CA - Loblaw: Cheap Growing E-Commerce And Double Digit Adjusted EPS Growth

2023-10-04 16:43:21 ET

Summary

- Loblaw Companies reported double-digit adjusted EPS growth and a 13.9% increase in e-commerce sales in Q2 2023.

- The company's business model includes retail stores, pharmacies, and the PC Optimum program for financial services.

- Loblaw expects further acquisitions, investments in digital retail, and data-driven insights to enhance FCF growth and improve operating margins.

Loblaw Companies Limited ( LBLCF ) delivered impressive outlook with double digit adjusted EPS growth, and noted that e-commerce sales increased by 13.9% in Q2 2023. I believe that further investments in digital retail and sufficient use of data driven insights may bring further understanding of consumer behavior, which may enhance FCF growth. There also seems to exist room for new acquisitions like that of Lifemark as the net debt/EBITDA recently lowered significantly. Yes, there are obvious risks from supply chain problems, failed M&A integration, or technological problems, however I believe that the shares are cheap.

Business Model, Recent Quarterly Figures, And Previous Long Term Growth

Loblaw Companies is a Canadian company in the field of health in general and food in particular, which operates through application centers and distribution stores retail throughout the country. The core of the company's business began in 1919 with the retail distribution of food items, fruits, and vegetables to expand into different areas, today being one of the companies with the largest number of employees in Canada, with more than 2,400 stores, dedicated to health, beauty, and food services.

At present, Loblaw's operations are divided into two segments. One segment covers the activity of all retail stores, without differentiating the category to which they belong, made up of stores under their ownership or franchises of their brand, in which they offer food, health, and beauty products, along with the pharmacies where they provide applications of vaccines and medications. The other segment is intended solely for the promotion and operation of its PC Optimum program, in which it offers financial services to its clients, through credit card benefits and day-to-day banking operations.

With that about the business model, I think that it is a great moment to review Loblaw Companies, especially after the recent quarterly reports. Management reported consolidated quarterly revenue growth of about 6.9% y/y and Adjusted EBITDA growth of close to 9%. Additionally, the company reported double digit net earnings per common share growth. I do not expect double digit net income growth in the coming years, but I did positively view the figures reported.

Source: 2023 Q2 Presentation

The numbers reported by the retail food and drug business segments are also quite beneficial. Management reported positive single digit net sales growth as well as increases in the EBITDA margin.

Source: 2023 Q2 Presentation

If this is the first time you are reading about Loblaw, previous annual figures are worth mentioning. The financial results for the last year showed an increase in sales and profits in almost all areas, with a 4.7% increase in retail sales and 5.7% increase in pharmacy sales. We are talking about a company that grows in the long term even if net sales growth is lower than 10%. As shown in the chart below, since the year 2000, shareholders enjoyed FCF growth and net income growth.

Source: YCharts

Expectations From Management And Other Financial Analysts

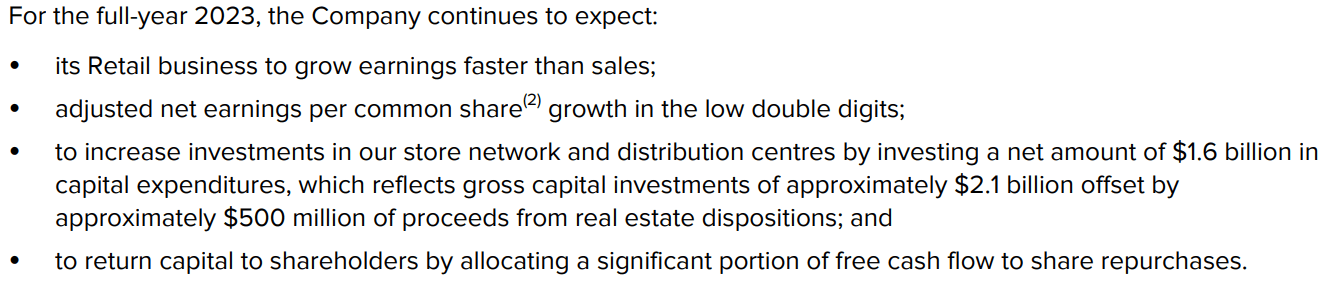

I did run my own financial model of Loblaw, however I believe that investors may want to have a look at the beneficial expectations reported by Loblaw. In the last quarter, management noted that retail business is expected to grow earnings faster than sales.

Besides, Loblaw noted that the adjusted EPS growth could reach the low double digits in 2023, which I believe is quite beneficial given previous financial figures. Additionally, it is also worth noting that the company expects to continue with share repurchases, which, in my view, may bring substantial demand for the stock, and could enhance the stock price.

{kind=link}

I think that the expectations from other financial analysts are also quite beneficial. The market expects net sales growth around 5%-2% in 2023, 2024, and 2025. Besides, with EBITDA/Net Sales close to 11%, operating margin of 6%-7%, and net margin close to 3%, the FCF from 2023 to 2025 is expected to be close to CAD1.85 billion and CAD2.6 billion. I did use some of these figures as a reference, so I think that it is worth having a look at these figures.

