CA - Lithium Americas: Here Comes The Lithium Bull

2023-03-09 00:32:40 ET

Summary

- Lithium Americas is preparing to cement itself as a lithium producer starting in 2023.

- Significant project funding and strategic partnerships have been secured.

- The company’s path towards growth and asset development has started to materialize as of the start of this year.

- The company’s 5-year outlook appears extremely positive and share price has significant room for growth.

It has been a few months since we last took a deep look at Lithium Americas (LAC). In that time, multiple news releases have covered the company’s announcement page that provide a clearer picture for what lies ahead:

- Lithium Americas to Acquire Arena Minerals

- Lithium Americas receives favorable ruling on record of decision for Thacker Pass

- Lithium Americas announces initial closing of $650 million investment from General Motors

- Lithium Americas commences construction at Thacker Pass

Things appear to be looking up and with the Cauchari-Olaroz mine getting ready to turn on later this year, the company will also have a consistent revenue stream to help accelerate future growth plans. Good news is great to hear, but stock appreciation is the end game for most investors. Valuing a company is no simple task and there are arguably multiple ways of doing it. The question becomes; “how does this news and future growth materialize into potential stock price appreciation?” Many articles have been written that highlight the “who” and the “what” LAC is and does. This article will focus on the valuation aspect by looking at the company’s assets and future earnings potential to understand how LAC will achieve becoming a top contender in the lithium mining space.

It should go without saying, but we are not financial advisors. Our model and predictions are based on our own research and assumptions. This is not financial advice and is purely our opinion. Now that the formalities are out of the way, let’s move to the fun part.

Question 1: How does the potential upcoming stock split impact the future value of the company?

While we are aware that LAC will separate into a North America and South America division at some point in the future , holders of LAC stock at the time of the split will receive shares of each company. Like most investors, people want to know what is the company worth at some point in the future? To simplify things, we have evaluated the sum of LAC’s current assets as of Q1 2023. The split will separate these assets; however, investors will still hold them in the form of two separate companies. How those future companies are valued, post-split, is a question for the bankers and the LAC Management team. For the sake of this article, we will focus on the combined assets and combined earnings potential.

Question 2: What does a potential milestone timeline look like for LAC?

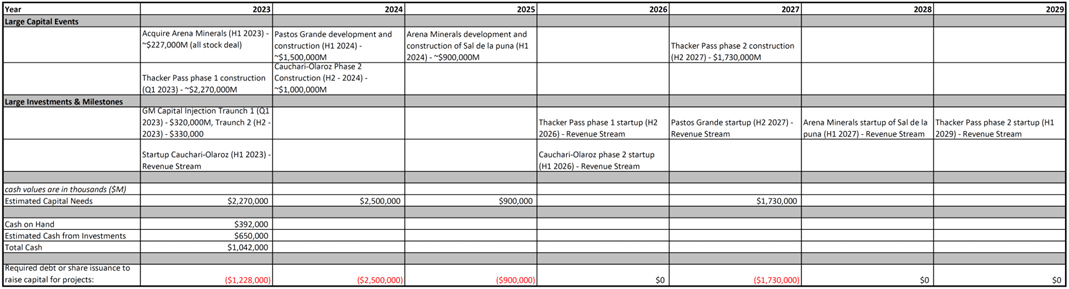

No model is perfect, but one needs a starting point to begin an evaluation. Let’s take a look at the below table to review potential project timelines and when certain sites could realistically come online. We are assuming that once Cauchari-Olaroz starts up and revenue starts coming in, this will serve as a catalyst for getting the next mine(s) developed and construction started. No one wants to be last to the lithium party. LAC has the assets in hand, it is just a matter of time and capital to develop and finance them.

{kind=link}

New construction takes a lot of time and money to get a plant operational. These are complex integrated systems that require a significant amount of time, engineering, patience and you guessed it, money! As confirmed in LAC’s most recent feasibility study for Thacker Pass, and to many people’s surprise, the costs of developing a mine have practically tripled since the previous study. For the sake of our modelling efforts, we made an educated guess for the development and construction costs of Arena Minerals' Sal de la Puna and Pastos Grande projects. However, I would anticipate a feasibility study in the next year to provide much clearer guidance. We have tried to estimate conservatively high for the sake of modelling.

The key take away from the above table is LAC needs a lot of money in the next few years that won’t come from its Cauchari-Olaroz operations. They will be forced to take on debt or issue more shares to raise capital. Our model considers both of these occurring in some fashion.

Question 3: How expensive is it to build a lithium mine?

One thing is for certain, to make money you need a product. LAC has it in the form for lithium, however they need to extract, process and purify the substance before money can be made. In order to reach this point, money is needed to facilitate the investment and development of their assets. A lot of money.

