LAC - Lithium Americas Corp.: Navigating A New Era Of Lithium Production Amid Global Demand

2023-06-04 03:26:15 ET

Summary

- Lithium Americas Corp. is uniquely positioned to capitalize on the global demand for lithium, with substantial lithium reserves, strategic production plans, and backing by GM.

- The company is expecting to initiate lithium production at the Argentine Caucharí-Olaroz site by June 2023 and is also advancing on the Thacker Pass project in the United States.

- Despite the current volatility of lithium prices, LAC's long-term valuation holds potential, with industry forecasts indicating a considerable increase in the demand for lithium in the coming years.

- Given LAC's promising growth trajectory, strategic positioning, and commitment to fulfilling the global lithium market's needs, it is considered a strong mid-term growth stock with a buy rating.

Editor's note: Seeking Alpha is proud to welcome Quinn Coughlin as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

In a world thirsting for batteries, Lithium Americas Corp. ( LAC , LAC:CA ) stands as an oasis, ready to quench the market's thirst with their untapped lithium reserves. As lithium prices dance to the rhythm of rising demand, LAC's vast resources, coupled with a strategic game plan, are poised to make a splash in this young growing market.

Background

Lithium Americas Corp. finds itself at the intersection of several global trends: the rise in electric vehicle (EVs) adoption, the growing demand for lithium, and the geopolitics of resource extraction.

Production Capabilities and Outlook

At the Argentine Caucharí-Olaroz site, mechanical construction has been completed, with the first lithium production targeted for June 2023. The site aims to ramp up to 40,000 tons per annum (~$1.28 billion in annualized revenue) of battery-quality lithium carbonate by Q1 2024. Operating costs at this plant are extremely favorable at $3,579 per ton of LCE. Additionally, a Stage 2 expansion is being planned to further increase lithium carbonate production. The company has also continued advancing the $30 million development plan at the Pastos Grandes Basin, with a construction decision expected in Q4 2023.

In the United States, the Thacker Pass project has commenced construction following receipt of notice to proceed from the Bureau of Land Management. Major earthworks are expected to begin in Q2 2023, supporting a target to start production in the second half of 2026. This project has received substantial support in the form of a memorandum of understanding with Bechtel Corporation and the North American Building Trade Unions, along with a potential funding contribution from the DOE's Advanced Technology Vehicles Manufacturing Loan Program. This is an encouraging step as they now look to be out of the legal woodwork. This site is expected to produce 80,000 tons per annum once at full capacity in 2029 and will operate at half capacity from start of production until then. Additionally LAC expects the operating cost of the mine will be $6,743 per ton of LCE which is a quite favorable operating margin.

Recent Developments

In a bid to streamline its operations and potentially mitigate geopolitical risks, Lithium Americas Corp. announced to separate its Argentine and North American business units into two independent public companies during their earning call on May 15, 2023. The separation will have the current Argentina-based assets roll up to "Lithium Argentina." The 100%-owned Thacker Pass lithium project in Humboldt County, Nevada, as well as the company's investments in Green Technology Metals Limited (GTMLF) (ASX:GT1) and Ascend Elements, Inc. will all roll up to "Lithium Americas (NewCo)". Their 6-K filing indicates this decision was made with the intention of providing companies with more narrow strategic focuses and to better pursue their independent growth opportunities. This move was also partly motivated by the complex dynamics of US-China relations and to distance the company from one of its top shareholders, Ganfeng Lithium Group Co., a Chinese lithium producer. Lithium Americas will file a circular with specific details on the separation by the end of June 2023 and will go to a shareholder vote July 31st, 2023. For now, their 6-k cites "Under the plan of arrangement, shareholders will retain their proportionate interest in shares of the Company and receive newly issued shares of Lithium Americas (NewCo) in proportion to their then-current ownership of the Company".

Financial Strength

As of Q1 2023, Lithium Americas Corp. held $604.1 million in cash , cash equivalents, and short-term bank deposits. Total assets amounted to $1,328.4 million, with real long-term liabilities at $213.7 million. This financial strength has been boosted primarily by a substantial equity investment by General Motors Holdings LLC, which agreed to invest $650 million ($320 million being realized on balance sheet in Q1) into the company and receive exclusive access to Phase 1 production at Thacker Pass.

