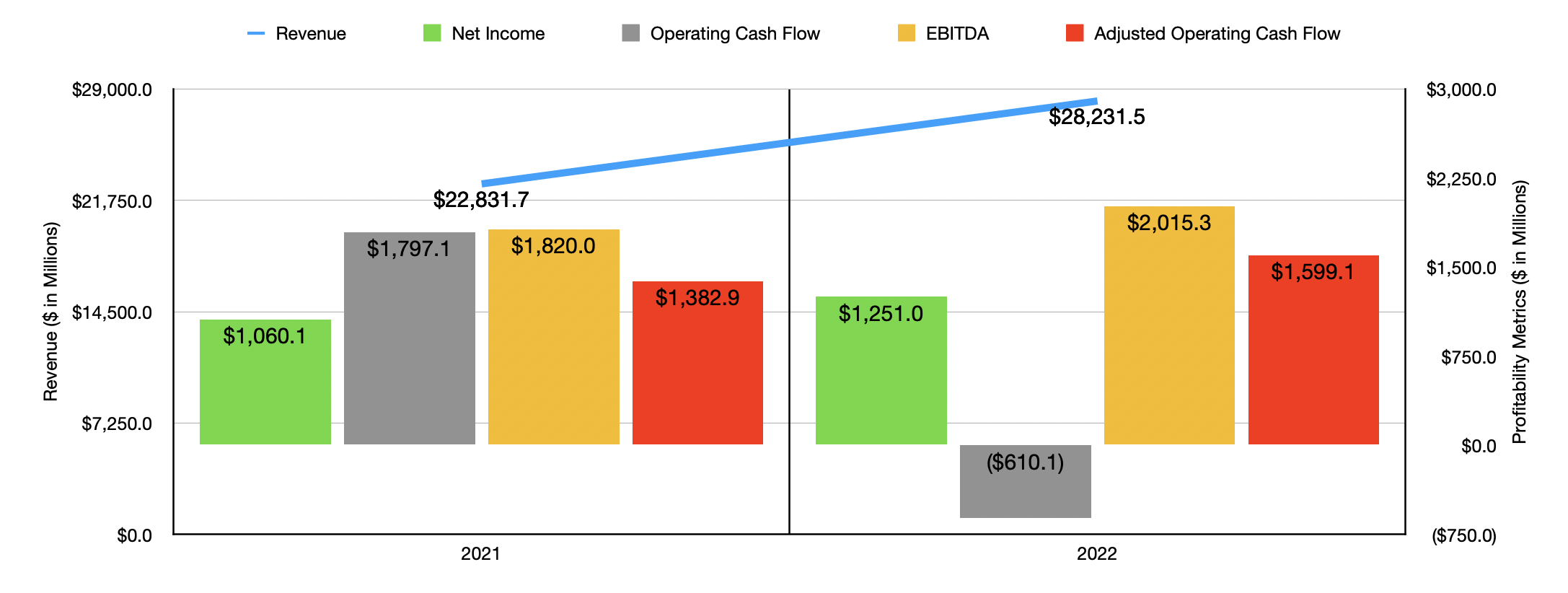

On the bottom line, the picture for the company also worsened, as the gross profit per vehicle sold contracted because of inflationary pressures and the inability to keep raising prices. Net income of $247.7 million came in lower than the $291 million reported one year earlier. As you can see in the initial chart shown in this article, most other profitability metrics also worsened year over year. Despite this weak final quarter, 2022 as a whole was rather robust. As you can see in the chart below, revenue for the year jumped 23.7%, while three of the four profitability metrics I looked at showed nice improvements. But again, really all of this upside was driven by acquisition activities. In fact, total new vehicle retail sales on a same-store basis declined by 15.4% last year. Over that same window of time, used vehicle retail sales declined by 0.9%.

{kind=link}

Keep an eye out on Q1 results

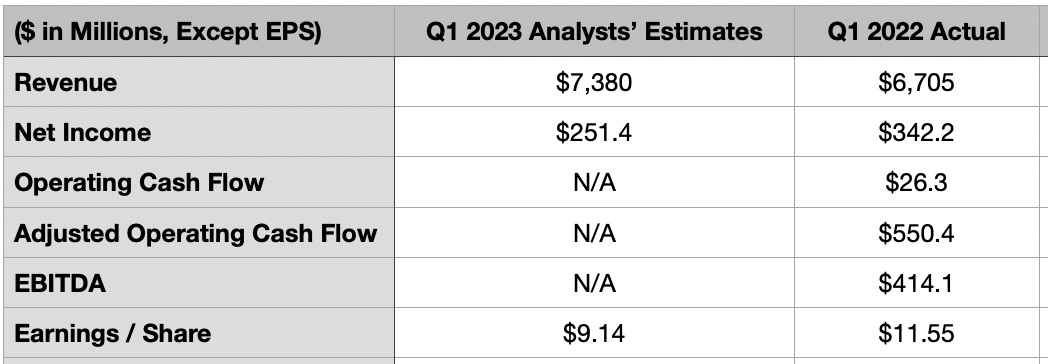

On April 19th of this year, the management team is expected to announce financial results covering the first quarter of the company's 2023 fiscal year. This will give investors a great chance to see exactly how much additional pain is building up in this space. At present, analysts have high expectations from a revenue perspective. No doubt driven by continued elevated prices and higher overall unit sales because of acquisition activities, analysts are anticipating revenue of $7.38 billion. That compares to the $6.71 billion the company reported one year earlier. Digging deeper into these numbers, investors would be wise to look at the same store figures. There are no estimates as to what these might come in at. But if we see significant same-store contraction, as I suspect we will, it could prove somewhat painful for the company in the near term.