Based on the most recent Thacker Pass Feasibility Study results, the total price to develop Thacker Pass (phases 1 and 2) has increased from ~$1.2 Billion to a staggering ~$4 Billion USD. LAC has not yet announced or disclosed an updated feasibility study for its Pastos Grande asset, or its soon to be acquired Arena Minerals Sal de la Puna asset, however have assumed there will be a similar 3x price spike. For reference, Pastos Grande previously had a price tag of $448 million. The point is, there is a lot of capital that is needed to build out and develop these assets.

Fortunately, LAC has been preparing for this eventuality. The following press releases confirm that funding, through outside investment and government issued debt, is being secured to press on with the development of the company’s lithium projects.

- Lithium Americas Receives Letter of Substantial Completion for Application to U.S. DOE ATVM Loan Program

- Lithium Americas announces initial closing of $650 million investment from General Motors

While I doubt the two (2) most recent announcements will secure all of the funding needs for the company's assets, it is a great start. The remainder of the money needed can later be sourced through issuance of shares or the taking on of debt.

Question 4: How do Questions 2 and 3 factor into a potential model for valuing a company?

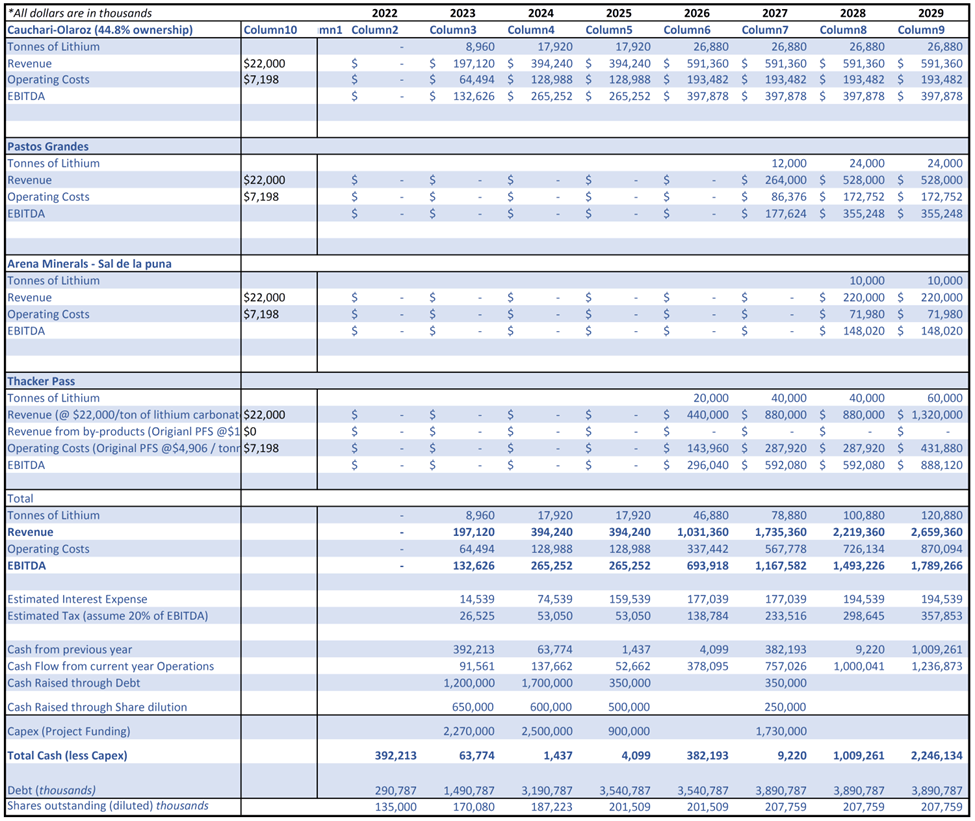

Moving onto the actual modeling portion, I want to layout a few assumptions. Using the most recent feasibility study from Thacker Pass will serve as a good conservative estimate. Our goal is to model things conservatively (estimate revenue slightly lower and the expenses slightly higher). If the model yields a good result (i.e. a higher future share price), then we know there is serious potential for this to be a great investment.

Some key assumptions we have made in the formation of our model:

- Pastos Grande development costs ~$1.5 billion (estimated based on previous price tag of $448 million and adjusted upwards based on Thacker Pass price tag adjustment factor in most recent feasibility study)

- Arena Minerals development costs ~$900 million for Sal de la Puna project (estimated based on Pastos Grande adjusted price tag and scaled down based on smaller LCE production estimate)

- Arena Minerals (Sal de la Puna) production estimated at ~10,000 tpa LCE (estimate based on March 2021 press release )

- Cauchari-Olaroz phase 2 development costs ~$1.0 billion (estimate)

- All mine sites are developed and come online as projected in Table 1

- All LCE from all sites is sold at $22,000 / tonne of LCE

- This assumes a $2,000 discount from the Thacker Pass Feasibility Study sale price of $24,000 / tonne of LCE. We do not know how the South American Lithium will sell and therefor have attempted to be conservative