Net change in cash was up $327 million this quarter which is an important development after the past two quarters both being down over $300 million. It is unclear what the separation means for the assets and cash on hand for both entities. We do know that the estimated cost to get Thacker Pass operational is $581 million and GM has committed to invest an additional $330 million that has not been realized on the balance sheet. Even with the unknown terms of the separation LAC's healthy cash holdings will be able to sustain the North American business until Thacker Pass starts producing.

The Bull Thesis

In late April Elon Musk stated, "We are begging you. We do not want to do it! Instead of making a picture-sharing app, please refine lithium. Mining and refining. Heavy industry. Come on!". Elon's statement was a reinforcement of the bull thesis for the Lithium Mining sector. Bottom-line is countries across the world are pushing for EV and clean energy adoption and lithium batteries are the best way to store energy. The world output of lithium batteries in 2022 was 737,000 tons with 2023 production currently forecasted at 964,000 tons. McKinsey's most recent projections have the need for lithium by 2030 to be at 3-4 million tons. That is an industry-wide CAGR of 17.6% in the bear case and up to 22.5% in the bull case. It is clear with the industry needing to meet the growing demand every Lithium producer deserves a look right now. The question is which firms are best positioned to capitalize on this opportunity.

The Elephant in the Room

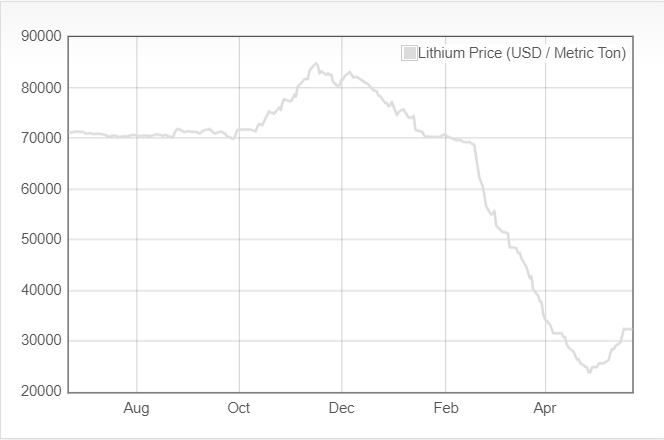

There is no doubt the market growth needed to meet global demand creates excellent upside potential. That being said, the valuation of LAC and competitors is and always will be tied to the price of lithium. Lithium has been on a wild ride this past year being one of the most volatile commodities over that period. This price action is the leading argument for bearish sentiment in the stock and is the reason LAC is down nearly 50% off of the highs.

www.dailymetalprice.com/metalpricecharts.php?c=li&u=kg&d=240

{kind=link}

With the rapid fall in price, it's easy to wonder if 30k/ton will hold and if it is a fair baseline to use for forecasting revenue. We do not see this as a dead cat bounce. There are several geopolitical, supply chains, as well as a pandemic that became macro factors that lead to lithium's parabolic rise and fall over the past 2 years. The headwinds of lower EV sales and expected higher inventories in the next few years have caused an overcorrection in our view, we see the bounce off ~24k as price stabilization. More forward-looking, the price is now in range for our consensus average of $31k for the year. We believe with production increasing and steady growth in (EVs) average lithium price with a stay between 31k - 37k per ton into 2028.

Valuation Analysis

Contrary to our peer analysts we see the price of lithium as a major bull factor. Currently analysts are for LAC's internal finance team and our peers are using $24,000/ton as the average rate over the lifetime of the mine. We see this as far off. With high inflation, global economic slowdown, and recessionary concerns it makes sense that demand has cooled off in the past year. That being said demand will not stay at the current levels as nations push for (EVs) and green energy. Furthermore LAC will not start production until Q1 2024 and won't reach peak production until 2029 so the current dip and macro conditions do not change the prospective future cash flows. For revenue forecasting, we used an average price of 31k growing 3.6% annually. Further out we believe demand will continue to grow faster than production and lead to market shortages where we might see more substantiated price growth.

