CA - Loblaw Companies: Continued Revenue Growth May Not Be Sustainable

2023-03-12 08:43:53 ET

Summary

- Loblaw Companies has continued to see significant revenue growth.

- However, this seems to be driven by higher prices across the food retail segment.

- Additionally, growth across the drug retail segment is showing signs of slowing.

Investment Thesis: I see little upside for Loblaw Companies in the short to medium-term.

In a previous article back in November, I made the argument that Loblaw Companies ( L:CA ) could see a plateau in growth despite impressive revenue growth in Q3. My reason for making this argument was that such growth may have been driven by rising prices as opposed to an increase in organic demand. As such, a plateau in inflation could also lead to a plateau in revenue growth.

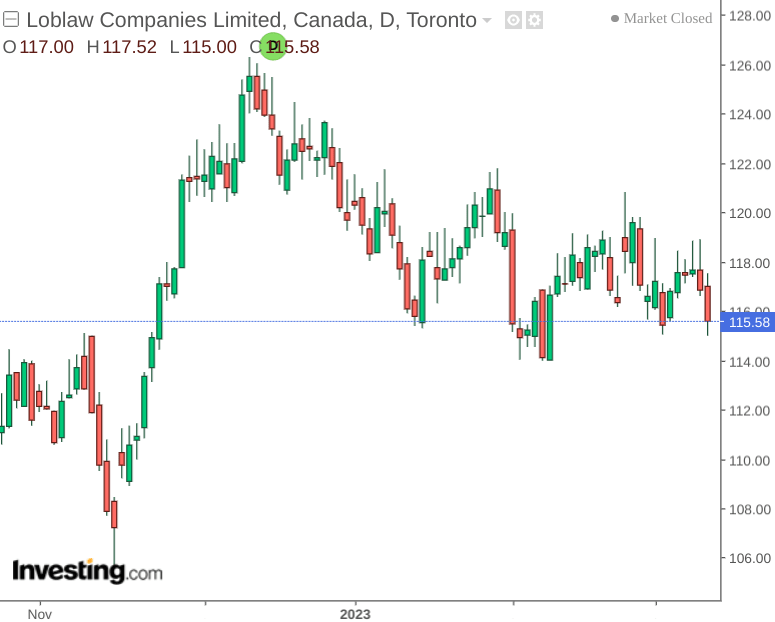

Since then, the stock saw some brief upside, but price is down overall from that of November:

{kind=link}

The purpose of this article is to assess whether the stock could see upside from here on the basis of most recent annual performance.

Performance

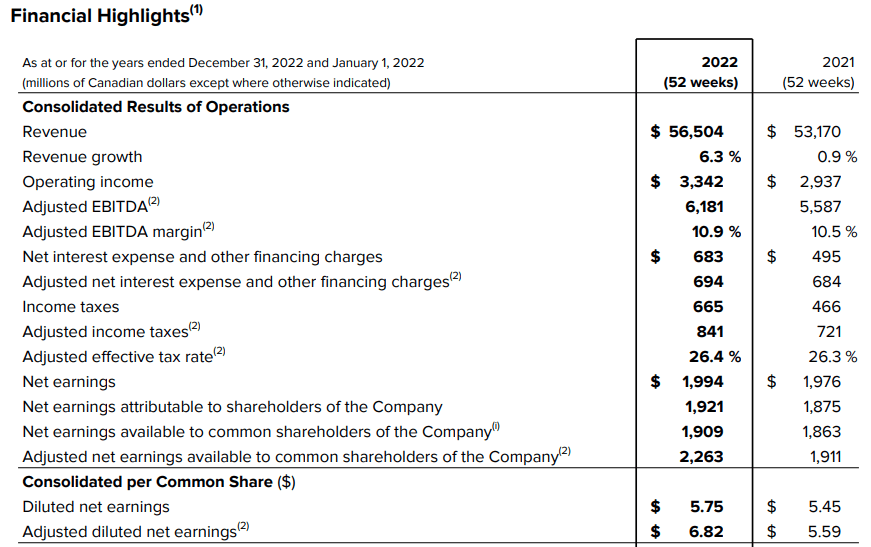

When looking at the company's 2022 annual report , we can see that revenue is up by 6.3% on that of the previous year, while adjusted diluted net earnings is up by 22% over the same period.