Source: S&P

Assets

As of June 17, Loblaw reported cash worth CAD1.2 billion, with short term investments of CAD531 million, and accounts receivable close to CAD1.2 billion. Besides, with credit card receivable of CAD3.9 billion and inventories of CAD5.5 billion, total current assets are equal to CAD13 billion. The current ratio is larger than 1x, and Loblaw reports cash in hand, so I think that liquidity does not seem like a problem here.

Long term assets include fixed assets of CAD5.7 billion, with right-of-use assets close to CAD7.4 million, intangible assets of CAD6.2 billion, and goodwill of CAD4.3 billion. Total assets stand at about CAD38 billion, and the asset/liability ratio is equal to more than 1x, so I think that the balance sheet appears quite solid.

Source: Quarterly Report

Liabilities

Loblaw does not report a lot of liabilities, and long-term debt appears quite limited. If we assume an EBITDA of CAD7 billion, the total amount of long term debt is not far from 1x EBITDA. Besides, the largest liabilities include trade payables worth CAD5.7 billion, with short term lease liabilities of CAD1.4 billion, and long term lease liabilities close to CAD7.7 billion. Total liabilities are equal to CAD26 billion.

Source: Quarterly Report

Considering the total amount of liabilities and debt, I would say that Loblaw could receive more debt to make new acquisitions. In the past, the company reported a financial debt/EBITDA of close to 4x right after two acquisitions made in 2014. According to YCharts, the financial debt/EBITDA is close to 1.3x.

Source: YCharts

We Can Expect Further Acquisitions Like That Of Lifemark, Which May Bring FCF Margin Improvements

Taking into account the current level of net debt/EBITDA and the acquisition of Lifemark reported in 2022, I think that we may see further inorganic growth in the coming years. Lifemark was bought for CAD829 million in cash. In order to reach a debt level of 4x EBITDA, Loblaw could acquire many more targets. In the best case scenario, the market may appreciate the acquisitions and the synergies expected.

Source: 2022 Annual Report Source: 2022 Annual Report

Investments In Digital Retail, Leveraging Data Driven Insights, And Connected Healthcare Will Most Likely Bring Operating Margin Improvements

For the immediate future, the company will focus on three key drivers: generating excellence in its retail operations, driving growth, and achieving investments in key areas. In the last annual report, the company noted investments in digital retail, payments and rewards, and connected healthcare. In my view, these investments may bring a significant amount of data from consumers, which may enhance the design of market campaigns.

Enabling these investments comes from a sharp focus on leveraging data driven insights and process efficiency excellence to deliver strong financial performance. The framework is supported by colleagues with a shared set of CORE values and culture principles that encourages colleagues to be authentic, build trust and make connections. Source: Source: 2022 Annual Report

More in particular, the company’s objective is to adapt to the uncertain economic conditions of the global economy, developing both its retail segment and the financial service through PC Optimum. With e-commerce sales increasing at a double digit and beneficial commentary about the performance of the PC OptimumTM Program, I really believe that Loblaw is going in the right direction. The following are comments from the recent quarterly release.

E-commerce sales increased by 13.9%. Source: Q2 2023 Press Release

Our discount offering, best-in-class control brand products and PC OptimumTM Program are resonating with customers who are looking for value without sacrificing quality. Source: Q2 2023 Press Release

The Stock Repurchase Program Will Most Likely Have A Beneficial Effect On The Stock Price

I expect that Loblaw will most likely continue to achieve capital remuneration for investors and shareholders by making a large amount of money available from its liquidity to generate share repurchases. In the last quarter, the company noted stock repurchases of close to $511 million, which, I believe, is a massive amount, and will most likely have a beneficial effect on the stock price of Loblaw.

Repurchased for cancellation 4.2 million common shares at a cost of $511 million. Source: Q2 2023 Press Release