{kind=link}

On the bottom line, analysts are a bit more conservative. They currently think that earnings per share will be about $9.14. By comparison, earnings per share in the first quarter of 2022 came out to $11.55. It is unclear what this means for the company's bottom line as a whole, since the firm has actively bought back stock. Throughout 2022, the company allocated $662.4 million to repurchase 2.4 million shares in all. And at the end of the fiscal year, they still had $501 million in capacity under their existing plan. Assuming that the share count has not changed since the end of the final quarter last year, this would translate to net income of $251.4 million. That's down considerably from the $342.2 million reported one year earlier. Investors should also be paying careful attention to other profitability metrics like operating cash flow, adjusted operating cash flow, and EBITDA. For context, these numbers can be seen in the chart above.

{kind=link}

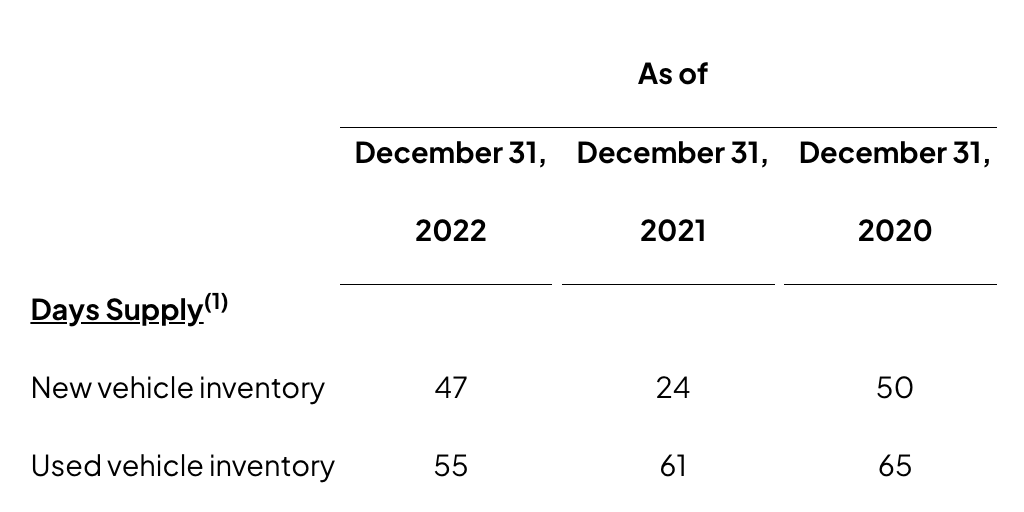

Another metric that is often overlooked is the day's supply of inventory. This is how many days the company has worth of vehicles before it would run out. Interestingly, at the end of the 2022 fiscal year, the company had 55 days' worth of sales for used vehicles. This was down from the 61 days reported one year earlier. However, there does seem to be a glut in new vehicles. Over the same window of time, the figure jumped from 23 days to 47 days. In the first quarter of 2022, the company had 50 days' worth of inventories when it came to used vehicles. But for new vehicles, that number was 27. In the event that the new vehicle numbers are deemed to be elevated, it could imply an inventory glut that could cause the company to significantly lower prices in order to keep customers buying. Obviously, economic issues like high inflation are a problem here, but also a problem are the high interest rates that are being dealt with that are aimed at combating said inflation. Higher interest rates make acquiring a vehicle more costly and, therefore, less appealing. For full transparency, though, what this may also represent is something more akin to a return to normalcy, as these latest numbers are more in line with what the company had in inventories in 2020. That would translate to shares being closer to fairly valued.