Loblaw Companies Limited: 2022 Annual Report

{kind=link}

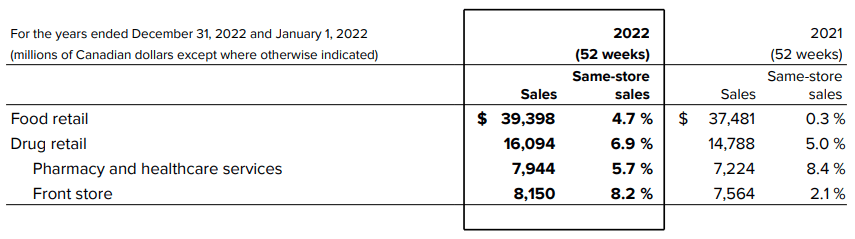

Additionally, we can see that same-store sales (sales excluding that of new outlets or closed stores) are up on that of last year - with growth of 4.7% and 6.9% for the Food retail and Drug retail segments respectively.

Loblaw Companies Limited: 2022 Annual Report

{kind=link}

With that being said, the company also acknowledges that the higher than normal growth we have been seeing across food retail was mainly due to rising prices. As a counterexample, we can see that sales growth for pharmacy and healthcare services was down on the previous year - from 8.4% to 5.7%.

There is a risk that while same-store sales for food retail are showing strong growth on a percentage basis - demand is not keeping up with price growth. This represents a risk in that once price growth starts to plateau - the company will be limited in being able to bolster revenue through organic demand. We could see sales growth drop significantly under such a scenario.

From a balance sheet standpoint, we can see that the quick ratio (calculated as total current assets less inventories all over total current liabilities) has remained virtually constant since October 2021. However, the ratio still remains below 1 - indicating that the company does not have sufficient liquid assets to cover its total current liabilities:

| October 2021 |

| October 2022 |

| December 2022 |

| Total current assets |

| 12010 |

| 13014 |

| 13376 |

| Inventories |

| 5214 |

| 5763 |

| 5855 |

| Total current liabilities |

| 9002 |

| 9709 |

| 10098 |

| Quick ratio |

| 0.75 |

| 0.75 |

| 0.74 |

Source: Figures sourced from Loblaw's 2022 Annual Report. Figures provided in millions of Canadian dollars except the quick ratio. Quick ratio calculated by author.

In this regard, I take the view that investors will increasingly be looking at such balance sheet metrics to determine whether Loblaw's can bolster its cash position given recent growth.

We can see that revenue and earnings growth have both remained solid - but higher inflation also means a higher cost base - which could affect cash flow going forward.

Risks and Looking Forward

In my view, the main risk to Loblaw's at this time is that should prices continue to increase - we could see a situation whereby the decline in demand could offset revenue gains from higher prices.

Additionally, growth across the drug retail segment accelerated significantly during the COVID-19 pandemic as a result of the roll-out of testing and vaccination services. However, with the emergency phase of the COVID-19 pandemic effectively being accepted as over - it is plausible that we may see demand across this segment start to decrease.

This poses a risk for Loblaw's in that continued higher prices could place downward pressure on the food retail segment, while demand across the drug retail segment could also see a concurrent decline.

Conclusion

To conclude, Loblaw Companies has continued to see growth in revenues and earnings. However, stock price has not followed suit and I take the view that investors are concerned as to the viability of revenue growth we have been seeing to date. I see little upside for Loblaw Companies in the short to medium-term.

For further details see:

Loblaw Companies: Continued Revenue Growth May Not Be Sustainable