Target Price and Fair Value

With production not reaching full output until 2029, this is a long-term play. There is room for price to play around leading up to the start of Argentine production next year, in the meantime with the uncertainty of the nuisances behind the separation, lithium prices, and overall macro conditions over the next 3 years. Looking at the end of 2026 this is a company that will be doing just over $2 billion in revenue. To be conservative and account for possible variance in timeframes and cost we take a 10% haircut off that figure. Being that this is a pre-revenue company the easiest method with the least amount of assumptions is revenue multiples. We have bear case as 3x revenue, base as 4x, and bull as 5x. We used industry averages and cut them by 5% to get to these multiples.

| Bull Case |

| Base Case |

| Bear Case |

| 2026 |

| $10.34 billion |

| $8.27 billion |

| $6.20 billion |

| 2029 |

| $24.21 billion |

| $19.37 billion |

| $14.53 billion |

The target is in the market cap of the combined entity as it is not possible to predict how shares outstanding will be divided between the two new entities. Additionally we did a discounted cash flow analysis using our revenue forecast to and cost assumptions to calculate Free Cash Flow as below in millions:

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| 2028 |

| 2029 |

| 2030 |

| 2031 |

| 2032 |

| $10.4 |

| $154.1 |

| $159.7 |

| $268.8 |

| $399.9 |

| $532.8 |

| $727.4 |

| $822.0 |

| $871.1 |

| $940.8 |

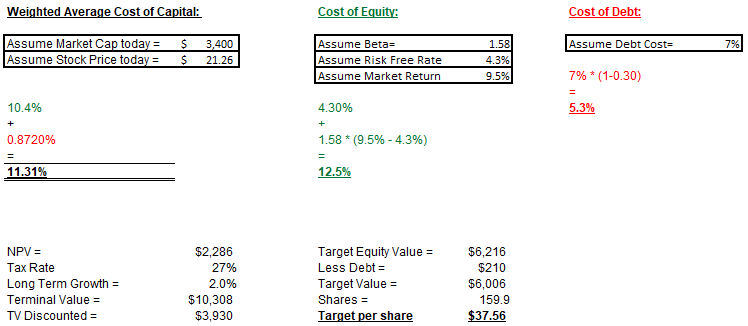

We calculated WACC ourselves as shown below. Tax rate is a conservative estimate, currently LAC does not have income so they have no historical tax rate we can use.

{kind=link}

Comparatively the consensus among analysts is a mean 12 month price target at a market cap of $5.79 billion with a buy rating.

Risk Exposure

We see exposure in three places for LAC. One is the uncertainty of the new capital structure and how the shares will be split post-Separation. Two is the chance of geopolitical issues in Argentina such as changes in export tariffs, environmental regulations, or mining laws could have a substantial impact on LAC's profitability and operational efficiency. As well as issues with China as they are a significant player in the lithium market, and any changes in its policies or economic conditions could impact lithium demand. As mentioned before, Chinese company Ganfeng Lithium owns a significant portion of the operations in Argentina. Beneficially, risk one is a precautionary measure for risk two. By separating the Argentine mines into a new company it prevents Ganfeng from interfering with the North American business. Overall, I think this current situation is being played well by the board and we anticipate the terms of the deal to not be compromising financial sanctity of the business. Lastly, the greatest risk is in the value of lithium dropping further lowering future revenues. Though unlikely a drop in price to $16k for example could cut forecasted revenue in half. That being said, we stand by our price analysis above. Additionally any short term drop in price will not affect the ability of LAC to finance construction as they have built their financing models on a price of 24k which we are comfortably above.

Conclusion

Lithium Americas Corp. is strategically positioned to capitalize on the burgeoning demand for lithium, with substantial developments in its production capabilities. With a 12-month target valuation of $6 billion we rate LAC as a buy. This is a strong mid-term growth stock that can be DCA'd over the next 6 months. Its revenue potential to the current market cap of $3.6 billion is enticing and investors may want to consider Lithium Americas Corp. for its promising growth trajectory and commitment to meeting the needs of the global lithium market.

For further details see:

Lithium Americas Corp.: Navigating A New Era Of Lithium Production Amid Global Demand