CA - Lithium Americas: An Assessment Of Relative Valuations For The Upcoming Split

2023-09-21 16:48:39 ET

Summary

- Lithium Americas will split into two companies: Lithium Americas (Argentina) and Lithium Americas USA.

- Falling lithium carbonate prices have put pressure on Lithium Americas' share price, despite positive news about project permits and production.

- The split will allocate assets and liabilities between the two companies, with General Motors investing further in Lithium Americas USA.

- Estimated relative valuations are presented for the two companies, post-split.

Lithium Americas ( LAC ) will be splitting into two companies next month. The company will change its name to Lithium Americas (Argentina) and its stock symbol will change to (LAAC), while the US assets will be spun off as Lithium Americas trading under the existing stock symbol LAC.

For clarity, I will refer to the existing company pre-split as Lithium Americas, the new US company as Lithium Americas USA, and the Argentine company as Lithium Argentina.

I have been invested in Lithium Americas for a couple of years. The stock price is down slightly from my initial investment, but I did sell some of my shares close to the high point, so I am about at break-even.

Lithium Carbonate prices are well off their recent highs, having fallen from around 600,000 CNY/tonne ( 84,000/tonne) per tonne in late 2022 to about 180,000 CNY/tonne ( 25,000/tonne). Those falling prices have put pressure on Lithium America's share price offsetting what has been mostly good news regarding the final permits and start of construction at the Thacker Pass project in Nevada, and the start of production at Cauchari-Olaroz in Argentina.

According to Fastmarkets , oversupply will continue to pressure prices until 2026 when demand from the growth of electric vehicle sales will catch up with extra supply that is coming online.

I will hold my shares until after the split, I am hoping the companies will trade at a higher combined price as separate companies than as a combined company. The two operations have different risk profiles and there are probably some investors who would buy into one or other of the two companies whereas they will not buy the combination of both.

After the split I will look at each on its merits and depending on the relative share price I may dispose of one or both.

The separation

The company's assets and liabilities will be allocated as follows :

Lithium Americas, USA

- The Thacker Pass project in Humboldt County, Nevada.

- Investments in Green Technology Metals Ltd (an Australian public company with Lithium projects in Ontario), and Ascend Elements Inc. (a battery chemical manufacturer and recycling company in the USA). Neither investment has a material impact on LAC's valuation.

Lithium Argentina

- 44.8% interest in the Cauchari-Olaroz lithium project.

- 100% interest in the Pastos Grandes lithium project.

- 65% interest in the Sal de la Puna lithium project.

The cash and cash equivalents will be split, approximately $306 million to Americas and $167 million to Argentina.

General Motors owns 9.4% of Lithium Americas having invested $320 million last year and will invest a further $330 million. However, the $330 million will not be invested until after the split and will be invested only in the new Lithium Americas USA, at a price to be determined by the 5-day VWAP after the separation.

Debt, in the form of $259 million of convertible notes bearing interest at 1.75% is due in 2027, and a $75 million subordinate loan (undrawn) will remain with Lithium Argentina. However, the debt holders have the option to convert the debt into shares of the combined company prior to the split. There has been no announcement as to whether or not any debt has been converted.

Evaluation of the assets

Thacker Pass

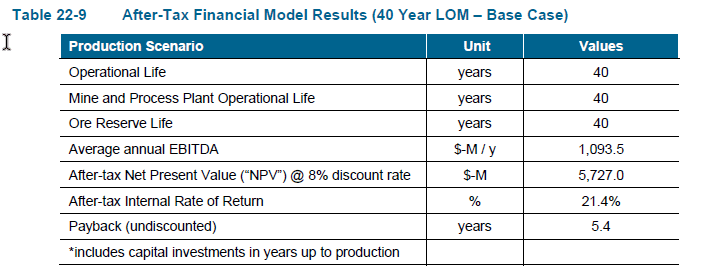

The Thacker Pass project will, I believe, be the first project in the world to extract lithium from clay. All other lithium production is from brine extraction or hard rock mining projects. The Thacker Pass area is known to contain substantial lithium deposits, and the claims owned by Lithium Americas include lithium-bearing clays that can sustain the mine well beyond the 40-year production life on which the financial evaluation is based.

This is the economic evaluation from the feasibility study completed in November 2022

Thacker Pass Economic Evaluation (Feasibility Study)

{kind=link}

Capital costs are estimated to be $3.996 billion , of which $2.268 billion will be spent in Phase 1, and the remainder in Phase 2 which will begin 3 years after Phase 1 is complete.

Operating costs are estimated to be $7,198/tonne of Lithium Carbonate

The assumed selling price for Lithium Carbonate is $24,000/tonne .

Thacker Pass has completed all the environmental studies and permitting requirements for the project, an extensive and time-consuming process, the completion of which significantly de-risks the project. Construction is at a very early stage and production is not expected until 2026.