- All expenses have been elevated to $7,198 / tonne of LCE based on the Thacker Pass Feasibility Study

- Estimated yearly interest expense will be 5% of the total debt outstanding (similar to other mining companies)

- Estimated yearly taxes of 20% of EBITDA (estimated in an attempt to account for some form of taxation not accounted for in the “Expense category”)

- Annual Cash Flow from operations has been considered within the model

- Cash raised through debt sourcing and cash raised through share dilution has been arbitrarily selected to balance the cash required for Capex (Project Funding)

- This ensures “Total Cash” doesn’t go negative as the company must be able to fund future projects

{kind=link}

To summarize some of the results from our model:

- Debt and share dilution will be the primary sources of raising capital until additional mines come online (estimated to occur in 2026 – 2028)

- Once additional mines come online throughout the 2026 – 2028 time period, the company will have a significant source of EBITDA (>$1 billion) and become self-sustaining from a cash standpoint

- After additional mines are constructed and come online, the company will have the potential to pay down debt and buy back shares (not currently modelled)

While no model is perfect and relies on many assumptions, we are able to develop a rough picture of what LAC's future production, income, expenses, shares outstanding and future debt loads could look like. Given this picture, and the projected mine startups, it’s clear to see that after the 2026 - 2028 timeframe the company really begins to pick up speed in terms of production and cash generation.

Question 5: What is LAC's future price tag when valued against its future competitors?

In my previous article, I briefly explained how and why we chose to value LAC against its future competitors. It’s critical to consider what LAC looks like years down the road after it is a developed lithium miner. Currently, there are a few companies who are existing and offer us a glimpse of how Mr. Market currently values them based on their enterprise value to revenue ratio and their enterprise value to EBITDA ratio. These ratios consider how much the company makes in terms of annual revenue and annual EBITDA and then compares that against how much the company is worth when considering the share price, # of shares outstanding , cash and debt (i.e., the enterprise value).

The below table shows a snapshot of these key ratios for some of LAC’s future competitors.

| as of Q1 2023 |

| EV/Revenue |

| EV/EBITDA |

| ALB |

| 10 |

| 28 |

| LTHM |

| 16 |

| 40 |

| RIO |

| 2 |

| 5 |

| SQM |

| 8 |

| 16 |

| Average |

| 9.0 |

| 22.3 |

| LAC future Ratio (discounted by 25%) |

| 6.8 |

| 16.7 |

Table 3: Key Valuation Ratios for Competitors and LAC Future discounted Ratios

Ultimately, what we are looking for is a future stock price estimate based on the model’s inputs. What we can see is there are some competitors in the mining space who can help us gain an idea of a future EV/Revenue and EV/EBITDA ratio for LAC. Averaging the above ratios, and applying a 25% discount for being conservative, we can estimate LAC’s future ratios. From this point, it is simply a process of plug and chug given the known variables to arrive at a future share price estimate for the stock given each year’s numbers. For those who aren’t familiar with the calculation, the below equations have been considered:

EV/Revenue equation rearranged for share price calculation (Investopedia)

EV/EBITDA equation rearranged for share price calculation (Investopedia)

Using the above equations and using the plug and chug method for the known variables in Table 2, we can estimate what the future share price of LAC could be at various points in the future.

{kind=link}

Considering a 5-year outlook, we believe LAC should be within the $58 - $105 share price range. This is dependent upon LAC achieving certain milestones as outlined in Table 1 and meeting the previously estimated revenue and EBITDA values outlined in Table 2. We have done our best to remain conservative within our model. Given the estimated prices, we feel confident in the future potential of LAC as a company.

Risks

In our opinion, LAC is a semi-speculative lithium mining play. Speculative in the sense there is significant potential to become an establish lithium miner, however they must achieve certain milestones and continue to progress forward with their plan. The company is gearing up to start one of their mines (Cauchari-Olaroz), which absolutely makes them more established than some joe-blow who drills a hole and says, “I’ve got lithium”.

In addition, looking at the broader picture, Goldman Sachs has come out and stated they think the lithium market will cool off significantly. This is a staunch contrast to what many in the lithium space are looking at given the projected supply and demand imbalance leading up to 2030.

If LAC is unable to deliver on their goals and develop their projects, I would expect a negative response from the market. In addition, if the global lithium market were to be disrupted, I would expect an equally negative market response and potential for delays.

Conclusion

We purchased LAC back in 2019 under the assumption that it is a long-term value play (5 – 7 years). We don’t try to time the market, rather we attempt to find solid companies that will be around for a long time and produce sustainable income and growth. While certain milestones and projects have been delayed due to legal proceedings, we still maintain our bullish stance and plan to maintain our position in LAC as the future projects unfold. We are excited to see how the lithium markets develops over the next 5 - 7 years and plan to add to our positions during market pullbacks.

For further details see:

Lithium Americas: Here Comes The Lithium Bull