Shares have nice upside

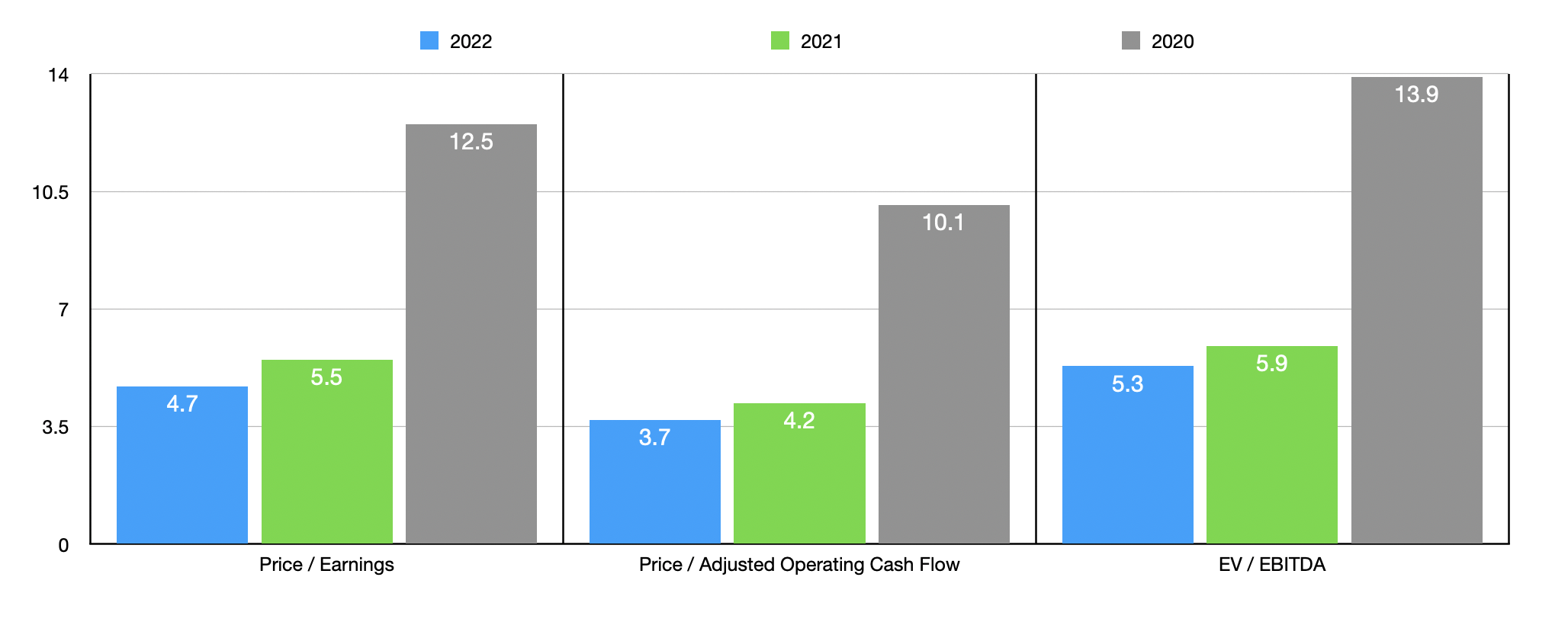

Looking at the recent weakness that the company has exhibited, and assuming that the picture will continue to worsen, it may seem unwise to buy stock in Lithia Motors or any of its peers. However, shares in the business look incredibly cheap at this moment. In the chart below, you can see how I priced the company using three different pricing metrics and using data from three different fiscal years. Using results from both 2021 and 2022, the company looks very cheap. Some investors may point out, justifiably so, that weakness ahead could result in financial performance reverting back to something like what we saw in 2020. In that case, shares wouldn't be cheap. But I wouldn't call them overvalued either. However, I think such a significant change in performance would be unlikely.

{kind=link}

I say this because much of the growth that the company has seen over this three-year window has been driven not by the aforementioned price increases or by organic growth, but instead by acquisitions. When a company grows by means of acquisition, it is establishing for itself what is essentially a permanent asset that should permanently elevate sales. For instance, from 2020 to 2021, new vehicle sales, on a unit basis, jumped by 52.3%, while used vehicle sales grew 50.4%. So taking its existing physical footprint and using the economics scene back in 2020 would not result in the levels of profitability experienced in 2020. But even in this unlikely scenario, I would call the company more or less fairly valued. Meanwhile, in the table below, you can see five similar firms that I compared Lithia Motors to. On a price-to-earnings basis and on an EV to EBITDA basis, only two of the five companies were cheaper than our prospect. Using the price to operating cash flow approach, our prospect was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Lithia Motors |

| 4.7 |

| 3.7 |

| 5.3 |

| Penske Automotive Group ( PAG ) |

| 7.3 |

| 6.9 |

| 6.7 |

| Sonic Automotive ( SAH ) |

| 30.1 |

| 4.9 |

| 10.5 |

| Asbury Automotive Group ( ABG ) |

| 4.3 |

| 6.2 |

| 4.8 |

| Group 1 Automotive ( GPI ) |

| 4.6 |

| 5.7 |

| 5.2 |

| AutoNation ( AN ) |

| 5.2 |

| 4.3 |

| 5.5 |

Takeaway

Operationally and fundamentally, I definitely like what I see when I look at Lithia Motors. Shares look dirt cheap at this moment, though I do believe that we will see some pain ahead. While some investors may think that this is the time to get out, I see this as an excellent buying opportunity. However, I also need to mention that Lithia Motors is not my prospect of choice in this market. The firm I prefer is Group 1 Automotive. Having said that, I do still think that Lithia Motors is cheap enough to warrant a solid 'buy' rating at this time.

For further details see:

Lithia Motors: Worth A Ride As Earnings Near