Cauchari-Olaroz

The Cauchari-Olaroz project (LAC website)

{kind=link}

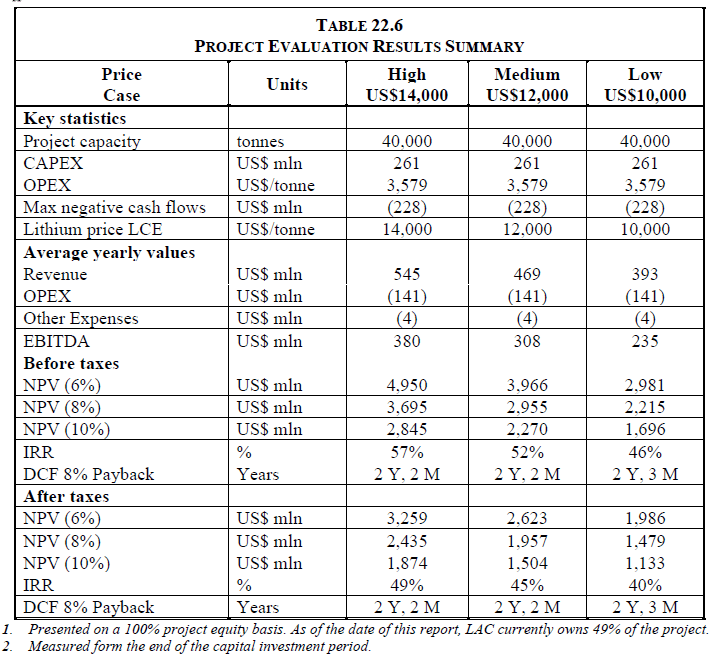

The latest feasibility study for Cauchari-Olaroz was issued in September 2020. The table below comes from that study.

Cauchari-Olaroz Economic Evaluation (Feasibility Study)

{kind=link}

The base case Net Present Value at an 8% discount rate is $1.957 billion, after taxes.

Operating costs are $3,579/tonne.

The point to note is that the base case for Cauchari-Olaroz uses a lithium carbonate price of $12,000/tonne compared to $24,000/tonne in the study for Thacker Pass. At a $24,000/tonne lithium carbonate price, the NPV for Cauchari-Olaroz would increase to $4.233 billion . Conversely, if Thacker Pass were to be evaluated at $12,000/tonne it would have a negative NPV.

Construction of Cauchari-Olaroz is complete, and the project shipped its first load of product in June 2023.

Pastos Grandes

The feasibility study for Pastos Grandes dates back to 2019 when the property was owned by Millennial Lithium. The study proposed a production rate of up to 24,000 tonnes per year over a 40-year project life.

The projected after-tax NPV was $1.03 billion based on a lithium carbonate price of $13,050/tonne. That would increase to $2.24 billion with a lithium carbonate price of $24,000/tonne.

Construction has not started, and no production is likely before 2026 at the earliest.

Sal de la Puma

Ownership of the Sal de la Puma property comes from the acquisition of Arena Minerals in April 2023. The property is in the early stages of development and there is no feasibility study or project evaluation.

Arena Minerals was acquired in exchange for 8.4 million Lithium Americas shares plus a small amount of cash. Its value on the balance sheet is $182 million .

Shares outstanding and potential dilution.

One of the key risks with non-producing mining projects is dilution from share issues during the period prior to the start of production when cash flows are negative.

Both companies will have 160 million shares outstanding after the split, but the US company will sell shares immediately after the split.

Lithium Americas USA will finance the Thacker Pass project with existing cash, a $330 million investment from General Motors, and an anticipated loan from the DOE for 75% of the value of the project. The GM investment will dilute the shares, the amount of dilution depends on the trading price in the five days following the split. For example, if the share price after the split is $12, GM will receive 27.5 million shares.

Lithium Argentina should be able to finance its future project from cash flow because capital spending at Cauchari-Olaroz is almost complete, and the project is already producing. I don't include any dilution for Lithium Argentina.

Discounting for risk

Mining is a risky business, and Lithium mining is no exception. The values from the feasibility studies must be discounted to account for risk.

It will be three years before Thacker Pass provides positive cash flow. Project risks include CAPEX and OPEX cost overruns and technical risks. This will be the first project to extract lithium from the Nevada clays and the process has not been proven at a commercial scale. I reduced the value of Thacker Pass to 70% of the feasibility study NPV to account for risk.

Cauchari-Olaroz is already producing, positive cash flow is imminent and there is very little process risk. However, there is a country risk. Argentina is going through a period of hyperinflation. That, in itself, is not a major issue since all evaluations are in US dollars and all income will be in US dollars. However, it does increase political risk, there is always a chance that the government will increase mining royalties, raise taxes, or even propose nationalization. For that reason, I discount the Cauchari-Olaroz project to 70% of the feasibility study value. The future Cauchari-Olaroz expansion and the Pastos Grande project are discounted to 30% as they include both country risk and project risk.

Summary

Below is a summary of my valuation, based on a $24,000/tonne lithium carbonate price for all projects:

Evaluation Summary (Calculated)

I put the value of Lithium America ((LAC)) at $24.77/share and Lithium Argentina (LAAC) at $14.71/share, a combined value of $39.48/share and a potential upside of approximately 100% versus today's share price.

The information comes from published feasibility studies, and the discount factors are my own judgment.

The major risk for both valuations is the future price of Lithium Carbonate. I have made the evaluation based on prices of $24,000/tonne, though quoted spot prices do not necessarily reflect actual prices since most lithium is bought and sold on long-term contracts. However, because of the higher operating cost, the Thacker Pass valuation is more sensitive to changes in lithium prices, so a drop in lithium prices presents more risk to Lithium Americas USA than it does to Lithium Argentina.

I believe Lithium Americas, pre-split is a worthwhile speculative investment, though certainly not risk-free.

After the split, I value the companies at 70% Lithium Americas USA, and 30% Lithium Argentina. If the share price after the split reflects a wildly different ratio, I may adjust my holdings accordingly.

For further details see:

Lithium Americas: An Assessment Of Relative Valuations For The Upcoming Split