My Financial Model Included Upside Potential In The Stock Price

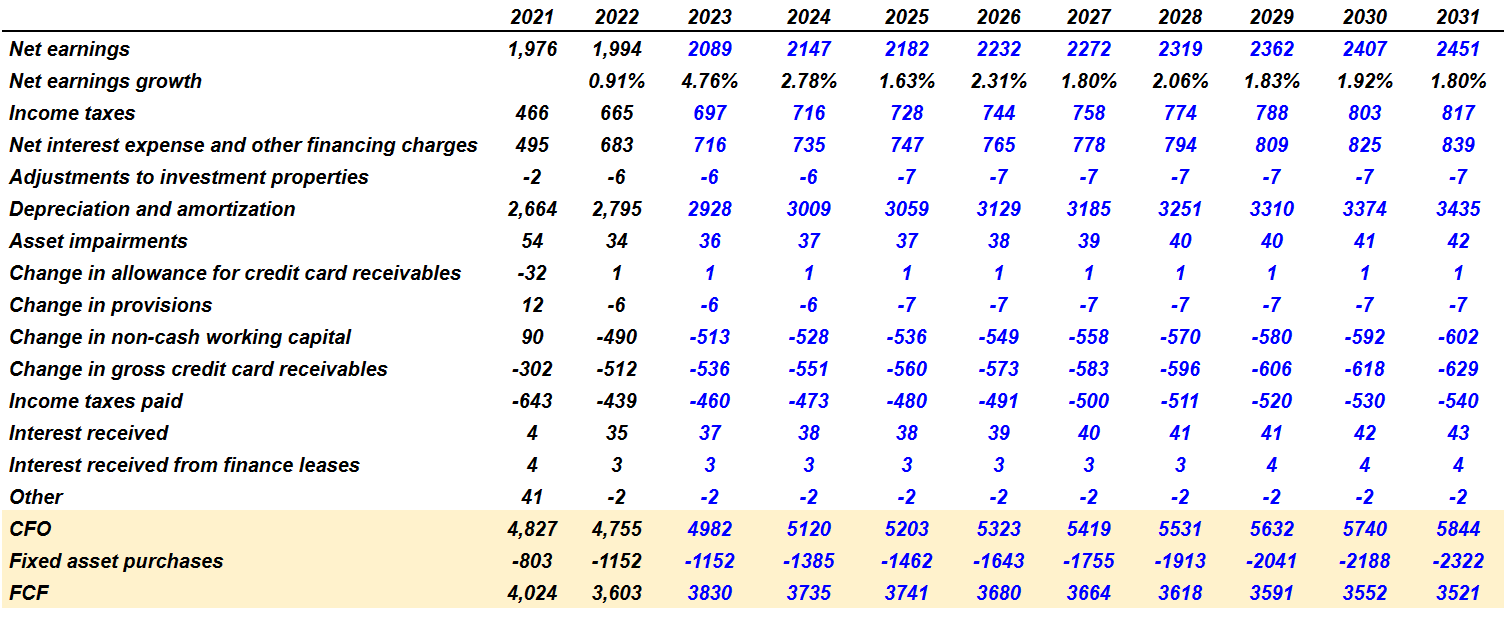

For the assessment of future cash flow statements, I had a look at previous financial figures, and included my previous assumptions. I really believe that my figures are very conservative.

Source: YCharts

Assuming single digit net income growth from now to 2031, I obtained 2031 net earnings of close to CAD2.450 billion, income taxes close to CAD817 million, net interest expense and other financing charges of close to CAD839 million, and depreciation and amortization of CAD3.434 billion.

Also, with change in provisions of close to -CAD8 million, change in non-cash working capital worth -CAD603 million, and change in gross credit card receivables of -CAD630 million, I also included interest received from finance leases of about CAD3 million. Besides, I obtained 2031 CFO of close to CAD5.843 billion and 2031 FCF of close to CAD3.521 billion.

{kind=link}

With a CAPM model that includes a selected beta close to 0.79, cost of equity of 9.4%, and cost of debt after tax of about 5.2%, I obtained a cost of capital close to around 7%-8.3%.

Using a WACC of 7.4% and a terminal EV/FCF of 19x, I obtained a total enterprise value of CAD58 billion and an equity value close to CAD51 billion. In sum, the implied price obtained is close to CAD164 per share, and the IRR would be around 5%-6%.

Source: DCF Model

Competitors

The retail industry in Canada is highly competitive, and is made up of a few national companies, such as Loblaw, and a large number of stores and distribution centers with regional reach. In this sense, Loblaw has a strong geographical footprint that allows 90% of the population to be less than 10 km from some of its stores.

Additionally, in some cases, competition also exists from wholesale distribution centers or retail e-commerce channels. The industry is not consolidated, and a large number of competitors are expected to enter in the future, along with increasing competition from companies developing their own trade channels. In this sense, Loblaw generates strategies to approach and retain its customers such as promotions, purchase cards, loyalty programs, and other activities of this type.

Risks

Firstly, in the context of an uncertain economy at an international and domestic level, any complication in distribution logistics, supply chains, variations in transportation prices, or dependence on third parties for access to products are risk factors in an operational sense for this company. Likewise, a sudden increase in the purchase and sale price of the products it distributes would generate financial complications for the company.

Furthermore, due to the activity of the financial services segment, the company is exposed to a series of risks in relation to these instruments, with regard to operations within that segment and the relationship they have with its financial activity. In this sense, any complication in relation to debt payments as well as access to credit lines in general can directly affect not only the financial results of the company but also part of its operating results involved within the segment in question. Ultimately, the company depends on the operation of critical technology for the development of its electronic commerce as well as the development of strategies for the launch of products and its relationship with customers.

Conclusion

Loblaw Companies recently delivered impressive quarterly earnings including double digit net earnings per common share growth, and noted that adjusted EPS growth could reach the low double digits in 2023. Also, with e-commerce sales increasing by 13.9%, investments in PC OptimumTM Program, and digital retail, data insights could bring even more understanding of client behavior. Additionally, I believe that further acquisition of shares via buybacks will most likely enhance stock price increases in the coming quarters. I did see risks from M&A integration, failed M&A, or supply chain issues, however I do believe that the shares are undervalued.

For further details see:

Loblaw: Cheap, Growing E-Commerce, And Double Digit Adjusted EPS Growth